Original Author: First Class Warehouse

Original source: medium

Radiant Capital is a cross-chain DeFi lending protocol that uses LayerZero as a cross-chain infrastructure to achieve full-chain leveraged lending and composability. At present, Radiant, as an early project in the cross-chain lending track, has a certain first-mover advantage. And as Radiant fully integrates LayerZero's full-chain technology in V3 and V4, it is expected to bring a new inflection point to the project and further push its full-chain lending to the market, which is worthy of attention.

Investment Summary

With the continuous development of the public chain and the second-tier track, the mobility between ecology will inevitably be further divided. The leading lending project Compound Finance previously launched Gateway to provide a testnet for cross-chain lending; Aave will also support cross-chain lending in the V3 version. Recently, Aave V3 proposals have passed V3 Portals and will add Hashflow/Wormhole and Stargate as "whitelists" Bridge” voting; Uniswap, Sushiswap and other mainstream DEXs are deployed on multiple chains at the same time. The entry of many old DeFi blue chips also shows that they do not want to miss the early industry dividends in the multi-chain market.

Radiant Capital is a cross-chain DeFi lending agreement. The team positions itself as an omnichain lending agreement, aiming to realize leveraged lending and composability between different chains, so that users can use the DeFi protocol it supports Leverage is obtained in the platform, which simplifies the operation of cross-chain lending and borrowing of assets between different chains.

The highlights of the Radiant Capital project are:

1) As the first cross-chain lending protocol launched in the LayerZero ecosystem, Radiant has completed the cold start of early projects and captured a certain scale of market share and user groups, which has a first-mover advantage in this track.

2) The improvement of the Radiant V2 version has extended the life cycle of the project and alleviated the inflation problem of the $RDNT token. The design of dLP is also expected to bring more liquidity to the protocol, but its impact is long-term The process remains to be further observed.

3) Based on LayerZero’s Radiant, at the level of cross-chain lending, due to the sharing of a token standard (OFT), liquidity sharing can be realized on all LayerZero-supported chains without relying on external third-party cross-chain bridges for additional trust assumptions . In the future, if Radiant can make a good security assumption between the oracle and the relay in its V3 and V4 versions, and realize the de-trust at the contract level, then in terms of asset cross-chain security assumptions, compared with the current mainstream on the market relying on the first The three-party cross-chain bridge may be more advantageous in realizing asset cross-chain.

The risks of this project are:

1) The team is anonymous. Although Radiant has briefly introduced the team in its official documents and in the community, the resumes of the specific members have not been disclosed.

2) Radiant does not have any innovative technical advantages in the lending field alone, and it mainly follows the design of Aave. With the subsequent launch of Aave V3's own cross-chain lending function - Portal, it will have a certain impact on Radiant.

3) Looking back at Radiant’s development history, a large part of the factors are inseparable from the high amount of token incentives in the protocol. In addition, it is also related to many factors such as the recovery of the market at the macro level, the hot Arbitrum ecology, and the expectations of the entire LayerZero chain. It also makes Radiant's expectations a bit stretched at the moment. If you just look at the FDV / TVL ratio, at present (April 25, 2023) Aave is 0.29, Compound is 0.3, and Radiant is about 1.68. This shows that Radiant's full-flow market cap is higher than its TVL. Compared with lending protocols Aave and Compound, it can be said that Radiant's current market cap is inflated.

4) Based on the underlying architecture of LayerZero, Radiant Capital uses Chainlink to ensure the accuracy of oracle quotations in terms of oracle machines. The choice of relay (Relay) has not been disclosed for the time being, and there are still certain security risks.

On the whole, although Radiant Capital is still facing some problems, with LayerZero's full-chain technology and the existing first-mover advantages of the project, there is still a chance to make more achievements in the field of cross-chain lending in the future, so it is worthwhile focus on.

Note: The [Focus] / [Not concerned] in the final evaluation of the first-class warehouse is the result of a comprehensive analysis of the current fundamentals of the project according to the first-class warehouse project evaluation framework, rather than the prediction of the future price rise and fall of the project token. There are many factors that affect the price of tokens, and the fundamentals of the project are not the only factor. Therefore, just because the research report is judged as [Not concerned], it cannot be assumed that the project price will definitely fall. In addition, the development of blockchain projects is dynamic. If the fundamentals of a project judged to be [not concerned] undergo major positive changes, we may adjust it to [concern]. If there is a major vicious change in the project of [Focus], we will warn all members and may adjust it to [Not Concerned].

1. Basic overview

1.1 Project Introduction

Radiant Capital is a cross-chain DeFi lending protocol. The team positions itself as an omnichain lending protocol, aiming to realize leveraged lending and composability between different chains.

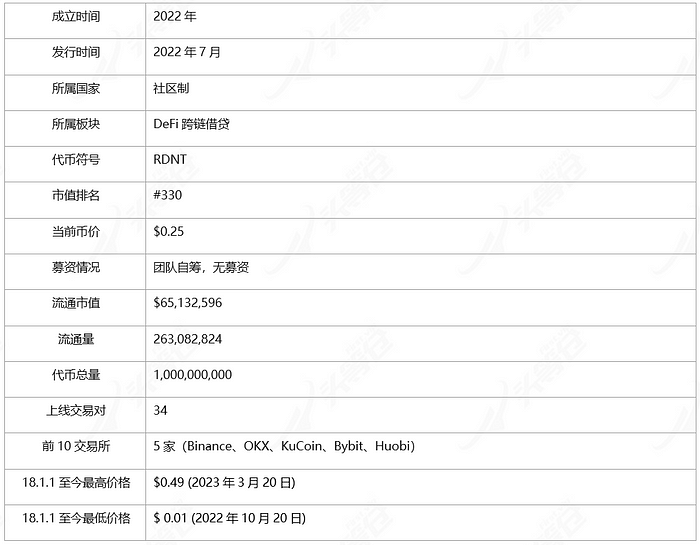

1.2 Basic information [1]

2. Project details

2. Project details

2.1 Team

Radiant Capital’s official documents disclose 16 team members, but only their names and responsible positions, and the resumes of the team members are not disclosed. It is essentially an anonymous team [2] .

In addition, Radiant mentioned in an official blog post in April this year that Radiant Capital has a team of 14 people who previously came from Morgan Stanley, Apple and Google, and the team members have been engaged in the DeFi industry since early summer 2020 , and there are many team members who have been engaged in cryptocurrency since 2015 [3] .

If the team members of a blockchain project are anonymous, there may be the following risks:

1) Trust issues: Anonymity of team members may cause distrust from investors and users. Because the anonymous team cannot provide personal identification and background information, this may lead investors and users to think that the project may be a scam or fraud project, thereby reducing their trust in the project.

2) Responsibility issues: Anonymous team members may allow team members to evade responsibility. If there is a problem with the project, it will be difficult for users and investors to find relevant team members to solve the problem.

3) Lack of transparency: Anonymous teams usually do not disclose information such as their experience, skills, and educational background, which makes it impossible for investors and users to determine the credibility of the project and the professional level of the team.

4) Marketing issues: Anonymous teams may face obstacles in publicity. Because investors and users usually prefer to cooperate with real and transparent teams, if team members are anonymous, they may think that the project does not have enough integrity and credibility to attract enough investment and users.

To sum up, anonymous teams may have adverse effects on the development of blockchain projects. Therefore, investors and users should carefully consider whether to participate in projects developed by anonymous teams.

2.2 Funding

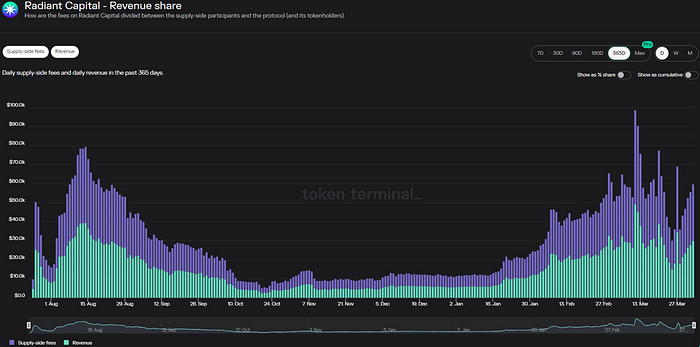

Since the establishment of the Radiant Capital project, there has been no IDO, private equity or venture capital participation. All the operating costs of the early project are raised by the team members themselves. The development of the Radiant protocol has successfully completed the early cold start and attracted a certain user base, which can bring stable income to the protocol (as shown in Figure 2-1 below), thereby covering a certain amount of operating costs. However, the specific situation of the current treasury of the agreement is unknown.

