Author: Ali, former technical director of Gridex; Translation: Jinse Finance xiaozou

1. Introduction

Friend.tech’s points system was launched in August last year, and now points have become the industry standard for off-chain rewards (or tokens, XP, and other similar rewards) to reward early adopters of the protocol. It can be said that this round of airdrop craze started with a series of projects launching tokens in the past year. Like many crypto crazes, the airdrop "gold rush" in people's eyes will eventually be like a bubble, beautiful but ephemeral.

Is the airdrop craze coming to an end? Or is it just a short intermission?

2. Performance of 47 airdropped tokens

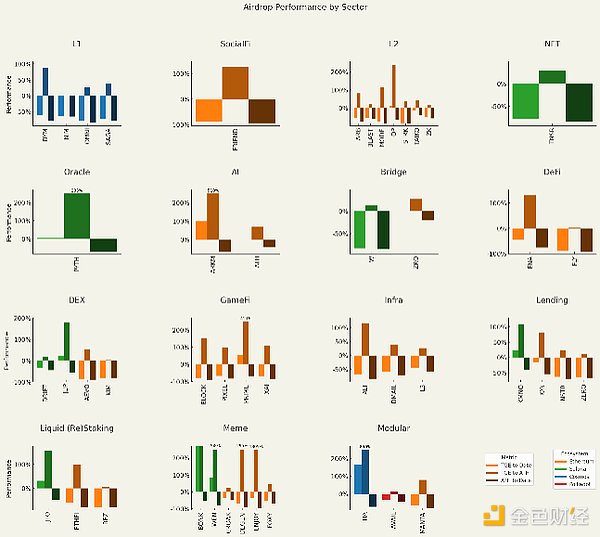

Airdrop tokens are notorious for their “down and up” price action. As of August 25, 2024, of the 47 airdrops I consider to be the most hyped, only 11 of them were priced above the TGE (Token Generation Event), with an average return of 49.56% (excluding BONK). Meanwhile, the 36 airdropped tokens that were priced below the TGE had an average decline of 62.15%. Now, some tokens did see some price gains, with the average gain from TGE to ATH being 162.23% (excluding BONK). However, among these tokens, the average retracement from the ATH was 70.89%. While a correction down from the ATH is also a normal market condition, it is concerning that many of these tokens are showing such large declines in a matter of months.

The trend is clear, with the exception of certain sectors that have been popular so far in this cycle (meme and AI), airdrop tokens have basically been in free fall since 2023 (of course there are some airdrops in between).

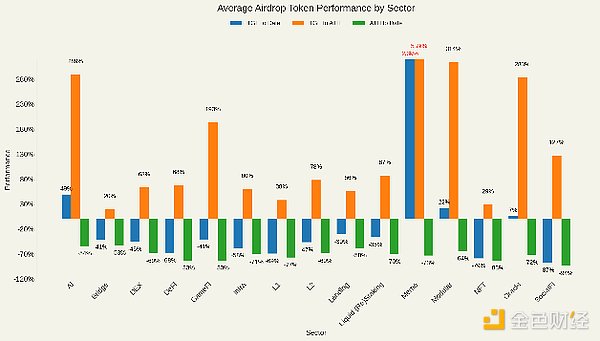

On average, only AI, meme, and modular airdrops actually rose after the TGE, while the others all fell sharply. Meme is by far the strongest performing sector, with an average gain of 2,300% since 2016, with BONK having the largest gain. In fact, in my opinion, it was BONK that saved Solana (Soylana two years ago) from the abyss of despair after FTX.

