Author: Ji Zhenyu, Tencent News "Qianwang"

Global stock markets entered a panic plunge mode.

In early August, the Bank of Japan and the Federal Reserve successively announced their monetary policy decisions. The Bank of Japan announced a 25 basis point interest rate hike, while the Federal Reserve announced that it would maintain the benchmark interest rate unchanged, but clearly released a signal that there is a high probability of a rate cut in September.

The market reacted to the news, and the yen-dollar exchange rate soared sharply, and the "carry trade" of borrowing cheap yen to enter the high-yield market came to an end. The Fed's clear signal of interest rate cuts only boosted the US stock market for one day. In the trading days in early August, the Japanese, European and US stock markets experienced a comprehensive decline.

The greater concern comes from the negative signals from the fundamentals of the US economy. The ISM manufacturing index, which reflects factory activity, was lower than expected, the number of first-time unemployment claims hit a new high since August 2023, and the US non-farm payrolls data in July showed that the unemployment rate rose further. For a time, panic about the US economy's impending recession swept the market.

Criticisms of the Fed have also followed, with many economists pointing out that the Fed's path of making corresponding monetary policy adjustments based on economic data is too conservative and lagging. Judging from the current situation, "standing still" in July was a wrong decision, and the Fed can only make up for it in the future by increasing the scale of interest rate cuts.

With the new round of economic data and changes in the macro environment, investors' expectations have also begun to change, and expectations of a sharp interest rate cut by the Federal Reserve before the end of the year have begun to dominate the market.

In addition to macro factors, concerns about whether generative AI can deliver on its large-scale investment have also begun to weigh on the market. In early August, trillion-dollar tech giants such as Microsoft, Google, Apple, and Meta released their financial reports. In this round of generative AI, although the giants are still investing heavily, the corresponding new revenue and profits have not increased proportionally, and Wall Street has begun to rethink the corresponding valuations.

In fact, the overall rise of the U.S. stock market this year has been mainly driven by the strong rise of giant companies that benefited from the concept of generative AI. The trend of capital concentration in leading companies has intensified. Apart from these factors, the stock price performance of most listed companies in the U.S. stock market is not very ideal. After this round of general correction of technology giants, the U.S. stock market may enter a new round of adjustment period.

Another signal may support the above view. The latest second quarter financial report released by Berkshire Hathaway, owned by Warren Buffett, shows that Buffett significantly reduced his holdings of Apple, his largest holding, by nearly 50% in the quarter, while cash reserves reached a record high of US$276.9 billion, a significant increase of 46.5% from the first quarter. The "stock god" who has been in the U.S. stock market for more than half a century may have noticed the market abnormality in advance.

Currently, "recession trading" dominates the market and bearish sentiment is spreading, but on the other hand, the Federal Reserve's interest rate cut in September and subsequent large-scale interest rate cuts have become high-probability events, which may provide conditions for the subsequent market to rise.

A person from a US private equity firm who used to work for Citadel, Point72 and other institutions told Tencent News "Qianwang" that usually in extreme market conditions, investors are prone to such a dilemma. On the one hand, the previous positions suffered heavy losses and were easily affected by the extremely pessimistic sentiment of the market. On the other hand, some investors are considering "buy the dips", but judging from the current market conditions, it may take a period of correction, and blindly entering the market may be irrational. He suggested that ordinary investors make corresponding decisions after this round of volatility slows down and the market trend becomes clearer.

Panic sell-offs started around the world, and no major market was spared

On August 1, the Dow Jones Industrial Average fell more than 700 points during intraday trading, the S&P 500 fell 1.37% throughout the day, the Nasdaq Composite fell 2.3%, and the Russell 2000 Index, which covers more small and medium-sized enterprises, fell more than 3%.

On August 2, with the release of the latest U.S. non-farm payrolls report, the market not only showed no signs of stopping its decline, but the extent of the decline continued to increase. U.S. stocks continued to fall across the board, with the S&P 500 index continuing to plummet 1.84%, the Nasdaq Composite Index falling more than 2.4%, and the Russell 2000 index continuing to fall by more than 3%.

