Written by Andrew Kang

Compiled by: J1N, Techub News

The passage of a Bitcoin spot ETF opened the door to the cryptocurrency market for many new buyers, allowing them to allocate Bitcoin in their portfolios. However, the passage of an Ethereum spot ETF has had a less obvious impact.

When the BlackRock Bitcoin Spot ETF application was submitted, I was strongly bullish on the price of Bitcoin, which was at $25,000 at the time. So far, Bitcoin has returned 2.6 times and Ethereum has returned 2.1 times. Since the bottom of the cycle, Bitcoin has returned 4 times and Ethereum has also returned 4 times. So how much upside can the Ethereum ETF provide? I don't think there will be much upside unless Ethereum develops a new model to improve its economic conditions.

I said on June 19, 2023 that BlackRock's application for a Bitcoin spot ETF had a 99.8% approval rate, which was the most positive news we had heard recently and could open the floodgates for tens of billions of dollars in capital flows. However, the price of Bitcoin rose only 6%, and the price performance did not meet expectations.

Traffic Analysis

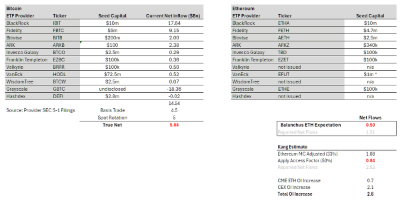

Overall, while Bitcoin spot ETFs have amassed $50 billion in AUM. However, when breaking down net inflows since launch by excluding pre-existing GBTC AUM and swaps (selling futures, buying spot ETFs), you get $14.5 billion in net inflows. However, these are not true inflows as there are a lot of delta neutral flows to consider, namely basis trades (selling futures, buying spot ETFs) and selling spot to buy spot ETFs. By looking at CME data and analyzing ETF holders, I estimate that approximately $4.5 billion of net flows can be attributed to basis trades. ETF experts say that large holders such as BlockOne have also converted large amounts of spot Bitcoin into spot ETFs, roughly estimated at $5 billion. Netting out these flows, we arrive at a true net purchase of $5 billion for Bitcoin spot ETFs.

In this way we can simply infer what the flow of funds for Ethereum will be. Bloomberg ETF analyst @EricBalchunas estimates that Ethereum flow may be 10% of Bitcoin. This makes the real net purchase flow in 6 months $500 million and the reported net flow of $1.5 billion. Although @EricBalchunas's prediction is not very accurate, I believe he represents the attitude of a number of traditional financial institutions.

Personally, I think Ethereum traffic is probably 15% of Bitcoin. Starting with the $5 billion of real net purchases of Bitcoin (mentioned above), by adjusting for Ethereum market cap (33% of Bitcoin) and a ⎡access factor⎦ of 0.5, we get $840 million of real net purchases and $2.52 billion of reported net purchases. There are some reasonable arguments that ETHE (Grayscale Ethereum Futures ETF) has less premium than GBTC, so I think the optimistic case is $1.5 billion of real net purchases and $4.5 billion of reported net purchases. This is about 30% of Bitcoin traffic.

In either case, the estimated $1.5 billion in real net purchases of Ethereum spot ETFs is far lower than the current $2.8 billion in Ethereum derivatives inflows, which does not include preemptive trading of spot (referring to market expectations of a bullish trend and buying spot in advance). This means that the inflows before the Ethereum spot ETF is listed exceed the estimated inflows of Ethereum spot ETFs, so the price of Ethereum spot ETFs has been largely priced in by the market.

⎡Access Coefficient⎦: Adjusted for the liquidity achieved by the ETF, Bitcoin clearly benefits more than Ethereum given the different holder bases. For example, Bitcoin is a macro asset and is more attractive to institutions with access issues (macro funds, pensions, endowments, sovereign wealth funds). Ethereum, on the other hand, is more of a technology asset and is more attractive to institutions that are not as restrictive in terms of crypto access, such as VCs, crypto funds, technologists, retail investors, etc. 50% is derived by comparing the CME OI (Open Interest, derivatives open interest) to market cap ratio of Ethereum to Bitcoin.