Figure 2–1 Radiant Capital Revenue Sharing [4]

Figure 2–1 Radiant Capital Revenue Sharing [4]

In addition, Radiant Capital, as a full-chain lending agreement on Arbitrum, received 3.34 million $ARB tokens in the previous Arbitrum DAOs Airdrop event. As of now (April 7, 2023), the value is nearly 400 million dollars, the seventh largest amount among DAOs that received airdrops .

2.3 Code

According to the team, Radiant Capital’s code is built on top of the 2021 Fantom lending protocol Geist, which in turn was built using the Aave codebase [5] .

The Radiant Capital codebase is not yet open source. However, according to the team, Radiant v1 has been audited by PeckShield and Solidity Finance, and Radiant v2 (mainly composed of the same codebase as Radiant v1) has also undergone multiple comprehensive audits with Peckshield and Zokyo. At the same time, Radiant also hired BlockSec to conduct white hat attacks to test the security of the network. The full reports of these audits are available through official Radiant documentation.

Radiant Capital is currently cooperating with Immunefi to launch a bug bounty program with a reward of up to $200,000. In addition, Radiant will use OpenZeppelin Defender's security system to monitor the network 24/7 and respond instantly to potential attacks/risks.

2.4 Products

Radiant Capital is a cross-chain DeFi lending agreement. The team positions itself as an omnichain lending agreement, aiming to realize leveraged lending and composability between different chains, so that users can use DeFi agreements supported by it Leverage is obtained in the platform, which simplifies the operation of cross-chain lending and borrowing of assets between different chains.

2.4.1 Operation process

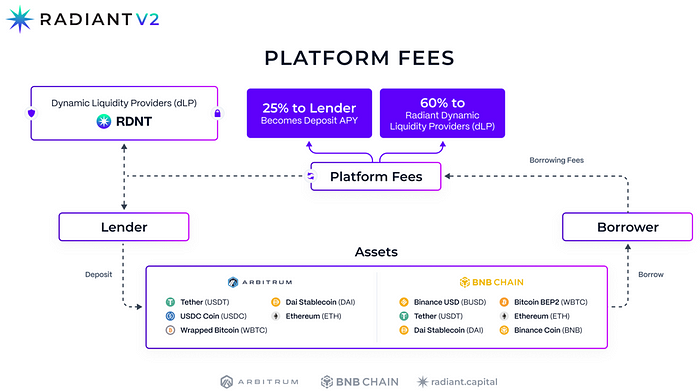

Figure 2–2 Radiant Capital platform fee structure [6]

Figure 2–2 Radiant Capital platform fee structure [6]

The operating mechanism of Radiant Capital can refer to Figure 2-2 above. It is essentially similar to the lending agreements currently on the market (such as: Aave, Compound, etc.). The collateral is deposited on the chain, and then the loan is carried out on the B chain.

Radiant's overall operating mechanism is relatively simple: when users need to use Radiant's cross-chain lending service, they need to deposit certain assets on the chains supported by the platform (currently the platform only supports two chains, Arbitrum and BNB Chain), to become a dynamic flow Property Providers (dLPs), who can then lend out the assets required by the target chain. The distribution of fees earned by the Radiant V2 protocol: 60% is allocated to dynamic liquidity providers (dLP), 25% is allocated to depositors (Lenders), and 15% is allocated to designated DAO-controlled operating wallets.

Additionally, Radiant offers a one-click revolving feature where users can increase the value of their collateral (up to 5x leverage) through multiple automatic deposit and borrow cycles.

For example, users can deposit ETH, WBTC or other corresponding assets as collateral on Arbitrum through Radiant, and then lend BNB on BSC to amplify their own leverage. In the process of borrowing and lending, users do not need to perform asset cross-chain operations (for example, in this example, there is no need to cross-chain their ETH on Arbitrum to BSC in advance). That is to say, from the user's point of view, the operation of cross-chain lending can be completed on different chains or L2 without cross-chaining assets to other chains.

2.4.2 Radiant V2

Figure 2–3 Radiant V2 improvements [7]

Figure 2–3 Radiant V2 improvements [7]

Figure 2-3 above shows the V2 version improvement process released by Radiant Capital on January 16, 2023.

Specifically, compared with Radiant V1, the changes in Radiant V2 mainly focus on two aspects:

1) Economic model

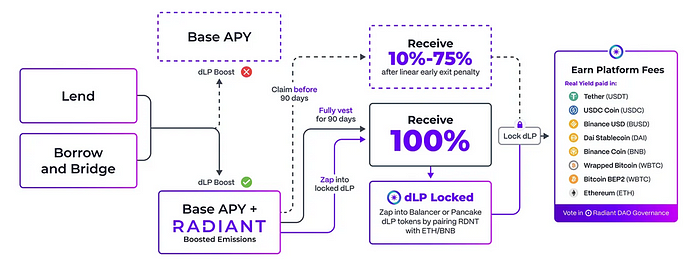

In order to solve the inflation problem of $RDNT, Radiant introduced the concept of Dynamic Liquidity Provisioning (dLP, Dynamic Liquidity Provisioning) . In the V2 version, users who simply deposit can only get the basic interest rate, and can no longer get the token reward of $RDNT . If you want to get $RDNT token rewards, you need to lock dLP tokens that are at least 5% of the total deposit value (because the value of LP is dynamically changing, it is called dynamic liquidity supply). This means that for a user’s USD equivalent deposit of USD 100, the user needs to hold at least USD 5 equivalent in dLP tokens in order to earn $RDNT token incentives.

Radiant currently offers two locked LP pools:

• Arbitrum: Balancer 80/20 composition (80% RDNT & 20% ETH)

• BNB Chain: Pancakeswap 50/50 (50% RDNT & 50% BNB)

As an example, User A deposits $1 million on Radiant and locks up $0 in dLP tokens. Then the user can only get the basic interest rate (APY), and there is no liquidity mining reward of $RDNT.

User B deposits $1,000 on Radiant and locks up $50 worth of RDNT/BNB dLP. Then user B will be eligible to receive $RDNT liquidity mining rewards (meeting the minimum 5% lockup threshold).

A simple understanding is the V2 version. Users not only need to provide LP, but also need to stake a certain ratio of RDNT/ETH or RDNT/BNB dLP to get $RDNT token rewards.

dLP currently supports a lock-up period of 1–12 months. The longer the lock-up period, the higher the corresponding token incentives. The token rewards obtained will be released linearly within 3 months. During this period, if users do not want to wait, they can also apply for early withdrawal penalties to obtain 10% - 75% of token rewards (as shown in Figure 2-3 above) .

Figure 2–4 Radiant official website page

Figure 2–4 Radiant official website page

As shown in Figures 2–4 above, Radiant’s official website shows that for users who only provide deposits but do not lock in dLP, they can only obtain the normal market lending rate on the Radiant platform (the red part in the above figure). For users who meet the dLP lock-up conditions, they will receive additional $RDNT token incentives (APY is the blue and purple part in the above picture).

Overall, the dynamic liquidity provision (dLP) launched by Radiant requires depositors on the platform to provide a certain percentage of liquidity if they want to receive $RDNT token rewards. On the one hand, it endowed $RDNT with more demand for tokens and increased the lock-up volume of its tokens. On the other hand, it also helps to improve the liquidity of $RDNT, attract more medium and long-term liquidity contributors, and realize a symbiotic development relationship with the platform.

In order to facilitate the user experience, Radiant has added a "Zap" function to almost every component introduced in the V2 version: adding liquidity, revolving loans, adding dLP, and one-click revolving loans and locking 5% of dLP.

