Track pattern of public chain order book

When it comes to DEX, most people will immediately think of AMM. AMM is very useful and is the key original mechanism of DeFi. Although compared with AMM, onchain LOB (on-chain order book) has been criticized for lack of LP ecology and regulatory arbitrage behavior on the chain of centralized exchanges, etc., but onchain LOB also plays a role that cannot be ignored in the entire DEX track, especially For professional traders and institutions, it is an important segment of the DEX track.

On the whole, order book exchanges can be divided into four types to understand. The first type has high performance such as excellent transaction speed and throughput, but highly centralized CEX is the trading choice of most people in the market. Such as Binance/OKX. The second is the order book on the Ethereum L1 chain , such as Gridex, which achieves a high degree of decentralization. However, since transactions are executed directly on the chain, performance is limited and users need to pay higher gas fees. The third is a Rollup-based high-performance off-chain order book , off-chain matching to reduce Gas costs, and batch processing and settlement on the chain to ensure security, such as DYDX v3, Vertex, Zigzag, etc. ETH L2 Base recently called for onchain order book dex to become A part of its ecological fund is deployed in its ecology, and the development of each L2 will provide a good development soil for onchain orderbook. The fourth type is the high-performance DeFi original chain/customized chain that meets the high-performance requirements of orders , such as Injective and Sei, DYDX V4, etc., which have not yet launched the mainnet .

In the fourth type of DeFi order book protochain, in addition to typical projects including Injective, DYDX V4, SEI, Osmosis, Kujira and Crescent, etc. are currently developing on a large scale, benefiting from the Ignite consensus Framework (formerly known as Tendermint, which is a proprietary Byzantine fault-tolerant BFT PoS infrastructure), IBC and the special structure of the customizable SDK, almost all order book protochains are built on the Cosmos ecology, but Injective is built on Cosmos -The forerunner of chain orderbook.

This article mainly introduces Injective in the original chain of the DeFi order book, focusing on the core advantages and moats of the public chain order book DEX and the situation of competitors, whether Injective has an advantage in fundamentals .

Injective is an interoperable L1 blockchain optimized for DeFi. In fact, before announcing the integration of Cosmos, Injective was considered an L2/sidechain of Ethereum, but after having a consensus layer and sovereignty on Cosmos , Injective has become a financial infrastructure with plug-and-play functions, covering high-performance on-chain decentralized exchange infrastructure, decentralized bridges, oracles and composable Smart contract layer. Other protocols in the ecosystem can use Injective's onchain-orderbook to start liquidity and matching services, adding a layer of composition.

The construction of Cosmos Tendermint/Ignite, SDK and IBC technical components helps Injective utilize the high finality and low transaction costs of the network to support its order book function, and further improve capital efficiency and liquidity segmentation, while maintaining interoperability with Ethereum, using FBA (Frequent Bulk Auction) order matching engine, which aggregates each order together at the end of the block and executes all market orders at the same price to help prevent front-running OME (Order Matching Engine) approach, making Injective as Compared with traditional financial order books and other AMM, the decentralized financial infrastructure has decentralization, high transaction speed, high finality and a moat against MEV.

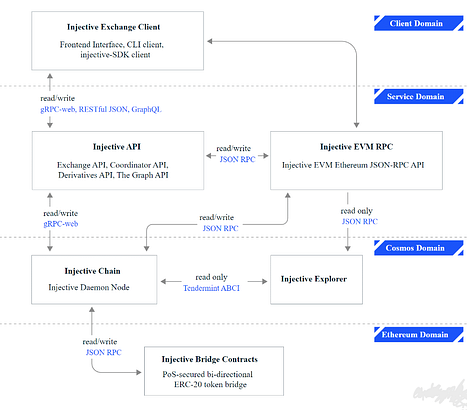

Injective construction

Injective Chain is the core component of Injective. The Injective Chain built using the Cosmos Tendermint/Ignite standard inherits decentralization, security and high performance.

The figure above shows the composition of the entire Injective Stack

Service Domain

The service layer acts as a bridge between exchange DApps (such as Helix) and the underlying blockchain layer. It consists of multiple APIs including Exchange API, Coordinator API, Derivatives API and The Graph API. These APIs play a key role in ensuring seamless communication between different components in the Injective ecosystem, helping users conduct transactions and access various DeFi services. APIs within the service layer enable Helix to interact with the Tendermint/Ignite-based Cosmos chain and the Ethereum blockchain. This modular approach to API design provides greater flexibility and scalability, ensuring that Injective can continue to grow and evolve to meet the ever-changing needs of the DeFi space.

