Written by: flowie, ChainCatcher

RWA (Real-World Assets), regarded as the next growth engine of DeFi, is heating up.

Recently, after the encrypted lending agreement Maple Finance announced that it will launch a US Treasury bond pool, its token $MPL rose by more than 20%. In the past three months, RWA concept tokens such as $CREDI, $SMT and $FACTR have all increased by more than 10 times.

In addition, Binance announced last week that it has become the Layer 1 blockchain Polymesh node operator, which also attracted the market's attention to RWA. Polymesh is not an ordinary Layer1, but an institutional-grade blockchain tailored for regulated assets such as security tokens. After the news was announced, Polymesh token POLYX rose by more than 10%.

A current trend that cannot be ignored is that, in addition to Binance, large traditional financial institutions such as Goldman Sachs, Hamilton Lane, and Siemens, and leading DeFi protocols such as MakerDAO and Aave are all vying to deploy on the RWA track.

According to the encrypted data platform Rootdata, there are nearly 50 projects in the RWA sector , and there are many innovative projects in the lending and real estate fields. Among them, there are many well-known institutions such as a16z, Coinbase Ventures, and Fenbushi Capital among the investors of projects such as Goldfinch, Centrifuge, and Maple Finance.

Why RWA Fire again ?

RWA — Tokenization of Real Assets, is not a new concept. Since the birth of the blockchain, discussions on the tokenization of real-world assets such as real estate, commodities, private equity and credit, bonds and artworks have been frequent, and many conceptual projects have appeared one after another, but none of them have caused too many splashes.

In 2020, MakerDAO officially included RWA in its strategic focus and released guidelines and plans for introducing RWA. The concept has gradually attracted more attention. In addition to issuing the stablecoin DAI, MakerDAO has adopted proposals for RWA as collateral in the form of tokenized real estate, invoices and receivables to expand the issuance of DAI. It is reported that about 70% of MakerDAO's revenue in December 2022 will come from RWA. Following MakerDAO, Aave announced the launch of the RWA market at the end of 2021, which also allows mortgage lending of real assets. However, despite the layout of the head agreement , RWA has been tepid .

Recently, Binance has stepped into the market, and the intensive layout of traditional financial institutions represented by Goldman Sachs, Hamilton Lane, Siemens, etc. and some on-chain U.S. debt agreements has brought RWA back into view.

Earlier this year, Goldman Sachs first announced that its digital asset platform GS DAP was officially launched, and the platform has helped the European Investment Bank (EIB) issue a two-year digital bond of 100 million euros. Soon after, Hamilton Lane, a private equity firm with a management scale of over 100 billion, tokenized part of its $2.1 billion flagship equity fund on the Polygon network and sold it to investors; the electrical engineering giant Siemens also issued 6,000 for the first time on the blockchain. million euros in digital bonds.

In addition to becoming the node operator of the Layer1 blockchain Polymesh mentioned above, Binance also released a 34-page in-depth research report on the theme of RWA in March this year.

In addition to the actions of large institutions, we also found that many projects that support on-chain US debt, represented by Ondo Finance and TProtocol, have frequent actions. Last week, Ondo Finance announced the launch of the money market fund (MMF)-based USD stablecoin OMMF, TProtocol launched a liquidity mining plan, and Maple Finance announced that it will launch a US Treasury bond pool.

Some crypto-friendly government agencies are also testing the waters of RWA , such as the Monetary Authority of Singapore (MAS), which announced a pilot program called Project Guardian, which will tokenize bonds and deposits for various Among the DeFi protocols, JPMorgan Chase and DBS Bank are the pilot partners.

Since RWA is not a new concept , why is RWA being taken seriously again at this point in time ? What is the driving factor ?

The Binance RWA research report mentioned that in the short term , the most direct reason is that the continued sluggish yield of DeFi cannot meet the growing demand for income from crypto users. During the DeFi Summer period, the high yield of the bull market can meet the income needs of crypto investors. However, after experiencing major market shocks and a continuous bull market, the TVL of DeFi has dropped by more than 70% from the high point in December 2021, and the yield of DeFi has fallen to the bottom. DeFi protocols or crypto investors need a new income growth channel.

