At present, the pledge rate of ETH has reached 19.6%, and the market value of ETH that has been pledged is 44.3 billion, of which the market value of LSTETH has reached 16.4 billion US dollars, and it is still growing. The release of Liquidity for such a large-scale interest-earning asset undoubtedly corresponds to a huge market demand; currently The development of USD Stablecoin mortgage lending agreements based on LST assets is relatively mature, and the competition pattern of the track is gradually stabilizing, such as CrvUSD, Prisma, Raft, Gravita, etc.; at a very early stage. Since WrapETH and the underlying LST assets have price fluctuations in the same direction, this type of product can hedge the risk of collateral price fluctuations to achieve no-liquidation loans while accumulating leveraged positions of yield. (For details on the impact of the expansion of LST asset scale on the lending track, please refer to "Inventory of Current Early LSDFi Potential Projects" )

ZeroLiquid is currently in the testnet stage, allowing users to mint zETH with a maximum of 50% of the LTV mortgage LST (when users deposit ETH, ZeroLiquid will convert it to LST). zETH is a loan certificate whose price is anchored to ETH. Since it has price fluctuations in the same direction as ETH, ZeroLiquid can Achieve no liquidation, hedge the price fluctuation risk of part of the borrowing, and do more interest rate exposure of ETH pledge. ZeroLiquid does not charge borrowing fees. The agreement income comes from 8% of the collateral LST interest, and 55% of the agreement income is allocated to ZERO single-currency pledge users; the above-mentioned parameter ratios can be adjusted through governance.

Project risk: The ZeroLiquid team is anonymous, the development progress is delayed, and the product is still in the testnet stage; according to the information announced by the team in Telegram, it is expected that the product code will be audited in early July; the cooperative audit companies are code4arena and immunify, both of which are in the industry The leading audit agency has participated in the code audit of many well-known projects such as ENS, BLUR, and GMX; what needs attention is that ZeroLiquid has not yet been seen in the pre-audit list disclosed by code4arena.

1. Specific product mechanism

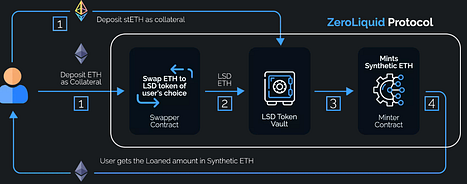

ZeroLoan module — minting zETH:

ZeroLoan is the basic functional module of the ZeroLiquid protocol. Users can provide LST or assets that can be converted into LST as collateral through ZeroLoan, and lend synthetic assets issued by the agreement at 50% LTV and 0 borrowing rate (for example, users can borrow up to 0.5 zETH by providing 1 ETH or stETH). At the same time, the agreement regularly collects the interest generated by LST to repay the user's debt according to the user's deposit ratio; the user can also repay at any time to get back the collateral.

ZeroLoans provides users with a relatively flexible borrowing tool, which allows users to enjoy the interest income brought by the collateral while obtaining part of the Liquidity. At the same time, due to the price fluctuation of the debt and the collateral in the same direction, there is no risk of liquidation of the debt; because ZeroLoans accepts Collaterals are all interest-earning assets, and have the characteristics of self-repayment without liquidation, so the product function of ZeroLoans can also be understood as the early withdrawal of collateral income.

ZeroLoan function module flow chart

Source: zeroliquid.gitbook, LD Capital

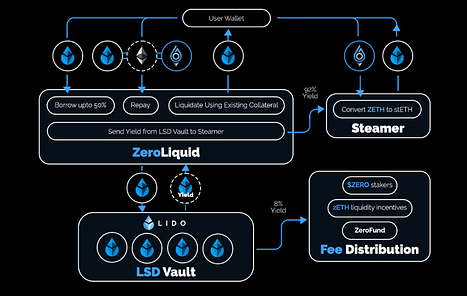

Steamer module — maintains the ZETH peg:

The Steamer module is the key to the smooth implementation of ZeroLiquid protocol functions and the adoption rate of the protocol. Steamer allows any user (with or without an outstanding debt position) to redeem zETH for stETH at a 1:1 ratio. The stETH in Steamer comes from the interest generated by the user’s collateral minus the protocol fee (8%). Therefore, when the inflow of funds from Steamer is greater than the outflow of funds used to redeem zETH, the scale of Steamer will grow, and there will be no secondary market for zETH Discount; but when the outflow of Steamer’s funds is greater than the inflow, the redemption of zETH will take a while, and zETH may also experience different degrees of discount in the secondary market. The key to avoiding a large number of redemptions caused by the discount of zETH lies in the expansion of zETH's use cases. The protocol will use tokens and 35% of the protocol revenue to provide incentives for zETH/ ETH LPs; use the protocol POL (protocol-controlled ZERO/ ETH LP and future zETH / ETH LP) and Zero Fund income to maintain the anchor of zETH, while actively promoting the integration of zETH with other protocols.

