Author: @sjbtc9

"Perp DEX is not a small sub-sector of DEX, but rather an on-chain mapping of the derivatives exchange war."

"From a trading perspective, any CEX can be described as a 'black box' ."

"This 'war' has only just begun."

Yesterday I posted about Perp DEX, and it just talked about one thing:

Many people still consider Perp DEX a niche DeFi sector, but judging from its online activity (OI), it has already begun to influence the portfolio allocation mindset of some mainstream funds.

But we won't continue piling up this data today, because data is just an entry point, and a single piece of data cannot completely define anything.

The more important question is:

Why is online inquiry retention becoming increasingly important on Perp DEX? And what's happening in this market surrounding perpetual contracts (Perp)?

I don't think the answer is "because it's actually going to replace someone".

I. Perp DEX is not a new track; what's new is that the measurement standard has changed.

Perp DEX is certainly not a new thing; it could even be called an "old-fashioned track."

Projects like dYdX and GMX have already "educated" the market in previous cycles. On-chain contracts and leverage can also be implemented, and a certain scale of trading volume can be generated.

Perp DEX has moved beyond the functional validation phase and is now entering the behavior retention phase.

The first question is: Can contracts be created on-chain? And will anyone actually use them?

The first question is: Can contracts be created on-chain? And will anyone actually use them?

The question now is: are investors willing to keep their positions here in the long term?

These two issues are completely different. On-chain contracts are a form of technical verification; someone's willingness to trade is a form of product verification; and someone's willingness to hold their positions long-term is a form of behavioral migration.

When people talk about Perp DEX, they often start by discussing the trading experience.

For example, is the speed fast? Is the slippage low? Are the transaction fees cheap? Is the interface user-friendly?

These are certainly important. If it's not user-friendly, users won't come. If it lacks depth and has a flawed settlement mechanism, large funds won't come, nor will they dare to.

But these are more like entry tickets than the ultimate moat.

In other words, previously you might only need to prove "this thing can run", "someone will use it", and "it runs stably";

Now you need to prove that "funds are willing to put their risk exposure with you".

This is what makes Perp DEX different from many other DeFi products.

Swap is often a one-time action, borrowing may be a low-frequency money management activity, but PERP is a continuous and relatively high-frequency behavior.

Therefore, if Perp DEX or similar trading platforms really succeed, they will not attract ordinary users, but rather a group of high-frequency, high-risk-preference, and high-willing-to-pay traders.

These users may not be the most numerous, but their value is the highest among market participants.

II. Perp's On-Chain Leaders, Veterans, and Off-Chain Players

1. Hyperliquid: Its most commendable feature is not trading volume, but rather its position sizing mindset and value capture.

