Capital is betting on card issuance, compliance, clearing and settlement, and enterprise APIs. The benefits of stablecoin payments are shifting from "cards" to the "underlying layer."

Written by: Farmer Frank

Li Lin placed another bet.

On June 3, 2026, WasabiCard, a global stablecoin payment infrastructure platform, completed its Pre-A round of financing. Including its previous early rounds, it has raised nearly $10 million in total funding. Investors include Vernal Capital, Avenir Group, Vision Plus Capital, and 01VC. Avenir Group is Li Lin's family office.

Interestingly, almost simultaneously, another message went viral in social media: Fiat24 suspended new account openings in mainland China, while several crypto payment card services familiar to Chinese users, such as SafePal and Bitget Wallet, have partnerships with Fiat24's card issuance capabilities.

On one hand, capital is pouring into an "invisible" payment infrastructure company, and on the other hand, policy adjustments are directly affecting some front-end card products of underlying service providers . When viewed at the same point in time, this provides a good entry point for re-examining the stablecoin payment track.

Behind the cut is a real demand that is rapidly expanding.

I. The Decline of U-cards: It's not demand that's declining, it's the business model.

According to Fireblocks' "State of Stablecoins 2025" report, 49% of the surveyed institutions are already using stablecoins in payment scenarios, and another 41% are in the testing or planning stage. This means that nearly 90% of institutions have already come into contact with stablecoin payments in some way.

Demand is rising, but the way that meets that demand is changing.

As we all know, the most discussed form of stablecoin payment in the Chinese market over the past few years has almost always been the "U card": users transfer stablecoins such as USDT and USDC into the card product and then use it for online subscriptions, consumption or offline payments. This is also the easiest for everyone to understand and accept.

But the U card is only the visible front end for users.

Behind a card lies a complex web of issues: card issuance qualifications, card organization partnerships, KYC/AML, risk control systems, stablecoin and fiat currency exchange, clearing and settlement networks, merchant channels, and cross-border payment capabilities. However, users tend to remember brands like RedotPay, KAST, and Crypto.com that are directly accessible to users, while institutions like WasabiCard remain relatively unknown.

In fact, thanks to infrastructure companies like WasabiCard, issuing a single card is not difficult today .

Project teams can completely outsource stablecoin redemption, quota allocation, card issuance, and consumption channels to third-party service providers. They only need to brand the product and launch it on the front end. In a sense, this is also an important reason for the rapid spread of U-card products in the past few years.

Therefore, Fiat24's tightening of account opening is just the beginning.

The real problem is that the rapidly expanding consumer-facing USB cards of the past few years are essentially a "light front-end, heavy external dependency" model. They outsource the most difficult aspects, leaving themselves mainly with branding, customer acquisition, and the user interface. While this solves the problem of "spending USB cards," it doesn't solve the problem of "how to sustain this business in the long term, stably, and compliantly."

The contraction or even exit of many front-end card products over the past year has repeatedly demonstrated that relying solely on front-end experience cannot sustain a payment business that can weather economic cycles.

This is crucial.

U-card products can be copied, subsidies can be followed, and users will quickly migrate as rates, risk control, and availability change. What's truly difficult to replicate is the backend capability:

- Can stable card issuance and acquiring partnerships be maintained in multiple markets?

- Can it handle identity verification and anti-money laundering requirements across different jurisdictions?

- Can the consistency of cash flow and information flow be maintained between stablecoin deposits, fiat currency exchange, card spending, and merchant settlement?

- Can a sufficiently mature risk control system be developed for handling abnormal transactions, high-risk addresses, chargebacks, refunds, account freezes, and compliance reviews?

This is also the starting point for the logic of Avenir Group and other institutions betting on WasabiCard— what these institutions are interested in may not be just another crypto card product, but a stablecoin payment business that is moving from "cards" to the "bottom layer".

II. Why did Avenir Group bet on WasabiCard?

Over the past few years, the crypto market has not lacked grand narratives.

From DeFi, NFT, and GameFi to public chains, L2, restaking, and AI + Crypto, industry cycles are often driven by asset prices, token expectations, and liquidity expansion. However, payments have always been a different kind of business. It is not as exciting and it is difficult to create extreme valuation imagination in a short period of time, but it is closer to the real-world transaction needs.