Investors' pessimism enveloped global markets, and almost all major markets were affected. Japan's Nikkei index continued to fall on August 1 and 2, hitting the largest single-day drop in more than four years, and European stock markets also fell across the board.

On August 5, the Japanese stock market continued to fall after opening, with the Nikkei 225 index falling more than 4% and the Topix index falling 3%. The Nikkei 225 index fell below 35,000 points for the first time since January 11.

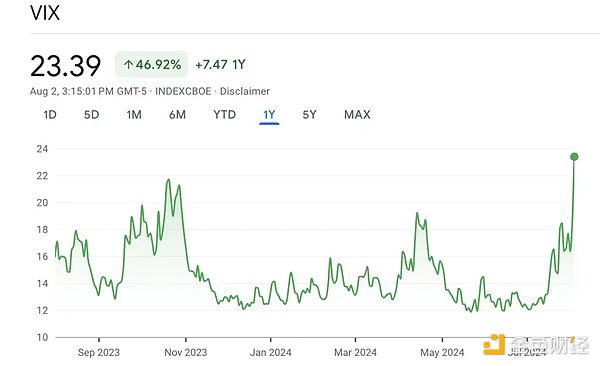

This round of decline in U.S. stocks was led by heavyweight stocks, including Apple, Microsoft, Amazon, Google, Nvidia and other technology giants with a market value of more than one trillion dollars, with declines ranging from 3-5%, and there are obvious signs of large-scale capital flight. The volatility index, which measures the degree of market panic, jumped 23%, the highest level since October 2023.

Market sentiment took a sharp turn for the worse as multiple factors weighed heavily on US stocks

On July 31, U.S. time, the Federal Reserve’s July interest rate meeting resolution was finalized. Although no reduction in the benchmark interest rate was announced, at this meeting, the Federal Reserve almost sent a clear signal to the market that the first interest rate cut would begin in September.

Investors' optimism on the day was obvious. The Nasdaq Composite Index, which is mainly composed of technology growth stocks that are most sensitive to interest rate levels, rose sharply by 2.64% that day. Other sectors also saw general increases to varying degrees.

However, such market performance was later verified to be short-lived. The day after the Fed's interest rate meeting, the US stock market began to plummet. The most direct cause was the July ISM manufacturing data released on August 1, which was only 46.8%, lower than the market's previous expectations. The index reflects the factory activity in the United States and is generally considered to be a signal of economic recession.

Subsequently, the non-farm payrolls data released on Friday continued to increase investors' concerns, with July data showing that the U.S. unemployment rate rose to 4.3%, the highest level since 2021. Combined with the number of first-time unemployment claims announced the day before, which hit the highest level since August 2023, it showed that the U.S. job market began to show signs of a significant slowdown.

The optimism about the Fed’s interest rate cut lasted only one day, and market sentiment took a sharp turn for the worse. The original “optimism caused by the interest rate cut” instantly turned into “recession-related panic selling.”

Some analysts began to criticize the Federal Reserve for being too slow in shifting its monetary policy and missing the best time to avoid a hard landing of the economy.

Some economists believe that the Fed itself has fallen into a very passive situation. On the one hand, the Fed has repeatedly publicly emphasized that it must rely on economic data to make corresponding decisions. On the other hand, due to the significant lag of economic data, if the Fed completely follows economic data to make corresponding monetary policy adjustments, it will inevitably be a step behind. Now the facts are developing in an increasingly unfavorable situation for the Fed.

After the economic data showed obvious weakness and the Federal Reserve made it clear that there is a high probability of starting a rate cut cycle in September, the market has formed a new round of expectations for the Fed's rate cut. Investors expect that the probability of the Fed directly cutting interest rates by 50 basis points instead of 25 basis points in September has increased significantly.