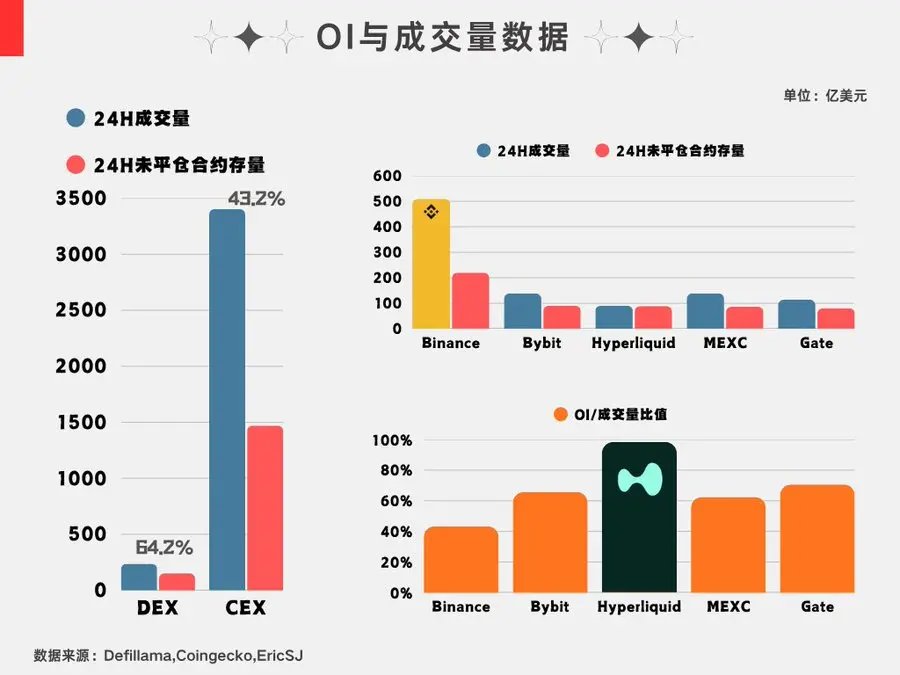

The most typical example here is Hyperliquid, which deserves a major portion of this article to discuss. It can be said that it was the changes in OI (Online Competition) that led to this series of viewpoints.

As I briefly mentioned yesterday, Hyperliquid's OI/volume ratio is as high as 97%, and today I checked the latest ratio again, which is even approaching 99%.

Regardless of the structure of its participants, funds are the most direct form of "voting," and a relatively strong mindset regarding position allocation has begun to take shape.

Therefore, Hyperliquid's strength lies not only in "creating a user-friendly on-chain contract exchange", but also in its ability to make a portion of funds the new default choice, which is what truly constitutes its competitive advantage.

Once the default choice of funds is formed, it will bring about a lot of chain reactions: more position accumulation, deeper market making, stronger revenue, more new markets, and stronger ecosystem stickiness.

What's even more noteworthy is that it has built Perp DEX into a relatively complete on-chain exchange system: it has its own high-performance chain, an order book, a margin system, a clearing system, market depth, protocol revenue, and token capture.

This is different from most DeFi protocols, many of which have the following problems:

There is TVL, but no high-frequency behavior;

There are users, but the revenue is unstable;

There are tokens, but value capture is weak.

I think Hyperliquid does this so well that I'm reluctant to use the less confident word "one of".

Firstly, user transaction behavior itself is a source of revenue, and this revenue can be more directly linked to $HYPE's value capture.

Therefore, its value chain is: user transaction → transaction fee generated → transaction fee enters the protocol revenue system → Assistance Fund buys HYPE → HYPE is removed from the supply chain.

Value capture has always been the ultimate question in the industry. The prerequisite for value capture is that at least the protocol must generate revenue. Some protocols have no revenue or unstable revenue, making value capture impossible. Others have revenue but it is not pegged to the token.

Hyperliquid has already set this standard. Even if competitors don't surpass it, failing to reach the same level will inevitably draw criticism from the community.

2. Aster and Lighter: One solves privacy, the other solves trust.

The issue of Perp DEX doesn't only have one answer from Hyperliquid, because the reasons for leaving funds behind are not entirely the same.

Some people care about depth, some about speed, some about privacy, some about cost, and some about whether the matchmaking and settlement processes are transparent.

This is why projects like Aster and Lighter are worth including in this discussion.

According to data from Defillama, Aster and Lighter, two Perp DEXs, are ranked 2nd and 4th in terms of OI and 30-day trading volume, respectively . They are similar products, but they provide different answers.

2.1 Aster focuses on position privacy.

Why are many users unwilling to switch from their old trading habits?

It's not that he doesn't know on-chain trading is possible, but rather that on-chain trading has long been perceived as troublesome: fragmented assets across multiple chains, unsatisfactory gas experience, complex transaction paths, and overly transparent positions.

In particular, the transparency of positions is crucial in the futures market. While it's not so problematic for spot trading to be visible, making your futures positions visible can expose your direction, costs, leverage, and potential liquidation range.