Because as long as a transaction occurs, every specific step—payment, currency exchange, card issuance, settlement, acquiring, and cross-border transfer—has the potential to generate revenue.

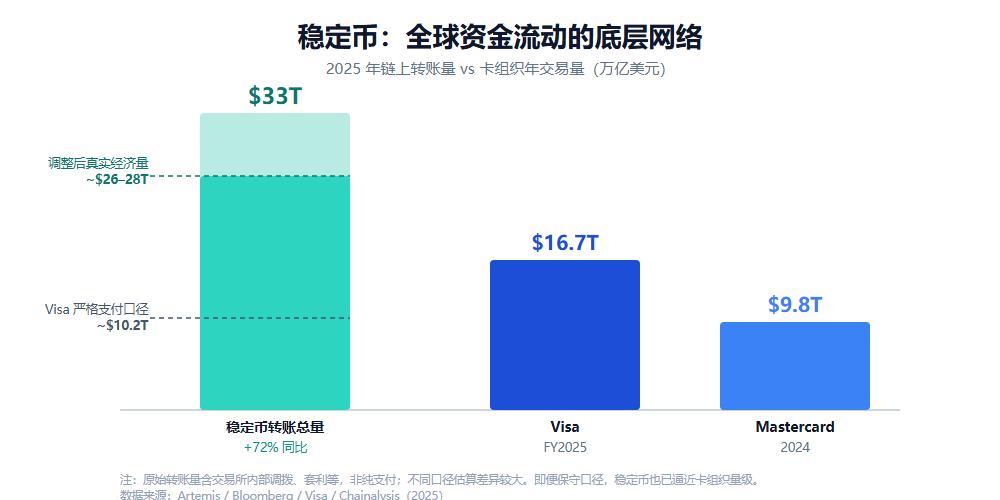

The scale of this business is already considerable. According to Artemis data, the total amount of on-chain transfers of stablecoins worldwide reached $33 trillion in 2025, a year-on-year increase of 72%, exceeding the combined total of Visa and Mastercard. Even excluding non-payment uses such as internal transfers within exchanges and arbitrage, its real economic size is already approaching the scale of traditional card organizations.

Whether these fund flows ultimately correspond to transactions, transfers, or settlements, it means that stablecoins have become an important underlying network for global fund flows. However, precisely because of this, for an on-chain USDT/USDC transfer to truly become a payment that enterprises can use, a salary that employees can receive, a settlement that merchants can accept, or a card balance that users can spend, a whole set of off-chain financial infrastructure is needed to support it.

This is precisely the opportunity for companies like WasabiCard.

They handle tasks that are closer to the "dirty work" or "hard work," such as connecting with card organizations and card-issuing resources, building enterprise APIs, processing fund settlements, managing risk control and compliance, and supporting enterprise clients in embedding stablecoin payment capabilities into their business processes. These tasks do not attract market attention as quickly as issuing a token, but once the capabilities are verified, they may become more reusable.

From a business model perspective, B2B infrastructure and C-end card products are inherently two different businesses.

Consumer-facing (C-end) card products require continuous customer acquisition, subsidies, and user education, while also facing repeated comparisons by users regarding rates, availability, and brand trust. In contrast, once B2B payment infrastructure is integrated by exchanges/wallets, payment companies, and overseas enterprises, it has the opportunity to continuously benefit as the transaction volume of its clients grows. The former is trapped in the cycle of customer acquisition, while the latter is more likely to generate compound interest.

More importantly, once a project team integrates a payment API into its own business, the migration cost will increase, and the cooperative relationship is more likely to deepen around transaction volume, settlement volume and business scale. This is the beauty of the underlying infrastructure: it does not have to outperform everyone else. As long as any of its customers succeed or achieve scale, it can share the growth dividend.

Breaking these down explains why capital is more willing to focus on the lower classes:

- Payment is one of the scenarios where stablecoins can most easily generate real cash flow . Compared to the Web3 narrative that still relies on token cycles and liquidity expectations, it is closer to real transaction needs and is a business model driven by transaction volume and network scale rather than market sentiment.

