Written by: David

Crypto payment cards are becoming an industry-wide business.

If you open social media such as Twitter, you can often see KOLs recommending various card types with different fees;

From centralized exchanges such as Binance, Coinbase and Bitget to crypto infrastructure such as Onekey Wallet, they have already joined this track, hoping to open up the channel between crypto assets and the real economy by issuing their own brand cards;

Image source: beincrypto.com

Recently, DeFi applications have also begun to plan the business of issuing cards.

In August, the decentralized stablecoin project Hope.money announced the issuance of HopeCard, which can be used for payment at merchants that support VISA around the world;

In recent days, Uniswap DAO has also launched a proposal to vote on whether to agree to issue VISA cards with the Uniswap logo...

Why is card issuing suddenly becoming popular in crypto circles?

When everyone wants to get a share of the exchanges, wallets, infrastructure, applications and even entrepreneurial teams focusing on card issuance, is there a good business behind encrypted payment cards?

Withdrawals and GPT, the trigger for demand

In fact, crypto payment cards are nothing new.

As early as 2015, Coinbase issued a Bitcoin-based crypto payment card. During the bull market wave of the past two years, although there were industry-related organizations exploring the card issuance business, its popularity and discussion were far less than today.

Why have crypto payment cards become particularly popular this year?

The key trigger may be the surge in demand brought about by withdrawals and ChatGPT .

The former represents the encryption circle’s desire for channel security, while the latter activates new payment scenarios .

First of all, withdrawing money is always a topic that cannot be avoided.

When the C2C withdrawal model becomes mainstream, the use of cryptocurrency for money laundering and the development of black and gray industry businesses are also using this channel. You will never know whether your next transaction will be frozen due to the above reasons. .

So much so that we often see various "perfect withdrawal" strategies popular on the Internet, and deposit and withdrawal service providers use "no freezing cards" as a selling point. These all indicate that there is an urgent need for safe withdrawals in the market.

Therefore, crypto payment cards have room for survival: instead of spending energy on researching withdrawals, it is better to use this card to bind commonly used payment methods and directly use cryptocurrencies for daily consumption .

In addition, the emergence of subscription services such as ChatGPT has also contributed to driving demand for encrypted payment cards.

For the trendsetters in the technology circle, GPT is undoubtedly the focus of the audience.

However, if you want to experience the updated and more powerful functions of GPT-4, you need to pay a monthly Plus membership subscription fee, and OpenAI does not accept mainstream domestic credit cards and debit cards.

In this case, encrypted payment cards successfully resolved the embarrassment of geographical restrictions.

The card numbers of most encrypted payment cards start with 4 or 5 and belong to American card organizations (VISA / Master / American Express, etc.). They perfectly meet OpenAI's requirements for card types and can convert cryptocurrency into US dollars to complete the recharge.

At the same time, most of these cards also support overseas shopping on foreign e-commerce platforms (Amazon, eBay, Shopee, etc.) and subscriptions to other software (Midjourney, Netflix, etc.); and with the end of the epidemic, for users with cross-border consumption scenarios For example, encrypted payment cards are also a convenient choice.

However, it needs to be pointed out that quite a few reports are using concepts such as "encrypted VISA card", "encrypted credit card" or "encrypted card" interchangeably, so that in the overwhelming social media promotion and publicity, a considerable number of novices do not know What kind of card is it that I am using?

If you want to pay with a card, it is the same as a bank card in traditional finance. There are two main forms: credit card (Credit Card) and debit card (Debit Card).

The former allows you to overdraft, that is, spend first and repay later; while the latter requires you to deposit first and then spend.

In the current market environment , most of the more popular ones are actually encrypted prepaid debit cards: there is no need to bind an existing bank account, but the cryptocurrency needs to be converted into legal currency and loaded into the card in advance .

