Today

Intel

Market

Earn

Settings

Account

Theme Selection

Light

Dark

Language

English

简体中文

繁體中文

Tiếng Việt

한국어

Followin APP

Mine Web3 Possibilities

App Store

Google Play

Log in

Crypto Rocketeer

189,443 Twitter followers

Follow

Crypto OG since 2011 | Early Investor | Crypto Trader | Web3 Writer | Portfolio ATH $4M | Marketing Advisor Channel: http://t.me/teamrocketeer

Posts

Crypto Rocketeer

Thread

#Thread#

ADI Predictstreet | @Predictstreet may be the largest distribution deal crypto has ever seen Imagine watching the 2026 World Cup. You predict the winner, goalscorer, halftime result a few times during the tournament. You don’t need to understand blockchain, but every interaction is a transaction. Now scale that: 104 matches → 2,600+ prediction markets, ~6B viewers. If 0.1% participate → ~6M users → ~30M tx. At 1–5% → 300M → 1.5B tx. And this is only match predictions. The FIFA Bracket Challenge, one of the most viral World Cup mechanics, is now powered by ADI Predictstreet. Each entry = another onchain tx. Everything runs on @ADIChain_ → every interaction requires $ADI for gas. Even at tens of millions or 1B+ tx, this is structural demand for $ADI, starting from World Cup 2026. ADI Predictstreet is the Official Prediction Market Partner of FIFA World Cup 2026™ and the first global partner in this category. ADI Predictstreet operates at a level of distribution rarely seen in crypto. When execution is right, $ADI is directly tied to real usage. DYOR. twitter.com/Defi_Rocketeer/sta...

ADI

1.67%

Crypto Rocketeer

04-01

Thread

#Thread#

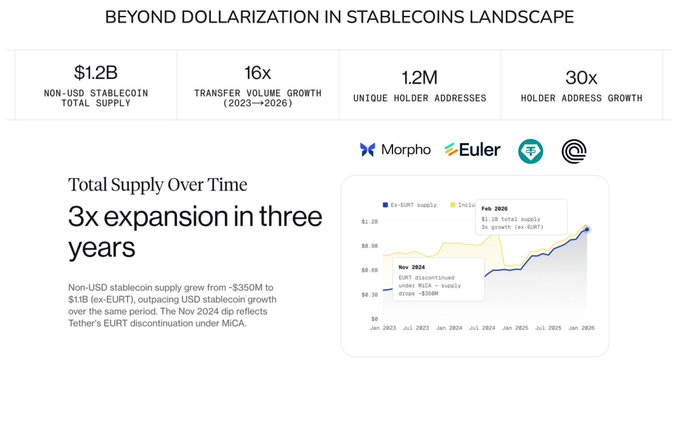

~$1.2B in non-USD stablecoins vs ~$300B USD stables made me realize crypto liquidity is just dollarized. at first, I thought stablecoin dominance was just a scale thing. Like USD got there first, liquidity compounds, others will catch up later. But after digging into how the flows actually behave, I don’t think it’s that simple. Here’s how I frame it: 1/ The data looks small, but the signal is loud - Total stablecoins: ~$315B vs Non-USD: ~$1.2B (~0.4%). - Transfer growth: +16x since 2023 an Users: +30x. So yeah, size is tiny but adoption curve is not. 2/ Liquidity is about usage - ~80% of non-USD flows = payments, payroll, settlement. - Only ~29% lending, ~17% DEX, ~14% CEX. Compare that to USD stables and I realized it’s heavily financialized, looping in DeFi and collateral for leverage. If I’m being honest, most USD liquidity is still inside the system, non-USD liquidity is already touching the real world. 3/ Not all stablecoin liquidity is the same There are 2 completely different liquidity systems forming: (1) USD liquidity - global, financialized. Dominant in DeFi, RWAs, collateral, backed by T-bills → deeply tied to TradFi. Extremely efficient, but centralized around a few issuers. This is where players like @tether | $USDT and @circle | $USDC completely own the game. (2) Local currency liquidity - regional, transactional This is used for payments, FX, settlement, plugged into local rails, kinda less liquid, but more economically real. Some references I’m watching: - $EUR → dominating DeFi lending within Aave, Morpho. - $BRL → integrated with PIX. - $SGD / $JPY → cross-border settlement in Asia. It’s finance entering crypto rails elsewhere, outside of crypto and outside of dollarizarion. Top protocols I’m watching right now: → @SkyEcosystem | $SKY - USDS & DAI combined ~$13-16B (USDS ~$8-11B + DAI ~$4.5B). Endgame rollout emphasizes RWA integration. → @ethena | $ENA - USDe ~$5.9B. Integrates with DeFi for "cash-and-carry" yields. → @PayPal - PYUSD ~$4B, enterprise payments focus. → @fraxfinance - FRAX/USDF, Algorithmic/hybrid models. → White-label infrastructure: Bridge (Stripe), @brale_xyz , @m0 , @Paxos - enable enterprises to launch custom stables quickly. 4/ Where liquidity infra is actually being won There are 3 layers that matter: → Issuance = still dominated by USDT / USDC, but local issuers will win regionally (regulation + banking access). → Liquidity sinks in money markets such as Aave, Morpho, etc. whoever captures deposits → controls idle liquidity. → Payment + settlement rails where real volume is forming, integrations > incentives 5/ My takeaway USD stablecoins won phase 1 → store of value + DeFi collateral. Non-USD stablecoins are playing phase 2 → real payments + local settlement. If that continues, liquidity will fragment across currencies, regions, and rails. I do think we’re moving from one global liquidity pool → to many localized liquidity zones connected onchain. And honestly, that system is way harder to build but also much closer to how real economies actually work. DYOR.

ETH

0.95%

Loading..