- Service providers like WasabiCard already have a business and compliance foundation , and have accumulated reusable capabilities in B-end customer relationships and highly compliant systems. For investors, "already integrated" is much more valuable than "planned to be integrated."

- Capital is not buying individual products, but a scalable infrastructure whose growth can be built on customer growth, rather than having to acquire new customers for every order.

For investment institutions, the ceiling of a single-point U-card product depends on how many C-end users it can acquire and the frequency of these users' active consumption; while the potential of a stablecoin payment infrastructure depends on how many enterprise clients it can serve, how many payment scenarios it has, and whether it can become a general capability layer behind more front-end products.

From this perspective, Avenir Group's investment in WasabiCard, rather than being interpreted as some kind of "authoritative endorsement," is more like a directional bet by a shrewd veteran cryptocurrency player on stablecoin payment infrastructure.

Where it points is perhaps more important than the funding itself.

III. Don't compare scale, compare position: Where are the barriers in the B2B market?

Of course, this does not mean that the infrastructure model is inherently easier to succeed. In stablecoin payments, C-end cards and B-end infrastructure are two separate tracks. It is meaningless to compare absolute scale; the key is to look at the position.

Let's first look at RedotPay, the benchmark in the C-end sector. It currently has over 6 million users, covers more than 100 countries, has an annualized transaction volume of approximately $10 billion, and annual revenue of over $150 million. By 2025, it had raised a total of $194 million and its valuation exceeded $1 billion.

It's practically the ceiling that U-cards can reach—but what's intriguing is that even for such a champion, issuing BINs used to rely on licensed providers like Reap, compliance required connecting to Fireblocks and Sumsub, and cross-border payouts required access to Circle's network.

In other words, the card that is running at the forefront is also standing on a layer of underlying infrastructure.

Looking at BVNK, a "graduate" in the B2B sector, it processes over $30 billion in payments annually, covers more than 130 countries, and holds licenses in multiple locations, including MiCA. It was eventually acquired by Mastercard for up to $1.8 billion, becoming the largest stablecoin infrastructure acquisition to date.

It offers an alternative outcome for this track: instead of vying for end-users, it focuses on developing deep underlying capabilities, continuously refining compliance, and ultimately being absorbed into the global network of giants.

WasabiCard is also on this track. As of this round of financing, the company has officially disclosed that it has served more than 500 enterprise customers worldwide, issued more than 500,000 cards, processed more than $1 billion in transactions, and completed the integration of multiple chains such as Avalanche, Arbitrum, and BNB Chain. Recently, it also joined Circle's partner program.

It integrates card issuance, API, settlement, and payment capabilities into a single interface, focusing on a localization strategy that collaborates with banking institutions in major global markets. It positions itself as an infrastructure company that can "one-click" export global white-label card issuance, API, clearing, settlement, and payment capabilities. The localization strategy allows WasabiCard to leverage local banking capabilities in various regions to compliantly issue cards to local users. Meanwhile, as its corporate clients, they only need to integrate the API once to complete global card issuance with a single click.

More importantly, according to publicly available information, WasabiCard's focus is not just on issuing cards to consumers, but on continuously expanding its global card issuance resources, enterprise payment APIs, global fund distribution (Payout), multi-chain asset access, and compliance system construction. This means that it does not provide a single payment product, but a set of underlying payment capabilities that can be called by different platforms and business scenarios.

So, where exactly is the moat protecting this ability?

The Fireblocks report provides further evidence: when banks and payment institutions select stablecoin infrastructure providers, 41% prioritize "fast and reliable payout" and 34% prioritize compliance . In short, payout and compliance are the two most important factors for companies when selecting a provider, which cannot be replaced by issuing a credit card.

For a representative B2B player like WasabiCard, this means proving that it can do more than just issue cards; it can become a stablecoin payment operating system behind various corporate clients, serving a broader range of internet companies and cross-border business scenarios.

IV. PayFi: When was the "underlying" technology rediscovered?

If the most exciting part of stablecoin payments in the past few years was U-cards, then the next stage that deserves more attention may be PayFi infrastructure.

For a long time, PayFi has been easily simplified to "card issuance" or "cashback on spending," making it look more like a user product track than a financial infrastructure track.