From this perspective, it is not difficult to understand why on-chain U.S. debt is the hottest trend on the RWA track recently. With the Fed continuing to raise interest rates, the yield of investing in U.S. bonds is much higher than that of DeFi agreements. The general yield of DeFi veteran protocols such as Curve, Aave, and Compound has fallen from the highest over 10% to 0.1-2%, while the yield of US bonds has increased from 0.3 to 5%. The latter also does not pose as many protocol security risks as the former.

In addition, in the long run , the story of RWA connecting traditional finance and encrypted finance does bring a lot of room for imagination .

The real assets of traditional finance such as real estate and non-financial corporate debt markets are huge trillion-scale markets. If DeFi is compatible with it, users can obtain greater liquidity, capital efficiency, and investment opportunities.

At the same time, traditional finance also has many pain points such as high entry barriers, many intermediaries, and many restrictions. For example, the investment capital of private equity funds generally requires more than 500,000 US dollars, and real estate investment also requires expensive capital support. Unable to enter the market, in addition to facing high fees from intermediaries, regulators restricting entry and risks of assets in third-party systems. The design of DeFi can also solve some pain points of traditional finance, and has the potential to attract more investors into DeFi.

According to a recent Boston Consulting Group report, RWA is expected to be a $16 trillion market by 2030.

What are some representative use cases for RWA ?

The story of RWA aiming to connect traditional finance and encrypted finance is not difficult to understand, but it is not easy to truly realize the connection and inject a large number of large-scale new assets into Web3.

"We are still far from the ultimate goal", @ThreeDAO member researcher Jason Chen believes that the development of the RWA track currently has two stages. One is the earliest process of using the blockchain to confirm the rights and authentication of real assets such as real estate and collectibles. For example, at that time, many alliance chains put stamps on the chain. Assets are brought on-chain. We are currently exploring the second stage.

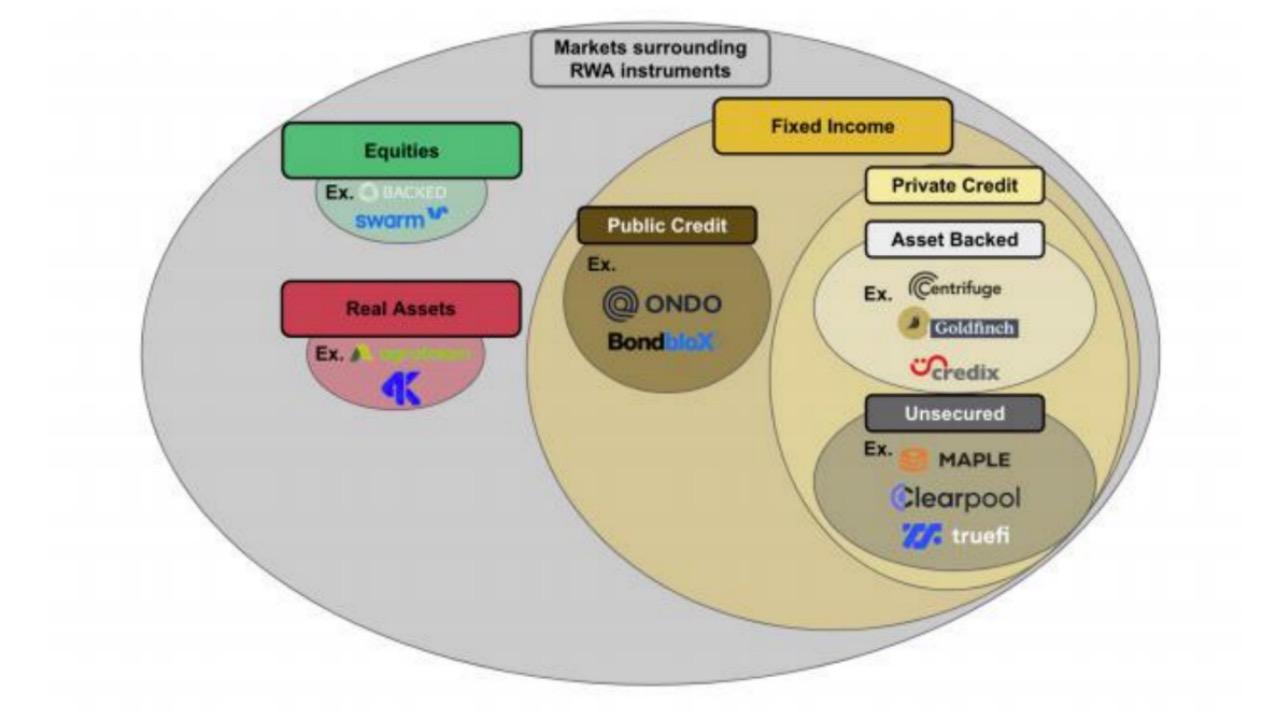

According to the classification of the Binance research report, there are currently three main markets in the RWA market: the DeFi market based on equity, the DeFi market based on real assets, and the DeFi market based on fixed income.

