Author: Revc, Jinse Finance

Ethereum in the doldrums

The crypto world was once described as a new world for marginalized Internet users. Young people who were "frustrated" in Web2 entered Web3 with the ideal of decentralization. The first stop they were attracted to was Ethereum, because Ethereum is the largest smart contract platform with EVM programmability. As the most advanced Web3 financial infrastructure, it has given birth to social SocialFi, financial DeFi, game GameFi, and creator economy CreatFi. The decentralized versions of Web2's top products are mapped on Ethereum. Decentralized Twitter (Farcaster), decentralized Tiktok (DeTiktok) and decentralized WeChat (DeBox) are emerging one after another.

Ethereum's position as the largest public chain is recognized by most people, not only because of its market value, technology, etc., but also because there is a young and charismatic decentralized fighter, Vitalik, who has been building the Ethereum ecosystem in accordance with the purest decentralized route for nearly a decade. Compared with Ethereum, some public chains are overly inclined towards VC in terms of ecological development mechanisms and token distribution.

Vitalik was also frustrated by the unbalanced changes to World of Warcraft heroes, which gave him the idea of building a decentralized world. The "disappointed people" in Web2 are more likely to be swept up by the Internet market monopolized by large companies and capital. The Chinese Internet landscape has not changed in the past 15 years. The two major camps of Alibaba and Tencent, while ignoring supervision and user interests, dragged the new Internet unicorns into their own trenches and competed for half of the Internet. This caused huge social friction costs and undermined the innovative development of the Internet. Finally, under the governance of the Chinese government, the entire industry returned to the right track, but the basic pattern has been formed, except for ByteDance, the world's largest unicorn in terms of valuation, which has been constantly stirring up the spheres of influence of various companies without boundaries in recent years.

In the blink of an eye, it is Web3. The industry is dragged down and troubled by the VC coins produced in an arms race, and has lost the ideal color of decentralization. In the traditional Web2 world, there are investment management methods to constrain the strategic investment departments of large companies (Note: At a Central Economic Work Conference held in December 2020, "strengthening anti-monopoly and preventing disorderly expansion of capital" was listed as a key task of economic work. Subsequently, strategic investment departments of large companies including ByteDance and BiliBili all made adjustments in scale), and there are IPO capital market management methods for long-term governance . However, in the Web3 world, blockchain financial liberalism has released crypto giants such as BTC and ETH, but it also lacks the ability to self-purify, supervise and govern due to its disorganization. The industry generally drives out good money with bad money, which is reflected in Ponzi schemes with extremely short lifespans, and the phenomenon of VC assembly line production of unverified projects exists in large numbers. We are all secondary market bag holders.

Back to Ethereum itself, Ethereum's failure is a dark moment on the eve of large-scale application of Web 3. Although Ethereum's current performance is not as good as Bitcoin, part of the reason is that it is in a special global financial cycle. Bitcoin and Ethereum represent different asset attributes. In the cycle of macro-financial instability, high inflation, and on the eve of interest rate cuts, Bitcoin, which has safe-haven or inflation-absorbing attributes, performs better. Bitcoin has also strengthened its position as the first encrypted asset through ETFs. U.S. mining listed companies and Wall Street also recognize Bitcoin assets more.

Ethereum is more in line with the development cycle of US technology stocks , that is, it will have better explosive performance in the middle and late stages of interest rate cuts . Although Ethereum's performance was mediocre when US technology stocks hit new highs before, Ethereum is the representative infrastructure of Web3 and an upgraded version of Web2. In recent years, the entire narrative of Ethereum has revolved around infrastructure , and not enough attention has been paid to the application layer . Builder, VC and foundation are the Lego of B-side users , that is, magical expansion , creating concepts to convince VC-style entrepreneurship . Web3 itself represents the evolution of production relations, and a large number of VCs on the market who claim to be research-driven have rolled into the ZK track, that is, they are obsessed with the development direction of productivity that they are not good at. In the end, ZK rolled to the hardware level, and ZK computing mining machines appeared. From the perspective of problem solving, it seems to be no different from Bitcoin mining, so it seems to have come back again.