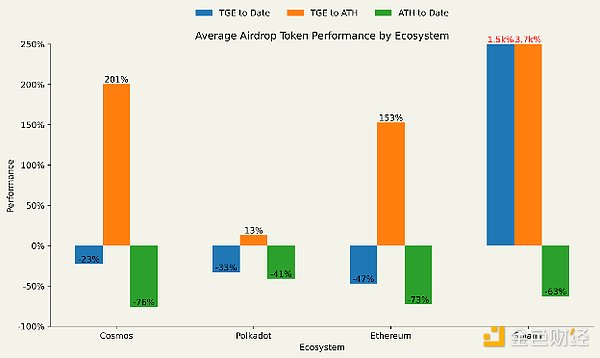

When breaking down the average return of airdrops by ecosystem, only Solana’s airdropped token has been priced above TGE levels so far, again with BONK as the main force. Ethereum-based airdrops were the worst performers, while Cosmos-based airdrops had the most intense price action. With an average ATH of 201% over TGE, coupled with TIA’s 850% gain, Cosmos-based airdrops were all the rage in Q4 2023. The Cosmos airdrop kicked off a short-lived phenomenon of staking airdrops to earn more airdrops, which quickly died down, and with the exception of DYM (down 61.1% from TGE), there have been no notable airdrops since TIA.

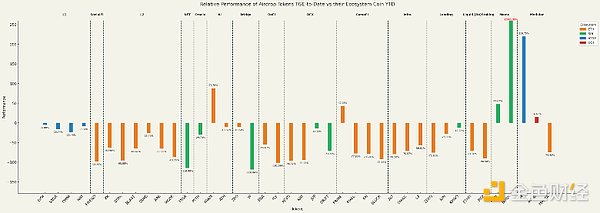

One could argue that the performance to date and the drop after the ATH is because of the general performance of the Altcoin market rather than the airdrop, however, when comparing the performance of the airdropped tokens since the TGE to the year-to-date performance of their underlying eco-coins, only 6 out of 47 tokens (half of which are in the meme or AI sector) have outperformed their eco-coins.

Relative performance of TGE airdrop tokens to date relative to their ecosystem tokens. Truncated outliers are highlighted in red. Source: CoinMarketCap and Coingecko as of August 25, 2024.

Crypto Twitter attributes this epidemic of symptoms to low-flow, high-FDV token economics — complaining that these tokens are merely VC dump vehicles and are therefore almost designed to go down, not up. While there is some weight to this argument, especially given that the utility of most tokens depends on governance rights, the value of which is murky, there seems to be a deeper, more concerning issue. Projects that rely on usage, whether measured by TVL, transaction volume, or other metrics, paint a troubling post-TGE picture.

3. L2

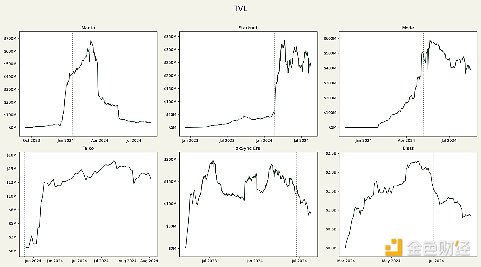

The TVL growth of the much-hyped emerging L2s has been less than impressive, and some have even shown a pure downward trajectory. Blast and zkSync Era are two of the most obvious examples - both of which were heavily airdropped by the studio and seem to have lost their popularity after the TGE. Manta Pacific initially continued to show strength after the TGE, but this can be attributed to their "New Paradigm" event, which only supported Manta Pacific's outbound bridge until March 26, 2024, after which the chain's TVL fell sharply and is currently down 94% from its ATH. A similar story may be happening with Mode, which has reserved 50% of the token allocation for the first 2,000 wallets for 3 months, unlocking on the condition that they will not outbound bridge during this period. Beyond this, Mode's relative strength may be attributed to its second season points program, which Manta does not have (although they did hold a "Restaking Paradigm" event), as well as Mode's inclusion in Optimism's Superfest event. Taiko chose to conduct a TGE at its mainnet launch, which had a positive impact on TVL, but at only $14 million — 0.73% of its token’s TVL — it’s clear that there is little attention in this space.

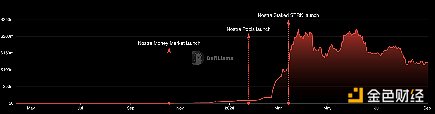

Starknet’s TVL did not follow this trend, but rather surged significantly after the TGE. While this performance is undoubtedly surprising, it is also suspiciously out of touch with market sentiment.