For ordinary users, this is a privacy issue; for both buyers and sellers, it is a transaction risk.

Therefore, Aster's focus is on privacy. It emphasizes that orders are encrypted before reaching the blockchain and decrypted only during execution. A user's position size, entry point, and liquidation price are not directly exposed in the order book.

Therefore, Aster tells a different story in the PerpDEX section: on-chain transactions should not only be transparent, but also protect the privacy of traders' strategies.

It is currently directly competing with Hyperliquid. Rather than talking about the aspects mentioned above, it's more accurate to say it's a power struggle behind the scenes between the old and new platforms (those who know, know).

2.2 Lighter is a different line.

It's easily summarized as zero fees, but I think zero fees are just the surface. What's truly more important is that it addresses the question of whether the matching and clearing processes are trustworthy.

The biggest problem with CEXs is not the poor user experience; on the contrary, the user experience of CEXs is excellent. The problem is that they are black boxes, and any CEX can be described as a "black box".

You don't know if the matchmaking is completely fair, you don't know if the settlement is transparent under extreme market conditions, and you don't know if the platform will prioritize its own interests...

These issues are not important under normal circumstances, but they become important in extreme market conditions or high-volatility market conditions.

The fundamental difference between Lighter and the other two lies in their underlying technology. While the former two are self-developed L1 algorithms, Lighter uses ZK L2 with zero-knowledge proofs. It generates a zero-knowledge proof for all operations, including order matching and settlement, and makes it verifiable on the Ethereum network.

Therefore, if Lighter can clearly explain verifiable matching and settlement, it will not solve the problem of cheapness, but rather trust.

So Lighter isn't saying "I have the most assets" or "I'm most like Binance." It's saying that the core operations of an exchange should be verifiable.

The three protocols listed above can all be considered typical examples of the [new cycle of Perp DEX], so I am not too keen on writing the competition between Hyperliquid, Aster and Lighter as: Who will be the next leader of Perp DEX?

This expression is too narrow.

I think a more accurate way to put it is that they are answering three different questions about Perp DEX: fund retention, privacy, and trust.

3. dYdX/GMX: The old entry points are not without value, but the standards have changed.

The PerpDEXs listed above are the most outstanding ones up to the current cycle, but I think it's also very necessary to elaborate on the "previous wave": dYdX and GMX.

This isn't to say they're no good, but to illustrate a more important point: entry points aren't permanent, and user behavior standards can change.

dYdX represents the previous generation order book Perp DEX, and GMX represents the LP pool model Perp DEX.

They have all solved real problems.

In the early stages, there wasn't enough order book depth or a smooth enough on-chain contract experience, so GMX's LP pool model was very effective. Users could trade directly with the pool, with LPs bearing counterparty risk and earning rewards from transaction fees, swaps, leveraged trading, and liquidation.

This was a very nice native DeFi solution at the time.

However, the problem is that as products like Hyperliquid, Aster, and Lighter begin to align the experience, depth, speed, and professional traders' needs with CEXs, the GMX model will face a challenge:

It is more suitable for native DeFi users, but may not necessarily become the main trading platform for professional traders.

dYdX faces a similar problem. It's not that it's heading in the wrong direction, but rather that its original label as "on-chain order book representative" is no longer sufficient in the face of new-generation competition. Or, more directly, it's because "it's too 'old' and has been defeated by the cycle."

According to DeFiLlama's current data, GMX and dYdX still maintain a certain level of online interest (OI) and trading volume, but their scale has clearly fallen behind Hyperliquid, Aster, and Lighter.

Therefore, the judgment here is not "old projects are reset to zero".

Instead, the competitive standards for Perp DEX have changed.

Previously, the competition was about "whether contracts can be executed on-chain"; now, the competition may be about "whether it can more closely resemble a CEX experience and retain funds."

(The next stage may also be about "whether it can become the underlying infrastructure of the derivatives market")

This is the value of dYdX / GMX as case studies; they are not negative examples, but rather references for the industry as it moves from one stage to the next.