In addition, in order to maintain the sustainability of the economic model, in the Radiant V2 version, Radiant has extended the original 2-year token release cycle to 5 years (July 2027). Radiant also modified the vesting time of Radiant V1's reward and punishment mechanism from 28 days to 90 days. Users who apply for withdrawal in advance can only get a linear reward of 10%-75%. Users who have not withdrawn rewards after the expiration date will be removed from the pool and will no longer receive incentives. Users can activate the re-lock option in the interface. The agreement fee has also been changed accordingly, and the dynamic liquidity provider (dLP) has become the biggest beneficiary. See the above description for details. The overall design is more reasonable than the V1 version.

2) Cross-chain mechanism

One of the first tasks of Radiant V2 is to convert the RDNT token standard from ERC-20 to LayerZero OFT (Omnichain Fungible Token) format. In Radiant V1, its cross-chain function mainly relies on Stargate’s cross-chain routing. In version V2, Radiant first replaced the Stargate routing interface of its native token $RDNT with LayerZero’s OFT cross-chain standard. This can help $RDNT deploy to the new chain faster, and control the ownership of the cross-chain contract by itself. The specific mechanism of LayerZero OFT is detailed in the following technical section.

summary:

Previously, as the price of $RDNT continued to rise, coupled with the incentives of liquidity mining, Radiant’s TVL was in a period of continuous rise. But historical experience also tells us that most liquidity mining can only bring false prosperity to the early stage of the project. As the rate of return declines, the competitiveness of the project will also decline. Of course, Radiant’s project team is also aware of this problem, and in the many improvements of the V2 version, a series of measures such as extending the release cycle of $RDNT tokens, adjusting fee distribution, modifying the attribution time of the reward and punishment mechanism, and setting dynamic liquidity supply , to achieve sustainable development of the project.

Theoretically, Radiant V2 alleviates the inflation problem of $RDNT tokens to a certain extent, and the design of dLP is also expected to bring more liquidity to the agreement, but its impact is a long-term process and cannot be effective in the short term Verification remains to be further observed. For the subsequent development of the project, it is possible to continue to follow up the overall liquidity within the ecosystem.

In addition, for a cross-chain lending agreement, the improvement and innovation of the economic model can only be regarded as the icing on the cake. In essence, the success of the agreement depends on whether it can generate actual loan demand and effectively retain users. Just like the current leading lending protocol Aave, even without token incentives, its overall scale is still far ahead of latecomers.

2.5 Technology

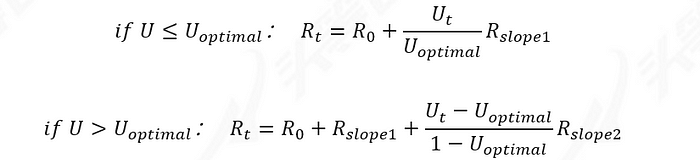

2.5.1 Interest Rate Model

Borrowers need to pay an interest fee when lending assets, and this fee will be accumulated into the user's loan value. Radiant Capital's interest rate model refers to Aave's design (the document part also directly quotes Aave's interest rate model formula), and adopts a dynamic interest rate model, which is essentially a general model of a lending agreement. The core idea is to maintain the borrowing demand of specific assets at within the optimum range.

Radiant's rate algorithms are calibrated to manage liquidity risk and optimize utilization. The borrowing rate is derived from the utilization rate "U". U is an indicator of the funds available in the pool.

The model followed by the interest rate Rt:

Radiant's interest rate model supports liquidity through user incentives and manages liquidity risk in the protocol. The interest rate will change with the utilization rate of the loaned assets. When the utilization rate reaches a critical level, the model will adjust the interest rate to change user behavior and bring the utilization rate back to the optimal range:

Radiant's interest rate model supports liquidity through user incentives and manages liquidity risk in the protocol. The interest rate will change with the utilization rate of the loaned assets. When the utilization rate reaches a critical level, the model will adjust the interest rate to change user behavior and bring the utilization rate back to the optimal range:

If the utilization rate U is lower than the value of the optimal utilization rate ( ), then the borrowing rate will rise slowly with the utilization rate, attracting users to borrow money through lower borrowing costs;

If the utilization rate is higher than the optimal utilization rate ( ) value, then the borrowing rate will rise rapidly, encouraging lenders to deposit more funds. At the same time, due to the high cost of borrowing, borrowers will also repay their debts in a timely manner.

Since this part of Radiant completely refers to the design of the Aave contract, more details can be found in the official document of the Aave interest rate model [8] .

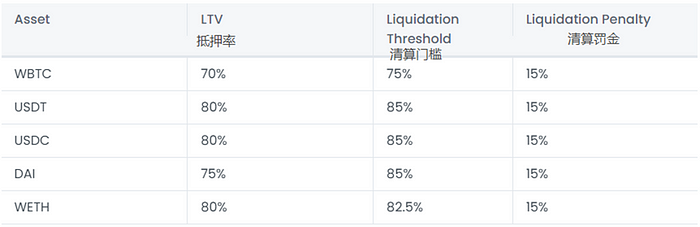

2.5.2 Clearing Mechanism

Radiant’s liquidation mechanism is still similar to Aave’s, using the Health Factor standard to determine whether users will be liquidated. When the health coefficient is less than 1, that is, when the collateral value < the loan/debt value, the user's collateral will be liquidated.

Collateral Value = Collateral * Mortgage Rate, Debt Value = Borrowing Value / Lending Rate

Once liquidation is triggered, the liquidator can take over the debt and collateral of the borrower, help repay the debt and receive a discounted collateral in return (also known as a liquidation reward). Like Compound and Aave, in Radiant the liquidator liquidates up to 50% of the borrower's debt at a time.

Figure 2–5 Radiant Capital Market Risk Parameters [9]

Figure 2–5 Radiant Capital Market Risk Parameters [9]

Liquidation incentives. In Compound and Aave, in order to motivate liquidators to participate in liquidation, a 5%-10% discount on the borrower’s collateral is usually provided as a liquidation reward. In Radiant, if the borrower is liquidated, it needs to pay a liquidation penalty of 15% of the bad debt of the collateral. Half of the penalty (7.5%) will be distributed to the liquidator as a bonus, and the other half (7.5%) will flow into the team treasury. However, it should be noted that this design may lead to the rush of liquidation transactions, and large depositors may need to bear higher losses. Therefore, in order to ensure that the liquidation is completed as soon as possible, the liquidator often chooses to pay a relatively high gas fee.

For liquidation scenarios in Radiant, for example:

Suppose user A deposits 10 ETH and lends DAI worth 5 ETH in Radiant. If during the borrowing period, the price of ETH plummets, causing the health factor of user A to be lower than 1, his loan will be liquidated.

At this time, the liquidator can repay up to 50% of the single loan amount of user A (in this example, DAI worth 2.5 ETH). In return, liquidators can claim a single collateral, ETH, with a 7.5% liquidation reward. The liquidator requests to repay user A's bad debt (DAI worth 2.5 ETH) with 2.5 + 0.1875 ETH (0.1875 ETH is rewarded by the agreement with a 7.5% liquidation claim and a total penalty of 15%).

After liquidation, User A is left with 7.125 ETH (10–2.5–0.1875–0.1875 ETH) of collateral and a DAI loan worth 2.5 ETH.

2.5.3 RDNT OFT (Omnichain Fungible Tokens)

As we mentioned above, Radiant V2 converts the RDNT token standard from ERC-20 to LayerZero OFT (Omnichain Fungible Token) format.

OFT (Omnichain Fungible Tokens)

OFT is a wrapped token that allows free flow between Chains supported by LayerZero. OFT is a shared token standard on all LayerZero supported chains, which can be seamlessly transferred on these chains without adding additional costs (such as: the cost of cross-chain assets). When OFT is transferred between chains, it will be directly destroyed on the source chain through the token contract, and the corresponding token will be minted on the target chain (destroy and mint mechanism).

Currently Radiant V2 only supports the OFT form of its native token $RDNT, which will enable $RDNT to be combined and fragmented on the chains supported by LayerZero, thereby reunifying the liquidity of assets. This means that $RDNT has an elastic supply on each chain. By deploying on more chains and Dapps, more complex strategies and high-frequency arbitrage opportunities can be created around $RDNT, which broadens the use of tokens Scenes.