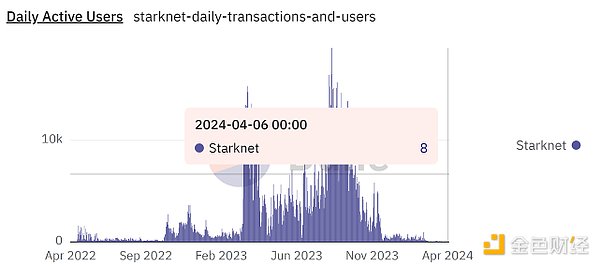

Can the last 8 users on Starknet really bring it back to full health? Before the Starknet worshippers crucify me, let me say that Dune's data is inaccurate; the DAU on June 4th was actually 212,000, which is down 94% from the ATH two months ago. The first thing to note is that Starknet successfully raised $282.5 million at an $8 billion valuation, which means that the TVL is still 18% less than the funds raised. In comparison, Blast only raised $20 million and its TVL is 190% higher than the amount raised, which is not surprising. It is also important to note that Nostra and Ekubo (both of which had disappointing airdrop performance) account for 85% of Starknet's TVL.

While it’s unclear what exactly drives Starknet TVL, one view is bullish on Nostra, with NSTR currently having a fully diluted market cap of $6.3 million and a FDV/TVL ratio of 5%.

4. Bridge

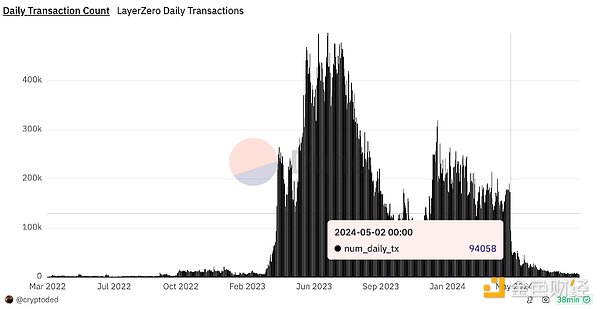

If we look at LayerZero’s daily transaction volume, everything will become clearer.

After the first snapshot of the ZRO airdrop was announced on January 5, 2024, daily transactions plummeted 52% to around 45k and are currently 92% below January 5, 2024 levels at less than 7k. To date, farmers, sybils - whatever you want to call them - have been the driving force of crypto adoption, or at least it seems so. While LayerZero is "old school" in that it does not have a points program, it always sends tokens and users act accordingly to drive as many transactions as possible to maximize their airdrops. These transaction volumes should be the exaggerated metrics thrown to VCs when LayerZero raises $120 million in Series B funding in April 2023.

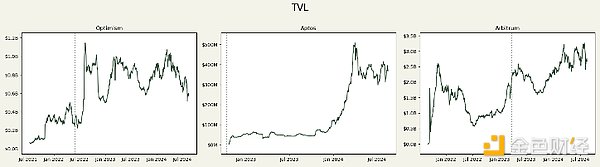

Comparing this performance to the airdrops prior to August 2023 (arguably from the previous cycle) paints a very different picture (of course, we’re talking about the performance of the projects here, not their tokens). With the exception of Aptos, which had to launch a TGE at mainnet launch (because APT is a gas payment token), Optimism and Arbitrum launched governance tokens more than a year after their mainnet launches, after they had already established a good foundation. This is in stark contrast to the more speculative market environment shown in this cycle, where projects fast-tracked their mainnet and TGEs in the hope of profiting. The L2 space is still in its infancy at this point — a far cry from the L2 feel of this cycle.

5. Where will the airdrop go?

Looking at the largest airdrops of all time (ranked by ATH value), at least 7 of them came as an unexpected surprise to those who received them, and this positive sentiment likely led to the token’s price rebound shortly after the TGE.

Last cycle, most airdrops were popular because they were seen as free money. Yes, at the end of the cycle, airdrop farming for profit became more popular, but it was nowhere near the mindshare of this cycle. While Friendtech’s points system was exciting at first, after a few months, every project was waiting for the bear market to end so they could release a TGE to create their own points program, making innovation a cliché.

Farming points season after season requires more and more time and money, which reduces the luster of airdrops. Now, airdrops are no longer "free money", people have to pay for them. Considering factors such as time, liquidity and fees, people are becoming more and more aware of the return on airdrops. Recently, almost all airdrops have fallen into the death spiral after TGE.