Cosmos layer

The Cosmos layer is the foundation of the Injective chain, built on top of Tendermint/Ignite, responsible for executing various types of transactions and derivatives orders. This layer contains the Injective API and the Injective EVM Remote Procedure Call (RPC), enabling connections with the Injective chain and the Injective Explorer. EVM (Ethereum Virtual Machine) is a decentralized, Turing-complete virtual machine for executing smart contracts on the Ethereum blockchain. Injective Explorer is a tool for tracking all transactions made on the Injective chain, providing users with valuable insights into platform activity and performance. The instant finality properties of Tendermint make it ideal for supporting Injective chains as it enables fast transaction execution and settlement. The Cosmos layer also offers a range of security and performance benefits, including Tendermint/Ignite consensus mechanisms, horizontal scalability, and a powerful application framework for building custom blockchain applications.

The importance of the consensus mechanism

Tendermint/Ignite was chosen as the consensus mechanism of the Injective chain because it can provide near-instant certainty, high fault tolerance, and support for horizontal expansion. Near-instant finality is especially important in the context of trading platforms, ensuring that transactions can be executed quickly and efficiently without the risk of rollbacks or double spends. This enables Injective to maintain a high level of performance as the volume of trading activity on the platform increases. Tendermint's PoS consensus algorithm also provides a high degree of fault tolerance, ensuring that the Injective chain will still function correctly in the presence of malicious or faulty nodes.

The specific implementation method is that the Tendermint/Ignite protocol uses multiple rounds to propagate blocks to network validators through proposal messages. For a block to propagate, it must be voted on by multiple block proposers and signed by the private keys of the corresponding validators. Verifiers communicate on Tendermint/Ignite through the peer-to-peer (P2P) gossip protocol. In order for a block to be considered valid, more than two-thirds of the verifiers must accept the block, which is also called Byzantine Fault Tolerance (BFT) Proof of Stake (PoS) consensus mechanism.

Ethereum Domain

The bridge layer is critical for cross-chain interoperability and communication between Injective and the Ethereum network. It consists of the Injective Bridge smart contract, which itself relies on Wormhole, Peggy, IBC, and Axelar. The bridge layer interacts with the Injective chain, the Ethereum network, and other supported blockchains. Injective Bridge enables two-way transfer of ERC-20 tokens and assets between Injective and Ethereum blockchain through Peggy. This cross-chain interoperability enabled by Wormhole, Axelar and IBC is critical to a decentralized blockchain infrastructure as it allows different networks to seamlessly share data and assets. Through Injective Bridge, utilizing the capabilities of the Ethereum network and its DApps ecosystem, Injective and the entire Cosmos ecosystem can inherit part of the huge liquidity on Ethereum.

Background of the project

Injective is incubated by Binance. It is one of the eight projects incubated in the first phase of Binance Labs and has received support from many investment institutions. This time Binance was greatly affected by the SEC crackdown, but the impact on the decentralized exchange Injective was limited.

Eric Chen, the co-founder and CEO of Injective Protocol, graduated from the New York University School of Computer Science. The core team has a good professional background and has worked experience in internationally renowned companies such as Open Zeppelin, Amazon, and hedge funds. The core members of the team graduated from well-known institutions such as Stanford University.

On July 29, 2020, Injective raised $2.6 million in a seed round led by Pantera Capital, with participation from QCP Soteria and Axia8 Ventures.

On April 20, 2021, Injective raised $10 million in a “party” funding round, with participation from Pantera Capital, Mark Cuban, and Hashed, among others.

On August 10, 2022, Injective raised $40 million in a funding round that included Jump Crypto and BH Digital.

In January this year, Injective announced the establishment of a USD 150 million ecological fund to promote ecological development. There are currently more than 20 projects in the Injective ecosystem, including Astroport, Celer Network, and Helix. In April, Injective announced a partnership with Tencent Cloud to support developers on Injective.

