Uniswap, the leading decentralized exchange, released a report yesterday (11th). This report collaborates with stablecoin issuer Circle and Copenhagen Business School to explore what factors drive cryptocurrency price fluctuations. In addition to outlining the research methods and hypotheses, we also use case studies on COVID-19, FTX, and BTC ETF, three events that are of great importance to the cryptocurrency market. This cooperation framework can serve as a model for cooperation between industry and academia. We look forward to seeing more industries combining research strengths with academia to explore these interesting topics.

Table of contents

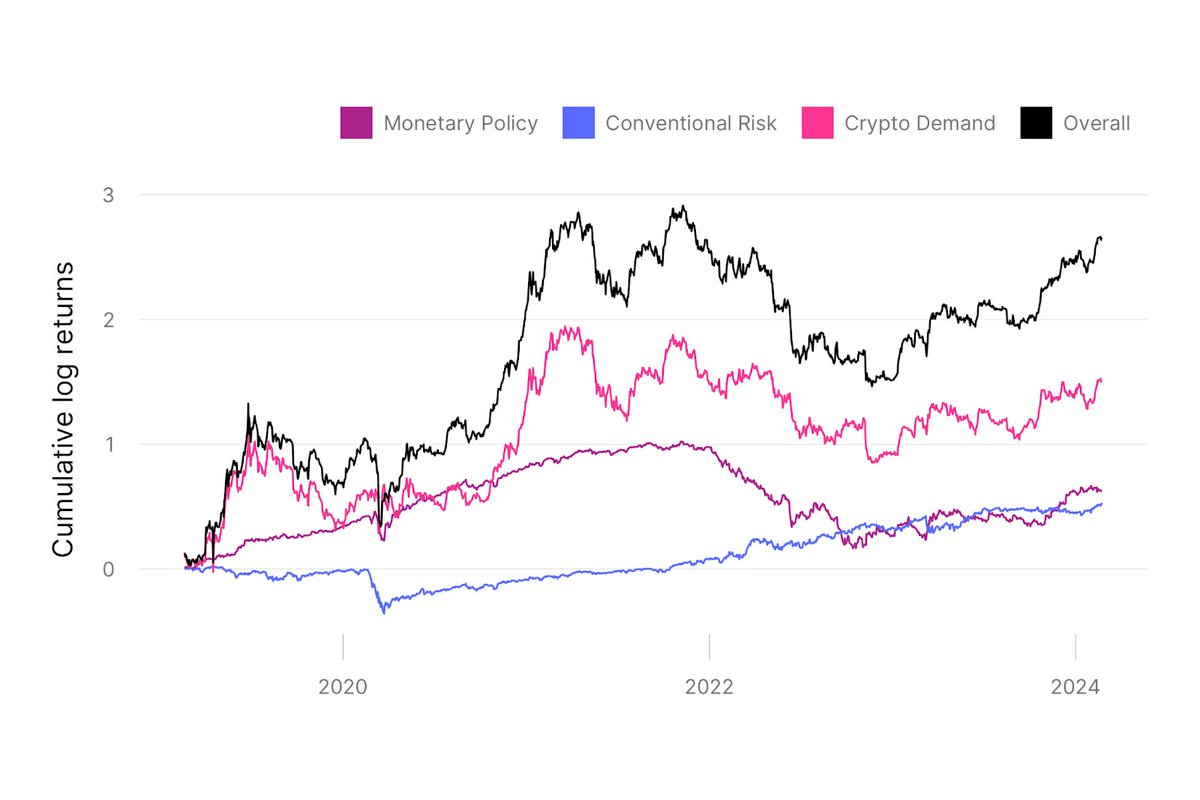

ToggleSafe haven assets? Data shows traditional finance still has a huge impact on Bitcoin price

The report uses a vector autoregression (VAR) model analysis proposed by econometrician Christopher Sims to first decompose Bitcoin returns into three structural shocks: traditional monetary policy shocks, traditional financial risk premium shocks, and crypto-specific demand shocks.

The model shows that traditional shocks can have a significant impact on returns in new asset classes. For example, monetary policy contributed 50 percentage points to Bitcoin’s rise in 2020, but more than -50 percentage points to Bitcoin’s decline in 2022. In other words, if the Fed had not tightened its monetary policy during 2022, Bitcoin returns would have been more than 50 percentage points higher.