Subsequent Radiant also plans to get rid of the dependence on the third-party cross-chain bridge (Stargate) in the V3 version, and fully integrate LayerZero to realize the seamless experience of Radiant cross-chain and support cross-chain lending of more EVM chains. The biggest advantage of integrating LayerZero is that it solves the problem of fragmentation to a certain extent, and can use a unified token standard on multiple chains (of course, the premise is that LayerZero can be widely expanded). And this is also conducive to the frictionless mortgage and loan of any native Token of the network supported by LayerZero in the process of Radiant cross-chain lending.

First-class warehouse note: LayerZero is a full-chain interoperability protocol designed for cross-chain transfer of lightweight information without running nodes on connected chains, by relying on oracles and repeaters , on different chains Transfer messages between endpoints [10] . Based on the underlying architecture of LayerZero, Radiant Capital uses Chainlink to ensure the accuracy of the oracle quotes. The choice of relay (Relay) has not been disclosed for the time being. The editor speculates that the subsequent V3 version may first choose the middle Repeater. Therefore, if cross-chain communication is to be performed on Radiant, the message will be forwarded to the target chain only after the oracle machine (Chainlink) and the relay have successfully verified each other.

Summarize:

Looking back at Radiant’s early successful launch, a large part of the factors are inseparable from the high token incentives of the protocol. In addition, it is also related to many factors such as the recovery of the market at the macro level, the hot Arbitrum ecology, and the expectations of the entire LayerZero chain. When the Radiant protocol initially achieved certain results, the team itself realized that the initial high token incentives were unsustainable, which led to excessive inflation. Therefore, in the subsequent V2 version, the shortcomings compared with the V1 version are also Corresponding improvements have been made, and the overall design is more reasonable.

For Radiant, it is undoubtedly the completion of an early successful project launch. But in terms of technology alone, Radiant does not have any innovative technical advantages in the lending field. In terms of products, it mainly follows the design of Aave. The inflection point of the project in the future lies in whether it can make full use of LayerZero's full-chain technology, further push its full-chain lending to the market, and capture more real user groups.

3. Development

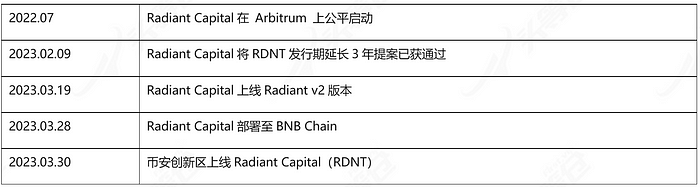

3.1 History

Table 3–1 Major Events of Radiant Capital

Table 3–1 Major Events of Radiant Capital

3.2 Status

3.2.1 Business data situation

As the first officially launched cross-chain lending project in the LayerZero ecosystem, Radiant Capital has already delivered a good answer.

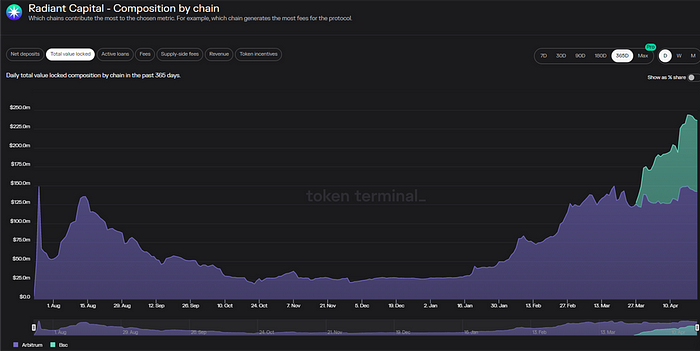

Figure 3-1 Radiant TVL scale [11]

Figure 3-1 Radiant TVL scale [11]

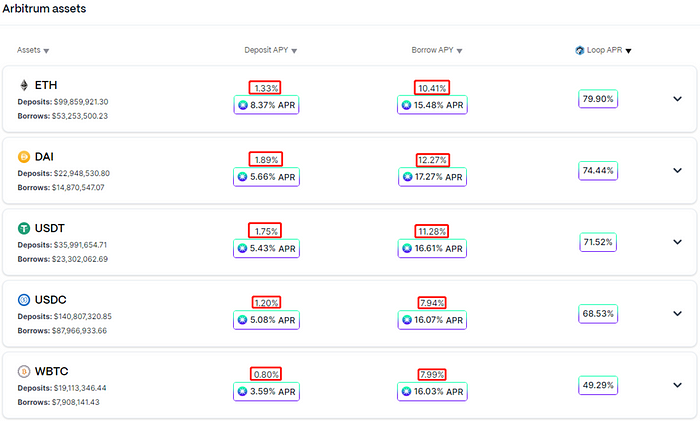

According to the Token Terminal data port, as of April 21, 2023, the TVL on Radiant is about 236 million US dollars, of which the TVL on the Arbitrum chain is 142 million US dollars, and the TVL on the BSC chain is 93.9 million US dollars.

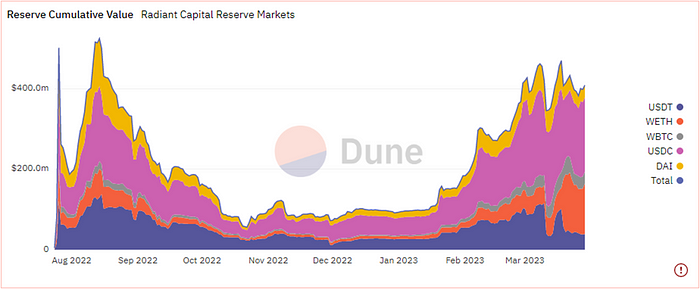

Figure 3–2 Radiant Capital Accumulated Reserves [12]

Figure 3–2 Radiant Capital Accumulated Reserves [12]

According to the Dune Analytics data port, as of March 30, 2023, the total deposit amount (Ether chain) on Radiant is about 435 million US dollars, including USDC 190 million, USDT 36.39 million, DAI 34.68 million, WETH 127 million USD, WBTC USD 46.57 million. The combined proportion of the three major stablecoins in deposits reached 60.09% .

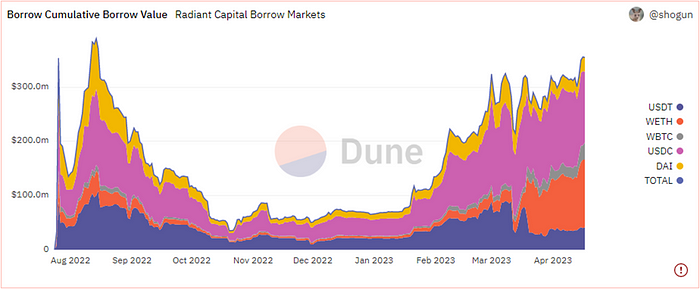

Figure 3-3 Radiant Capital Borrowing Situation

Figure 3-3 Radiant Capital Borrowing Situation

As of March 30, 2023, the total borrowings on Radiant are approximately US$296 million, including US$141 million in USDC, US$37.1 million in USDT, US$22.78 million in DAI, US$792.1 million in WETH, and US$16.39 million in WBTC. The three major stablecoins accounted for approximately 67.71% of borrowings.

Overall, Radiant's capital utilization ratio (total borrowings/total deposits) is approximately 68.05%, meaning that for every $100 deposited in Radiant, $68.05 is lent out. According to official documents, when the loan occurs, the LTV of USDC, USDT, and DAI are all 80%, that is, for every USD 1 deposited in USDC and USDT, a maximum of USD 0.8 of assets can be borrowed. The capital utilization ratios of the three major stablecoins have almost reached the upper limit, indicating that a considerable part of the funds in Radiant are for the purpose of liquidity mining, rather than real borrowing needs .

From another perspective, although a considerable part of the funds in Radiant are for the purpose of liquidity mining, it has also brought actual benefits to the project. The official blog post in April 2023 shows that the Radiant protocol has accumulated Generated approximately US$ 7 million in revenue [13] .