Tokenomics

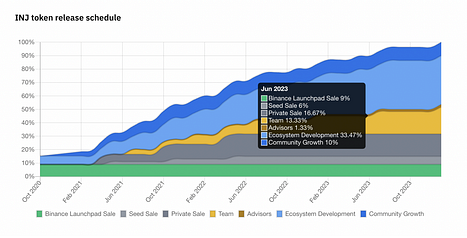

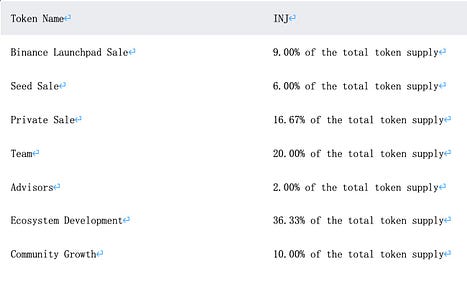

The total amount of INJ is 100mln, and block rewards are compensated by minting new tokens, so there is inflationary pressure. The target inflation rate of INJ tokens is initially 7%, and gradually decreases to 2% over time. However, 60% of the transaction fee is repurchased and destroyed in INJ, making it currently in a state of deflation. More than 90% of the tokens have been released, and about 5% have been released in the near future (June-August), most of which come from Team, Advisors, Ecosystem Develpoment and Community Growth, and the part belonging to Team and advisors may become potential selling pressure, while others It will be converted into APY in Injective, and there will be a certain selling pressure, but higher incentives will increase the ecological data of Injective.

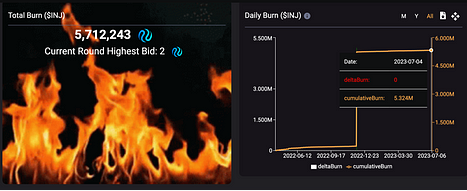

INJ is deflationary, and 60% of dAPP’s fees will go to the chain to repurchase INJ and burn it (60% of the trading fee is auctioned to Bidder, Bidder bids with INJ, and the INJ obtained from the auction will be destroyed), and the weekly supply burn will Creates a deflationary effect and offsets to some extent the increase in supply caused by token minting. To be more precise, the annual inflation rate of 39.78 million pledged INJ is 5%, which is equivalent to minting 2M INJ in one year, and the cumulative destruction has reached 5.32M INJ, accounting for 5.32% of the total supply.

Photo: INJ Burn

Figure: INJ Stake situation

value capture

1) Protocol fee value capture

After 40% of transaction fees are allocated to exchange DApps, Injective uses the remaining 60% for buyback. The protocol conducts a weekly auction where participants bid for that week's fees via INJ . Auction winners receive a basket of tokens and profits from the arbitrage opportunity, while the protocol uses the proceeds to buy and burn INJ to maintain the deflationary nature of the INJ token.

2) Tendermint-based proof-of-stake (PoS) security

Use INJ tokens to secure the Injective blockchain using a proof-of-stake mechanism. Both verification nodes and delegators can participate in stake pledge.

3) Developer Incentives

40% of the fees generated by users of dApps built on Injective are directly used to incentivize new developers to build applications on Injective, which will bring a growing developer community.

4) Protocol Governance

The INJ token is responsible for managing every component of Injective, including chain upgrades.

Token allocation

Token sales data

Ecological project

At present, there are 24 Dapps that have been launched on the Injective mainnet. Most of the Dapps are related to Defi, and there are also communication infrastructure, information protocols, NFT and other related applications built on Injective.

InjectiveMain Dapp

Helix

Helix is the Injective order book transaction front end, originally known as Injective Pro. Its goal is to provide a cross-chain spot and perpetual contract market, enabling users to trade various cryptocurrencies. Helix supports zero gas fees, which helps reduce transaction costs for users.

Mito

After a long wait, last month Injective Labs officially announced Mito, formerly known as “Project X,” and launched closed testnet access to the platform. Mito is an agreement composed of automated trading vaults driven by smart contracts. Each vault executes advanced trading algorithms and is usually only held by institutions and hedge funds. It is currently in the early access stage. Mito consists of two key components: an automated strategy vault for easy yield generation and a sophisticated token launch platform. Through this innovative platform, users have access to various trading strategies that generate income while exploring new coins in the cryptocurrency space.

Astroport

Astroport is an AMM protocol that allows any user to use multiple types of pools for the exchange or liquidity provision (LP) of encrypted assets, including Curve-style stablecoin exchange pools and Uniswap V2-style constant product pools. Astroport is able to utilize Injective’s interoperability network to exchange assets bridged from Cosmos or Ethereum and chains such as Solana, Aptos and Avalanche through Injective’s Wormhole integration.

