Key points summary

This article was written by Tiger Research . The Lehman Brothers crisis and the Kelp DAO incident exposed the same type of structural flaw: a single shared funding pool architecture can amplify the risk of a single asset, causing it to evolve into a systemic crisis. The traditional financial response is to separate each functional layer of the financial system.

The DeFi ecosystem is moving in the same direction: building a modular architecture with risk isolation at its core.

This transformation accelerated as RWA assets began to flow on-chain.

In a modular architecture, the ability to actually manage the operational layer of the product becomes a key differentiator.

1. Lessons from the Lehman Brothers Crisis

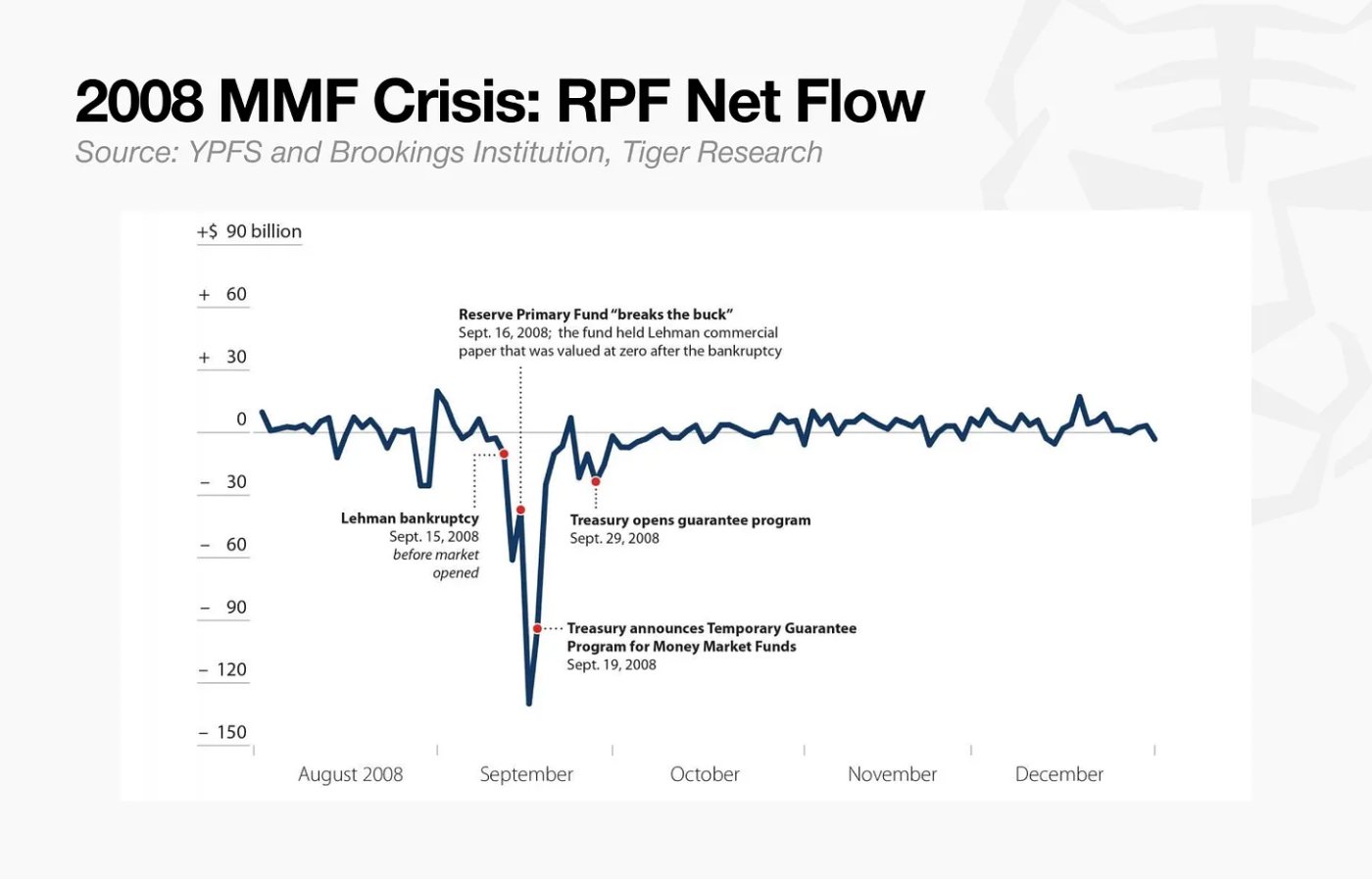

In September 2008, the collapse of Lehman Brothers triggered an unprecedented crisis, and the world's third-largest money market fund, the Reserve Level 1 Fund (RPF), suspended all redemptions within a single day.

At the time, RPF's investment in Lehman Brothers debt accounted for only 1.2% of its managed assets. The collapse of Lehman Brothers rendered this 1.2% of debt unrecoverable, and the fund's total asset value plummeted from 100% of its face value to 98.8%. This was enough to break the fundamental principle of maintaining a fixed net asset value of $1 per share in the money market fund industry. The fund's value per share fell below $1, to $0.97.

Once the principal loss became apparent, panic spread almost immediately. Fearing that waiting would lead to even greater losses, an unprecedented bank run ensued, with redemption requests reaching $40 billion within two days. Unable to withstand such immense pressure, the fund froze its funds and halted all withdrawals.

The Lehman Brothers bankruptcy forced a comprehensive restructuring of traditional capital markets. In the money market fund sector, risk-tiered liquidity buffers and redemption restrictions underwent radical reform. In the hedge fund sector, lessons were learned from the Lehman Brothers re-collateralization risk, namely the centralized custody of client assets by a single prime broker.

As a result, assets and credit are no longer concentrated in a single intermediary, but have undergone a structural adjustment. Separating execution infrastructure from risk management and distributing risk exposure across multiple prime brokers has become the global standard for risk isolation. It is precisely on this institutional guarantee of separating infrastructure from risk to curb contagion that the asset management industry has been able to rebuild operational trust and resume growth.

2. How do traditional capital markets solve this problem?

In 2014, the U.S. Securities and Exchange Commission (SEC) restructured the money market fund (MMF) framework. Funds are now classified according to their capital structure, with each class subject to different standards. This move aims to prevent a run or bankruptcy in one fund class from spreading to other fund types or the entire system, and each fund class has its own dedicated buffer mechanism.

The core concept of traditional financial risk control methods is separation. This involves decentralizing power to prevent risk from concentrating in a single link and introducing independent verification mechanisms at each stage of the money flow.

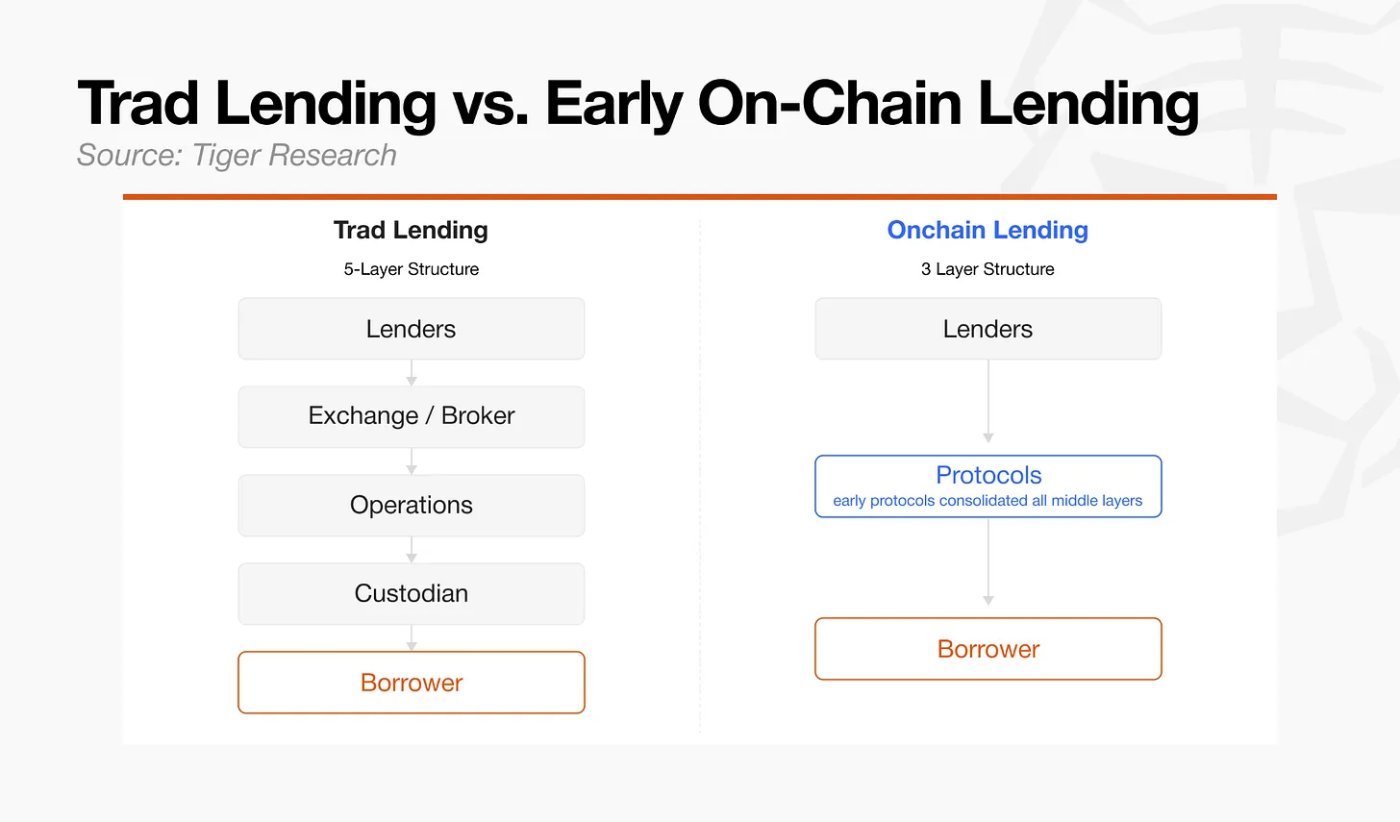

This principle is best exemplified in prime brokerage in the capital markets. Investment decisions are made by hedge funds, while risk management is exercised by brokers. These two functions are deliberately separated. The same logic applies to the traditional lending market: credit assessment, underwriting, collateral management, and custody are handled by different independent institutions.