First-class warehouse note: Since the above-mentioned Radiant Capital accumulated reserve data of Dune is only disclosed until March 30, 2023, for the convenience of comparison, the editor also took the data on March 30 for the loan data on Radiant. But combined with the latest data, as of April 19, 2023, the total borrowing on Radiant is about 355 million US dollars, including USDC 131 million US dollars, USDT 41.36 million US dollars, DAI 26.33 million US dollars, WETH 123 million US dollars, WBTC 3,146 US dollars Ten thousand U.S. dollars. The three major stablecoins accounted for approximately 55.91% of borrowings. Compared with the data 20 days ago, there is a certain difference, so the editor speculates that the main reason for the difference is due to the fact that with the rise of market fluctuations, there is a certain amount of actual loan demand in Radiant (especially from the above figure 3- 3 It can be seen that the borrowing demand of WETH has increased significantly), so the proportion of stablecoin lending has relatively decreased.

At present, in Radiant, deposits and loans of USDC, USDT, DAI, ETH, WBTC, ARB, and wstETH 7 assets can obtain RDNT tokens through liquidity mining, and the rate of return for each asset is higher than The interest that needs to be paid on the loan will give the funds the motivation to mine liquidity.

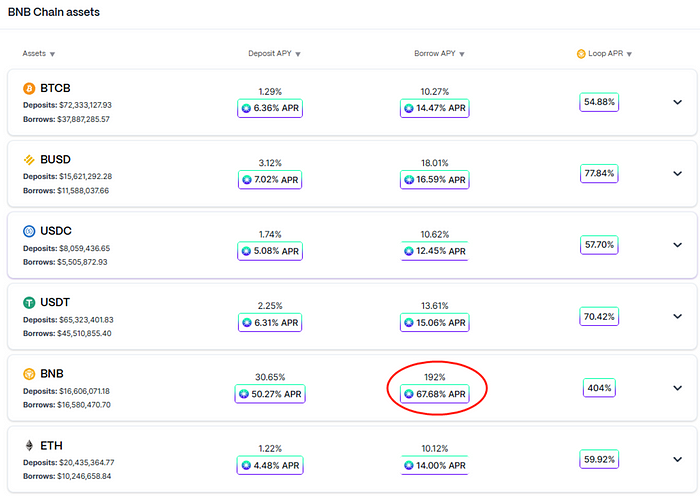

However, it should be noted that due to the enthusiasm of the previous Binance Launchpad activities (commonly known as new campaigns) [14] , the demand for BNB in the market has increased, and it has also led to an increase in the BNB lending rate on the Radiant market. As of April 23, 2023, the current borrowing rate of BNB on Radiant is as high as 192%, but the yield of BNB borrowing and mining is only 67.68% (as shown in Figure 3-4 below) [15] . So currently, for users, revolving BNB loans on Radiant is a loss of money. Therefore, users still need to do research in advance before participating in mining.

Figure 3-4 Radiant’s lending rate and mining yield on the BSC chain

Figure 3-4 Radiant’s lending rate and mining yield on the BSC chain

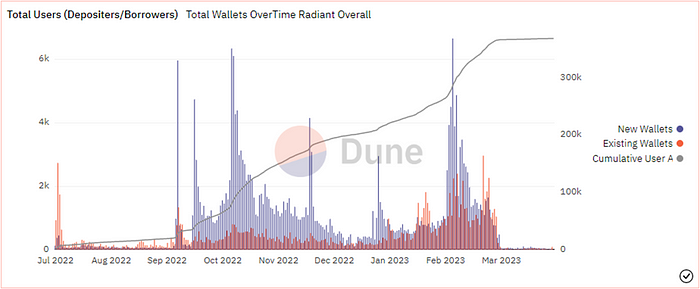

3.2.2 Users

Figure 3–5 Radiant Capital users

Figure 3–5 Radiant Capital users

In terms of users, according to the data port of Dune Analytics, since the protocol went online, after a slow transition in the early stage, the number of Radiant users will rise rapidly in 2022 Q4 and 2023 Q1 Arbitrum boom respectively. However, combined with Figure 3-5 above, we can also clearly see that after Radiant launched the V2 version on March 19, 2023, the growth rate of its user numbers slowed down significantly (the black broken line in the above figure), the number of new wallets and the number of existing wallets Both dropped from the original hundreds to ten figures, a drop of more than 90%. As of April 18, 2023, the total number of Radiant Capital users is 368,799.

3.3 Future

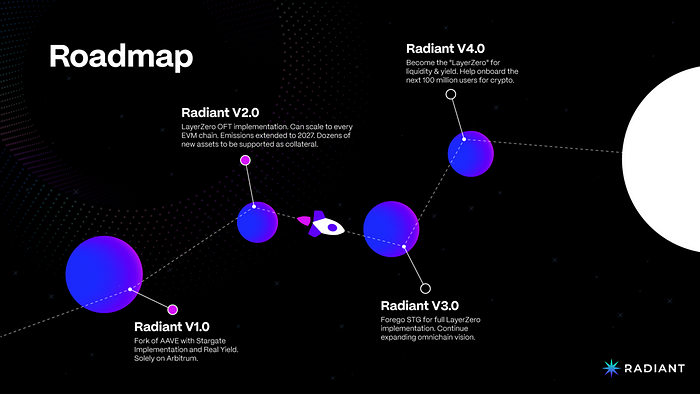

Figure 3-6 Roadmap of Radiant Capital [16]

Figure 3-6 Roadmap of Radiant Capital [16]

Radiant has disclosed a simple roadmap for the project in its official documents. Radiant is currently in the stage of iterating to V2, and the follow-up team will plan to launch V3 and V4 versions. Specifically, in addition to deploying Radiant cross-chain, the team's top priority in the current V2 version is also planning to expand the collateral on the platform. As part of V2 governance, new collateral assets can be voted on to be added to the protocol, and a newly formed protocol risk committee will determine reasonable collateral and lending parameters. Recently, the team has just launched $ARB and $wstETH mortgage assets.

In the subsequent Radiant V3 version, the team plans to completely get rid of the dependence on the third-party cross-chain bridge (Stargate) and fully integrate LayerZero; in the V4 version, it will become the "LayerZero" of liquidity and yield, and become the preferred currency market and cross-chain platform for DeFi. Chain liquidity source.

Summarize:

Radiant has achieved a certain market size so far. However, through the above data analysis, we can also see that in Radiant, although a certain proportion of actual loan demand has been generated, a considerable part of the funds are still based on liquidity mining. Purpose. If the price of RDNT remains unchanged or rises, the amount of deposits and borrowing in Radiant is likely to continue to rise under the incentive of high liquidity mining. But it is clear that Radiant's competitiveness will decline without mining revenue. In addition, from the perspective of user usage, Radiant seems to have stagnated after the V2 version went live.

At present, for Radiant, it is mainly to expand to more chains and support more collateral assets, so as to boost Radiant's growth in the next stage. In the long run, the core of the agreement is whether it can truly promote the practical application of full-chain lending.

4. Economic Model

Radiant Capital's native token is $RDNT, with a total of 1 billion tokens. According to the CoinGecko data port, the current circulation of $RDNT is about 261 million, accounting for about 26.13%.