In general, Steamer provides Liquidity for the 1:1 exchange of zETH and stETH for market arbitrageurs to level the price and maintain the anchor. Recently, there have been many LSDFi agreements of Liquidity Fork in the market. The rigid payment Liquidity of this type of agreement is provided by some borrowers, and additional incentive costs need to be paid for this agreement. In contrast, the arbitrage model of ZeroLiquid is more concise and has fewer participants. The cost of the agreement is low, but correspondingly, the risk that the secondary market discount cannot be quickly leveled due to insufficient Liquidity has increased.

Steamer function module flow chart

Source: zeroliquid.gitbook, LD Capital

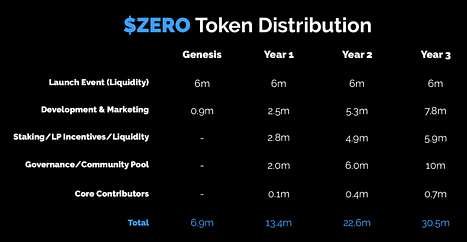

2. Token distribution

ZERO tokens were sold on the Uniswap platform in the form of self-funding on March 19, with a total of 30.5 million tokens (the initial total was 100 million, and 69.42% were destroyed after the community proposal), of which 6 million To provide initial Liquidity, 13.7 million tokens belong to the community, 1 million tokens belong to the national treasury, and 700,000 tokens belong to core contributors. The initial circulation in the secondary market is 6.9 million, and the rest will be gradually vested within 3 years; the team has already executed the first token destruction, destroying 3.49 million ZERO, and the current circulation of 7.84 million corresponds to a market value of about 3.5 million US dollars (Data websites such as Coingecko do not count the destroyed part, resulting in data distortion).

Distribution and unlocking of ZERO tokens

Source: zeroliquid.gitbook, LD Capital

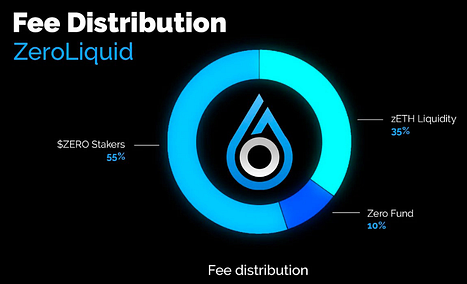

3. Agreement income distribution

The agreement does not charge borrowing fees, and 8% of the collateral income is charged as the agreement income. 10% of protocol income is allocated to ZeroFund for maintaining anchoring and protocol development; 35% is allocated to zETH/ ETH LP incentive Liquidity; 55% is allocated to ZERO single currency pledgers. Therefore, ZERO has the right to distribute dividends while having the right to govern the agreement. Simple calculation: If the protocol has a TVL of 100 million US dollars (currently LSTETH has a market value of 16.4 billion US dollars), assuming that the ETH pledge yield is 5%, the estimated annual income of ZERO pledgers is 220,000 US dollars.

Agreement income distribution

Source: zeroliquid.gitbook, LD Capital

4. Comparison of similar protocols

ZeroLiquid's product model is similar to Curve's ecological projects Clever and Alchemix. The main difference between Zeroliquid and Clever is that the underlying collateral of Clever is mainly CVX(a small number of Stablecoin) while the underlying collateral of Zero is ETH . market value of 221.2 billion US dollars, LSTETH market value of 16.4 billion US dollars), the current market value of Clev is 3.4 million US dollars and is similar to ZERO; but if the ZeroLiquid product is successfully launched, its growth potential is undoubtedly greater than Clever. The main difference between Alchemix and ZeroLiquid is that its protocol tokens do not have dividend rights, while ZERO single currency pledge can share protocol income. Currently, the deposit volume of LST/ ETH in Alchemix is 42.7 million US dollars, and the circulation market value of ALCX is 26.5 million US dollars, which is about ZERO 7.5 times.