However, as asset management and lending began migrating to DeFi, the multi-layered intermediary structure of traditional finance was compressed into a single layer. Early DeFi protocols focused on eliminating the intermediaries required for this decentralized structure, directly encoding the relevant mechanisms into smart contracts, and automating processes previously handled by multiple parties.

3. From Shared Pools to Modular Architecture

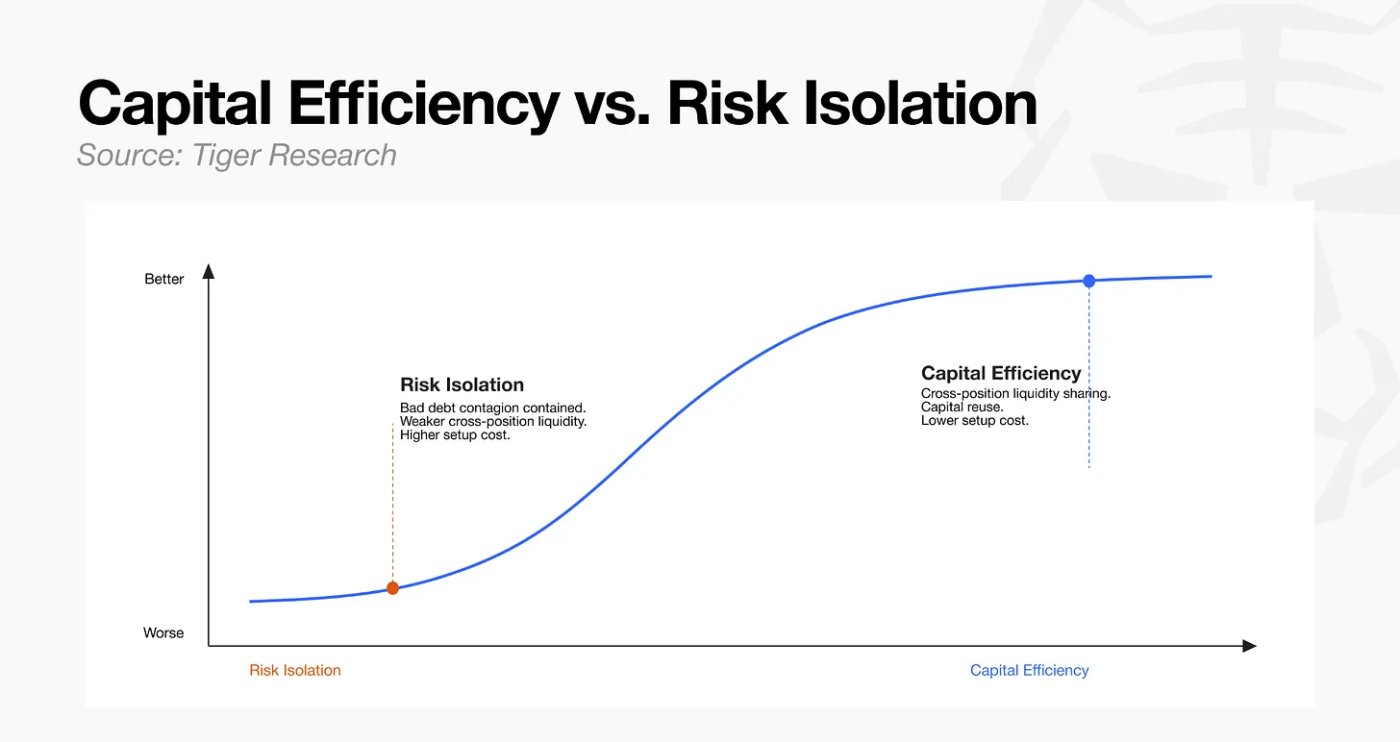

Early DeFi initiatives compressed all lending mechanisms into a single smart contract, reducing intermediary costs but also concentrating all risks in one protocol. Because credit assessment, underwriting, and collateral management all run within the same codebase, rather than as separate functions, defaults or liquidation failures of a single asset could directly paralyze the entire system's liquidity.

This potential contagion risk forces protocol governance to conservatively set risk parameters. Assets with short historical records or high volatility, as well as any asset other than Bitcoin and Ethereum, are structurally excluded from collateral eligibility. Packing functionality into a single contract has ironically led to decreased capital efficiency: asset diversity is limited, and market access is restricted.

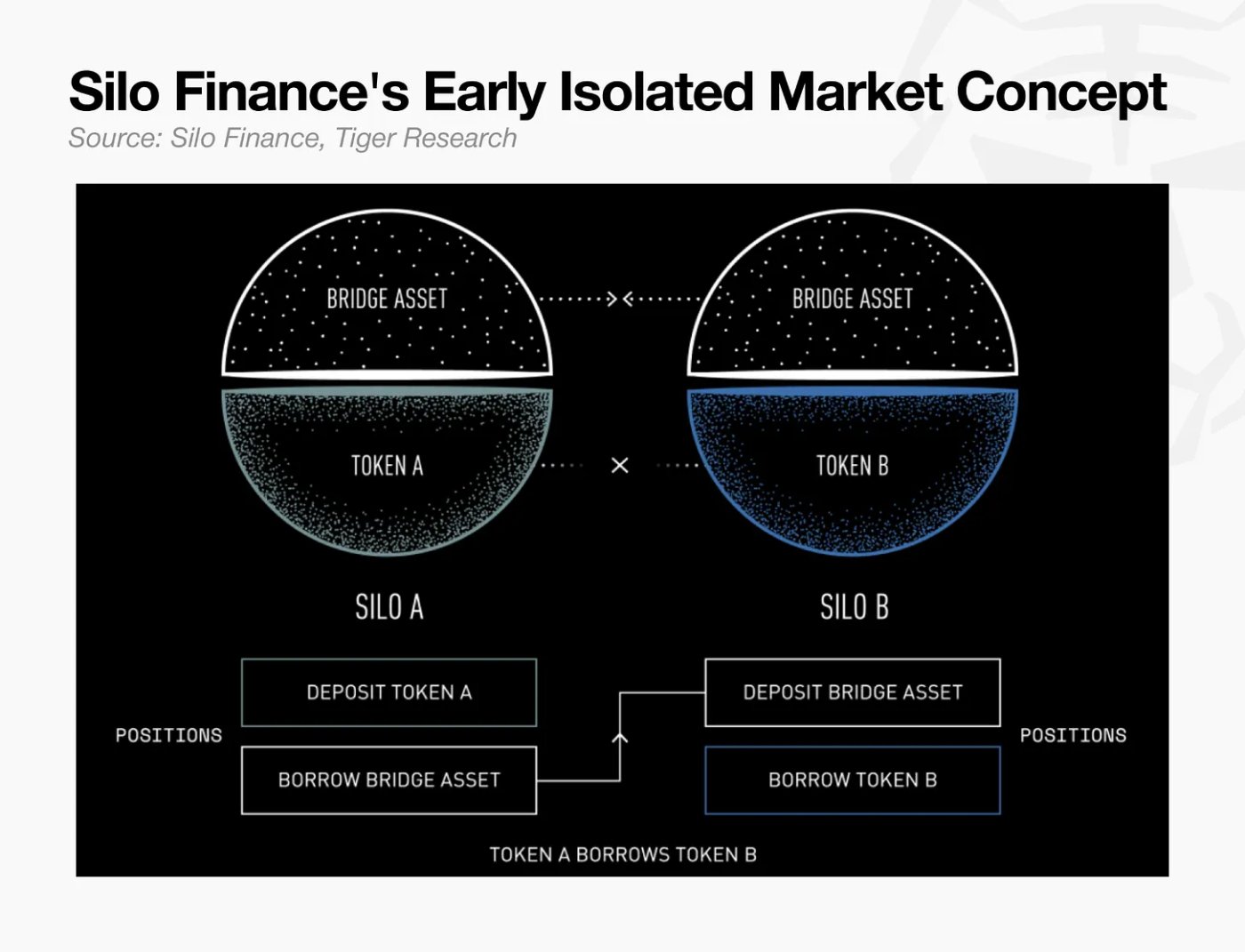

Silo Finance addresses the risk concentration problem of unified asset pools by introducing independent loan pools for each asset. By confining price manipulation or value crashes to a single collateral pool and preventing risk from spreading to other asset pools, Silo demonstrates the ability to lower governance approval thresholds and accelerate the expansion into new lending markets. This architecture shows that a single, large asset pool can be broken down and risk isolated at the market level, while also laying the foundation for subsequent tiered, modular structures.

