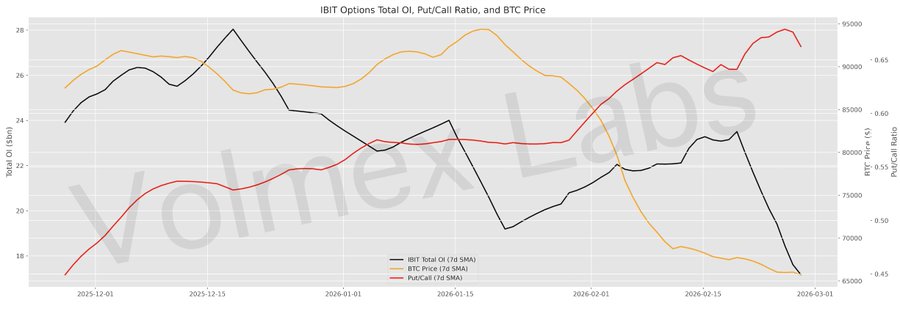

IBIT ETF options currently indicate less risk-taking and more downside protection.

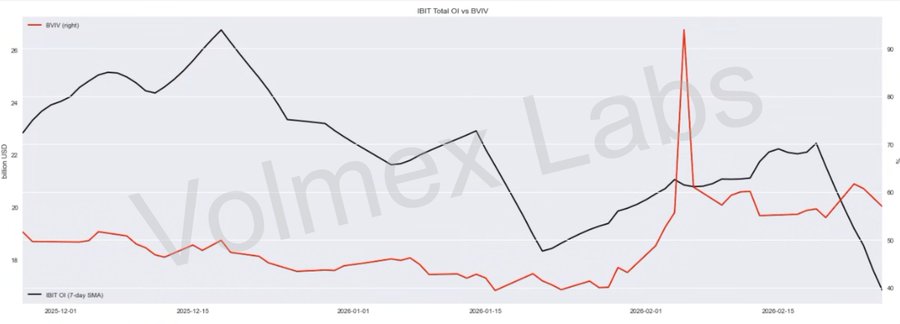

• IBIT options open interest (OI) deceased materially from mid-Dec (~$28B, ~Dec 18). For context, all-time high IBIT options OI was above $40b in Q4 2025.

• By Feb 27 (4pm ET), IBIT OI was ~$15B — about 45% below the mid-Dec peak (last ~3 months).

• As OI fell, put/call ratio rose (from 0.47 to 0.64; briefly 0.74 on Feb 20). That means traders preferred more protection, or call positions were closed faster.

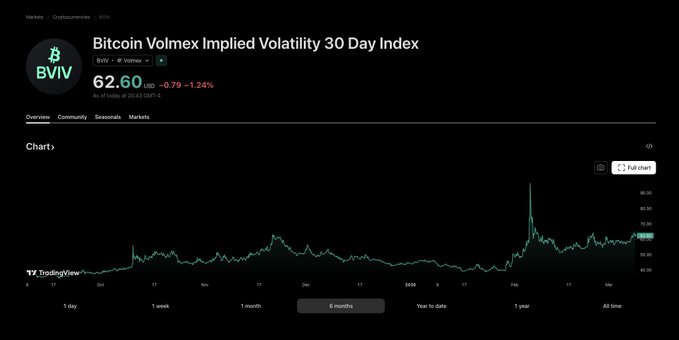

• The BVIV Index and BVIV-US Index respectively increased 9.62% and 4.66% in February. Both indices saw extreme moves on February 5th.

• Bottom line: IBIT options data currently indicates more defensive positioning.