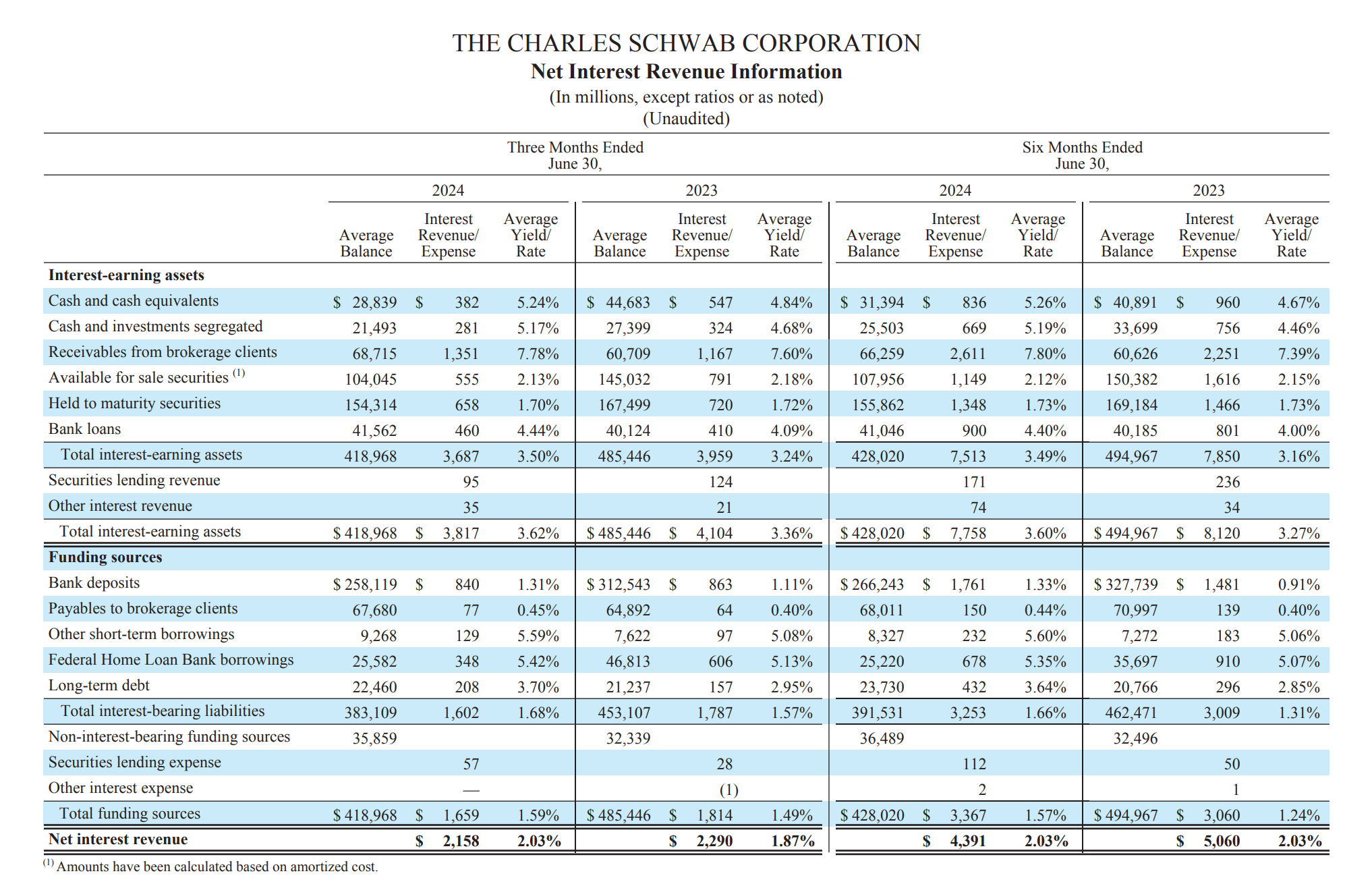

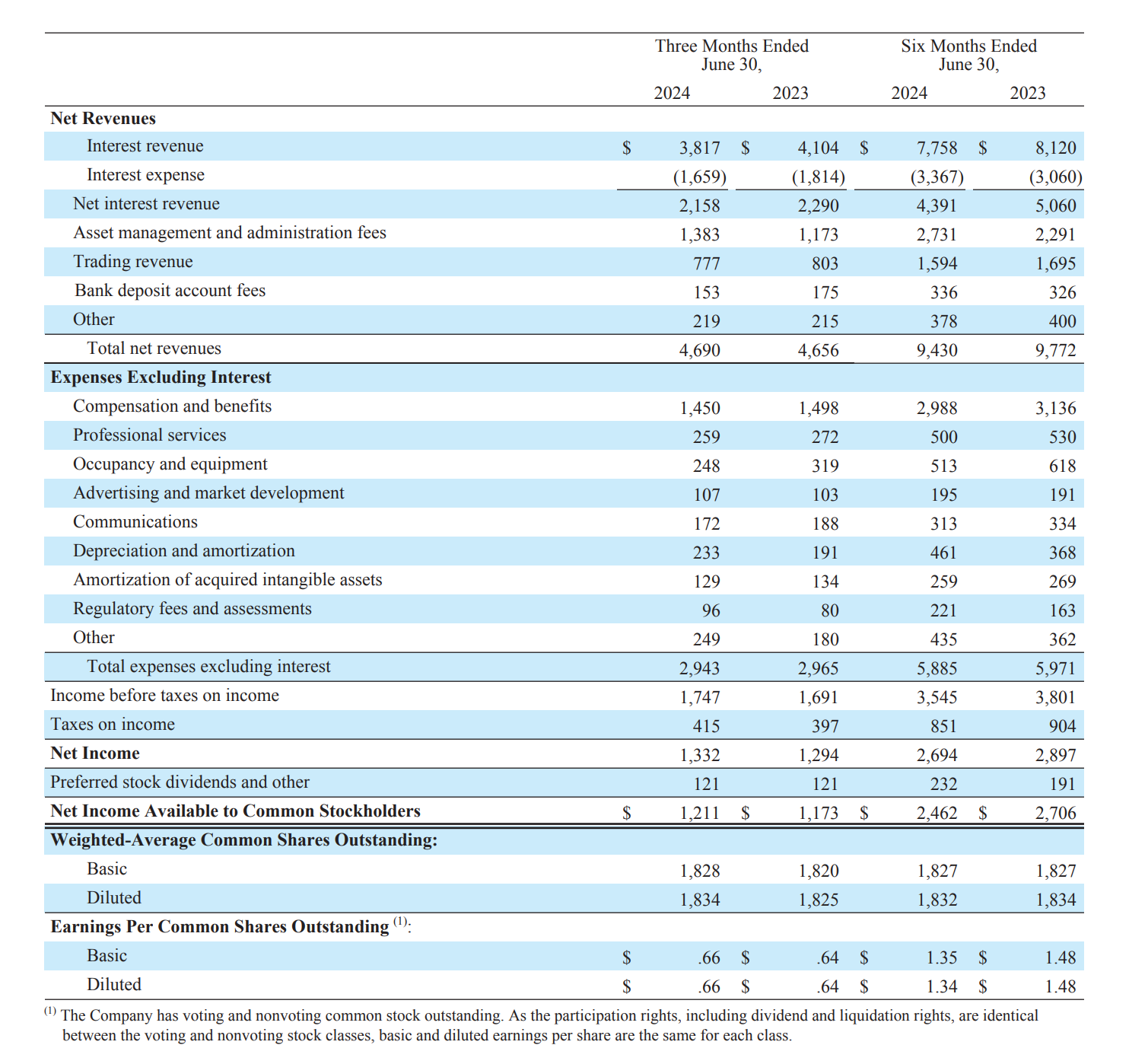

Schwab reported Q2 earnings yesterday. Revenue was $4.69B vs. $4.68B expected. Adjusted EPS was $0.73 vs. $0.72 expected. Net interest income fell 5.7% YoY and bank deposits fell 17.4% YoY. In addition, Schwab still has $154B (or ~37% of its total assets) of HTM (held-to-maturity) security on its balance sheet that’s earning a whopping 1.7% yield while borrowing $25.6B from FHLB at 5.42%. Q2 2023 is the first quarter after the SVB fiasco. If they were doing well, the deposits shouldn’t have fallen so much from Q2 2023 to Q2 2024. Their average 3-month bank balance is $258B for Q2 2024 vs. $424B for Q4 2022, a ~40% drop. It appears, due to the high interest rates, the bank deposits are still fleeing. In the meantime, Schwab is pretty much stuck with the HTM assets that are paying a very low yield.

Theoretically, they are making $1.3B this quarter. But the opportunity cost of the HTM security is basically 154B*(5-1.7)%*1/4 = 1.27B, which pretty much offset all the income they made for the quarter. Unfortunately, Schwab will need to deal with the very low-yielding HTM portfolio for a while. ZIRP period is not coming back any time soon while the bank deposits are still fleeing to higher yielding products. Schwab stock tanked 15% after the earnings. I believe Schwab will slowly recover from the HTM mess but they basically have to pay for it with all the profits generated from asset management and trading for a few years. It’s totally understandable why investors are frustrated.