However, in the past two years, the situation has been changing significantly.

The financial infrastructure related to stablecoin issuance, payment, and clearing and settlement has become one of the few assets in the crypto industry that can generate stable cash flow. The PayFi sector, which is tied to it, has also gathered almost all types of players , from native crypto projects, traditional payment giants, stablecoin issuers, exchanges, to dedicated stablecoin public chains, all vying for their positions in their own way.

The most telling evidence is the series of actions taken by traditional payment giants:

- In October 2024, Stripe acquired stablecoin infrastructure company Bridge for approximately $1.1 billion, which was considered one of the largest mergers and acquisitions in the crypto space at the time.

- In March 2026, a year and a half later, Mastercard announced its intention to acquire stablecoin infrastructure provider BVNK for up to $1.8 billion, about $700 million more than Stripe paid that year, setting a new record.

- Around the same time, Visa expanded its partnership with Bridge, which had already been acquired by Stripe, with plans to expand stablecoin-linked cards from 18 countries to more than 100 countries.

- Even earlier, PayPal had already launched its own stablecoin, PYUSD.

When these moves from payment giants, card organizations, and large fintech companies are viewed on the same map, it is no longer an isolated bet by a single company on crypto payments, but rather a preemptive positioning by the entire payment industry around stablecoin entry points.

Because stablecoins have never only impacted the payment experience, but also the deeper profit and power structures in the traditional financial system—it directly relates to who can control the accounts, cross-border channels, and even clearing and settlement in the new era. From this perspective, the giants' initiative to connect on-chain accounts, stablecoin assets, and merchant payment terminals is less about embracing innovation and more about not wanting to be bypassed and left behind in the next round of payment and clearing restructuring.

However, as giants begin to directly compete for the underlying infrastructure, the window of opportunity for independent infrastructure players becomes exceptionally clear—either become an irreplaceable part of the giants' networks, or grow into those networks themselves. After all, regulation and licensing, KYC/AML, card organization cooperation, and localization compliance are precisely the parts that C-end U-card products that relied on traffic and subsidies to grow in the past are most difficult to sustain in the long run.

This also explains why companies like WasabiCard are primarily investing in building a global compliance system, connecting with multi-bank business networks, and upgrading their core clearing and settlement systems in this round of funding. These areas may not seem appealing, but they are precisely the underlying capabilities that stablecoin payments must acquire as they transition from user products to financial infrastructure.

Looking further ahead, PayFi's vision may extend to AI Agent payments. If AI Agents do begin to automate transactions on behalf of users in the future, then payment infrastructure cannot be designed solely around "people." Machines will also need callable accounts, verifiable authorization, controllable limits, auditable transaction records, and the ability to automatically execute small-amount, high-frequency payments within compliant boundaries.

This will complicate the endgame of stablecoin payment infrastructure, though of course, this is still a long-term vision.

But it at least shows that the value boundary of stablecoin payments is far greater than that of a U card.

In conclusion

Encrypted payment cards are certainly a good business.

It connects stablecoins with real-world consumption, allowing users to intuitively experience for the first time that "U can be spent." This is why U Card has quickly broken into the Chinese market and become the most easily understood entry point for PayFi by ordinary users.

But the biggest benefits may not necessarily be found in the card.

In the past, the market was more likely to remember a card, an app, a cashback campaign, or a low-fee entry point. However, as stablecoins enter larger-scale real-world business scenarios, what truly determines the long-term landscape of the industry may be the more fundamental capabilities.

Players like WasabiCard, who operate relatively behind the scenes, may not have been the most familiar names in the Chinese-speaking market in the past. However, stablecoin payments are a slow and intensive business. If they can achieve continuous scale in areas such as compliance, card issuance, settlement, acquiring, cross-border payments, and enterprise APIs, they have the potential to become a model of a key company in the PayFi era.

Returning to the two recent news items mentioned at the beginning, they actually point to the same thing: the competition in stablecoin payments is moving from the "card surface" that users can see to the "bottom layer" that users cannot see.

Therefore, as more and more capital begins to re-examine stablecoin payment infrastructure, this industry may be entering a new phase.