Source: Barron's Chinese

"The long-taut rubber band has finally snapped," as the stock market continues to clear excess liquidity, investors should be prepared for more declines.

The Federal Reserve's calm forecast for interest rates and inflation in 2025, made on Wednesday (December 18), shocked the market, and the market correction may have already begun, but it's not time to panic yet.

Fed Chair Powell conveyed an unwelcome message: the process of disinflation is slower than expected, and it is expected that there will only be two rate cuts of 25 basis points each in 2025. Compared to the previous larger rate cut forecasts and more progress in lowering inflation, the signals released by Powell on Wednesday disappointed investors.

After a 25 basis point rate cut on Wednesday, the federal funds rate target range fell to 4.25%-4.5%, but there was significant dissent within the Fed on the rate cut, with four officials opposing the cut.

Affected by the Fed's "hawkish" tone and Powell's speech, the S&P 500 index, Dow Jones Industrial Average, and Nasdaq Composite all fell across the board. The 3% drop in the S&P 500 index on Wednesday was the largest single-day decline for the index on the day of a Fed rate decision in nearly 15 years. The Dow fell 2.6%, marking its 10th consecutive trading day of declines. The Nasdaq fell 3.6%, its worst performance on the day of a Fed rate decision since March 2020.

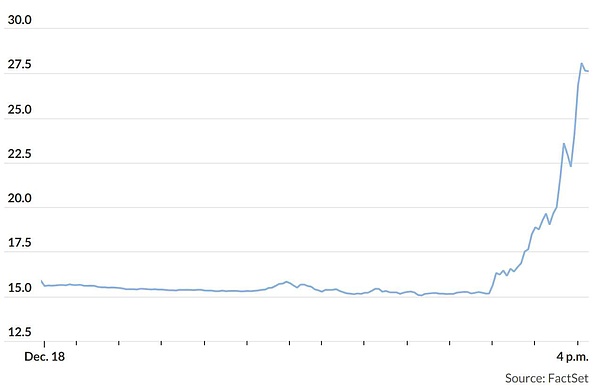

Small-cap stocks, which are more sensitive to interest rates, were hit harder, with the Russell 2000 index falling 4.4%. At the same time, market volatility surged significantly, with the VIX fear index soaring 74% to 27.62, the largest single-day percentage increase since February 2018 according to Dow Jones Market Data.

VIX fear index soars

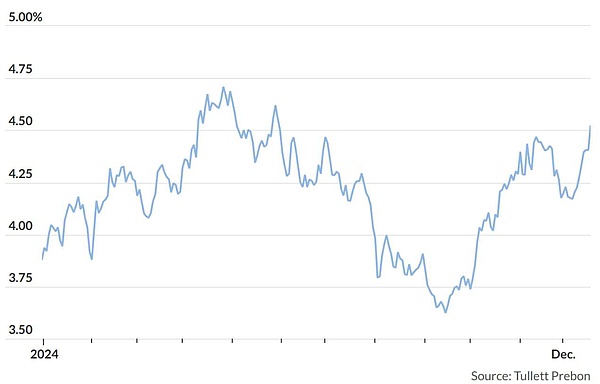

Bonds were not spared either, with the 10-year U.S. Treasury yield soaring to 4.5%. In the past eight trading days, the 10-year U.S. Treasury yield has risen on six trading days, and has risen 0.87 percentage points from the 52-week low of 3.62% reached in September.

10-year U.S. Treasury yield rises to the highest level since May 31

The message conveyed by Powell is not as alarming as it may seem, but since the market is already on the edge of a cliff, it doesn't take much to push it over. BTIG technical analyst Jonathan Krinsky wrote in a research report on Wednesday that "today, the long-taut rubber band has finally snapped."

Krinsky noted that the technical indicators of the stock market have become "exhausted": the number of declining stocks has exceeded the number of rising stocks for 13 consecutive trading days, and only 8% of the S&P 500 component stocks are trading above their 20-day moving averages. In addition, LPL Financial's chief technical strategist Adam Turnquist pointed out that only 53% of stocks are trading above their 200-day moving averages, at their lowest level of the year.

Krinsky pointed out that high-momentum stocks had already been approaching a collapse, and this finally happened on Wednesday: high-momentum stocks fell nearly 6%, experiencing their worst performance since May 2022.

As the stock market continues to clear excess liquidity, investors should be prepared for further declines. Strategist Ed Yardeni wrote in a research report that "the turmoil in financial markets today after the Fed's 'hawkish' rate cut may be the start of the correction we've been expecting all along."

At the same time, investors are not just selling indiscriminately. Tesla (TSLA), which fell 8.3%, was not spared, but Nvidia (NVDA) fell relatively less, by 1.1%, reflecting that the company's stock price has already fallen significantly in recent trading days.

In addition, UnitedHealth (UNH) was the only Dow component stock to rise, up 2.9%, and other health insurance companies such as Cigna (CI), Centene (CNC), and CVS Health (CVS) also rose. The healthcare sector has been declining since the murder of a UnitedHealth executive, and investors seem to believe that the bad news has already been priced in.

Investors still have ample reasons to expect the market to digest and cope with the Fed's more pessimistic outlook. First, Powell reiterated that the U.S. economy remains healthy. Second, the inflation rate is fluctuating in the 2%-3% range, making it difficult to decline further, but not as bad as the sharp rise in inflation that was the root cause of the stock market sell-off in 2022. Finally, there are no signs yet that corporate profits will start to decline.

It is also worth noting that the stock market is still far from a correction (at least a 10% decline). The S&P 500 index closed at 5,872 on Wednesday, down only 3.6% from the record high of 6,090 reached on December 6.

When technical indicators deteriorate like they have recently, it may take some time for them to recover. Krinsky said he could not rule out the possibility of further declines in the stock market, and expects a "more severe and longer-lasting decline" in the stock market in early 2025.

However, there are still many supporting factors for corporate earnings, and at the same time, Trump's proposed deregulation and tax cut plans are expected to provide some stimulus for U.S. economic growth, and help corporate earnings continue to grow (provided that tariffs do not cause the U.S. economy to deviate from its growth trajectory and inflation to spike again).

The always bullish Yardeni has not changed his stance, writing in a research report that "concerns such as government shutdowns, port worker strikes, and tariffs imposed on the first day of the new Trump administration may cause the market correction to continue into January 2025, but we maintain our year-end 2025 target price of 7,000 for the S&P 500 index."