Author: Terry, Plain Language Blockchain

Who is the liquidity cornerstone and innovation hotbed of the on-chain crypto market?

Most people would probably say DeFi. That’s right, as the cornerstone of the on-chain liquidity market, it not only provides a low-friction transaction and real native income environment for existing funds, but also becomes the main channel for introducing incremental funds such as RWA and underlying high-quality assets. It is an indispensable positive factor for the funding side of the entire crypto market.

However, since 2023, in the face of the successive hype of other concepts, the voice of DeFi as an overall narrative has gradually declined, especially in the context of the market crash, it often leads the decline sharply, so fewer and fewer people mention it, and it has become a forgotten narrative in the rotation of sectors in the crypto world.

However, it is worth noting that now, three years have passed, and the DeFi narrative has begun to show some new changes worthy of attention. Whether it is the new actions of old giants such as Aave and Compound, or the development of emerging DeFi ecosystems such as Solana, there are some quite interesting variables.

01 The DeFi narrative that has never recovered

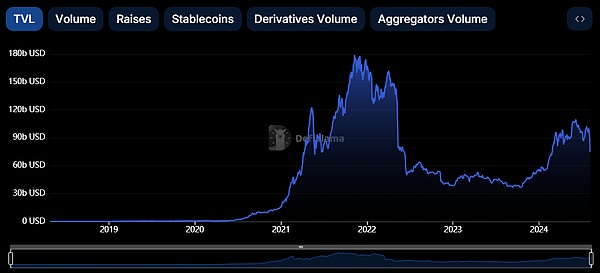

Although the "DeFi Summer" in 2020 has left a deep impression on crypto players, if we look back strictly from a timeline perspective, we will find that the prosperity of the entire DeFi market only lasted about a year and a half, and data such as TVL is the most intuitive.

According to DefiLlama data, in November 2021, the overall DeFi locked volume in the crypto market reached a historical high of approximately US$180 billion, and then fluctuated/declined all the way. In 2022, it experienced the Terra/Luna, Three Arrows Capital, and FTX/Alameda crises one after another. Liquidity was continuously drained, and finally hit a temporary low in October 2023.

As of the time of writing, the total TVL of the entire DeFi track has fallen back to approximately US$85 billion (as of August 13), which is only 47% of the historical high at the end of 2021. This huge gap is not only reflected in the numbers, but also in the ecological development of DeFi projects and user confidence.

For example, many DeFi projects that once attracted much attention have had to scale down their business due to the withdrawal of funds and the lack of market confidence. Some projects have even stopped operating directly:

On September 20, 2023, DeFi yield aggregator Gro Protocol announced the cessation of operations and the dissolution of Gro DAO;

On September 21, 2023, Fuji Finance, a cross-chain DeFi lending aggregator, announced the closure of the protocol and the cessation of operations;

On December 15, 2023, DeFi protocol SafeMoon officially filed for bankruptcy under Chapter 7 of the U.S. Bankruptcy Code;

On January 30, 2024, the fixed-rate lending protocol Yield Protocol reminded users to close their positions in the protocol, and official support will end on January 31;

On July 20, 2024, the decentralized derivatives trading platform Rollup.Finance announced that it would cease operations, and the infrastructure would be completely shut down after September 21, 2024. Users would have one month to close their positions and withdraw funds;

It should be noted that the above are only the relatively well-known DeFi protocols that have been reported in the newspapers. In fact, according to incomplete statistics, the number of projects that have chosen to stop operating in the crypto industry has suddenly accelerated since the second half of 2023, and the entire track has even experienced a "shutdown wave". Many projects seemed to fall into trouble overnight and could no longer maintain normal operations.

The token prices of the DeFi protocols that are still persisting in the secondary market are also very sluggish. What is strange is that even in the same period, the trend of Bitcoin and even Ethereum, which have always been regarded as "Beta" returns, is much better than the overall performance of DeFi Tokens, which were once regarded as "Alpha":

If we take November 2021 (BTC: US$68,999) as an important reference point for analysis, we can clearly see that the current price of Bitcoin is about US$60,000, which is approximately 86% of its high at the time; the price of Ethereum is about US$2,670, which is approximately 55% of its high at the time (ETH: 4,800).

However, the performance of the DeFi field can almost be described as terrible, and it has almost suffered an ankle-breaking blow - according to Binance's DeFi contract index data, the current price is about 630, which is only less than 20% of the high point in November 2021 (3400)!

Although such a comparison may not be rigorous enough, it also indirectly proves a fact that cannot be ignored: against the backdrop of the overall market's continuous recovery and even BTC hitting new highs, the DeFi sector has failed to keep up with the overall pace of the market, nor has it been able to further attract capital inflows. Investors' enthusiasm for the DeFi sector has clearly cooled, and they are no longer as keen to participate in and invest in DeFi projects as in the past.

This also sounded the alarm for the future development of the DeFi field.