Let's analyze how the economic attributes of users change with the large-scale development and application of Web3. First of all, using Web3 as the starting point to attract Web2 users' expansion strategy, the user's time cost is plummeting. Now Web3 is full of investors and builders, but there are no users. Users who entered the circle in 2021 are now dead silent on Twitter. As the user's time cost decreases, the sensitivity to decentralization decreases. Now who will bear the cost of the entire Ethereum or Web3 decentralized infrastructure, and who will take over the VC coin projects worth billions of dollars? Yes, over-emphasizing decentralization and designing a project without a business logic basis is a cost for the entire Web3. Making users pay in the form of VC coins has greatly increased the threshold for Web2 users to enter Web3.

A more vivid metaphor is that Web3 users range from Wall Street investors to grocery shopping aunties at the country market. They don't care whether the currency in their hands is decentralized. They care about the stability of the currency value and business convenience. If you want to build a bank and fleece them through inflation, they will switch to another currency.

Rethinking the current state of POS

Whether it is Layer2, LSD track or DA modularization, they all hold the banner of shared security. The shared security model itself is a good model, but fair pricing of the opportunity cost of pledged assets is a big problem, especially since many projects grow on Ethereum's L1. Ethereum is inevitably affected, and VCs favor tracks such as L2 and LSD, which are also the hardest hit areas for VC coins.

The tokens are distributed to TVL holders through the Restake method, which is a win-win for the project party, Ethereum ecosystem, and large holders. The only losers are the market and users. It is incomprehensible that project tokens, i.e. shares, can be obtained through staking. Shouldn't the ownership structure or certificate of a project be oriented towards individuals or organizations that can contribute to the operation and development of the project itself? The simple and crude method of staking caters to the project party's demand for rapid rise in TVL and the large holders' demand for wallet expansion through mining, selling and withdrawal. As a result, a deformed business model has been derived. Staking not only gives tokens, but the project party also gives money directly.

The current POS model also reduces the competitive efficiency of blockchain consensus maintenance. In addition to staking rewards, large households under the POS model also greatly increase the voice of large households and VC institutions in the development of the ecosystem, leading to the emergence of VC coins, such as a certain parallel chain design. The POW network maintenance participation threshold is relatively low. In addition to the head mining machine companies that can obtain phased mining advantages through mining machine iterations, normally, the threshold for small miners to join the Bitcoin network maintenance is lower than POS, and it is more fair.

Poor operation of the POS mechanism may lead to the bubble of assets such as governance tokens

At present, the POS design of most public chains , especially the design of staking rewards interest rates , can easily deviate from marketization , resulting in a mismatch between interest rates and the level of ecological development . The level of ecological development is relative to the open market , so interest rate inflation will raise the threshold for assets and users to enter the public chain ecosystem , and deflation will inhibit the development of the ecosystem . The main function of staking is to maintain blockchain network security, and network security costs are dynamic and difficult to price. It is difficult to find a staking rewards model that meets this design. If the staking market is small and the degree of marketization is not high, this unfair distribution will be more obvious. The mainstream POS public chain staking inflation will flow to the foundation reserve, but the foundation does not seem to always have efficient operation capabilities, which will lead to reduced public chain development efficiency, centralized benefit distribution, out-of-control ecosystem inflation, and ultimately assets such as governance tokens will become bubble-like. Ethereum's POS mechanism is currently leading the industry.

Data Observation

On-chain

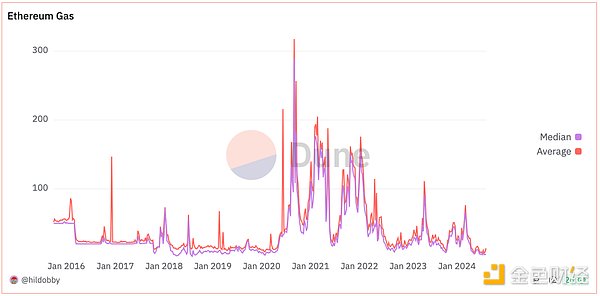

1. The current basic network fee of Ethereum hovers between 1 and 2 gwei, a record low in several years. At the same time, due to the lower Gas fee, the daily destruction of ETH has hit a new low.