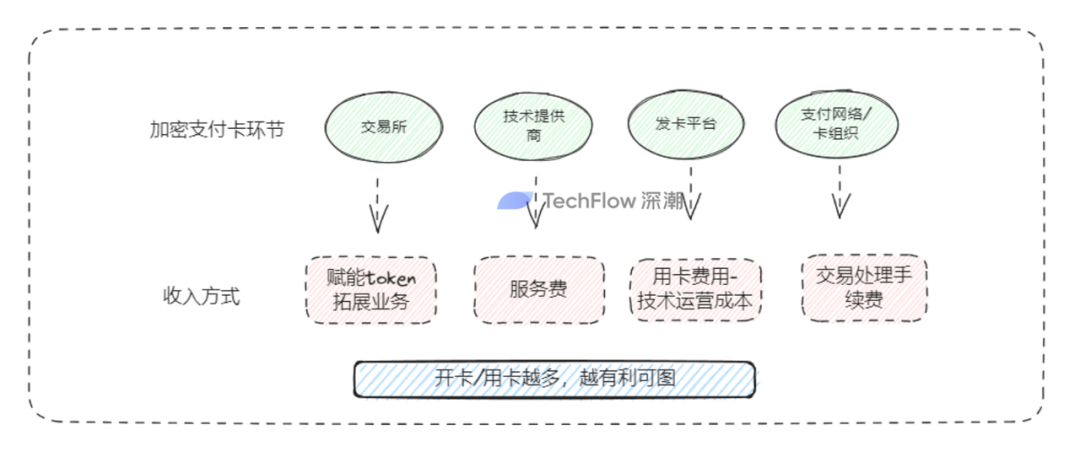

Card issuance as a service, replicating the driving force behind the popularity

Exchanges are issuing cards, wallets are issuing cards, and payment startup teams are also issuing cards... Can anyone issue an encrypted payment card?

In our inherent impression, issuing credit cards and debit cards seems to be the patent of banks, and there are high technical and qualification thresholds to carry out this business; but in the field of encrypted payment cards, this is not the case.

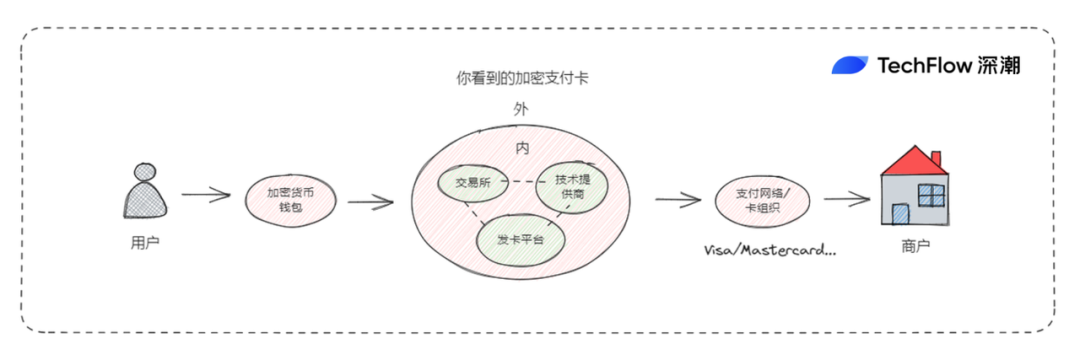

When a user sees a card bearing the brand of a certain cryptocurrency exchange and the VISA logo, what is unknown behind it is actually the cooperation model between the card issuer and the technology provider.

For example, Coinbase's VISA card is actually supported by technology provider Marqeta, which enables it to issue encrypted debit cards and provide users with real-time transaction authorization and fund conversion services; similar providers include Immersve, Reap, Striga and Alchemy Pay, which are more familiar to domestic readers, etc.

Furthermore, the issuance process of crypto payment cards becomes simpler due to the role of “ technology provider ”.

In the complete chain from payment initiation to completion, it goes without saying that traditional roles such as users, merchants and card organizations (Visa/MasterCard) need not be mentioned; technology providers provide a capability similar to " card issuance as a service ":

Support crypto card issuance, currency conversion and payments by providing the necessary security technology, payment processing systems and user interfaces to organizations that need to issue cards.

The card issuing party only needs to call the technology provider's API or SaaS solution to issue and manage encrypted credit cards/debit cards.

At the same time, the technology provider's "card issuance as a service" also includes a variety of functions including transaction authorization, fund conversion, transaction monitoring and risk management, helping card issuers simplify operations and improve efficiency.

Therefore, in theory, institutions subject to compliance supervision or holding licenses, with the support of technology providers, can issue encrypted payment cards. This is why we can see a variety of encrypted payment cards from different issuers on the market.

Take Galileo, a well-known overseas solution provider, as an example. Its API has been integrated with payment networks such as Visa and MasterCard, and it has also established cooperative relationships with upstream and downstream industries such as card issuing banks. Demand parties can complete card issuance by calling its services. .

As you can see from the picture above, cryptographic applications that require card issuance may only need to provide wallet addresses and management accounts (purple). Consumers' card opening, transactions, authorization, settlement and other behaviors are all completed by Galileo (blue).