Among them , the DeFi market based on fixed income is currently the most important market for RWA , and this market mainly includes DeFi agreements that provide private credit and public bonds . Other physical assets such as real estate, artwork, and projects based on private equity or stock tokenization are relatively few or have limited activity.

private credit

In terms of private credit, one type is private credit agreements that require asset guarantees for Centrifuge, Goldfinch, and Credix, and the other type is private credit agreements that do not require guarantees, such as MAPLE, Clearpool, Truefi, and Ribbon Lend. At present, the seven largest RWA private credit agreements have a historical loan amount of more than 4 billion US dollars, active loans of nearly 500 million US dollars, and an average annual interest rate of over 12%.

Among them, Centrifuge was established as one of the earliest DeFi protocols involved in RWA. It is also the technology provider behind top protocols such as MakerDAO and Ave. Its investors include Distributed Capital, Coinbase Ventures, and IOSG Ventures. In December 2022, Centrifuge also announced the establishment of a $220 million fund in partnership with DeFi Fintech, MakerDAO and BlockTower Credit.

Centrifuge aims to help central enterprises obtain financing with a lower threshold, while allowing investors to obtain income from real assets. Centrifuge basically simulates the process of corporate credit in traditional finance, but uses DeFi+NFT to eliminate the participation of some intermediaries and the cumbersome process under the chain.

The process of financing on Centrifuge can be roughly summarized as follows: the borrower packages and uploads the real assets under the chain, generates a legally effective NFT for mortgage, and obtains interest-bearing ERC20 tokens, and investors can use DAI to purchase these interest-bearing tokens ERC20 tokens; the promoters get the redemption after the financing expires, and the investors get the benefits. The fund pool generated by interest-bearing ERC20 tokens is also divided into primary and advanced. Investors in the primary fund pool have high returns but higher risks, while advanced fund pools have relatively lower returns and risks.

Although Goldfinch, founded by former Coinbase employees, entered the market later than Centrifuge, it has obtained large-scale financing from well-known institutions with its innovative model, and its cumulative financing has reached 37 million US dollars. , Alliance DAO, BlockTower Capital and other well-known investment institutions, as well as angel investors such as Balaji Srinivasan also participated in the investment.

Goldfinch mainly provides loans to debt funds and financial technology companies, provides USDC credit lines for borrowers, and supports converting them into legal tender for borrowers. Goldfinch's model is much like a traditional financial bank, but with a decentralized pool of auditors, lenders, and credit analysts. Auditors for Goldfinch auditing borrowers must have staked governance token GFI. Goldfinch can provide a high rate of return. Due to the low mortgage threshold, Goldfinch's borrowers can pay 10-12% interest rate, and there are currently no bad debts.

Protocols such as Maple and TrueFi offer high active lending in bull markets due to their unsecured credit model compared to asset-backed private credit protocols. The difference between Maple and Goldfinch is that users are used as audits. Maple will appoint professional credit reviewers to strictly audit the credit of borrowers. However, under the unsecured mode, with the thunderstorm of Three Arrows Capital, FTX, etc., Maple has a bad debt of 52 million US dollars, and it is controversial that it is not centralized enough because borrowing requires KYC. Recently, Maple has also expanded the real asset-backed lending model to reduce risks.

public bonds

Compared with private credit agreements , on-chain bonds also usher in dividends due to the Fed's continued interest rate hikes . As mentioned earlier, in addition to traditional financial institutions all deploying U.S. bonds on the chain, there are also Flux Finance (developed by the Ondo Finance team) and TProtocol, Backed Finance, PV01, Kuma Protocol, Arca Labs, Stream Protocol, Cytus Finance, BondBlox, etc. Watch out for protocols in the field.