4.1 Supply

4.1.1 Token Distribution

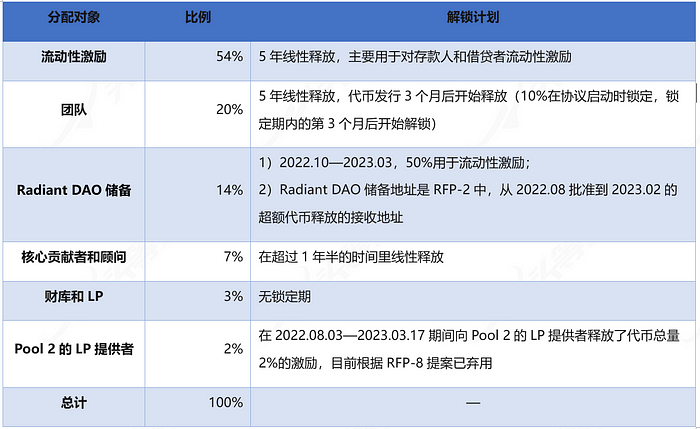

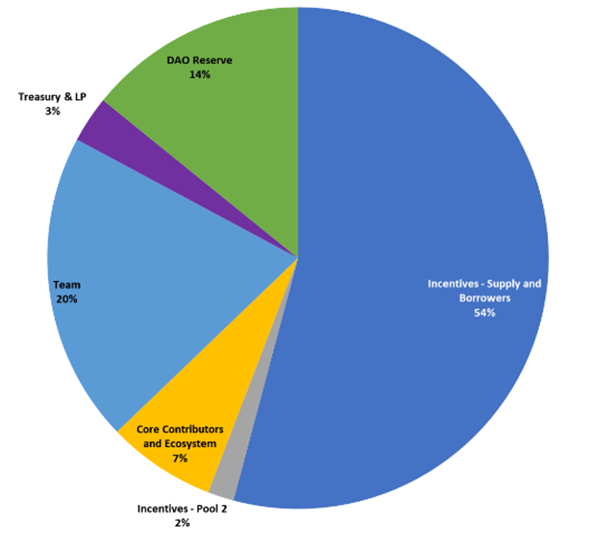

The distribution of the initial 1 billion tokens is as follows:

Table 4–1 $RDNT Token Distribution Details

Table 4–1 $RDNT Token Distribution Details

Figure 4–1 $RDNT Token Distribution Detail [17]

Figure 4–1 $RDNT Token Distribution Detail [17]

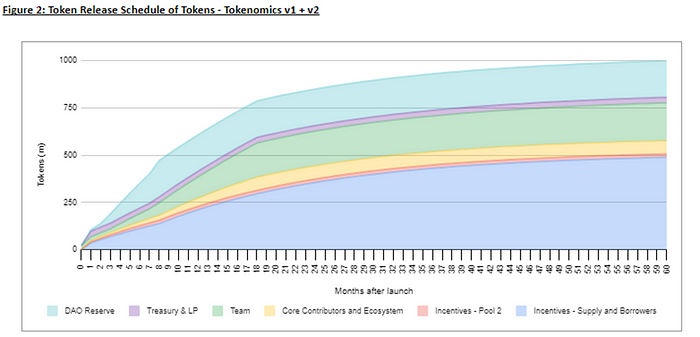

Figure 4–2 $RDNT Token Release Schedule

Figure 4–2 $RDNT Token Release Schedule

4.1.2 Analysis of currency holding addresses

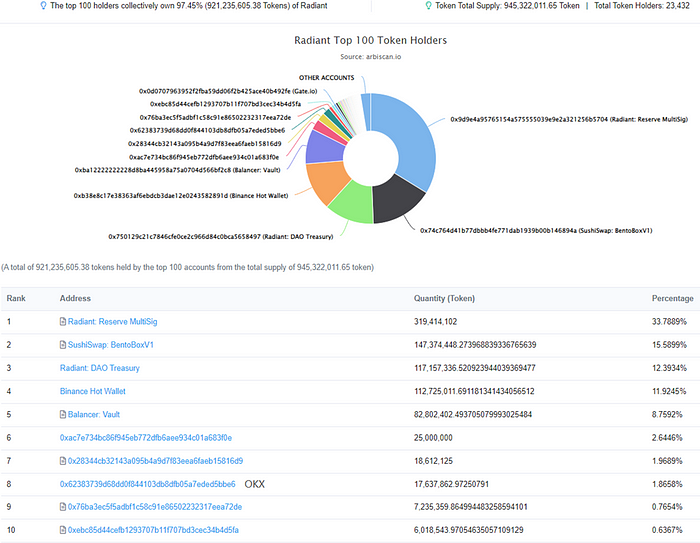

Figure 4-3 Analysis of $RDNT holding address [18]

Figure 4-3 Analysis of $RDNT holding address [18]

According to Arbiscan data, as of April 20, 2023, there are currently 23,432 $RDNT holding addresses, with the top 100 holdings accounting for 97.45% and the top 10 holdings accounting for 90.34%.

Among them, 9 of the top 10 addresses are contract/exchange/LP addresses, accounting for 87.69%. After deducting this part, the top 100 addresses account for a total of 9.76%. It can be seen that the concentration of $RDNT holding addresses is relatively high at present, and the tokens are mainly concentrated in the hands of the team and market makers.

4.2 Requirements

The token role of $RDNT is currently similar to the governance tokens of most DeFi protocols, mainly used for community governance and incentive liquidity. The overall token use case is still relatively single, and we look forward to the subsequent integration with LayerZero. By deploying $RDNT on more chains and Dapps, more complex strategies and high-frequency arbitrage opportunities can be created around $RDNT, creating more Token usage scenarios.

Summarize:

The total amount of Radiant Capital tokens is 1 billion. The V2 version extends the life cycle of token incentives by extending the original 2-year token release cycle to 5 years (July 2027). However, at present, the token function of $RDNT is still relatively single, and it needs to be further developed in the future to expand more usage scenarios in order to better capture the ecological value.

5. Competition

Radiant Capital is a cross-chain DeFi lending agreement, and the team positions itself as an omnichain lending agreement.

5.1 Industry Overview

In recent years, we have taken the lead in seeing application scenarios with practical needs on Ethereum: DeFi, NFT, GameFi, etc., and the ecological construction is thriving. But on the other hand, with the rapid development of the ecology, it has also exposed the problem of insufficient performance of the underlying layer of Ethereum. Network congestion and high Gas fees have hindered the further expansion of the ecology. At the same time, some people "save themselves" and focus on Layer 2, and some people "want to go out and see" and devote themselves to other public chains besides Ethereum.

So in 2021 we saw the rapid development of the public chain track ecology other than Ethereum. Many emerging public chains (such as: BSC, Solana, Near, Avalanche, Fantom, etc.) have made corresponding trade-offs in the impossible triangle, supplemented and expanded in terms of scalability, and because most of these chains are compatible with EVM, It is easier to integrate DeFi and NFT type projects, so as to complete the simple replication of the applications that Ethereum has successfully landed.

At the Layer 2 level, we have also seen that various projects are entering the Arbitrum and Optimism ecology, from the "GLP War" triggered by GMX, to the trading activity of some projects on Layer 2 that has exceeded their level on Layer 1. In terms of activity, the Layer 2 ecology has developed to a scale that cannot be underestimated. According to the DeFiLlama data port, as of April 23, 2023, the total TVL of the Arbitrum ecology is 2.170 billion, and the total TVL of the Optimism ecology is 907 million.

In addition, since the second half of last year, projects related to ZK Rollup expansion have also begun to focus on efforts to catch up with progress, and related programs and projects have also begun to emerge, and have gained more funds and attention. It is foreseeable that as the fierce competition between Layer 2 intensifies, the mobility between ecology will inevitably be further divided.

Of course, no matter how the market evolves, it is impossible for one chain to cover everything, and Ethereum cannot take over the entire market. Judging from the current market structure, the future development trend is likely to be based on Ethereum and Layer 2 based on it, and other public chains will be dominated by stars .

In fact, whether it is the traditional financial field or the DeFi protocol on the chain, the original intention is to meet the investment and financial needs of users, and this demand has always existed. For cross-chain DeFi, the core point is — is it necessary to interconnect with other public chains in the financial field to achieve more composability. The successful start of many public chains and second-tier projects has confirmed this point for us. Although part of the reason for the phenomenon of multi-chain coexistence is the continuous operation of external capital, the emerging public chain and the second layer have indeed hit the pain points of Ethereum in terms of scalability and low gas fees.

Nowadays, in the blockchain world, many ecology are blooming, which also makes the asset management of users on the chain more diversified. With the increase in the number of public chains and Layer 2 projects and the gradual improvement of their ecology, the demand for cross-chain user assets on the chain will increase with a high probability, and this is precisely where the demand for cross-chain DeFi lies.