Silo's pioneering modular system became the foundational standard for on-chain lending as RWA assets, including tokenized government bonds and private lending, began to flow onto the chain in large quantities. Each type of RWA differs fundamentally in terms of transaction timing, oracle reliability, regulatory requirements such as KYC and AML, and liquidation procedures. Early shared liquidity pool models required the use of a single, uniform set of parameters to manage such diverse assets, which was clearly impractical.

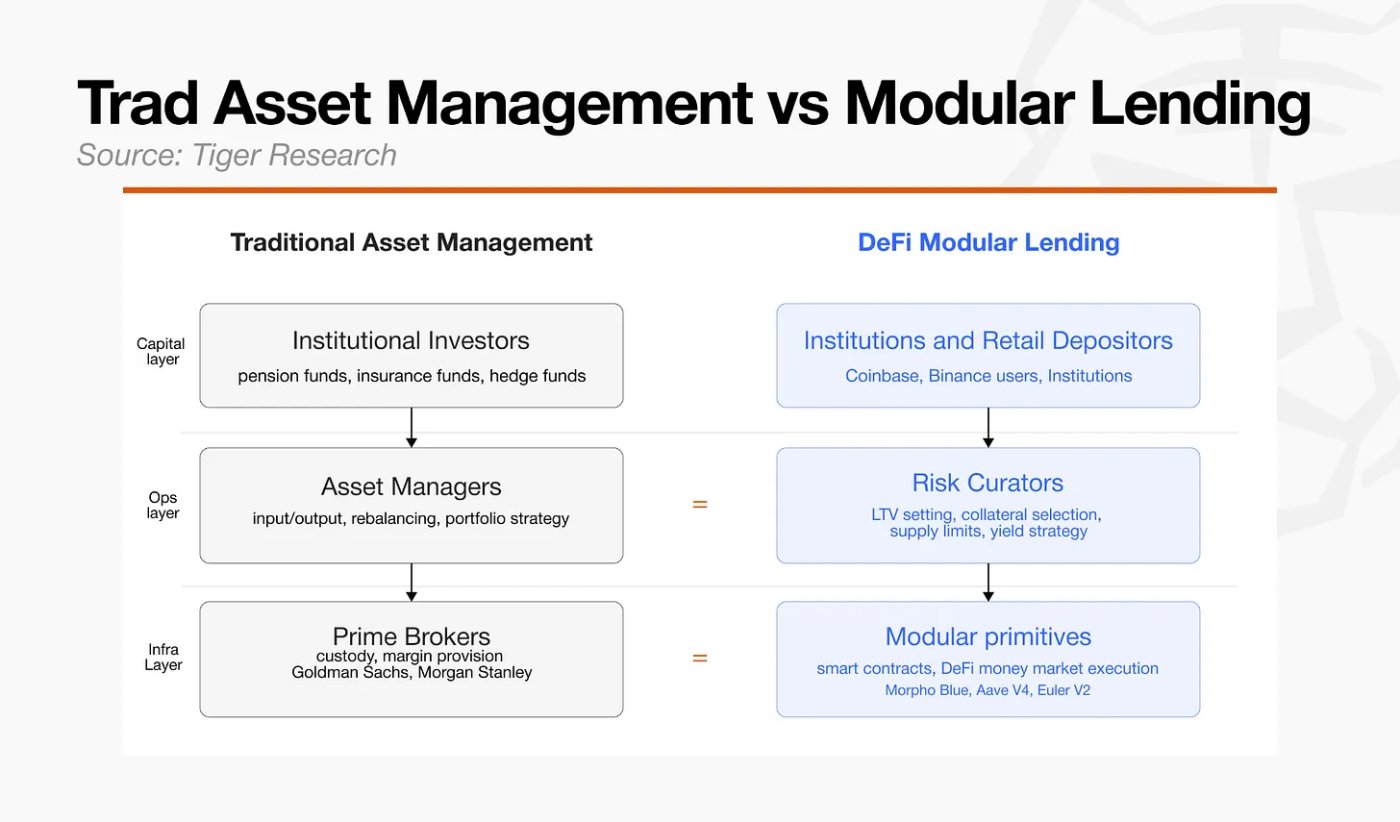

The influx of Real-World Assets (RWAs) has created a need that goes beyond simple asset segregation. It requires migrating the complex risk control frameworks of traditional finance to the on-chain environment. As assets diversify, the risks emerging on-chain also become increasingly complex. To manage these risks, a structural separation is needed: on one hand, an immutable infrastructure layer responsible for clearing and settlement, and on the other hand, an operations layer with real-time permissions to adjust and assume risk parameters.

Early decentralized finance (DeFi) compressed the middleware of finance into a single codebase. With the influx of RWAs and the maturation of the lending market, the development path shifted: clearing and settlement efficiency was delegated to the blockchain, while risk oversight was separated into a distinct tier. To address increasingly complex assets, on-chain lending has ultimately evolved into an architecture similar to traditional financial systems (such as prime brokers and independent credit assessments), where investment and risk monitoring are decoupled. This modular architecture has become the new standard in the on-chain lending market.

4. Institutional-level risk isolation and integration

Although the modular architecture originated in the DeFi ecosystem itself, it happens to meet the risk control standards required by institutional participants.

Morpho's decision to prioritize complete risk isolation at the infrastructure layer, even at the cost of some capital efficiency, spurred institutional demand. This demand became a turning point, prompting other major lending protocols, especially those that initially adopted a shared funding pool structure, to move in the same direction.