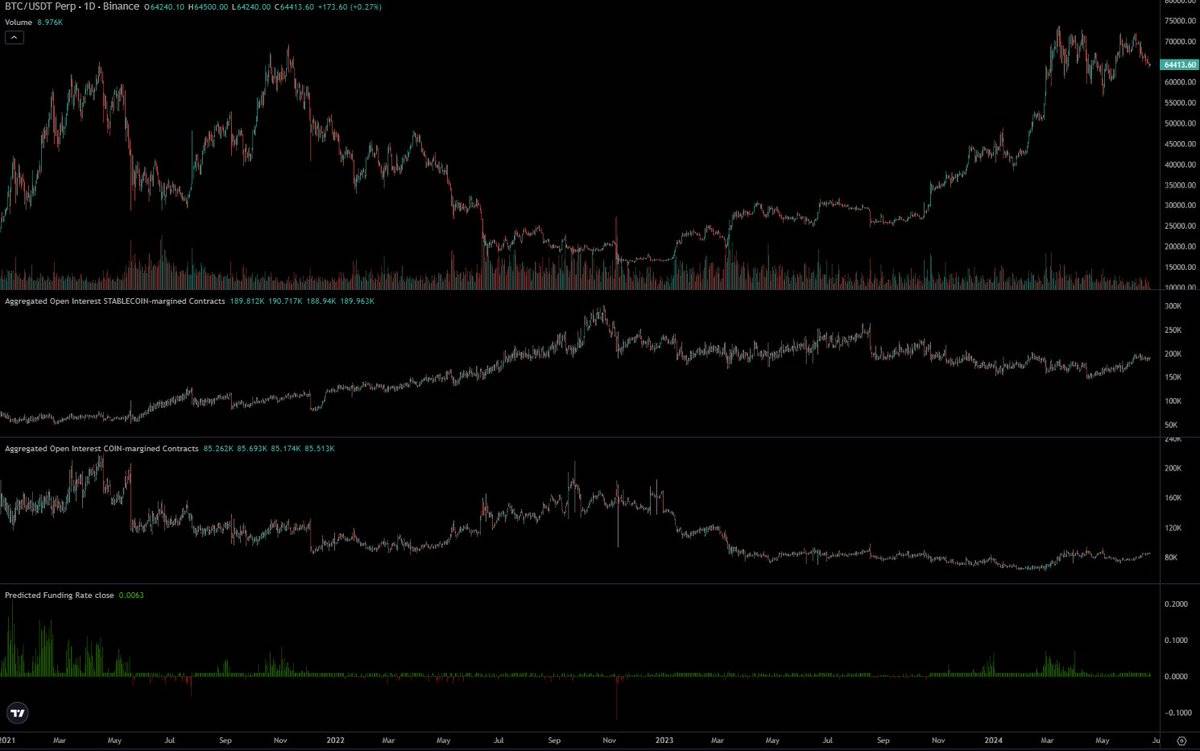

Looking at CME data, Ethereum's OI was significantly lower than Bitcoin's before the Ethereum spot ETF was launched. OI was about 0.3% of supply, while Bitcoin was 0.6% of supply. At first, I thought this was a sign of early days, but one could also argue that this masks the fact that traditional financial funds have a lack of interest in Ethereum ETFs. Wall Street traders are more likely to trade Bitcoin spot ETFs, and they often have front-line information, so if they are not using the same trading method on Ethereum, then there must be a good reason, which may mean that there is insufficient information about Ethereum liquidity.

How $5 billion pushed Bitcoin from $40,000 to $65,000

The most clear and direct answer is that $5 billion alone cannot do it. Because there are many other buyers in the spot market. Bitcoin is an asset that is truly recognized as a key portfolio asset worldwide, and has many large institutions holding it for a long time, such as Saylor, Tether, family offices, high net worth individual investors, etc. Although Ethereum is also held by large institutions, I think its order of magnitude is lower than Bitcoin.

Remember, before the emergence of Bitcoin spot ETFs, Bitcoin's highest price had reached $69,000, with a market value of over $1.2 trillion. Market participants and institutions own a large amount of spot cryptocurrencies. Coinbase custody $193 billion, of which $100 billion comes from other institutions. In 2021, Bitgo reported an AUC of $60 billion and Binance custody over $100 billion. Six months later, Bitcoin spot ETFs custody 4% of the total supply of Bitcoin.