Previously, most of the lending protocols on the market deployed different versions on different chains or Layer 2. For example, some blue-chip lending protocols on Ethereum, in order to further expand the market, would choose Arbitrum, Optimism, BSC, Different versions are launched on chains such as Polygon. Although they belong to the same protocol, on different chains, assets cannot be transferred between each other, and the liquidity on each chain is fragmented. To achieve interoperability, assets need to be cross-chained first. The current emerging concept of full-chain lending is essentially to integrate the liquidity on different chains, improve the utilization rate of funds, and reduce the user's operating threshold.

5.2 Introduction of competing products

At present, many projects have entered the cross-chain lending track, such as: the top lending project Compound Finance provides cross-chain lending through Gateway (Compound has previously launched the Gateway corresponding testnet, but due to unknown reasons, the corresponding code of Gateway The sub-library will stop updating after 2021.07 [19] ); Aave will also support cross-chain lending in version V3, but this function is not yet online. In addition, BSC, Cosmos, Polkadot and other public chains have also launched their own corresponding cross-chain DeFi protocols, but at this stage, they are basically the first to realize the bridge with the Ethereum blockchain, and no projects have yet realized cross-chain The interoperability between DeFi protocols is still at an early stage.

The Radiant Capital discussed in this article is a cross-chain/full-chain lending protocol based on LayerZero, and its future competition will first start within the LayerZero ecosystem. Therefore, the competing products in this chapter are mainly focused on the cross-chain lending project that is also the LayerZero ecosystem, and Aave V3.

5.2.1 Aave V3

In the introduction of Aave V3 in 2021.11, Aave mentioned a new function of "Portal" , which will allow assets to seamlessly circulate between Aave V3 markets through different networks. Since the official launch of Aave V3 on 2022.03.16, the Portal function has actually reached a deployable state, but users are still unable to use it. The main reason is that the integration of the whitelist cross-chain bridge has not been completed yet.

The good news is that with Aave deploying Aave V3 on Ethereum in January this year, in the following March and April 2023, we saw that Aave V3 proposals were passed. V3 Portals will add Hashflow/Wormhole and Stargate as "whitelist" Bridge" vote [20] [21] . We may see the Portal feature go live soon.

First-class warehouse note: Aave V3 includes multiple updates, and the Portal function is just one of the highlights.

5.2.2 TapiocaDAO

TapiocaDAO is a cross-chain DeFi lending protocol. The team positions itself as an omnichain lending protocol, aiming to realize leveraged lending and composability between different chains, so that users can use it in the supported DeFi protocols. Gain leverage and simplify the operation of assets across chains. The project just went live on the testnet in 2023Q1.

In terms of lending, TapiocaDAO's core smart contracts include Singularity (based on Kashi launched by Sushiswap) - an independent full-chain lending engine, and Yieldbox (Bentobox V2) - a token vault that does not require permission, allowing idle Funding for yield farming. Both contracts were created by BoringCrypto [22] .

At the cross-chain level, TapiocaDAO uses LayerZero as its cross-chain infrastructure, and based on the LayerZero OFT20 (Omnichain Fungible Token) standard, designed a decentralized over-collateralized stablecoin — “usd0”.

5.2.3 Cedro Finance

Cedro Finance is also a LayerZero-based cross-chain lending platform, which is currently on the testnet. The platform introduces the innovative unified liquidity token CULT to ensure the liquidity supply of the agreement. In addition, the platform also greatly optimizes gas costs by moving some calculation operations (such as interest rate calculation, tracking different assets, tracking different positions, and liquidation, etc.) to the Root contract. Currently, users can give feedback on the testnet and earn reward points by completing tasks.

5.3 Competition Analysis

Since the products of Aave V3, TapiocaDAO, and Cedro Finance have not yet been officially launched, there is no data to support the horizontal comparison with Radiant for these three projects. This section mainly introduces the mechanism of the three projects and their respective advantages and disadvantages.

5.3.1 Aave V3

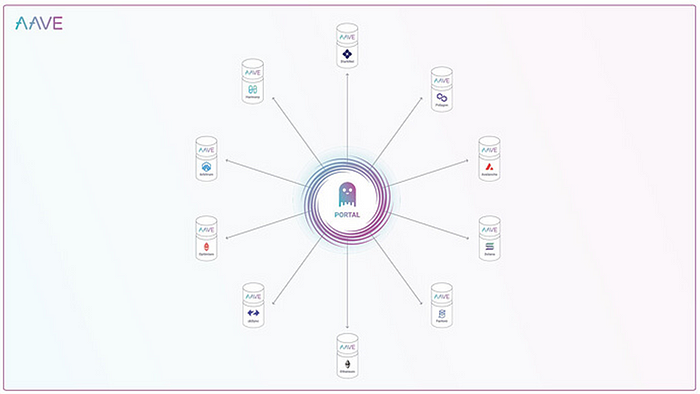

Figure 5-1 Aave V3 Portal concept map [23]

Figure 5-1 Aave V3 Portal concept map [23]

According to the team, Portal allows users to seamlessly move their assets from V3 deployments across different networks. Its core functionality is simple: user-supplied liquidity can be transferred from one network to another by simply burning aTokens on the source chain (e.g., Ethereum) while simultaneously minting them on the target network (e.g., Polygon). Network interconnects built around this functionality are called ports.

The realization of the Portal function relies on the cross-chain bridge protocol of an external third party. Aave governance votes to select a "white list" cross-chain bridge protocol, that is, the "burn — mint" operation on different chains is not done by the Aave protocol. carried out, introducing third-party security assumptions.

Previously, the community forum of Aave V3 also mentioned that "Portal will be able to bridge Connext, Hop Protocol, Anyswap, xPollinate and other solutions that utilize Aave protocol liquidity to facilitate cross-chain interaction. Aave Governance will be able to grant Any cross-chain protocol access to ports.”

Currently in March and April 2023, we have seen Aave V3 proposals pass votes for V3 Portals to add Hashflow/Wormhole and Stargate as "whitelist bridges" respectively. These are also the two cross-chain bridge agreements voted by V3 Portal for the first time.

In addition, according to the current information, Portal will integrate multiple "whitelist cross-chain bridges" in the future, and allow each cross-chain bridge protocol to mint corresponding aTokens on different networks according to their respective credit limits. And Aave V3 will also allow full refinement of the fee model, each port can require a unique fee model, or even a different fee model for each network and asset. Portal proposes to adopt a business model for governance. This helps to promote "involution" between different cross-chain bridges on Portal, thus bringing lower fees and slippage to users on Aave. As for the cross-chain bridge project, by applying for the Portal whitelist to integrate with it, the potential influence can also be expanded, which is a win-win situation for the participants.

First-class position point of view: A simple understanding of the Portal function of Aave V3 will support users to deposit ETH on Arbitrum for pledge, and then borrow on Polygon. This is exactly the same as Radiant's full-chain lending concept.

As the largest lending agreement in the cryptocurrency market, Aave will directly become the lending agreement with the best liquidity on multiple chains if it launches multi-chain shared liquidity. The launch of the Portal function is expected to improve the liquidity and capital utilization rate of Aave's entire ecological territory, and further enhance the lending business of the entire agreement to a higher level. At that time, the Matthew effect may be triggered and may quickly spread to all blockchains, and it will also become Radiant's strongest competitor.

On the other hand, in fact, as early as 2022.03.16, since Aave V3 was officially launched, the functions of Portal have already reached a deployable state. It took more than a year for us to see the corresponding community vote, and there is still no exact time for the official landing. The main reason is that the Aave team is more cautious in governance proposals and technical implementation due to security considerations. After all, as mentioned above, Portal’s asset cross-chain is not carried out by the Aave protocol, but a third-party cross-chain bridge protocol is introduced. Wormhole, the "white list bridge" that was voted recently, has also been hacked before. The team needs to carefully weigh how to weigh the uncertain external security assumptions introduced by the protocol.

In contrast, for Radiant based on LayerZero, if the follow-up (V3, V4 version) can make a good security assumption between the oracle and the relay (see LayerZero operation mechanism for details), and realize detrust at the contract level, then in the assets Cross-chain security assumptions may be more dominant.