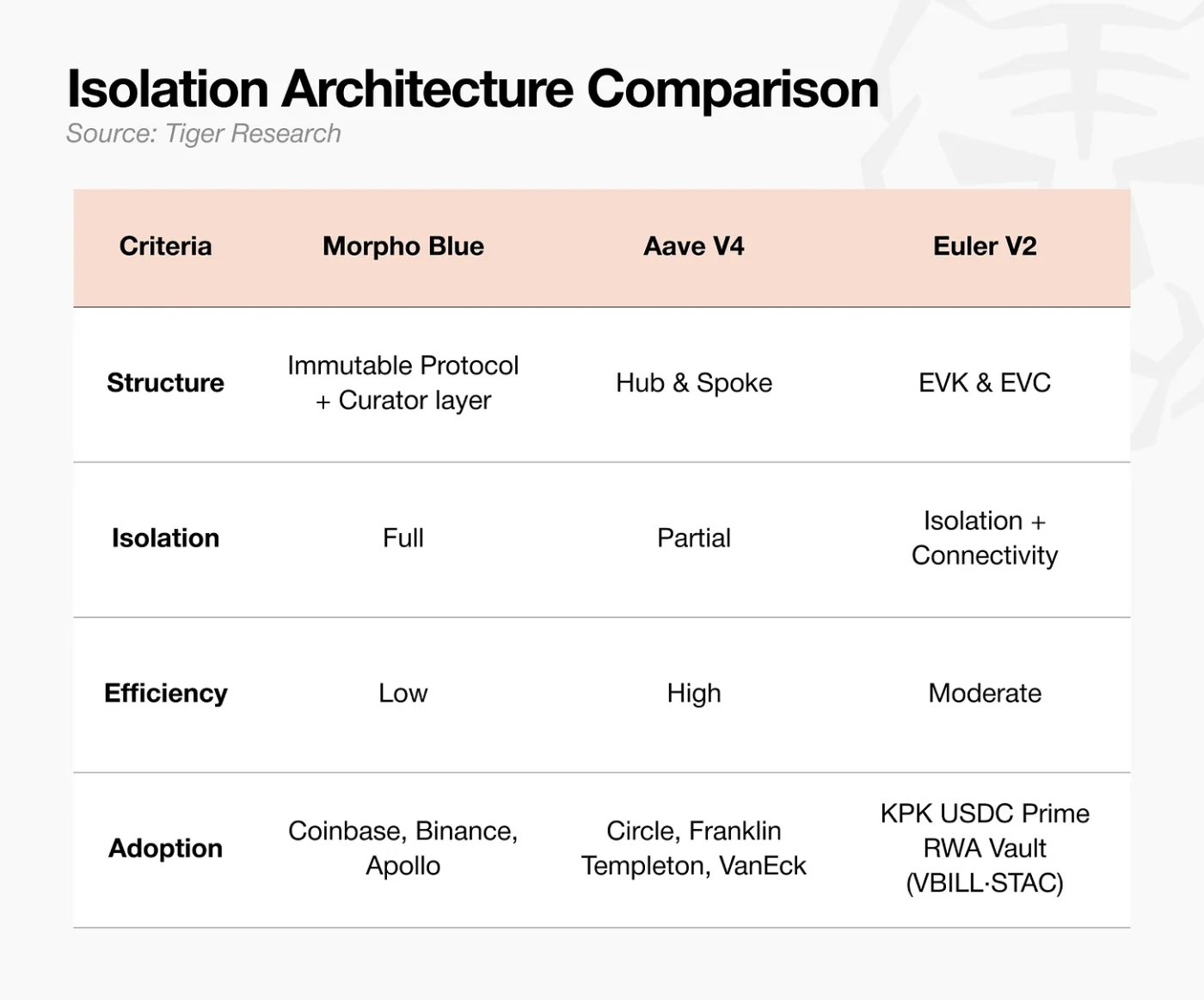

4.1 Morpho Blue: Prime Broker

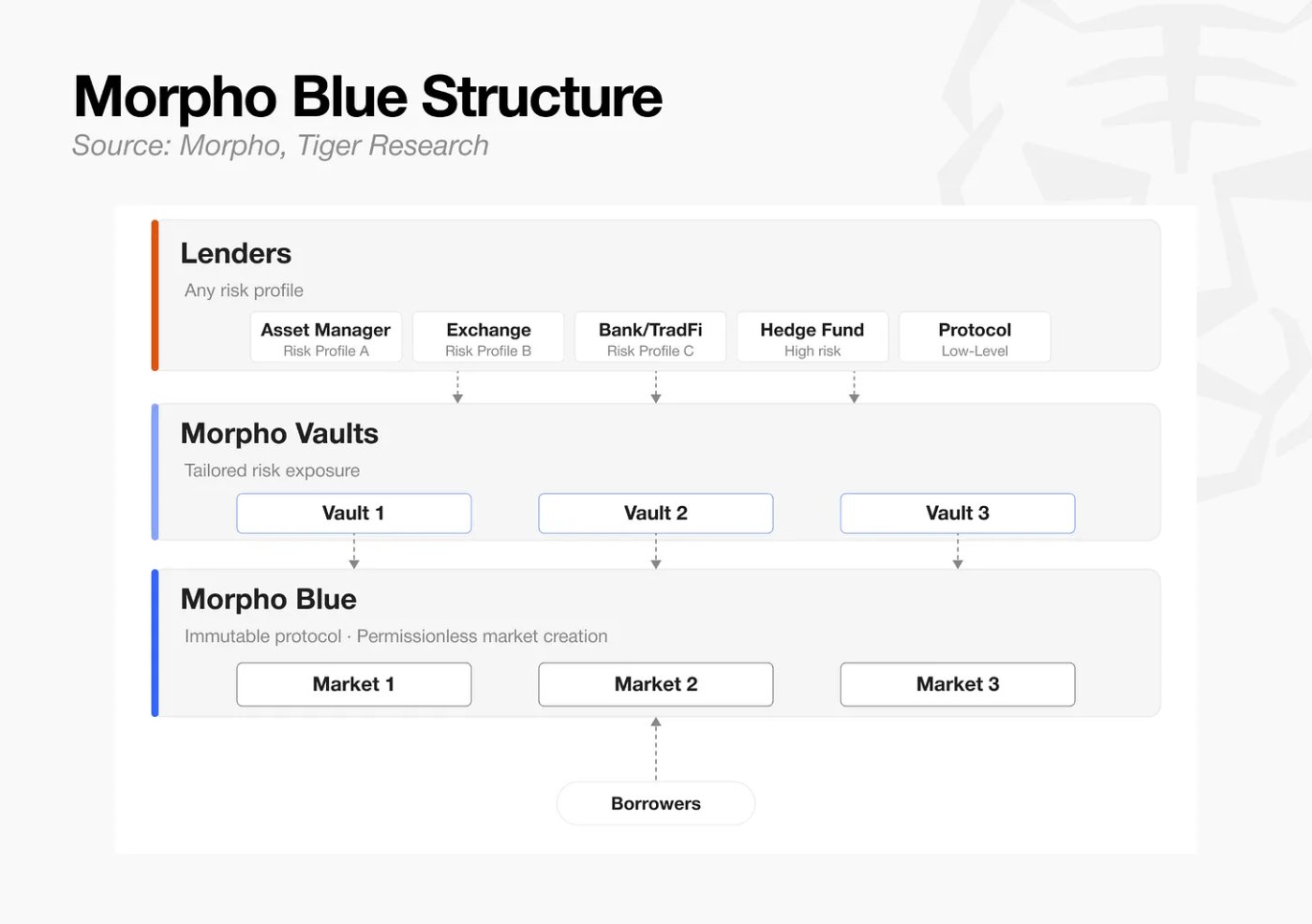

Morpho was initially an intermediary layer designed to optimize interest rates on top of first-generation DeFi lending protocols like Aave and Compound. In this model, it couldn't exist independently. In 2023, Morpho released the Morpho Blue white paper, and in early 2024 launched Morpho Blue and Morpho Vaults, officially announcing its independent operation.

This shift abandons the previous structure in which governance bodies handled all market risk decisions and separates market creation and risk assessment from the agreement itself. This separation forms the structural basis for institutional participants to select and control risks based on their own compliance standards.

Architecture

Morpho Blue : An immutable protocol. Five parameters are fixed when a market is created: collateral, borrowed assets, liquidation loan-to-value ratio (LLTV), price information, and interest rate model. Anyone can create a market without permission. The protocol itself is only responsible for executing pre-written code.

Morpho Vaults : A risk management system where independent curators select qualified markets, set supply limits, and allocate funds. Each vault has a unique risk profile.

Lenders : Depositors with varying risk tolerance, including DAOs, agreements, individuals, and hedge funds, choose vaults that suit their circumstances and provide funding.

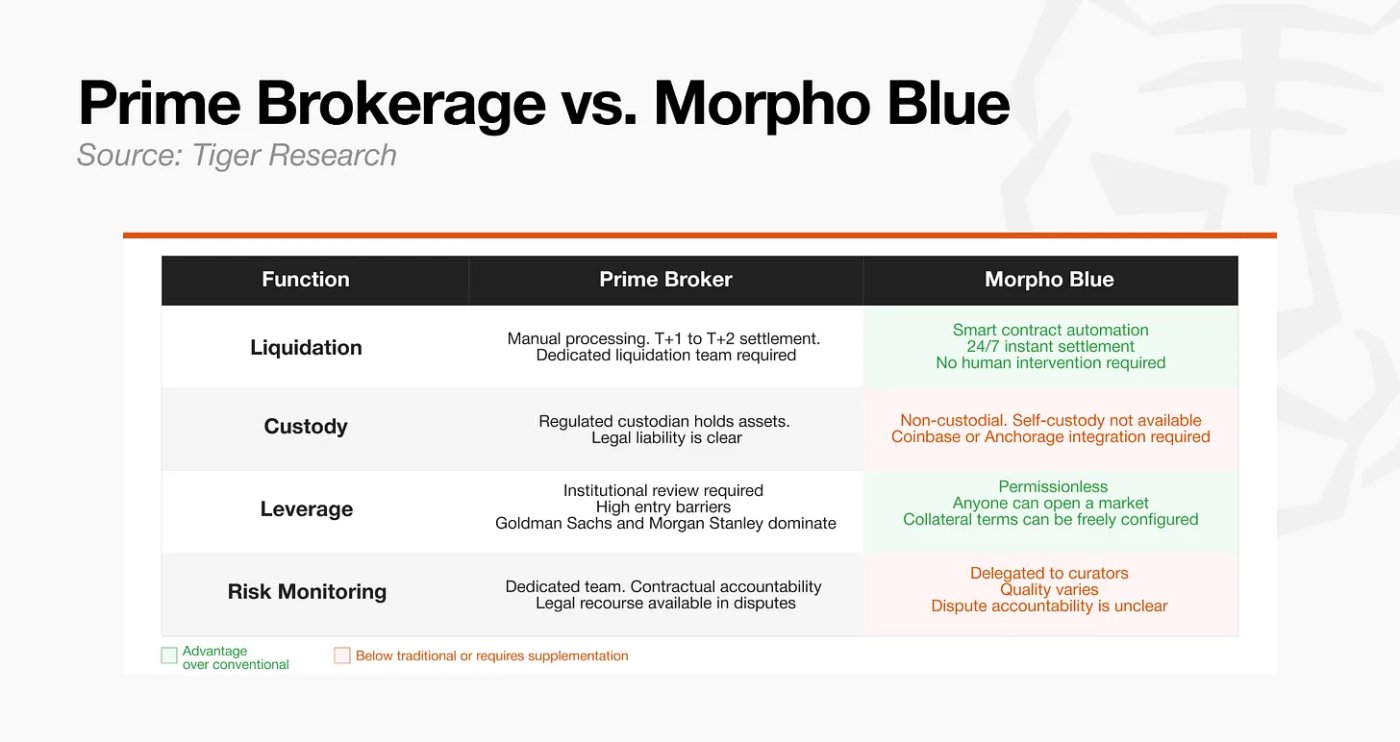

Traditional prime brokers typically perform four functions: clearing, custody, leverage provisioning, and risk monitoring. Morpho automates clearing and leverage provisioning at the protocol level through smart contracts. However, due to its non-custodial structure, it cannot provide the custodial environment required by institutional investors to meet regulatory requirements. Therefore, integration with external custodians such as Coinbase or Anchorage is necessary.

Similarly, risk monitoring depends not on the agreement itself, but on each custodian's ability to select assets and manage risk exposure. This creates a persistent risk: the quality of custodians varies greatly. The xUSD and Stream Finance incidents in 2025 directly exposed this vulnerability. Multiple Morpho vaults held xUSD exposure, resulting in bad debts. Following these events, the market began to scrutinize custodians' asset selection and real-time risk management capabilities more rigorously, and institutional capital concentrated its investments in top-performing custodians such as Steakhouse, Gauntlet, and Sentora.