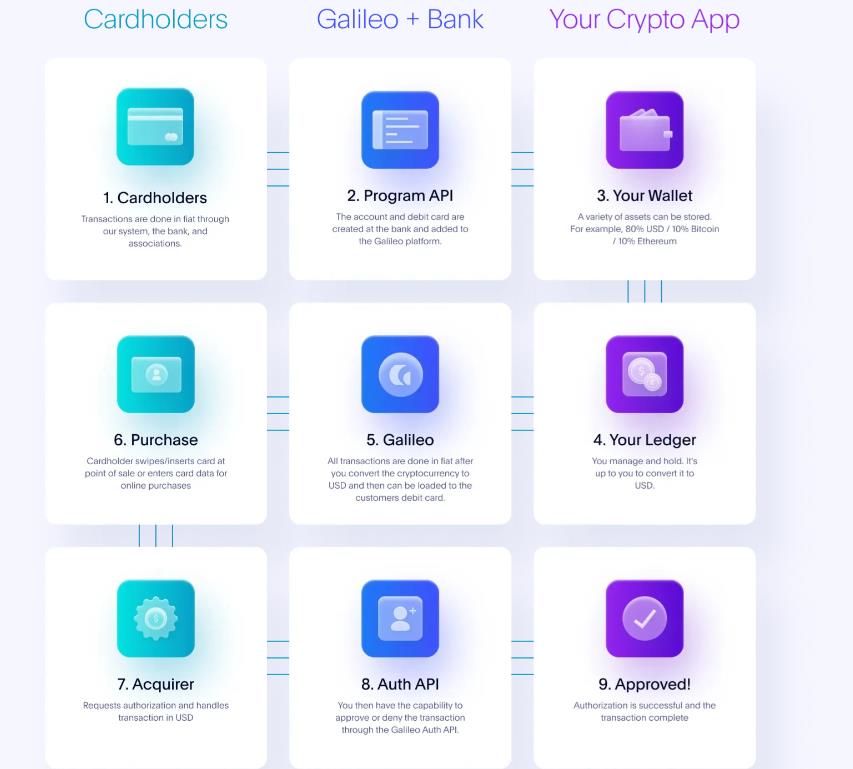

And Galileo's technical solution is not an isolated case.

In July this year, the well-known multi-signature wallet Gnosis Safe launched Gnosis Pay, a network dedicated to encrypted payments, which also supports the issuance of Visa cards.

One end of this technical solution is bound to an encrypted wallet, and the other end connects the banking system, Visa, MasterCard and third-party payments. In the middle, a Polygon-based L2 is specially built to handle the conversion and payment between cryptocurrency and traditional finance.

Similarly, Gnosis also plays the role of a technology provider: providing a set of developer integration tools, opening API calls, and allowing other encryption applications to customize their own payment cards.

Overall, technology providers are more like bridge builders, bridging the gap between the crypto world and traditional finance, allowing more payment applications to run on this bridge.

The geese are plucked, and the business experience in the payment chain

Having said that, why is everyone so focused on the crypto payment card business?

Crypto payment cards are a multi-party business form, and each party in the chain has profit aspirations and their own business experience.

For large exchanges : making encrypted payment cards is not just about paying a small amount of card opening fees and handling fees. It is often combined with other businesses of the company:

Empower your own token : You can get token cashback by using encrypted payment cards, such as Binance Card’s BNB, and Crypto.com’s CRO, etc. This will go a long way to increasing the influence and awareness of your own token; at the same time, according to the pledge Depending on the amount of BNB or CRO, the equity level of the payment card will also change, which may also attract users to purchase or pledge their own tokens;

Expanding trading business : With huge traffic and users in hand, exchanges are still trying to get out of the digital currency trading business and expand more C-side payment scenarios. Although affected by compliance issues, the development logic is clear - refer to WeChat, which after accumulating a large amount of traffic and stickiness, makes payments based on social networking.

For encryption application/technology providers : If they are engaged in hardware/software wallets, then it seems logical to engage in payment card business. Since they can provide users with storage services of encrypted assets, it is inevitable to open up the next consumption link;

Another technology service provider, such as AlchemyPay or the aforementioned Galileo and Gnosis, encrypted payment cards have become a business selling SaaS services, collecting money according to calls from B-side customers or customized services;

For other card issuers : the income after card issuance consists of card opening fees, annual/monthly fees, transaction fees, etc. At the same time, according to the author’s understanding, some card issuers will also use the amount deposited by users in the card to make U.S. government bonds. Invest and get a share of RWA’s earnings.

For card organizations : VISA and Mastercard are in the business of accepting everyone who comes, and the more the better. Whether it is an encrypted payment card or a traditional bank card, the more users spend, the number of transactions, and the number of overseas transactions, the more handling fees they receive from clearing and settlement. The larger the amount, the higher the revenue.