It’s time for the points craze to fade. If the project regresses to indiscriminately squeezing farmers’ value through points and leaderboards, and the overall market turns bullish, farmers may suffer again.

6. Are there any other airdrops worth paying attention to? Are they worth taking advantage of?

There are always no less than dozens of projects on the TGE track, and we will only discuss a few here.

( 1 ) Linea and Scroll

Linea and Scroll are the last two large L2s without tokens (assuming Base does not issue a token), with Scroll raising $80 million at a $1.8 billion valuation, while Linea’s parent company Consensys has raised a total of $725 million at a $7 billion valuation. While Consensys has many other projects, such as MetaMask, it is certain that Linea has strong financial support. Compared to zkSync and Starknet, which raised $458 million and $282.5 million at a valuation of $8 billion, respectively, Linea is at least a potential stock, depending on the overall market enthusiasm. STRK briefly peaked at $50 billion in FDV minutes after launch - more than 6 times its valuation - ZK was launched with an FDV of about $4.7 billion, which are very reliable airdrops for zkSync farmers and developers (who happened to submit a project at the Starknet hackathon). Even though zkSync's FDV release before March 2024 will be considered FUD, most dedicated farmers have still harvested at least a few thousand dollars worth of ZK. For this reason, I think farmers who yield farming Linea pre-surge and Scroll pre-marks can expect an early Christmas gift in Q4. If you are a latecomer, it will take a lot of financial support to catch up with everyone else, but if you are farming multiple protocols at the same time (for example, providing WRSETH/ETH liquidity on Ambient to yield farming Kelp, Scroll, and Ambient), such an investment may be worth it.

Linea :

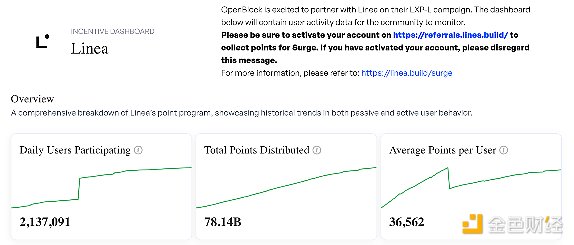

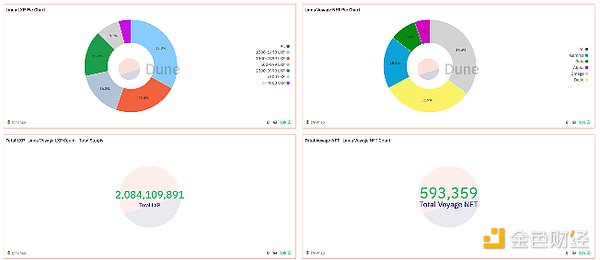

According to data from WhalesMarket, LXP and LXP-L are currently valued at $0.11 and $0.003 respectively, meaning the general airdrop associated with LXP-L is only $109, while the total airdrop for LXP-L is over $234 million.

According to a Dune data, most users have between 1,000 and 1,499 LXP, which means only $137 in pre-market value for most users - very little for a few months of friction and clicks. There is also the Linea Voyage testnet NFT, which

The Delta version is currently priced at 0.00187 ETH (about $5) on Element.

If the pre-listing is to be believed, the average Linea farmer can only expect to receive $251, which is probably around $150 after gas fees. I personally think that the pre-listing is overly bearish due to the trauma of the L2 airdrop, and if overall market sentiment turns bullish and CT's attitude towards airdrops returns to the direction it was before March, then LXP should be worth at least $0.50. Despite this, I still think most people will be disappointed with Linea because as the project focuses more and more on TVL, it is no longer as profitable to drive transactions as before.

Doing the same calculation for the user who has earned the most available LXP, and has earned over $20,000 from the initial Surge Points Program, we know that:

● Alpha NFT = 0.05991 ETH (about $151)

● Top 4.3% of LXP holders = 4,000 LXP (approximately $440)

● Top 1,500 LXP-L holders = 3.5 million LXP-L (approximately $10,500)

● A total of $11,091

I expect the Q4 testnet NFTs and LXP to be more valuable at the TGE, and I also expect some traceable LXP to be distributed in general activities before the TGE. Regardless, this is already a very good airdrop for Surge, with an APY of 25% for providing liquidity.