Traditional brokerage businesses integrate clearing, custody, leverage, and collateral management into a single institution. Morpho replaces this model with a division of labor, distributing these functions among specialized participants within the ecosystem, rather than concentrating them in one institution.

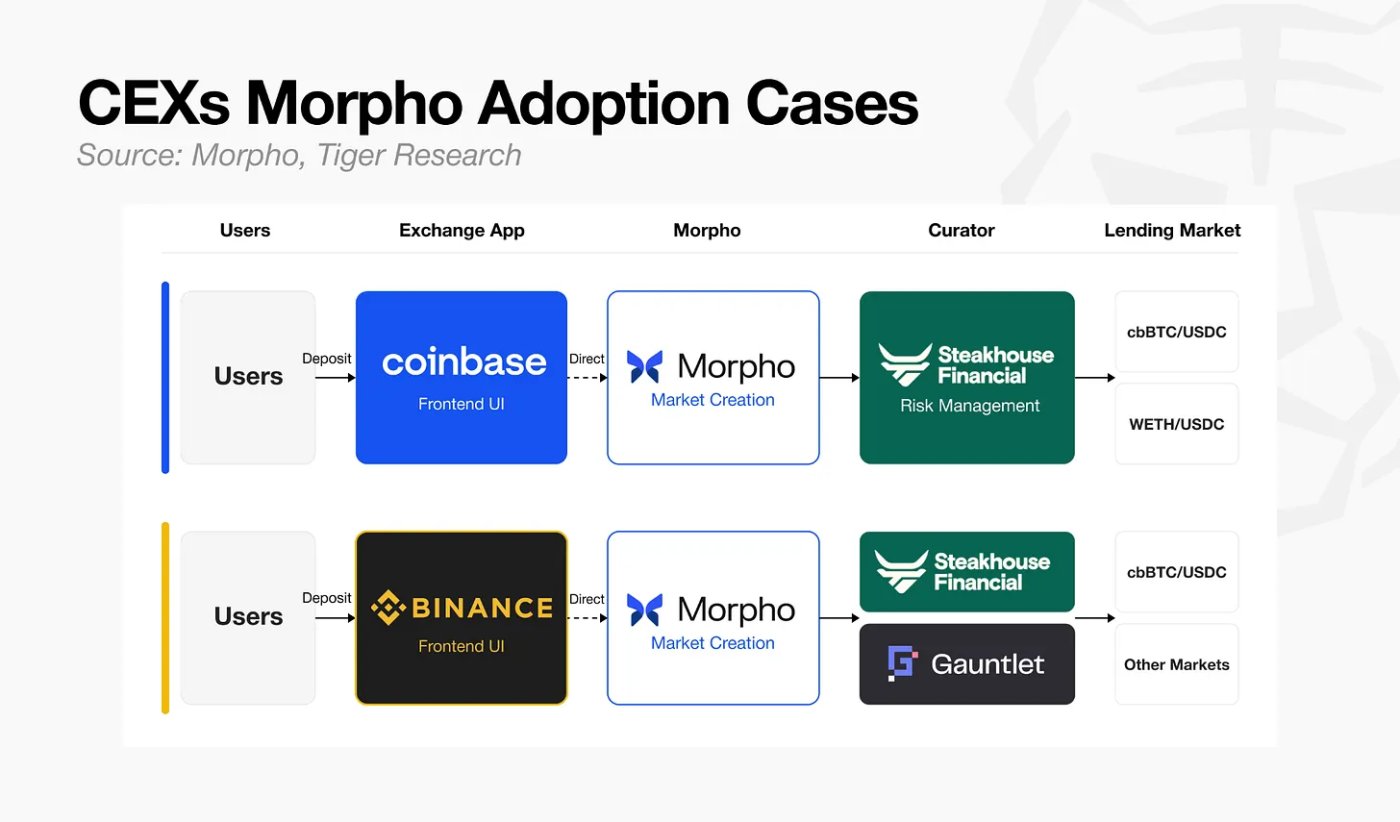

Institutional adoption is happening on a massive scale, and it all started with centralized exchanges.

Coinbase : A USDC lending service built on Morpho Blue, with custody services provided by Steakhouse Financial.

Binance: It adopted the same structure, with Steakhouse Financial and Gauntlet serving as curators.

Users can obtain loans by clicking the "Lend" button in the Coinbase or Binance apps. The world's two largest exchanges by trading volume have chosen the same architecture. This architecture has also been extended to traditional financial institutions.

SG-FORGE : Deploy MiCA-compliant stablecoins EURCV and USDCV on Morpho.

Apollo : Puts the private credit fund ACRED on the blockchain and uses it as collateral for Morpho.

Bitwise : Risk management directly on top of Morpho Vaults.

If tokenization opened up channels for acquiring assets, then Morpho pioneered a path to transform those assets into productive capital. The development trajectory set by Morpho is gradually showing a new direction of evolution, a direction that is difficult for lending protocols with drastically different starting points to ignore.

4.2 Aave V4: General Bank

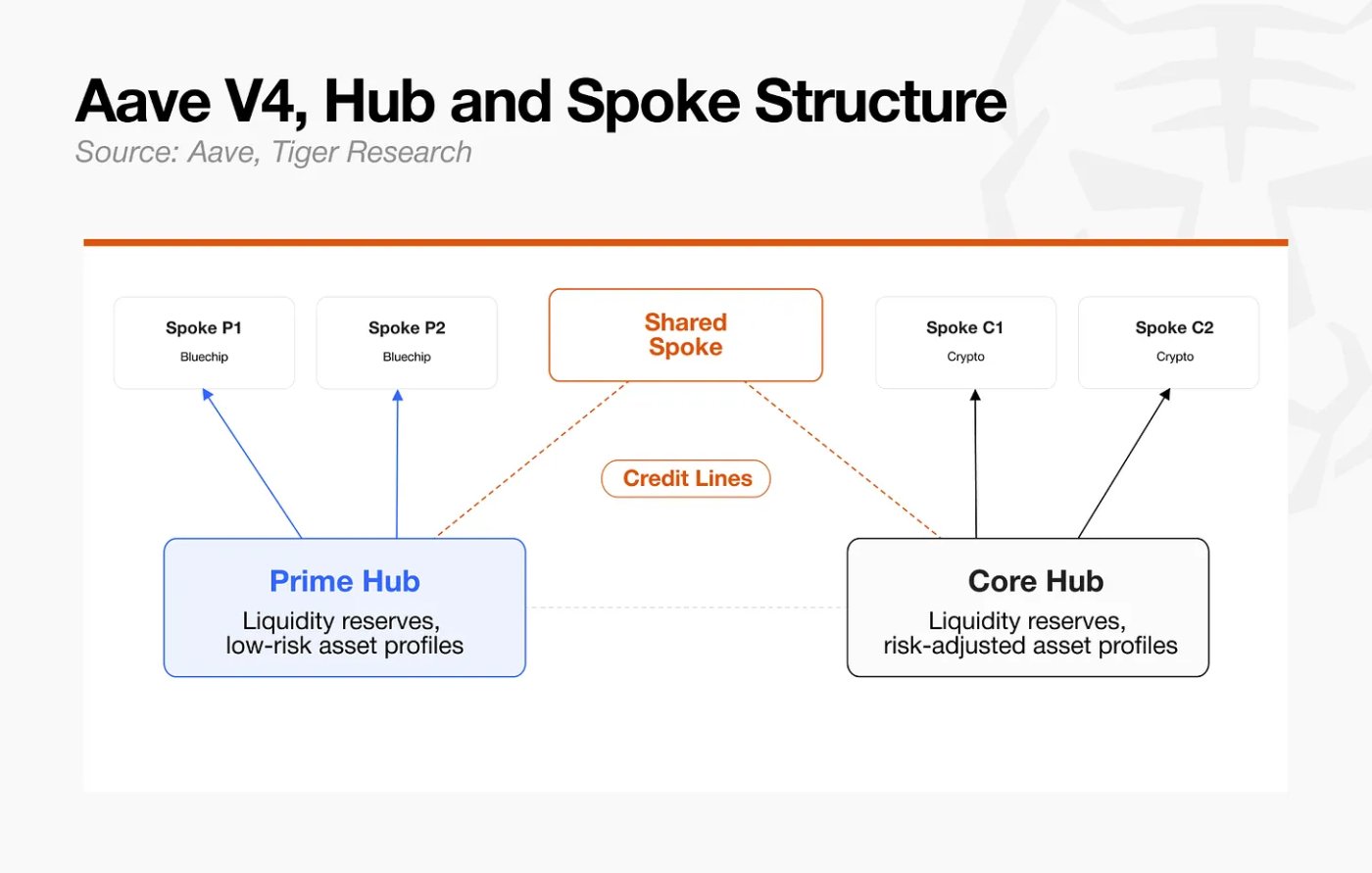

Aave, originally named ETHLend, was a peer-to-peer lending matching platform. It went through three versions—V1, V2, and V3—and gradually evolved into a shared liquidity pool architecture. In March 2026, Aave launched version V4 on the Ethereum mainnet, a modular architecture. Unlike Morpho, which structurally separated infrastructure from operations, Aave V4 adopted a hybrid model, controlling risk while maintaining liquidity efficiency.

Aave recognized the trade-off between risk isolation and capital efficiency. Moving towards risk isolation can curb the spread of bad debt, but it weakens liquidity network effects and reduces capital efficiency. V4 is designed to structurally address this trade-off.