Since Astroport is built on Injective, users will be able to leverage Injective’s interoperable network to exchange assets from chains bridged from Cosmos or Ethereum, as well as Solana via Injective’s recent Wormhole integration. Users can bridge assets to Injective through Injective Bridge, then create a liquidity pool on Astroport, start earning income as a liquidity provider and start trading new markets.

Astroport brings important advantages to the Injective ecosystem. Originally built on Terra, Astroport contributors spent a lot of time analyzing multiple major L1 networks, and finally decided to use Injective as the custody chain for its V2 version. Astroport has now officially migrated its mainnet to Injective, becoming one of the largest AMM in the Injective ecosystem.

As of the end of June, Astroport had a total TVL of 32.94M, and the TVLs on the Neutron, Terra, and Injective chains were 21.99M, 6.42M, and 4.52M, respectively.

competitive landscape

SEI is a protocol comparable to Injective in terms of consensus mechanism basis, OME type (FBA), FDV, etc. SEI has a detailed difference from Injective in OME mechanism, which will be introduced in detail below.

DYDX is about to migrate from Ethereum to Cosmos and launch the DYDX chain (DYDX V4). Currently, V4 is in the testnet. The launch of the DYDX v4 mainnet may squeeze Injective’s market share to a certain extent. The specific impact depends on the transaction incentives and Institutional preferences, from the token release stage, 90% of the Injective tokens have been released, and DYDX, including the unlisted SEI, may have an advantage in the token incentive space.

In terms of valuation, SEI completed a financing of 30 million U.S. dollars in the last round of 800 million U.S. dollars. Jump Capital and Distributed Global participated in the investment. Injective is currently less than 800 million, and DYDX is 1.9 billion. Injective’s valuation still has room for growth, but the transaction The volume of key business data Injective is obviously inferior to other competitors (Helix 24hrs trading volume 22mln, DYDX 600mln), and the trading volume gap with DYDX is very large, which is related to the fact that Injective trading pairs are mainly assets in the Cosmos ecosystem.

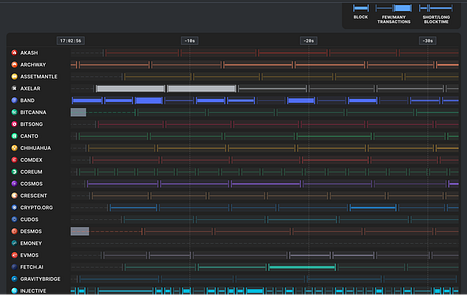

Compared to other blockchains on the Cosmos network, Injective is currently the fastest with an average block time of about 1 second. It can be seen from the figure that Injective’s block generation speed is significantly higher than other chains.

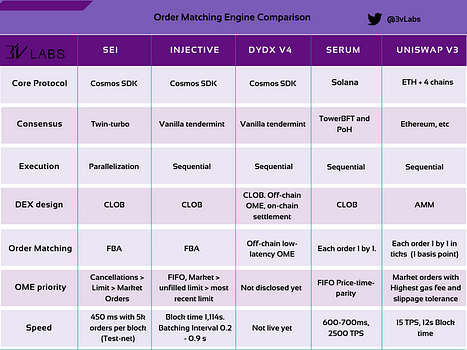

Order Matching Engine (OME) Comparison

The picture above is a comparison of order matching mechanisms of @3V Labs about SEI, Injective, DYDX V4, Serum, and UNI V3

The order book is resistant to MEV, which is required to handle large-scale institutional order flow. At present, the defense mechanism of most public chain order book DEXs is to minimize bad MEV through frequent batch auctions (FBA). Except for FBA, Off -Chain Low Latency OME is the order matching mode of DYDX V4.

For Injective, the FBA matching mechanism is an important upgrade, which adopts the frequent batch auction model. The results achieved are maintaining fast trading times, accessing market prices through higher liquidity, and narrowing spreads.

So what is FBA? To understand FBA, you need to understand the concept of continuous two-way auction CDA. FBA actually solves the problem of CDA capital inefficiency.

Problems with CDA Continuous Two-Way Auction

Centralized exchanges for crypto derivatives and traditional financial markets use a Continuous Double Auction (CDA) model. In this model, orders are processed as soon as they reach the exchange. This can be achieved by immediately executing the order on the opposite order of the order book or by holding it on the order book until a matching order is found.

