Source: Zhibao Investment Research

summary

At this meeting, the Fed cut interest rates by 25bp to 4.25%-4.5%, in line with expectations. The overnight reverse repo facility was technically adjusted to the lower end of the range of the federal funds rate .

The wording of the meeting statement was adjusted, reflecting that the FOMC considered that the "rhythm" and "magnitude" of the implementation of subsequent policies had changed. There were also differences in the votes, with some members opposing the December rate cut.

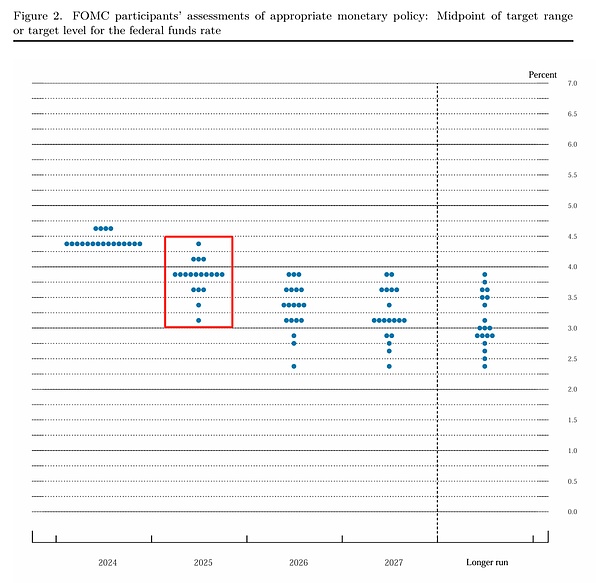

The economic forecast clearly reflects concerns about inflation risks , and the Fed's risk balance has clearly shifted back to inflation . The dot plot only suggests two rate cuts next year, showing an absolute hawkish tendency .

In his opening remarks at the press conference, Powell mentioned the "more neutral setting" and was "cautious" about further interest rate cuts, expressing a hawkish stance.

The USD/VIX surged, while U.S. bonds, U.S. stocks, gold, and Bitcoin fell sharply.

Statement (bold indicates changes)

Recent indicators suggest that economic activity has continued to expand at a solid pace. Since earlier in the year, labor market conditions have generally eased, and the unemployment rate has moved up but remains low. Inflation has made progress toward the Committee's 2 percent objective but remains somewhat elevated.

Recent indicators suggest that economic activity continues to expand at a solid pace. Labor market conditions have generally eased since the beginning of the year, with the unemployment rate rising somewhat but remaining low. Inflation has moved toward the Committee's 2 percent objective but remains slightly elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are roughly in balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

The Committee seeks to achieve maximum employment and 2 percent inflation over the longer term. The Committee judges that the risks to achieving its employment and inflation goals are roughly balanced. The economic outlook is uncertain, and the Committee is mindful of two-way risks to its dual mandate.

In support of its goals, the Committee decided to lower the target range for the federal funds rate by 1/4 percentage point to 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

To support its goals, the Committee decided to lower the target range for the federal funds rate by 25 basis points to 4.25% to 4.5%. In considering the magnitude and timing of further adjustments to the target range for the federal funds rate , the Committee will carefully assess incoming data, the changing outlook, and the balance of risks. The Committee will continue to reduce its holdings of Treasury securities, agency debt, and agency mortgage-backed securities. The Committee is firmly committed to supporting maximum employment and returning inflation to its 2% objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the achievement of the Committee's goals. The Committee's assessments will take into account a wide range of information, including its readings of labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Philip N. Jefferson; Adriana D. Kugler; 4-3/4 percent.

Voting in favor of the monetary policy action were: Chairman Jerome Powell, Vice Chairman John Williams, Thomas Barkin, Michael Barr, Raphael Bostic, Michelle Bowman, Lisa Cook, Mary Daly, Philip Jefferson, Adrienne Kugler and Christopher Waller. Beth M. Hammack voted against, preferring to maintain the federal funds rate target range at 4.5% to 4.75%.

Economic Forecasts and Dot Plots

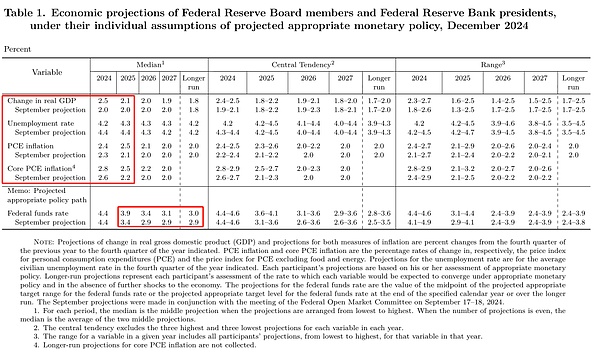

The economic forecast for 24/25 years was raised, the unemployment rate forecast was lowered, and the inflation forecast was raised, with the inflation forecast for 25 years being raised significantly.

The dot plot only indicates two interest rate cuts throughout next year , showing a strong hawkish tendency.

Question and Answer Session

Mi Kou was unable to attend the entire press conference due to illness, and the specific questions and answers are still to be sorted out after the official document is released.