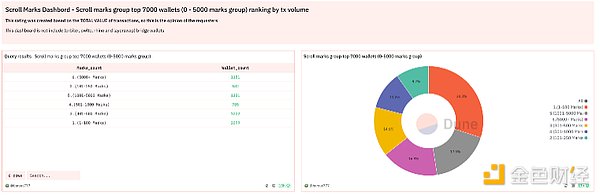

Scroll :

The data for Scroll is more straightforward. In the WhalesMarket market (where the volume is very low), Scroll marks are currently worth about $0.27, and most wallets holding 0-100 marks are worth $27, but this is only the first phase, so we can expect this number to rise. The number of wallets holding more than 5000 marks is quite significant, accounting for 16.9%, with a profit of more than $1350.

Additionally, Scroll Canvas requires users to collect more NFT badges through traditional trading methods. While the project no longer provides large token allocations for trading-based activities, I find it hard to believe that badges have nothing to do with airdrop allocations. Considering that badges are separate from the points program, they may act as a multiplier for points.

Overall, unless you are yield farming before the marks are released, I think there are better places to keep your funds. That being said, if Crypto Twitter's attitude towards airdrops returns to the pre-March attitude, then airdrop mining may be worth it.

( 2 ) LRT (Liquidity Re-staking Token)

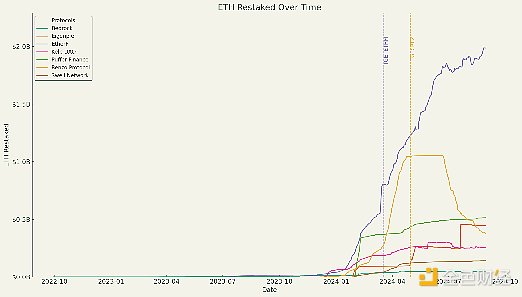

Of the top 7 ETH liquidity re-staking protocols, only 2 have airdropped so far: EtherFi and Renzo. While their tokens have performed mediocrely, down 60.4% and 79.7% from the TGE respectively, EtherFi has shown considerable strength and solidified itself as the must-have LRT. Meanwhile, Renzo's TVL stagnated after the TGE, only to begin its dramatic decline a few months later. This is likely due to the fact that withdrawals were not available until June, meaning many farmers were left holding onto their ezETH wallets as it decoupled on the open market. So, it's no surprise that there were no new ETH inflows after the TGE after their "chart crime" on Twitter.

Other major LRTs haven’t shown strong growth momentum since the airdrop craze died down, so I doubt there’s room for gains, even though I’m farming Linea and Scroll along with Kelp.

We are still waiting for the EIGEN TGE, but with a pre-launch price of $3.62, most farmers won’t invest more than $400, even if they can get an extra 100 EIGEN. We can see Karak and Symbiotic get ahead of EIGEN on the TGE, but these yield farming are capital intensive.

( 3 ) Berachain and Monad

Finally, we have two of the most mysterious and hyped projects we have ever seen: Berachain and Monad. While there has been a lot of attention on both over the past 6 months, it is unclear how the airdrops will be conducted, and there is no clear mainnet launch date. Considering that they raised $142 million at valuations of $420.69 million and $244 million respectively, this is undoubtedly a good thing for those who received token allocations.

We start with the less mysterious of the two, Berachain, where collecting countless (expensive) Bera NFTs and gaining exclusive Discord characters is probably the most rewarding. If you don’t like trading NFTs, then your best bet is to regularly interact with all the major dapps on the testnet (BEX, BEND, BERPS, etc.). A great way to do this is to collect badges through TheHoneyJar’s missions, although they are not directly associated with Berachain. That said, testnet interaction may not mean anything (never forget Sui).

Monad is essentially a cult, at least for now, and the only way to yield farming is to gain reputation on their socials, as there is no testnet.

7. Conclusion

Yes, the airdrop craze is dead, but it will be revived one day.