Architecture

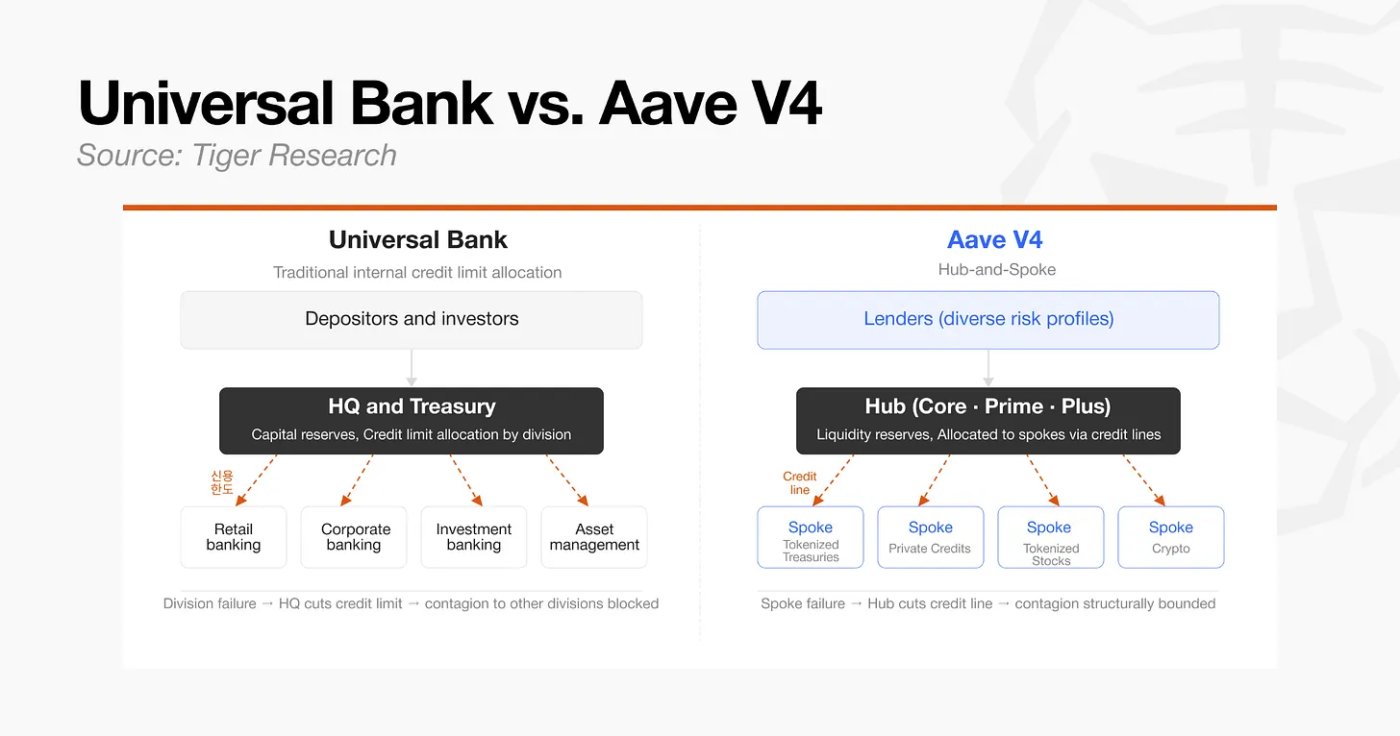

Hub : The core layer integrating liquidity and accounting. It allocates credit and debit limits to each branch, restricting liquidity available for withdrawal in any given market. The basic risk firewall consists of these branch limits and local parameters.

Spoke : An independent lending market where each asset has its own independent parameters. When a branch or asset encounters problems, governance and risk managers can reduce risk exposure by adjusting the credit limit for that branch, restricting new borrowing, or initiating emergency control measures. Because the maximum risk exposure is fixed at the credit limit, the structural contagion effect is limited by design.

In traditional finance, this structure resembles the internal credit allocation system of a comprehensive bank. The head office allocates credit lines to each department, and when a department encounters difficulties, the head office adjusts these lines to control interest rate spreads. The central hub acts as the head office, while each branch operates like an independent business unit. Unlike Morpho's fully segregated model (where capital is strictly locked in each asset pair), this hub-and-spoke structure allows unused liquidity in one branch to be flexibly reallocated to more efficient branches through the central hub's credit lines. The result is higher capital efficiency.

This structure becomes a significant advantage in the RWA market. Emerging RWA markets often struggle to attract initial liquidity, but in Aave V4, existing liquidity hubs can serve as seed mechanisms for new fork markets. By building tokenized assets as independent forks and setting credit limits at the hub, the liquidity base of safer assets can be leveraged to bring new asset classes to market at lower startup costs, while keeping initial exposure within credit limits.

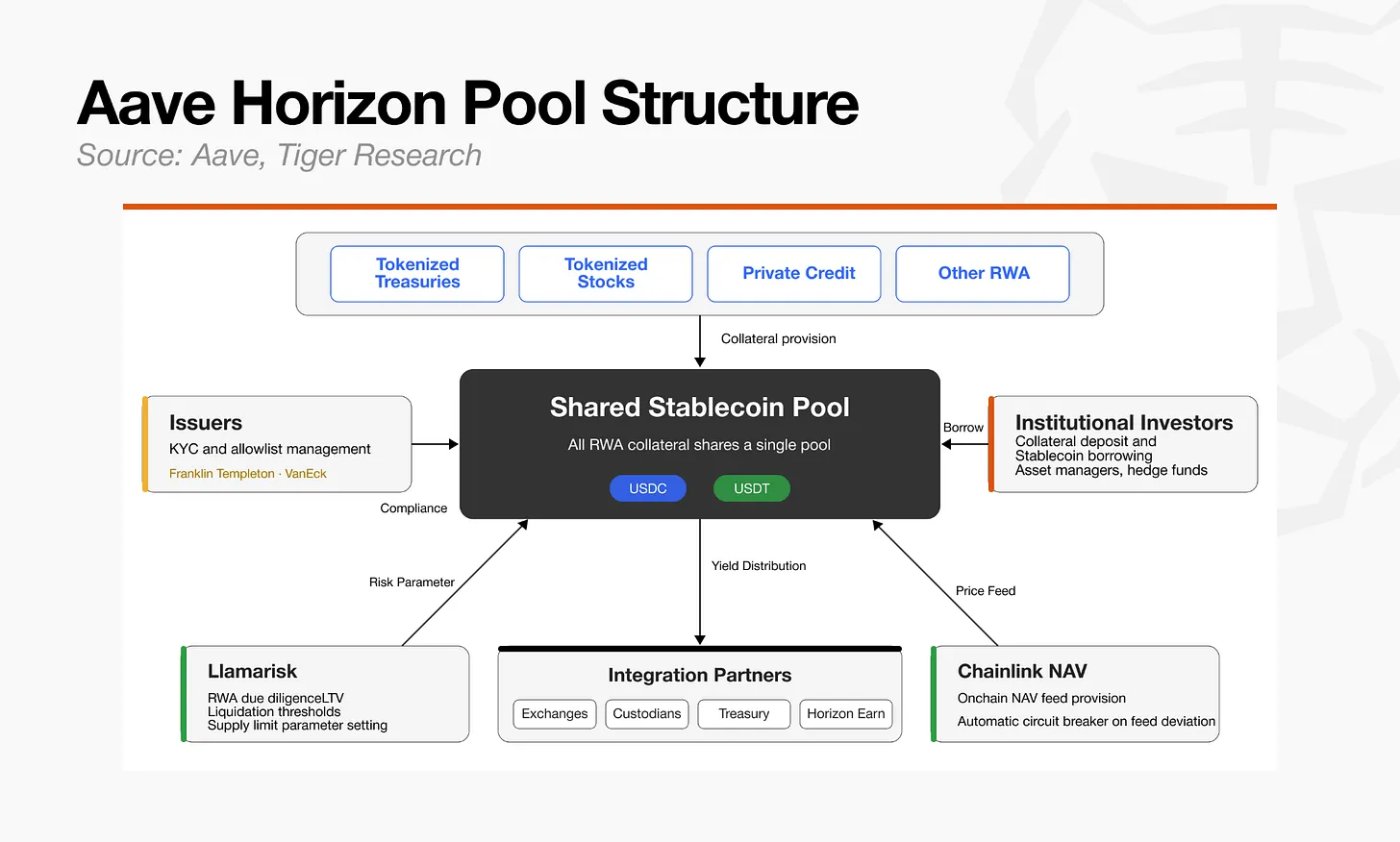

Institutional adoption primarily revolves around Horizon. Horizon was initially built as a standalone RWA lending instance based on Aave v3.3, but its design philosophy aligns with V4's unified liquidity and risk separation approach. As Horizon becomes increasingly integrated with V4's credit facility structure, it is likely to be further integrated into Aave's institutional RWA layer.

Horizon aims to allow regulated tokenized government bonds, money market funds, and institutional funds to serve as collateral for stablecoin lending, and has the potential to expand to asset classes such as tokenized stocks and ETFs.

Because approved institutional assets within Horizon are linked to the same institutional liquidity layer, any newly added RWA can immediately utilize existing stablecoin liquidity .

The roles within this liquidity layer are defined as follows:

Issuer : Investor access and KYC/AML allowance list management.

