As I said before, there's no need to panic (Part 3): Interest Rate Hike Expectations Have Declined

Last night, the Federal Reserve released the minutes of its April meeting, indicating that interest rate hikes have begun.

However, recent medium- and long-term US Treasury yields have changed the environment.

┈➤In fact, the US has been in a soft landing phase.

In the past two or three years, there have been frequent reports of things going wrong—first employment, then US Treasury yields, then weak GDP growth… Think back, hasn't this been the case for the past two years? It always feels like a recession is imminent.

This has always been Powell's strategy.

When the pandemic hit, there was massive monetary easing, temporarily halting the recession. Then came interest rate hikes and balance sheet reduction, keeping the economy close to recession thresholds, almost in recession but not actually in recession.

Whenever the economy is in danger, interest rates are lowered. Three rate cuts are expected by the end of 2024, three in 2025, and in 2026, if it weren't for Iran's blockade of the Strait of Hormuz causing oil prices to plummet, there would likely have been rate cuts as well.

┈➤Interest Rate Hike Expectations Declined

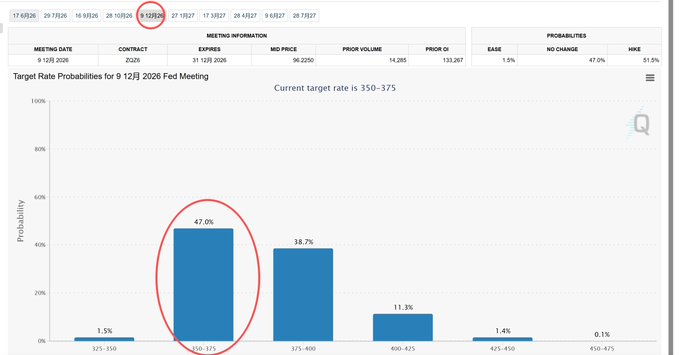

The current US Treasury yields indicate risk, thus weakening the conditions for interest rate hikes. CME Group interest rate futures showed that the market previously expected one rate hike in 2026, but yesterday, the situation changed, with market expectations shifting to unchanged rates in 2026.

If US Treasury yields remain high, it even increases the possibility of a rate cut. While the Federal Reserve can disregard the Treasury's financing costs when US Treasury yields rise, it cannot ignore the impact on the pricing and risk of other assets (US stocks, real estate, and almost all other assets).

A rate cut is something the Federal Reserve can do.

As mentioned in the previous article, the rise in short-term bonds and the fall in long-term bonds reflects market expectations for future inflation, US Treasury expansion, and even dollar easing.

twitter.com/blockTVBee/status/...