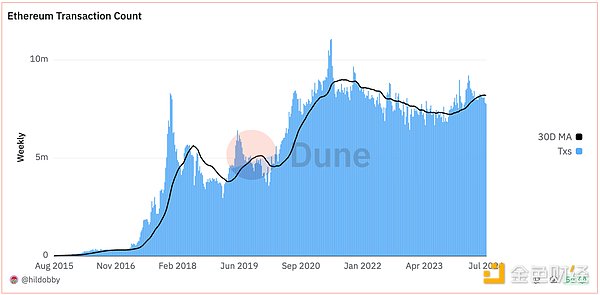

2. On August 6, the number of Ethereum network transactions has dropped to a five-month low, with a seven-day moving average of 1.12 million transactions per day. Currently, more and more activities have shifted to the Layer 2 network, among which Coinbase's Layer 2 network Base has the highest transaction volume, with a seven-day moving average of 3.83 million transactions.

3. The SOL/ETH exchange rate broke through 0.064, setting a new all-time high.

The above data reflects several trends. Ethereum has completed its mission at the current stage, reducing network transaction costs through technical upgrades, and on this basis, allowing decentralized infrastructure to support a wider range of L2, thus laying the foundation for the development of the entire Web3. Solana's challenge is reflected in the rapid development of its application layer and the efficiency gained by sacrificing decentralization. Solana's progress in the application layer is faster, and its products are more in line with the needs of new Web3 users, such as the MEME coin launch platform and tools that link Web2 such as Blink, Solana mobile phone and Depin. Although Solana's innovation is more radical, it is closer to the market than Ethereum, because Web3 is also the Web, and new users pay more attention to UI, interactive experience, efficiency and wealth creation, followed by decentralization. At present, decentralization is what the project tells VCs, and users don't care, and users don't accept the decentralization costs raised by VCs.

Head mechanism operation

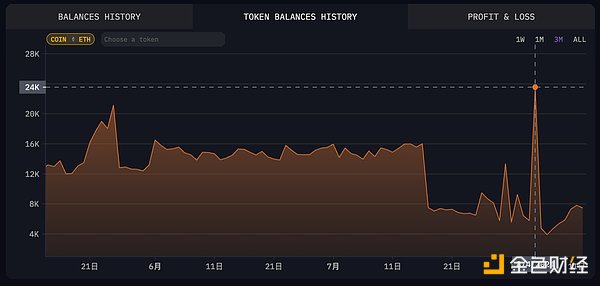

Jump Trading recently transferred about $315 million worth of pledged Ethereum to cryptocurrency exchanges, a move that sparked debate and speculation in the market. The move came before the historic collapse of the Japanese stock market, when the Nikkei 225 index plunged 12.4%. Some analysts pointed out that Jump Trading may have foreseen the market downturn and converted risky assets into stablecoins. The figure below shows the changes in Jump Trading's ETH holdings.

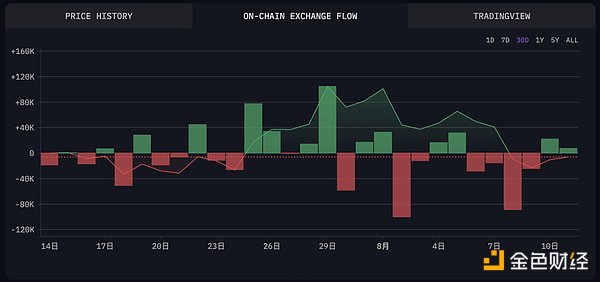

Before and after the crash on August 3, the five leading market makers transferred more than 130,000 ETH directly or indirectly to CEX that week. The figure below shows that Binance's ETH holdings are also at a high level.

Recent actions of Whale

Recently, a whale liquidated 14,387 ETH, with a loss of $12.55 million. In addition, a whale that had been dormant for seven years transferred more than 92,000 ETH, causing the price of ETH to fall below $3,100. Another address participating in the Ethereum ICO transferred 48,500 ETH to OKX in the past month, worth about $154 million.

From the end of July to August 8, there was a small peak in ETH conversion activity on the Ethereum chain. Combined with the actions of the leading institutions, during the market transition phase, whale with high risk preferences are more sensitive to market changes, and their position switching behavior has led to large liquidations on the chain. High leverage is also one of the reasons for the recent sluggish performance of Ethereum.

In addition, James Fickel, who has long held ETH/BTC positions, began to reduce his positions. He reduced his ETH/BTC long position by selling 10,000 ETH in exchange for 425.75 WBTC to repay the loan. From January to July this year, he continued to borrow WBTC from Aave and converted it to ETH to bet on the ETH/BTC exchange rate, with an exchange rate cost of about 0.054. Although he has partially reduced his positions, his ETH/BTC long position is still large, with 2,438.5 WBTC still borrowed, worth about $148 million.