Risk Manager (LlamaRisk) : RWA due diligence, risk framework and parameter recommendations.

Oracle (Chainlink) : Provides on-chain price information.

Protocol (Aave) : Smart contract execution.

In traditional Aave markets, new assets require review and voting by the DAO governance committee, which slows down the process. Horizon separates these responsibilities: the issuer is responsible for compliance for each asset, LlamaRisk handles risk due diligence, and Chainlink verifies prices. This architecture allows institutional assets to be listed and risk-adjusted much faster than if all decisions were approved by the DAO governance committee.

Morpho minimized its governance involvement and outsourced market creation and risk management, opting for speed and choice; while Aave took a different path: controlling governance delegation and sharing liquidity to maintain capital efficiency.

Both approaches are coherent solutions that transplant the risk allocation concepts of traditional finance to the on-chain environment, but it remains to be seen which one the RWA market will ultimately gravitate towards .

4.3 Euler V2: Multi-Strategy Hedge Fund

In March 2023, Euler suffered a loss of $197 million. The attack exploited a vulnerability in the smart contract code, causing the loss to spread across multiple assets because multiple asset markets were connected to the same protocol's accounting and clearing structure.

After approximately three weeks of negotiations, most of the stolen assets were recovered. Nevertheless, Euler chose to rebuild the structure rather than merely repair it, and subsequently repositioned itself as a flexible institutional lending infrastructure.

Euler's drive into the RWA and institutional credit markets stems from the shortcomings in the tokenization of traditional financial assets. While banks have issued tokenized bonds, funds, and government bonds, these assets lack the on-chain infrastructure needed for lending or credit provision.

Instead of bringing institutional demand into the volatile long-tail crypto asset market, Euler has begun to position itself as the credit layer for institutional finance, providing on-chain liquidity for these assets.

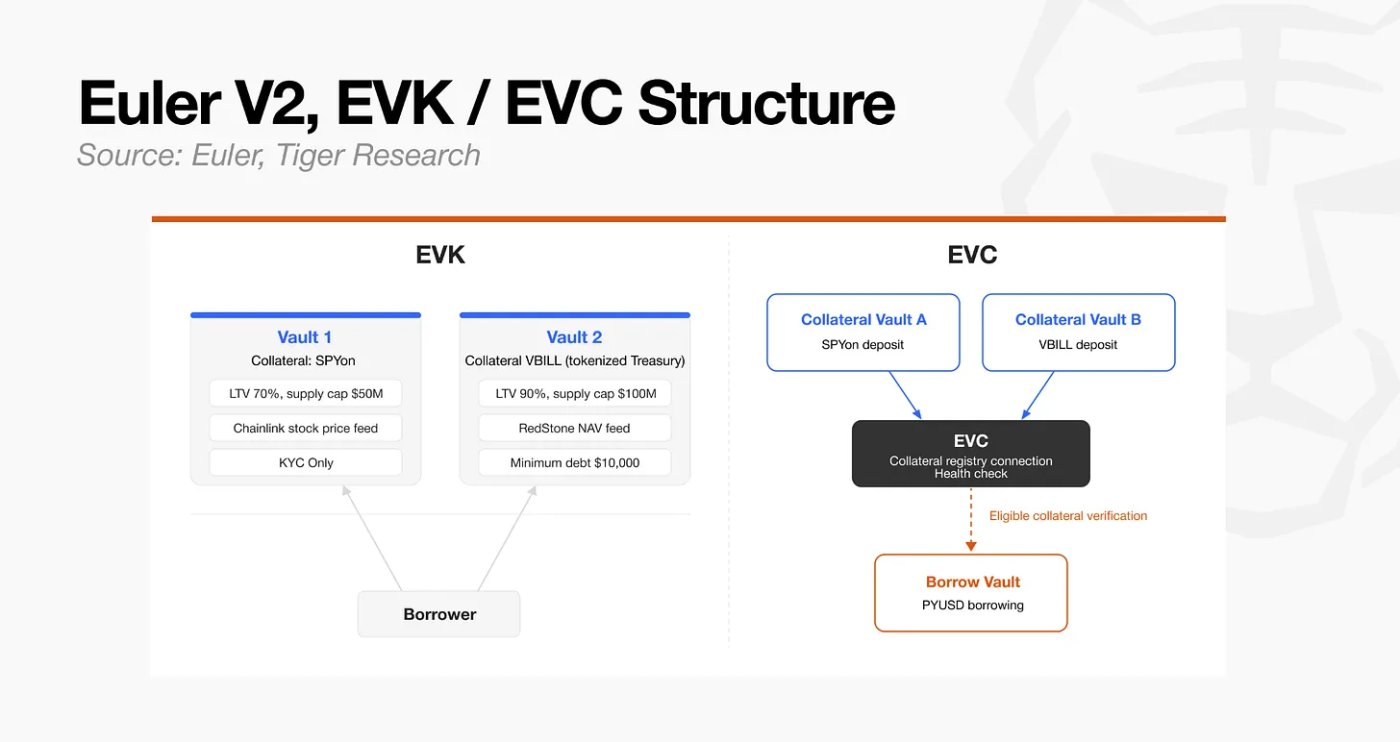

structure

EVK (Euler Vault Suite) : A suite for creating credit vaults based on ERC-4626 and equipped with lending functions. Each vault contains independent parameters for specific asset and risk configurations and connects with other vaults through EVC to form a lending market.

EVC (Ethereum Vault Connector) : The core immutable primitive used to connect collateral and debt relationships distributed across multiple vaults and manage them in a single account. In traditional financial terms, it's similar to consolidating multiple decentralized asset accounts into a single margin account that provides cross-collateralization.

EVK allows for independent design at the asset level, while EVC connects previously disparate assets into a unified account and position management framework.

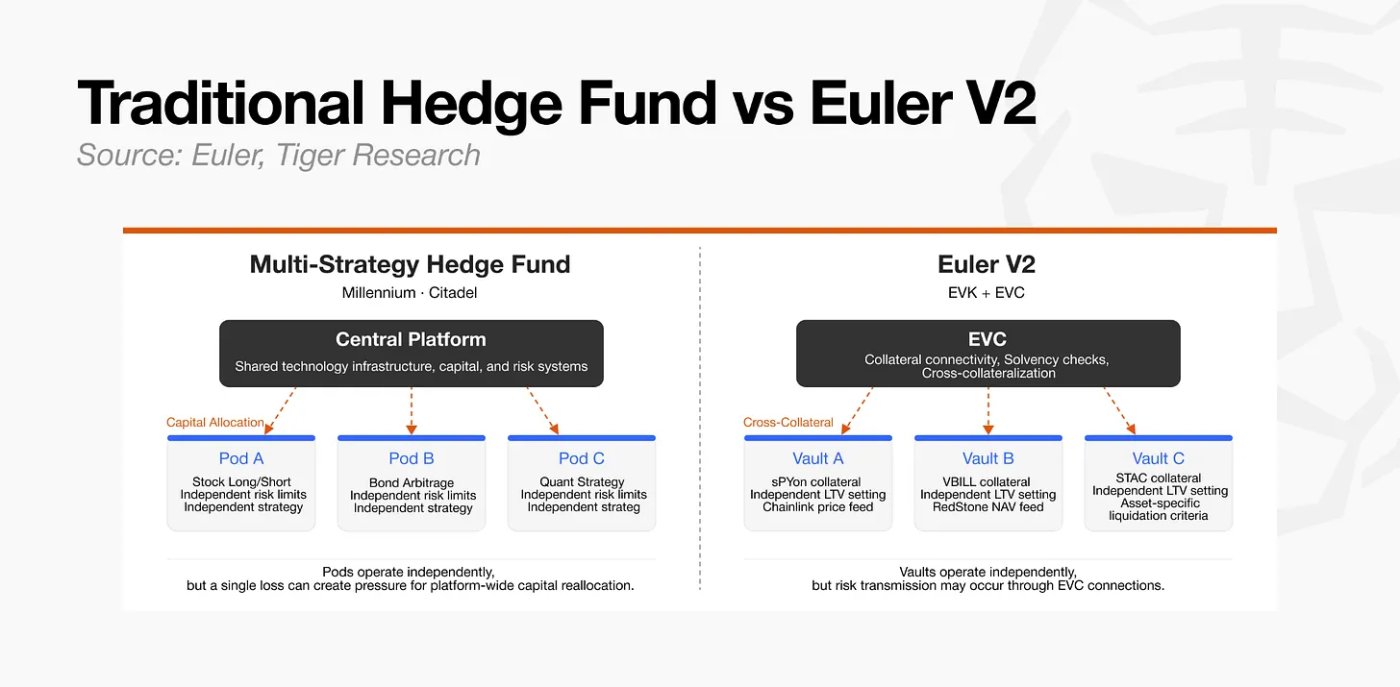

From a traditional financial perspective, Euler funds share some common characteristics with the "team" structure of multi-strategy hedge funds. Each independent team employs its own strategy and risk limits, while sharing technological infrastructure and capital management systems.

The key difference is that Euler is not an internal organization of a company, but an open infrastructure in which multiple independent participants can create and connect vaults.