Among them, Ondo Finance, founded by former Goldman Sachs digital asset team member Nathan Allman and former Goldman Sachs technology team vice president Pinku Surana, has received $34 million in investment from investors including Pantera Capital, Coinbase Ventures, Tiger Global , Wintermute and other well-known institutions.

Ondo Finance can provide investors with four types of bonds, U.S. money market funds (OMMF), U.S. Treasury bonds (OUSG), short-term bonds (OSTB), and high-yield bonds (OHYG). Users can trade fund tokens after participating in the KYC/AML process and use these fund tokens in licensed DeFi protocols. Among them, OUSG is used on the largest scale. OUSG holders who have passed KYC can deposit their tokens into Flux Finance, a decentralized lending agreement developed by Ondo Finance, to lend their tokens for USDC leverage; non-KYC USDC holders can pass to KYC's Leverage Seeker offers loans to get yields as low as 50 basis points.

Tioga Capital investor Tzedonn mentioned in the latest report that the existing market value of bond tokens is 168 million US dollars, and Ondo (OUSG) has a 61% market share, of which 28% is deposited in Flux Finance. At present, the total supply of Flux Finance has exceeded 40 million US dollars, and the market value of OUSG has exceeded 100 million US dollars.

Real estate and other real asset markets and equity markets

Compared with private credit and public bonds, there are relatively few or limited projects based on real assets such as real estate and art, and based on private equity or stock tokenization. On the one hand, these assets can only be offered by registered and vetted exchanges, which are strictly regulated. On the other hand, they usually require off-chain physical ownership of the underlying asset class, which is more complex to operate. However, many protocols in this field are still exploring the introduction of more valuable real-world assets for Web3.

Among them, real estate-based tokenization has a growing development trend, and representative projects include Propy, ReaIT, Atlan, LABS Group, ELYSIA, Tangible, etc. The liquidity and transaction costs of real estate assets can be solved by tokenizing real estate. For example, real estate that needs to be bought and sold in sets can be sold in fragments, allowing ordinary investors to participate in the investment in the form of holding partial ownership.

In addition to real estate, the tokenization of carbon credit certificates and transactions on the blockchain is also an emerging market with potential, and representative projects such as Toucan, Flowcarbon, and Regen Network have emerged.

Is the RWA narrative too optimistic ?

Behind RWA's re-heating, it is also facing a lot of doubts. Many crypto people pointed out that many RWA projects are just DeFi derivatives with a new shell of the RWA concept, and the real resistance to connecting traditional finance and encrypted finance is too great.

The first is regulation . Many cryptographers have pointed out that tokenization means global transaction flow, while real assets are subject to geographical restrictions. The core of RWA lies in the credit mechanism. The key to promoting global circulation is the establishment of internationally accepted bills, and the relevant bills should also have the ability to enforce. But at present, the resistance of RWA in terms of compliance is still quite large.

Twitter user @0xChok, who has ever put stamps and other assets on the chain, also agrees with the above point of view. He said that at the beginning, he could only use the alliance chain to put stamps and other assets on the chain. , if it cannot be used globally, it will be difficult to really start liquidity.”

At the same time, a reality is that some asset protection mechanisms are also facing challenges . At present, many private loans such as MAPLE and TrueFi have experienced bad debts, but since the collateral is not a liquid ERC-20 token, liquidating these assets to recover the lender's capital will be much more troublesome than a loan using encrypted collateral.

In addition, there are also views that the attractiveness of RWA to crypto users may decline after DeFi picks up. Once the macro economy and DeFi pick up, RWA may not be attractive enough for crypto users, and it will be difficult to escape the fate of a flash in the pan.

Despite the challenges, infrastructures such as blockchains purpose-built for RWA are emerging. Due to regulatory and other restrictions, unlicensed public chains such as Ethereum may be difficult to meet the transaction of RWA assets, so the vertical application chain specially established for RWA came into being. For example, Polymesh, an institutional-grade blockchain tailored for regulated assets such as security tokens, recently announced Binance as one of its nodes. In addition, RWA vertical application chains such as MANTRA Chain, Realio Network, Provenance, and Intain are also worthy of attention.

At present, the RWA track is still in a very early stage, and it still needs to wait for the gradual improvement of supervision and infrastructure. However, the RWA narrative still has huge growth potential. While linked to real assets, it may also introduce more traditional users into the DeFi and Web3 world, truly reshaping the crypto market.