The model even suggests that monetary policy will have a greater impact on driving cryptocurrency returns in 2022 than crypto-specific demand shocks. Over the sample period, traditional risk premium shocks (risk-off shocks) generally have a positive impact on cryptoasset returns, suggesting that traditional risk premiums are declining, except during the COVID-19 sell-off in March 2020. Except for a short period of time. Finally, while the low-frequency effects of traditional shocks on crypto prices can be large, most day-to-day fluctuations in Bitcoin prices cannot be explained by traditional shocks.

To explore how much of cryptocurrency price volatility comes from spillovers from traditional financial markets, compared with idiosyncratic risks inherent in the assets themselves. The researchers compared four assets - Bitcoin, stablecoin market capitalization, two-year Treasury zero-coupon bonds and the S&P 500 Index. Representing cryptocurrency, monetary policy and traditional finance respectively.

The report attributes much of the growth in Bitcoin prices from 2020 to mid-2021 to demand for the cryptocurrency. Because during this period, both stablecoin market capitalization and Bitcoin price experienced tremendous growth. The report defines a crypto adoption shock as one that would increase stablecoin market capitalization and Bitcoin price. Conversely, as the growth of stablecoins has slowed since late 2022 and even reversed in some periods, Bitcoin price A negative crypto adoption shock (representing an outflow of crypto market capitalization) is shown.

Data during the epidemic show that the U.S. dollar is the safe-haven asset recognized by the market

Observing data from the early days of the COVID-19 outbreak, in March 2020, the price of Bitcoin dropped significantly (25% in a single month), while the market value of stablecoins increased significantly. Asset prices fell more than could be explained by declining fundamentals, indicating heightened risk aversion.

The huge growth of stablecoins during this risk-off period shows that stablecoins are indeed regarded as safe-haven assets in the crypto asset space. During risk-off periods, we expect traditional risk premium shocks and crypto risk premium shocks to play a dominant role. Although Treasury yields have declined over the medium term, immediate changes in Treasury yields are highly volatile when the Treasury market faces liquidity issues. Therefore, the monetary policy shock may not be the only reason as yields temporarily rose in March 2020. The model attributes the decline in Bitcoin prices in 2020 to a combination of a positive traditional risk premium shock and a positive crypto risk premium shock.

The primary impact on the cryptocurrency market was the main reason for price changes during the FTX incident

The report goes on to mention data before and after the FTX incident, with Bitcoin prices falling significantly from September 2022 to January 2023. Most of the decline occurred during the FTX crash in November 2022. At the same time, the market value of stablecoins declined slightly during this period, with a brief increase occurring when FTX collapsed in November 2022, again in line with the characteristics of stablecoins as safe-haven assets.

Crypto market prices fluctuated wildly before and after the FTX crash, while traditional financial market prices changed little. Therefore, during the FTX collapse, crypto shocks are expected to play a dominant role, specifically positive risk premium shocks and negative adoption shocks. In comparison, the impact of traditional shocks on FTX’s collapse should be smaller. And the model does identify a negative crypto adoption shock and a positive crypto risk premium shock during the FTX crash.

At the time of the FTX collapse (November 2022), rising crypto risk premiums drove the price of Bitcoin downward, while stablecoin inflows could be observed. Meanwhile, a negative crypto adoption shock further depressed Bitcoin prices and negatively impacted stablecoin flows.

Bitcoin ETF listing reflects market interest in institutional entry

The report also concludes by comparing the specific reasons that will affect cryptocurrency prices after the listing of Bitcoin ETFs. When BlackRock announced the submission of a Bitcoin spot ETF application, the price of Bitcoin increased significantly. This period represents a major shift in investor sentiment and market dynamics in the cryptocurrency industry. The model identifies two main influencing factors: a positive crypto adoption shock and a negative crypto risk premium shock. The positive crypto adoption shock may reflect the market’s increased legitimacy and investor interest in the entry of important institutional players like BlackRock into the Bitcoin market.

Crypto-specific factors gain Bitcoin’s primary pricing power

While traditional monetary policy and risk premium shocks have some impact on cryptocurrency prices, their effects are more pronounced at lower frequencies. Crypto-specific factors play a leading role in explaining daily Bitcoin price changes. Additionally, the report found evidence in multiple cases to support the safe-haven properties of stablecoins in the crypto-asset sector, as stablecoin market capitalization tends to increase during market periods.

Event research on COVID-19 market turmoil, the FTX crash, and the launch of the BlackRock Bitcoin Spot ETF further validates previous sentiments. These case studies highlight the importance of crypto-specific factors in driving cryptocurrency prices during major market events.