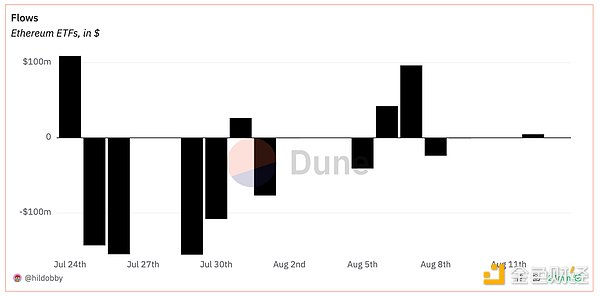

ETF Data

Since the launch of the Ethereum ETF, funds have shown net outflows for many days, most of which came from Grayscale's selling.

Reflections on a Decade of Cryptocurrency

Over the past decade, cryptocurrency has evolved from an emerging technological concept to an important force influencing the global financial market. The decentralized revolution initially led by Bitcoin challenged the authority of the traditional financial system and gave birth to Ethereum and other blockchain platforms, which are not only digital currencies, but also provide a broad stage for smart contracts and decentralized applications. However, this wave of innovation is accompanied by drastic market fluctuations, changing regulatory policies, and challenges in security and sustainability. Looking back over the past decade, the huge potential of cryptocurrency in promoting financial innovation, promoting industry transparency and inclusiveness also requires vigilance against bubble risks.

Venture capital (VC) has played a vital role in the development of the crypto industry. By injecting capital and providing strategic guidance, VC has driven the growth of countless blockchain projects and start-ups, enabling innovative technologies to quickly move from the conceptual stage to market application. VC not only provides the necessary financial support, but also brings valuable industry experience, personal connections and business acumen to the project, helping young crypto companies avoid common entrepreneurial pitfalls. In addition, VC participation has also brought credibility to the crypto industry. Through the promotion of venture capital, the blockchain ecosystem has continued to grow and mature, prompting technological innovation and business models to continue to evolve, and ultimately driving the entire industry towards a more sustainable future.

At present, the theoretical basis and governance mechanism of the entire industry are still imperfect. Here are some thoughts from the industry:

1. How can the crypto industry resist and reduce the negative impact of VC?

Driven by the urge to seize market share, investment institutions of centralized crypto exchage have been unrestrainedly training athletes (project incubation), building tracks (exchange wallet platforms), holding competitions (listing coins) and acting as referees (delisting tokens) in the Web3 field. This has triggered an arms race in the crypto VC industry, increased friction costs in the Web3 innovation field, led to a mixed quality of secondary market projects, and even hijacked the development of public chains.

2. Are there market makers manipulating the market, causing token prices to deviate from fair value, thereby causing losses to investors?

3. How can decentralized and community-first projects get more resources, rather than just entrepreneurs from VCs and foundations?

4. Most application-layer products and services are still at the P2P stage. Is there a problem with the talent system in the Web3 industry? How to attract Web2 operational talent and spread the concept of decentralization?

5. Is the VC qualified to decide which project will run on which track? Can the VC’s vision and values correctly judge which projects represent progress in productivity and production relations?

6. Whether the cash flow generated by the business model can drive the development and operation of the project without relying on financing or other means.

summary

The author is optimistic about the long-term development of Ethereum. Ethereum is the purest decentralized smart contract platform with a strong community consensus and a good foundation governance mechanism, and is not overly controlled by venture capital and large project parties. However, it should be noted that the development of L2 is too dependent on VC.

In the development of Ethereum, the primary goal of technological progress, network design and governance is decentralization, followed by efficiency and commercial viability. This priority setting has led to the recent Solana network data surpassing Ethereum in some aspects, because Ethereum has not paid enough attention to the application layer, especially in the commercial dApp developer atmosphere for C-end users. However, Ethereum will still maintain its core position in the Web3 field, because the endogenous development momentum of the Web3 industry is essentially derived from decentralization.

In the short term, the ETH/BTC exchange rate has fallen rapidly, while Ethereum developers are actively promoting expansion solutions and introducing account abstraction to improve user experience and reduce transaction costs. However, the price of ETH is currently mainly affected by macroeconomic factors.