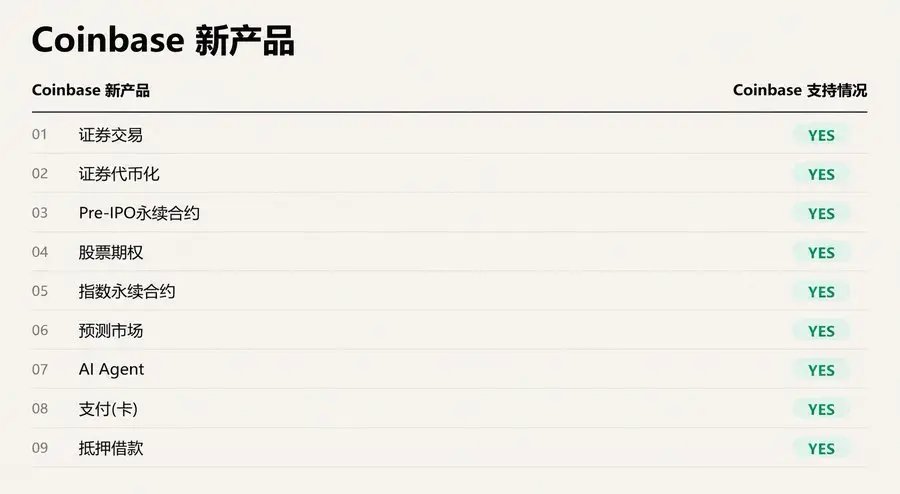

4. Coinbase: Not just on-chain

Finally, I'll include an off-chain case study because if the entire article only discusses Hyperliquid, Aster, Lighter, and other on-chain protocols, readers might easily mistake it for mere self-indulgence on the blockchain.

But that's not the case.

At the end of last month, Coinbase and prediction market platform Kalshi announced the official launch of cryptocurrency perpetual contracts. This marks the first time a compliant US-based exchange has offered such trading products to domestic investors.

A few days ago, Coinbase further opened up other perpetual contract products, which is a very important signal.

This illustrates that the Perps market is no longer just something that on-chain companies are eyeing, but a core product form that compliant exchanges and prediction markets are vying for.

Furthermore, perpetual contracts, a relatively new derivative instrument in the financial market, are beginning to be widely accepted. Coinbase is doing this by bringing high-frequency derivatives trading, which originally occurred on offshore exchanges and in the gray market, back to the US compliance framework.

Overall, all of these cases focus on one thing and attempt to answer one question: Who can take over the next generation of high-frequency risk trading?

Both sides are trying to answer this question with different solutions. On-chain solutions use decentralized infrastructure, on-chain margins, transparent clearing, token incentives, and market creation mechanisms, while off-chain solutions use regulatory licenses, compliance frameworks, existing user bases, and traditional financial market structures.

III. In Conclusion

I've placed the main sections of this article in the second paragraph, hoping to use several classic examples to help everyone understand the competition and future prospects of Perp DEX and even Perp itself.

(As I write this, I suddenly realize that some of you might not know what Perp is; it's an abbreviation for perpetual contracts.)

Therefore, the final conclusion of this article is: Perp DEX is not a small DEX sector; it is an on-chain projection of the derivatives exchange war. What is truly being fought over is the closed loop of fund behavior and stickiness.

Finally, summarizing these cases again, we can see a different debate surrounding Perp:

Hyperliquid is saying: On-chain Perps can become exchange systems and new entry points; Aster is saying: To attract CEX users, performance and privacy issues must be addressed; Lighter is saying: The next stage will shift from competition based on user experience to competition based on trust mechanisms; dYdX / GMX is saying: The old model is not without value, but industry standards have changed; Coinbase is saying: The Perps war is already expanding outwards.

......

And this "war" has only just begun.