Every link in the crypto payment chain is profitable for users. As long as regulations and the general economic environment are stable, this seems to be a win-win business for all parties.

Cakes in the big market

The narrative in the crypto world is changing rapidly, but in the final analysis, most of it is still inside the circle.

In terms of business attributes, encrypted payment cards are a track that needs to “go outward”:

Whether it is short-term withdrawal and GPT subscription service needs, or long-term compliance, using the convenience of cryptocurrency in cross-border payments to open up more online and offline payment scenarios, what crypto payment cards want to do , is an "export" business, and the cake is undoubtedly huge.

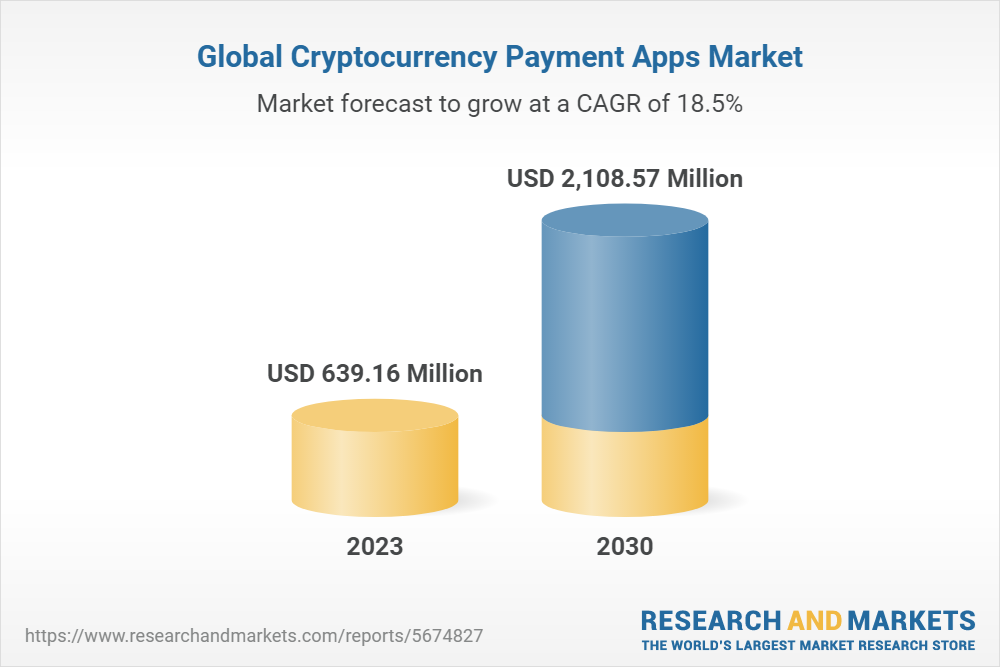

Relevant research reports also show that the compound annual growth rate of global crypto payment applications exceeds 18%, and crypto payments are likely to form a market size of 1 billion.

And the rewards for slicing a small piece of cake in such a big market are obviously huge. This may also be one of the important reasons why all parties in the industry are actively deploying encrypted payment cards.

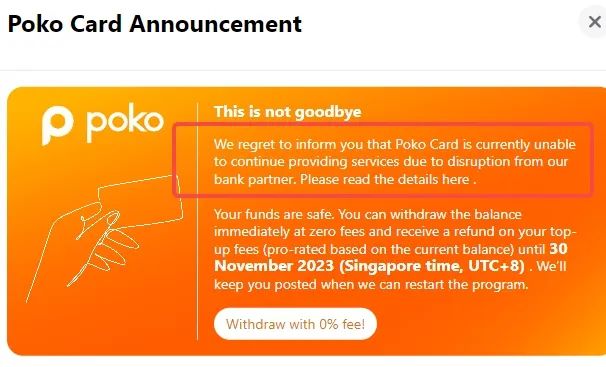

But looking at reality, any product also has current risks and limitations.

Crypto payment cards may stop serving due to poor cooperation with banks. If users do not check emails or use the card regularly, they may miss the withdrawal time and cause losses; at the same time, with the tightening of supervision and changes in the attitude of card organizations, , even an industry leader as strong as Binance may suspend card issuance because of this.

The revolution has not yet succeeded, and comrades still need to work hard .

We look forward to the pie getting bigger and end-users getting a taste of the benefits on the crypto payment card table.

At the same time, in the next article, we will also conduct in-depth research on the card opening conditions, functions, rates and discounts of mainstream crypto payment cards in the market, providing more practical and useful references for everyone to choose and use cards. Stay tuned.