I tweeted on February 12th and expressed my opinion on the size of the cryptocurrency market, ⎡ I estimated that long-term Bitcoin demand is $40-130+ billion this year. One of the most common pet peeves for crypto investors is underestimating the wealth in the world, how much people earn, how liquid money is, and how that affects crypto. We hear statistics about the market cap of gold, stocks, real estate so often that crypto can be overlooked by many. Many crypto people are stuck in their own box thinking, but the more you travel and meet other business owners, high net worth individuals, etc., the more you realize how unimaginable the amount of dollars there is in the world and how much of that can go into Bitcoin or other cryptocurrencies.

Let me explain this with a rough demand sizing exercise. The average US household income is $105k. There are 124 million US households in the US, which means the total annual income of US individuals is $13 trillion. The US accounts for 25% of GDP, so the global total is about $52 trillion. The average global cryptocurrency ownership is 10%. In the US, it is about 15%, and in the UAE it is as high as 25-30%. Assuming that cryptocurrency owners only allocate 1% of their income each year, it would cost $52 billion per year to buy BTC, or $150 million per day ⎦.

MSTR (Microstrategy) and Tether bought billions of dollars of Bitcoin when the Bitcoin spot ETF was launched, and investors who entered the market at that time also had low holding costs. At that time, people generally believed that the passage of the Bitcoin spot ETF was a signal for shipment. Therefore, billions of dollars of short-term, medium-term and long-term positions have been sold and need to be bought back. On top of that, once the Bitcoin spot ETF flow forms a significant upward trend, the shorts need to buy back. Before the launch of the Bitcoin spot ETF, the open interest actually declined, which is crazy.

Ethereum spot ETF is positioned very differently. Ethereum price is now 4x from pre-spot ETF low, while Bitcoin is 2.75x. Crypto native CEX OI increased by $2.1 billion, bringing OI close to ATH levels. Markets are efficient. Of course, many crypto natives saw the success of Bitcoin spot ETF and they also had the same expectations for Ethereum and positioned accordingly.

Personally, I think the expectations of crypto native users are exaggerated and out of touch with the real preferences of traditional financial markets. This results in relatively high mind share and purchases of Ethereum by those deeply involved in the crypto space. In reality, for many large non-crypto native capital groups, the purchase of Ethereum as a key portfolio allocation is much lower.

One of the most common pitches from traditional finance is that Ethereum is a ⎡tech asset⎦. The global computer, the Web3 app store, the decentralized financial settlement layer, etc. This is a nice pitch, and I bought it in the last cycle, but it’s hard to swallow when you look at the actual returns.

In the last cycle, you could point to the growth rate of fees and argue that DeFi and NFTs generate more fees, cash flow, etc. and make a compelling case as a tech investment through a similar lens to tech stocks. But in this cycle, the quantification of fees is counterproductive. Most charts will show flat or negative growth. Ethereum is a cash machine, with $1.5 billion in revenue in just 30 days based on its annualized rate, a P/E ratio of 300 times, and a negative P/E after deducting inflation, how will analysts justify this price to their family office or macro fund bosses?

I even expect the first few weeks of fugazi (usually refers to seemingly large volume that is not caused by actual capital inflows) flow to be lower for two reasons. First, the approval of the Ethereum spot ETF was unexpected, and the issuer did not have much time to convince large holders to convert their Ethereum to the spot ETF form. Second, it is less attractive for holders to convert because they need to give up the yield on staking or Ethereum in DeFi. But please note that the current Ethereum staking rate is only 25%.

Does this mean that Ethereum will go to zero? Of course not, at a certain price, it will be considered good value for money, and when Bitcoin rises in the future, Ethereum will not necessarily follow. Before the launch of the spot ETF, I expect Ethereum to trade between $3,000 and $3,800. After the launch of the spot ETF, my expectation is $2,400 to $3,000. However, if Bitcoin rises to $100,000 in Q4 2024 or Q1 2025, then this may push the price of Ethereum above the ATH, but Ethereum and Bitcoin will go lower afterwards. In the long run, there are some developments to look forward to, and you have to believe that BlackRock and Fink are doing a lot of work to build some financial infrastructure on the blockchain and tokenize more assets. How much value this can bring to Ethereum and the specific time are still uncertain.

I expect Ethereum Bitcoin to continue trending downwards, with the ratio between 0.035 and 0.06 over the next year. Although our sample size is small, we do see Ethereum Bitcoin making lower highs every cycle, so this should not be surprising.