Under such expectations, the Fed's policy making is caught in a dilemma. On the one hand, if the Fed directly cuts interest rates by 50 basis points in September, it will undoubtedly announce to the outside world that the Fed had misjudged the situation before and can only make up for the negative impact of its previous slow action through a one-time and larger interest rate cut. On the other hand, if the Fed still cuts interest rates at the previously planned pace of 25 basis points, it will not be able to curb the trend of rapid economic decline.

In addition, another major factor in the sharp correction of the US stock market came from external influences. The day before the Federal Reserve announced its monetary policy decision, the Bank of Japan announced a 25 basis point interest rate hike, and the yen-dollar exchange rate rose accordingly. The carry trade that had previously borrowed cheap yen to invest in the US stock market died down, which also had a negative impact on the US stock market in the short term.

In addition, the U.S. stock market is in the earnings season, and some technology giants that have already announced their earnings, such as Microsoft and Google, have maintained solid fundamentals, but the revenue and profits of new businesses related to generative AI, which were previously highly expected by investors, have not increased significantly, but capital investment is still growing significantly. This reflects that the leading companies are still in the "arms race" stage, and the real added value generated by generative AI has not yet been fully reflected in the financial performance, which has also caused investors to begin to reposition the valuation of related listed companies.

The interest rate cut is clear, but the extent still needs to be discussed

After last week’s sharp market sell-off, investors are currently focusing on two aspects: one is whether the Federal Reserve is slow to adjust its monetary policy and how to form expectations for the Fed’s next move; the other is whether the generative AI concept can continue to maintain the high valuations of some companies.

For the first question, many economists who closely follow the trend of the time have expressed their opinions. Julia Coronado, founder of the research institute MacroPolicy Perspectives, said that the Fed is definitely slow and they need to catch up.

Mark Zandi, chief economist at rating agency Moody's, was even more blunt, saying the Fed made a mistake and should have made the decision to cut interest rates months ago.

"It feels like a 25 basis point rate cut in September is far from enough. A 50 basis point rate cut and more aggressive monetary policy measures are what the Fed needs to do," Zandi said.

Michael Feroli, chief U.S. economist at JPMorgan Chase, also believes that the Federal Reserve should make a decision to cut interest rates at the Federal Reserve Monetary Policy Committee meeting at the end of July. Under the current circumstances, they have to cut interest rates as soon as possible.

He expects the Fed to make two consecutive 50 basis point rate cuts at its monetary policy meetings in September and November.

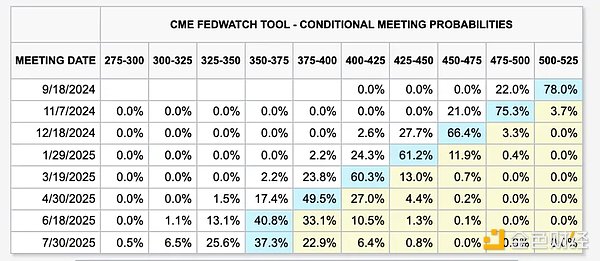

The Chicago Mercantile Exchange's real-time Fed monitoring tool shows that the market currently expects the Fed to announce a 25 basis point rate cut at its September meeting at a 78% chance, and a 50 basis point rate cut at a 22% chance. By the end of this year, when the Fed's last meeting is held, the market expects the probability of a cumulative rate cut of 125 basis points to be 2.6%.

However, some economists have expressed a relatively cautious view. Blerina Uruci, chief U.S. economist at T. Rowe Price, believes that a one-time 50 basis point rate cut currently looks a bit radical, which will clearly declare to the outside world that the Fed was indeed slow to act before, which may cause greater panic in the market.

She believes that the extent of the rate cut will also depend on the data of the August non-farm payrolls report. If the data shows that the July data was simply over-interpreted due to weather factors, then Fed officials will consider a 25 basis point cut in the benchmark interest rate to be more appropriate.