By analogy, if Morpho resembles the division of labor model of prime brokers, and Aave resembles the shared liquidity model of universal banks, then Euler resembles the interconnected modular structure of multi-strategy hedge funds. The flexibility and capital efficiency brought by this architecture also mean that risk can potentially be indirectly transmitted from one asset to other positions within the interconnected vault ecosystem. Therefore, the custodian's risk management capabilities remain a core challenge for the Euler V2 ecosystem.

Euler's institutional applications are evolving to adapt to asset characteristics and regulatory requirements. A primary goal is tokenized stocks. Equity assets, traded 24/7, need to reflect price information that reflects company events such as dividends and stock splits. Building a separate market that meets these conditions under a single risk-sharing structure is impractical. EVK enables this by allowing for independent design at the asset level.

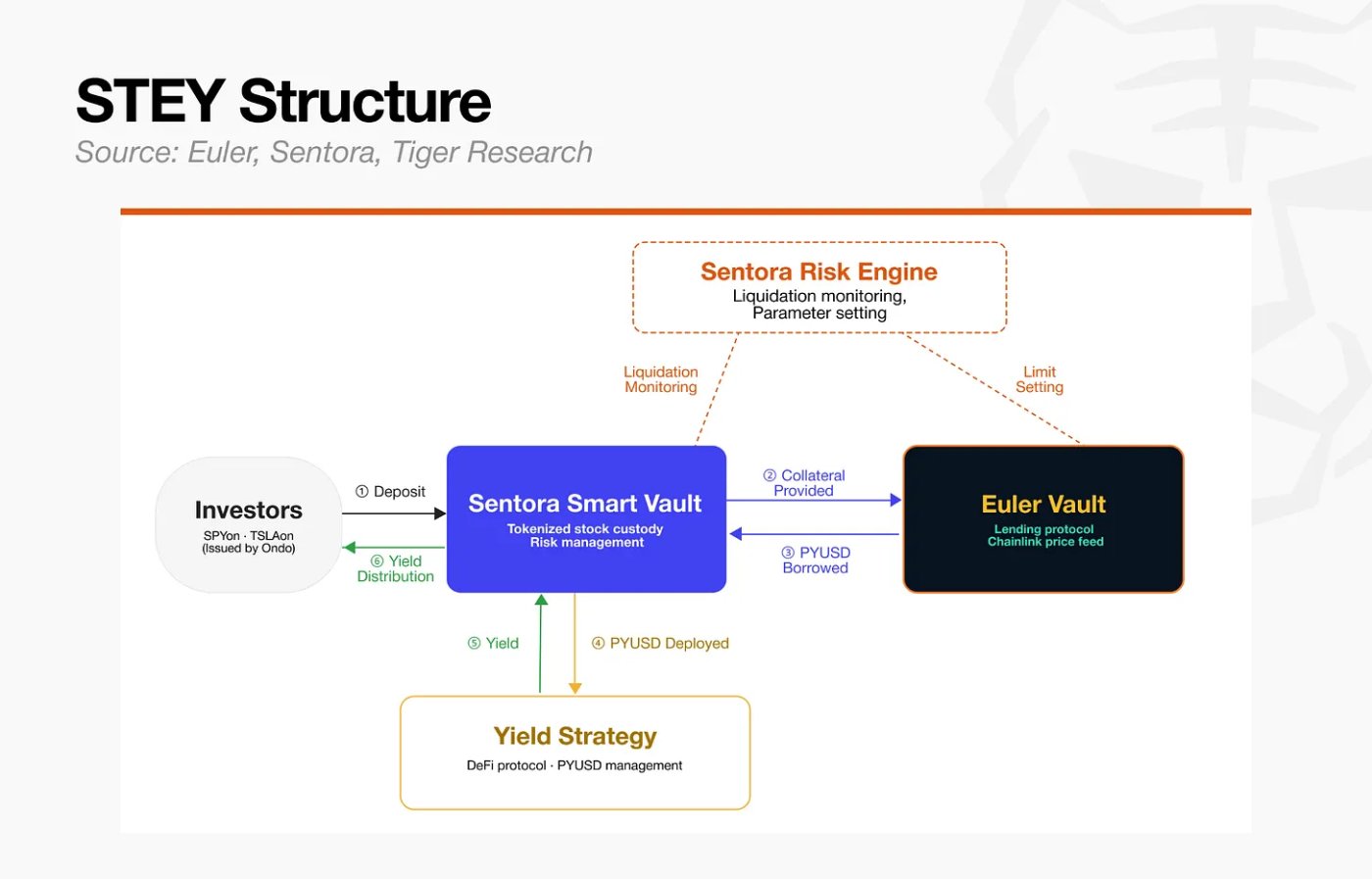

Euler has partnered with Ondo Finance to launch STEY, a lending marketplace that accepts SPYon (S&P 500), QQQon (Nasdaq 100), and TSLAon (Tesla) as collateral.

STEY Market Structure

Collateral : Ondo tokenized shares (SPYon, QQQon, TSLAon)

Borrowed asset : PYUSD (PayPal stablecoin)

Price Information : Chainlink Real-time Stock Price Information

Risk Management : Planned by Sentora

Just as traditional finance uses Lombard loans to release liquidity for stock holdings, the STEY market replicates this mechanism on-chain. Investors can maintain price exposure to tokenized stocks while redeploying borrowed stablecoins into on-chain yield strategies, thereby maximizing capital efficiency.

The second aspect is the combination of tokenized government bonds and CLOs (collateralized loan obligations). Euler launched the KPK USDC Prime RWA Vault to demonstrate this structural flexibility.

KPK USDC Prime RWA Vault Architecture

Collateral : VBILL (VanEck Tokenized Treasury Bonds), STAC (Securitize AAA-rated CLO)

Borrowed Assets : USDC

Price Information : Redstone Daily Net Asset Value Information

Risk Management : Planned by Sentora

CLOs require regular net asset value pricing via oracles and adherence to specific asset liquidation standards. Tokenized treasuries require stringent compliance controls. Without a modular infrastructure allowing for customized interfaces and parameters at the treasury level, launching these two asset classes as on-chain lending collateral will be extremely difficult.

Nevertheless, the possibility of indirect risk transfer due to overlapping exposures to the same assets, oracles, and collateral remains, and Euler V2 faces the ongoing challenge of striking a balance between flexibility and control.

These three agreements address institutional access barriers from different perspectives and with different approaches .

Morpho : Fully externalizes market creation and risk management to maximize speed and choice, and uses the quality of the curatorial layer as a key variable for validation.

Aave : Combining controlled governance delegation with V4’s central-radial architecture, it pursues a hybrid approach that maintains capital efficiency without compromising stability.

Euler : Utilizing EVK and EVC to simultaneously ensure single-asset independence and cross-collateral flexibility, seeking the optimal risk balance in a multi-strategy structure.

Their approaches differ, but all three are moving in the same structural direction: separating the basic execution infrastructure from the risk assessment layer and designing asset-specific risk parameters for each type of collateral.

5. Conclusion

In traditional capital markets, prime brokers spent decades establishing themselves as the core infrastructure for hedge funds, encompassing all aspects of trading, custody, settlement, leverage, and risk management. The collapse of Lehman Brothers and the run on reserve funds in 2008 exposed different types of systemic risks, leading the market to focus more on issues such as custody, collateral, liquidity management, and role separation.

The DeFi ecosystem reached a similar structural conclusion in a much shorter time. Its rapid development is due to the faster iteration speed of code compared to regulation.

Early risk-sharing architectures encountered governance bottlenecks and experienced unexpected risk exposure and bad debt contagion. Morpho, Aave, and Euler all quickly implemented risk isolation and operational separation on-chain. Through repeated real-world capital losses and architectural reconstruction, the DeFi market has accomplished in just a few years what traditional finance took decades to achieve.

Traditional financial history shows that the maturation of infrastructure such as brokerage services is one of the conditions driving the development of the hedge fund industry. After 2008, as the infrastructure stabilized, institutional capital began to flow in, and the total assets under management of hedge funds approached $2 trillion. Between 2015 and 2025 alone, the industry's size is projected to grow from $1.4 trillion to $4.5 trillion. With the maturation of infrastructure, real competition in strategy and risk management begins at the upper operational levels, and fund managers demonstrating exceptional capabilities attract market capital.

The on-chain lending market is approaching a similar turning point. With Morpho, Aave V4, and Euler V2 converging on risk isolation and operational separation, the core question now is what kind of competition will emerge at the operational layer above these infrastructures.

Currently, the total assets under management of on-chain vaults are approximately $7.4 billion. Given the rapid growth of the hedge fund industry after the infrastructure was built, the current on-chain credit market is more like the early stage of a larger-scale expansion.

In traditional finance, Goldman Sachs and Morgan Stanley virtually monopolize prime brokerage infrastructure, and hedge funds must accept their terms to gain access. On-chain infrastructure operates quite differently. Opening a market on Morpho or Euler requires no institutional permission.

With the breaking of infrastructure monopolies, competition at the on-chain operational level may unfold more openly and rapidly than in the traditional financial sector. In traditional markets, platforms such as Bridgewater Associates, Millennium Investment Group, and Citadel Investments, as well as alternative asset management firms like Blackstone Group and Apollo Global Management, have attracted substantial funds by leveraging their operational capabilities and infrastructure advantages.

On-chain, any participant capable of assessing collateral, designing risk parameters, addressing institutional regulatory requirements, and establishing a track record now has the opportunity to gain a foothold in emerging credit markets, where the infrastructure is far easier to access than that offered by traditional finance.