5.3.2 TapiocaDAO

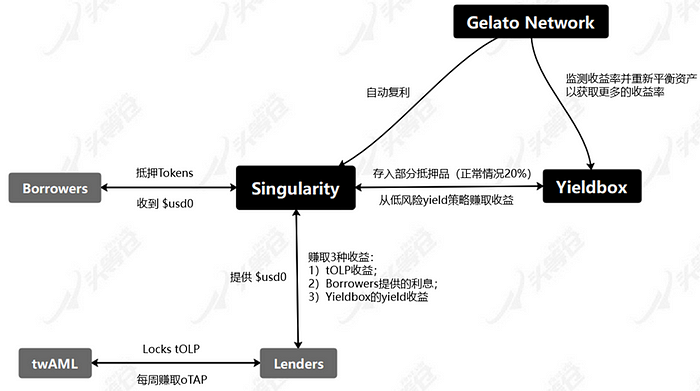

The core products of Tapioca are Singularity and Yield Box :

• Singularity is an independent full-chain lending engine, previously adopted by Kashi based on Sushiswap. Currently Singularity is a modified version of Kashi, which is licensed to TapiocaDAO.

• Yieldbox (Bentobox V2) is a permissionless token vault that allows idle funds in the Singularity platform to be yield-farmed.

At the cross-chain level, TapiocaDAO uses LayerZero as its cross-chain infrastructure, and based on the LayerZero OFT20 (Omnichain Fungible Token) standard, designed a decentralized over-collateralized stablecoin — “usd0” .

In addition, in terms of economic model, Tapioca introduced twAML , which aims to change the disadvantages of existing liquidity mining, improve the distribution efficiency of LP and realize the sustainable development of the protocol.

Simply understand, TapiocaDAO realizes the function of cross-chain lending through Singularity and LayerZero, and applies a layer of yield protocol (Yieldbox) on this basis to help users farm more income. In addition, TapiocaDAO also introduced the innovation of twAML option mining in terms of economic model.

The operating logic of TapiocaDAO products is shown in the figure below:

Figure 5–2 Tapioca product operation logic

Figure 5–2 Tapioca product operation logic

For the borrowers (Borrowers), it is simple to over-collateralize the assets supported by the Tapioca platform in the Singularity fund pool, borrow currency ($usd0) and pay interest on the debt.

Depositors (Lenders) can provide liquidity for the Singularity fund pool and earn deposit interest, or earn higher returns by minting $usd0 and staking (normally to encourage users to mint a new stable currency, the platform will will be given higher incentives at the beginning). When depositors provide LP, they will receive “tOLP” receipt tokens. When the option expires, users can choose to buy $TAP at a discounted price and sell it for profit.

Here, in Tapioca’s setting, when user assets are lent to the Singularity market, Singularity will put part of its liquidity (20%) into the Yieldbox for income farming, so depositors can also get a part of the yield income .

In Yieldbox, Tapioca helps users realize automatic compound interest through the external Gelato Network [24] , and monitors the income of Yieldbox's different strategy pools, and regularly rebalances the asset distribution of each fund pool to achieve higher yields.

First-class warehouse view:

TapiocaDAO and Radiant are two similar projects, the core of which is to achieve cross-chain functions through LayerZero. At the lending level, Radiant refers to Aave's mature lending model design, while Tapioca is based on BoringCrypto's contract improvement, and has a successful operation case of SushiSwap. The difference is that on the basis of cross-chain lending, Tapioca has superimposed a layer of yield function.

By reading the official documents of Tapioca and Radiant, it can be seen that Tapioca will disclose more details in various aspects in comparison, and there is also an innovative economic model design (for more details, please refer to the "TapiocaDAO investment" previously released by the first-class warehouse. Research Report"). But on the other hand, it should also be noted that the twAML introduced by Tapioca is relatively complicated, and the threshold for early user education is relatively high, which will also test the team's operational capabilities.

Therefore, in the opinion of the editor, if Tapioca and Radiant go online at the same time, they may be two comparable projects. But the current situation is that Radiant already has a first-mover advantage in the field of cross-chain lending, and has accumulated a considerable portion of liquidity and user groups. However, Tapioca has just launched the testnet version in 2023Q1, and it will be difficult to catch up with it in the future.

5.3.3 Cedro Finance

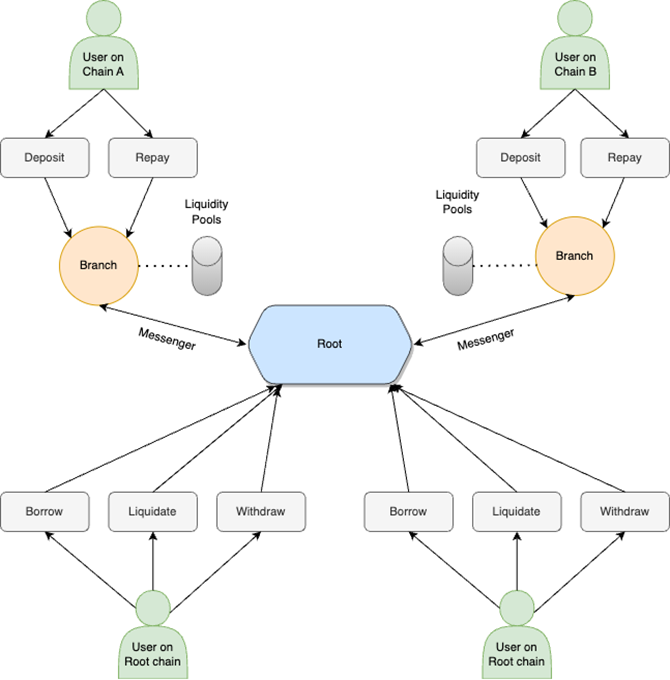

Cedro Finance protocol architecture:

Figure 5–3 Cedro Finance protocol architecture [25]

Figure 5–3 Cedro Finance protocol architecture [25]

As shown in Figure 5–3 above, in Cedro Finance, a branch (Branch) is deployed on multiple chains, all of which interact with the root (Root), and Root is deployed on a single chain that is responsible for storing the protocol The global state of the network and pass information between chains. Branch and Root interact using Messenger. Through this modular design, when Cedro wants to add a new chain to the protocol, it only needs to deploy Branch on the new chain and establish a connection with Root.

The protocol architecture of Cedro Finance is mainly divided into 3 parts:

1) Branch

Branch is the main interaction point for users to make deposits and repayments. For example, if a user wants to deposit USDC in Ethereum, the user will interact with the depositRequest() function of Branch in Ethereum. The deposited amount is stored in the USDC liquidity pool of Ethereum, the information is sent to Root through Messenger, and the user receives ceToken on the Root chain.

Branch handles the asset pools it deploys to each chain. This means that when a user deposits AVAX on Avalanche, it is sent to the AVAX pool managed by Branch itself. Every asset listed in Cedro has a pool that stores funds in Branch but managed by Root. In order to add a new chain to the protocol, Cedro will first deploy a Branch on the chain, and then establish a Messenger connection between Root and Branch.

2) Messenger

Messenger is a stack composed of multiple general-purpose cross-chain messaging protocols (such as LayerZero). Messenger analyzes different factors, such as estimated transaction cost, speed, security, etc., to choose a messaging protocol from the stack for a given transaction. The benefit of having a cross-chain messaging protocol aggregator is that it gives users another level of freedom. Users can choose the protocol they want, or let Cedro choose based on their priorities in terms of cost, speed, security, etc. Once a protocol is selected, it is used to send the required cross-chain messages to Root and Branch.

3) Root

The Root is deployed in a single chain and is the connection point for all Branches. Each Branch is connected to Root in a two-way manner through Messenger.

Root stores global variables for all protocols, including total deposits, total borrowings, total protocol liquidity, etc. across multiple chains. Therefore, whenever a user deposits assets on the A chain, the information is passed to the Root chain to update the user's liquidity and the liquidity of the asset.

In addition, Cedro Finance also introduced the innovative unified liquidity token CULT (Cedro Unified Liquidity Token) to ensure the liquidity supply of the agreement. Simply understood, CULT allows users to deposit multi-chain assets from different chains and import them into a unified liquidity pool. For example, when a depositor deposits 100 USDC in Ethereum and 200 USDC in Solana, he will receive 300 c