The way orders are processed by a continuous two-way auction incentivizes speed, while a highly volatile market creates huge arbitrage opportunities. The role of Market Makers (MMs) is to follow the market price of an asset and provide depth by placing orders on both sides of the order book. As prices move, MMs must cancel and create orders accordingly.

However, in the time period between price updates from external signals, high frequency traders (HFTs) have the opportunity to execute stale MM orders before the MM cancels the order. Therefore, HFTs can obtain arbitrage income. The profits in this obsolete order-snapping game are so large and sustained that HFTs invest in advanced technologies like microwave towers and FPGAs to compete at nanosecond (billionth of a second) speed, leaving MMs at an insurmountable disadvantage.

Because of these obvious problems, MMs are often forced to increase their investment in competing technological solutions, which is often paid indirectly by traders through higher transaction fees. Additionally, MMs often become more risk-averse because they offer a lot of depth around market prices. Not only does this hurt retail traders who want to execute their orders at a fair price, it also creates high volatility within the spread, destabilizing the market on small timescales. As a result, retail traders are often forced to enter into positions at unfavorable prices.

The matching engine for continuous two-way auctions requires high-throughput processing during unpredictable times, and minimal demand most other times. Even when built by centralized institutions, exchanges based on continuous double-sided auctions can rarely meet the market demand for 100% uptime. Within the confines of blockchain networks, the situation is further exacerbated. As a result, decentralized exchanges have far less flexibility to solve the same challenges than today's most modular centralized exchanges.

Minor changes in the continuous double auction (CDA) design of decentralized exchanges have proven unsatisfactory and end up causing only financial losses to retail traders. For example, instead of prioritizing orders by submission time, orders that pay higher gas fees are executed while other orders with reasonable gas fees are ignored.

Anyone who has traded more aggressively on a particular AMM exchange protocol has experienced the pain of being bots paid for by high gas fees profiting on the margins of a trader's slippage tolerance. AMM are designed to eliminate the need for institutional MMs, and the cost of capital inefficiencies associated with CDAs is passed directly on to retail traders.

Look at the advantages of FBA and Injective FBA

Injective's Frequent Batch Auction (FBA) has been commonly proposed as a definitive solution to the capital inefficiencies associated with CDAs. One of the benefits of FBA is that it improves the fairness and liquidity of the market by eliminating front-running transactions.

Injective FBA is defined by three characteristics:

1) Discrete time; orders are accepted during a discrete period of time called the auction interval. At the end of each auction interval, cross orders are filled in the following priority order:

Market orders are filled first, then outstanding limit orders from previous auction intervals are filled, and lastly limit orders from the latest auction interval are filled. If the quantities of buyers and sellers are different, the order of the party with the smaller quantity is fully filled, while the order of the party with the larger quantity is filled proportionally (evenly and partially filled).

2) Uniform clearing price; limit orders are filled at the unified clearing price of the highest cross order quantity. If the quantity of buyers and sellers is the same, the mid-price is used as the liquidation price.

3) Closed bidding; orders are not published to the order book until the auction interval ends and the batch auction is executed. This eliminates the possibility of front-running trades and negative spreads.

Market Maker Incentives in Frequent Lot Auctions Relatively long auction intervals provide sufficient time for market makers to cancel stale orders before HFTs are able to execute. This removes the risk of market makers having to deal with front-running issues, thus not requiring them to invest capital in advanced technology.

Market makers are encouraged to offer deeper liquidity and tighter spreads around market prices, which is not only a better situation for retail traders trying to fill their orders at close to fair prices, but also reduces the risk associated with potential price crashes. associated volatility.

Frequent batch auctions aggregate orders onto a set of auction intervals for state changes or order book inclusions. The blockchain queues transactions and writes successive blocks in batches. For FBA, the optimal batch interval is still controversial, but it has been reported in academic reports to be between 0.2 and 0.9 seconds, which is consistent with Injective's auction interval, and batch auctions are executed at the end of each block.