02 Self-rescue and expansion of OG DeFi

However, observing from within the DeFi track, there are some quite interesting variables happening recently, especially the actions of leading blue-chip projects such as Aave and Comound.

1) MakerDAO: RWA and stablecoins work together

MKR is, to some extent, one of the most resilient veteran DeFi projects. Maker and MakerDAO have also been seeking continuous evolution. "Maker Endgame" is one of the boldest moves taken by the DeFi protocol, especially in the RWA field.

As of August 2024, according to Makerburn data, MakerDAO's RWA portfolio has total assets of approximately US$2.1 billion.

Source: Makerburn.com

Source: Makerburn.com

The total supply of DAI has returned to the $5 billion mark since November last year. In addition, in May, MakerDAO also proposed plans to launch stablecoins and governance tokens with new token symbols to replace DAI and MKR.

Among them, NewStable (NST) will be an upgraded version of DAI, still focusing on maintaining a stable peg to the US dollar, with RWA as the reserve asset. Dai holders can choose whether to upgrade to NST.

PureDai aims to achieve an idealized DAI - using a highly decentralized oracle and only accepting extremely decentralized and well-verified collateral (such as ETH, STETH). In addition, PureDai will launch a lending platform to maximize the supply of PureDai.

2) Aave: Update security module and repurchase tokens

On July 25, Aave's official team's governance representative ACI initiated a proposal for Aave's new economic model, proposing to launch a "purchase and distribution" plan to purchase AAVE assets in the secondary market from protocol revenue and enrich the ecosystem reserves to reward major users of the ecosystem.

At the same time, the Atokens security module will be activated through a new security module, the GHO borrowing rate discount will be cancelled and the Anti-GHO generation and destruction mechanism will be introduced to enhance the consistency of interests between AAVE pledgers and GHO borrowers. In addition, it is recommended to upgrade the current AAVE security module to a new "pledge module".

To put it bluntly, because Aave’s security module has repeatedly encountered problems in terms of bad debt processing efficiency, such as the 2.7 million CRV bad debts generated in the previous CRV hunting war - it will lead to the temporary issuance of AAVE Tokens for auction to cover the debt deficit.

Therefore, the biggest change in the new security module is that it is upgraded to a "staking module", which blocks the loophole of additional issuance from the supply side; at the same time, because the protocol income will be used to purchase AAVE assets from the secondary market and allocate them to the ecosystem reserve, this has found a long-term demand side for AAVE in the secondary market. This two-pronged approach has enhanced the appreciation potential of AAVE from both the supply and demand dimensions.

3) Compound: A whale takes over the property, and it is hard to tell whether it is a blessing or a curse

On July 29, Compound went through a fierce voting battle and finally passed Proposal No. 289 with a subtle advantage of 682,191 votes to 633,636 votes, deciding to allocate 5% of the Compound protocol's reserve funds (499,000 COMP tokens worth approximately US$24 million) to the "Golden Boys" yield protocol to generate income over the next year.

At first glance, this seems to be a pretty good decision. After all, it is equivalent to giving COMP, which was originally a pure governance token, a new income attribute. However, when we delve deeper into the "Golden Boys", we will find the clues - the leader behind it is Humpy, the whale who once successfully controlled Balancer through similar governance attacks .

I won’t go into details about Humpy’s previous success story, but in essence, this time Humpy once again hoarded a large number of tokens, and then used his voting rights to deposit $24 million from the Compound vault directly into the goldCOMP vault under his control. From a process point of view, this may be a legal operation, but it is undeniable that this behavior has undoubtedly caused harm to decentralized governance.

However, Compound also released a proposal yesterday, proposing the concept of "proposal guardians", which aims to prevent malicious voting through a multi-signature mechanism . The guardians will initially be composed of 4/8 multi-signatures of Compound DAO community members, and can veto proposals that have passed a majority vote and are awaiting execution when the protocol faces governance risks.

In addition, Uniswap and Curve are relatively slow in their actions. Curve recently encountered a large-scale token liquidation crisis of its founder. In addition, the $140 million CRV reservoir, which has always been like a sword of Damocles hanging over its head, was finally detonated in this crisis, causing great shock and anxiety in the market.

03 Summary

In fact, the prosperity of most DeFi projects in 2020 and the difficulties they encountered in 2021 were doomed from the beginning - generous liquidity incentives are unsustainable. For this reason, the new product directions or token empowerment attempts of current DeFi blue chips are a microcosm of self-salvation starting from different channels.

It is worth noting that although the recent market shock has led to large-scale liquidations in the DeFi field - the Ethereum DeFi protocol set a record for liquidations this year on August 5, with a liquidation amount of more than US$350 million, but there was no panic stampede. This also indirectly shows that DeFi’s own resilience is constantly increasing, and the overall trend is one of adjustment and exploration coexisting.

In any case, as the liquidity cornerstone and innovation hotbed of the crypto market, after the bubble is cleared, those valuable DeFi projects that have not died and continue to innovate are expected to stand out, re-attract funds and users' attention, give birth to a new narrative, and usher in their own breakthrough.