As a protocol for using FBA as order matching on Cosmos, SEI has some differences from Injective FBA in terms of details, such as 1) SEI implements block parallel processing and no longer processes transactions sequentially. Multiple transactions involving different markets can be processed simultaneously, improving performance. According to recent load tests, it was possible to see a block time reduction of 75–90% compared to sequential processing, with a latency of 40–120 ms for parallel processing versus 200–1370 ms for sequential processing;

2) SEI's price oracle is responsible for streaming off-chain price data to the blockchain and built into the chain. This means that all validators need to propose their price (exchange rate) when submitting a block. Blocks are only created when all validators agree on a common price. Validators are penalized if they miss certain voting windows or offer prices that deviate too far from the median;

3) Trading order bundling, market makers can cancel and create orders involving multiple markets in one transaction (that is, combine the orders of all BTC perpetual contracts into a smart contract call for a specific market).

Injective is built on top of Tendermint/Ignite's BFT-based PoS consensus with instant finality, which fits well with FBA execution at the end of each interval . Since FBA has no concept of time priority between auctions, it is a market design that perfectly matches the blockchain operating on the same basis. This is due to the fact that Tendermint/Ignite is a consensus engine based on the BFT (Byzantine Fault Tolerance) consensus algorithm. It uses a pre-selected set of validator nodes to reach consensus and vote and confirm the order of transactions through consensus rounds. The design goal of Tendermint/Ignite is high security and determinism, suitable for application scenarios that require strong consistency and finality , and this design fits perfectly with Injective's infrastructure.

By replacing Continuous Double Auctions (CDAs) with Frequent Batch Auctions (FBAs), Injective employs a market design that is technically robust and competitive with centralized exchanges. Injective eliminates front-running that hurts traders, helping market makers provide deeper liquidity and tighter spreads. The implementation of frequent batch auctions positions Injective to compete with the trading volume of institutional-grade centralized exchanges.

Summarize

Injective has the best transaction speed, instant finality, almost zero gas cost and anti-MEV advantages. These advantages come from 1) The block confirmation speed based on the Tendermint BFT consensus mechanism is fast (but the degree of centralization is relatively low. Higher) and has timely finality; 2) Since the exchange broadcasts the signed message to the Injective Chain node instead of the trader itself, all fees related to chain interaction are paid by the exchange's DApp, which means that the trader does not need to pay any Gas fee; 3) Use frequent batch auction (FBA) as the order clearing mechanism. Orders submitted to the memory pool are executed at the end of each block (about 1 second of block time), and will not be published on the order book until the auction process is completed, which effectively prevents pre-transactions by MEV bots.

Compared with AMM, the built-in setting of Injective onchain order book is more friendly to ordinary users, especially institutional strategic orders (for example, AMM cannot implement stop loss orders at present, Univ4 may be able to achieve it to some extent). AMM has a huge TVL, and LP has become an organic part of the entire market. For LOB, there are naturally no steps to pledge assets on the chain. The attraction of MM needs external subsidies, and it is difficult to form an LP similar to AMM. Ecology, unable to capture the value chain derived from LP ecology. Of course, AMM products can also be built on Injective, but currently the most important transaction volume of Injective still occurs on the front-end Helix of Orderbook.

Before Rollup improves LOB dex performance on a large scale, building a native chain on Cosmos is still the best solution for high-performance LOB. The launch of the DYDX v4 mainnet may squeeze Injective’s market share to a certain extent, depending on the transaction incentives of the two and institutional preferences. The LOB dex on Rollup will also form some competition, but due to the definition of dapp non-public chain and lack of sovereignty, the valuation system is completely different from the original order book chain. Both LOB DEX and AMM adopt a decentralized approach. At the current stage, there is no need to define the shape of the end game. This market always needs a variety of solutions.

Injective uses LOB as the core transaction model, which has the characteristics of "MEV protection". It provides a highly decentralized, high-performance and reliable environment by building on Tendermint and can be used for cross-chain derivatives, foreign exchange (FX), synthetic assets and futures Provides a safe and efficient platform for institutional order flow and market makers for trading applications, and eliminates the risk of market manipulation and exploitation by high-frequency traders. The implementation of frequent batch auctions makes Injective ready to compete with the trading volume of institutional-level centralized exchanges, making Injective a decentralized trading platform that is naturally supported by institutions. But this also means that the price of Injective is closely related to the support of institutional funds. In the next cycle, the high-performance chain-based trading engine, one-click release chain and other projects will further promote professional market makers to establish liquidity in the DEX field, and together with AMM will help gradually transfer pricing power from CEX to DEX.