Author: Chen Yulu

On February 22, 2025, the China Digital Economy Development and Governance Academic Annual Conference was held at Nankai University. The theme of this conference was "Artificial Intelligence, Digital Economy, and New Productive Forces", actively responding to the strategic call in the report of the 20th National Congress of the Communist Party of China to "accelerate the construction of a network power and a digital China". The conference brought together the wisdom of the academic and industrial communities to jointly explore the future development direction of the digital economy. More than 40 experts, scholars, and institutional representatives were invited to the conference to conduct in-depth discussions on core issues such as the digital economy, digital finance, digital trade, data elements, and AI innovation development.

Nankai University President Chen Yulu delivered a keynote speech on "The Rise and Challenges of Cryptocurrencies".

Chen Yulu Delivers Keynote Speech

The theme I want to share today is "The Rise and Challenges of Cryptocurrencies". Cryptocurrencies are a type of digital currency that operates through computer networks, and the ownership of each cryptocurrency unit is recorded and stored in a digital ledger or Blockchain. Blockchain is the underlying technology of cryptocurrencies, and its core is the Proof-of-Work (PoW) consensus mechanism.

Cryptocurrencies can be mainly divided into three categories: payment-type cryptocurrencies such as BTC and ETH; stablecoins, the most famous of which are the US dollar stablecoins USDT and USDC; and central bank digital currencies, also known as sovereign digital currencies, with large-scale representatives such as China's Digital RMB.

Cryptocurrencies have seven main characteristics: decentralization, security, scarcity, anonymity, high price volatility, large energy consumption in the mining process, and global instant transactions without considering currency exchange costs and international transfer time costs.

Since Satoshi Nakamoto (the team) mined the first BTC Block (Genesis Block) in January 2009, cryptocurrencies have gradually gained a foothold in the financial ecosystem, from a niche virtual currency experiment to a mainstream discussion. Currently, more than 130 countries and regions have begun to incorporate different forms of cryptocurrencies into the mainstream financial system.

Against the backdrop of escalating global geopolitical turmoil, persistently high US fiscal deficits, and rapidly rising US debt, cryptocurrencies represented by BTC are receiving widespread attention. The latest developments show that the US government is accelerating the construction of a "digital US dollar hegemony system" from three aspects: national strategic reserves, cryptocurrency legislation, and cryptocurrency financial infrastructure, and attempting to extend its global hegemony in traditional finance to the digital economy era. Based on this background, I will focus on elaborating on the global situation and risk challenges of cryptocurrency development.

The Cryptocurrency Market is Experiencing Breakthrough Progress

In January 2024, the BTC spot platform exchange-traded fund (ETF) was officially launched, marking a landmark event in the integration of crypto assets and traditional financial assets.

In December of the same year, the BTC price broke through $100,000 per coin, driving the total cryptocurrency market capitalization to surge from $800 billion to $3.4 trillion in just two years. Meanwhile, the total market capitalization of crypto assets has rapidly risen from less than 1% of the liquidity of the world's six major central banks (G6) in 2009 to 12% at the end of 2024. In the mainstream market, the investment attributes of BTC are shifting from a niche risk asset to a mainstream asset class. The strategic BTC reserve plan (SBR) proposed by the new Trump administration has further stimulated and strengthened this transition process.

Since the second half of 2023, the US government's regulatory stance on the cryptocurrency field has undergone a significant shift, and its strategic intention is likely to be an attempt to extend the US traditional financial hegemony to the digital finance field.

Against the backdrop of the US government's high debt and persistent inflation, this strategy can both ensure the centralized position of the US dollar in the digital finance revolution and indirectly support and alleviate its increasingly severe federal debt situation. This strategy may contain short-, medium-, and long-term goals: in the short term, the US government is trying to build the initial framework of global digital currency hegemony through three means: cryptocurrency strategic reserves, encouraging the expansion of US dollar stablecoins, and controlling the core infrastructure of crypto asset transactions; in the medium term, through a relaxed regulatory environment, tax incentives, and long-arm financial sanctions, it will continue to attract (or coerce) the world's top crypto companies to migrate to the US or be incorporated into the US government's regulatory system, promoting industry clustering, employment, and economic growth, and maintaining the US's leading position in blockchain technology R&D; in the long term, the US will ensure the centralized power in the decentralization wave of the digital economy by dominating the formulation of global digital finance infrastructure and rules, and ensuring the US dollar maintains a centralized position in global investment and transactions in the digital economy era.

The US Shift and Its Strategic Intentions

1. Since the second half of 2023, the US government and the industry have seen five landmark changes in the cryptocurrency field

First, the stance of the US financial regulatory authorities has shifted from "severe crackdown" to "guiding regulation". Paul Atkins, the new chairman of the Trump administration, is a long-term supporter of cryptocurrencies, and after taking office, he actively promoted the compliance path of crypto assets, coupled with his close relationship with the new Treasury Secretary Scott Bessent, reflecting the new US government's positive support for crypto assets and the trend of finding a new balance point between financial innovation and financial investment protection. In December 2024, the SEC approved the listing and trading of Franklin Templeton's crypto index ETF (EZPZ) on the Nasdaq, which is an important milestone in the comprehensive shift of the US financial regulatory stance.

Second, from legislative suppression to legislative support. The US Congress is actively promoting the "dual pillar" of crypto regulation legislation - the "21st Century Financial Innovation and Technology Act" (FIT21) and the "Guiding and Establishing the US Stablecoin National Innovation Act" (GENIUS). The FIT21 Act will comprehensively lay the foundation for the crypto regulatory framework, resolve many classification and jurisdiction issues, and clarify the regulatory boundaries between the SEC and the CFTC, formulate standards for identifying the attributes of digital assets as commodities and securities, and establish a legal framework for institutional digital asset custody services. GENIUS is dedicated to establishing a comprehensive regulatory framework for stablecoins and will bring the two largest stablecoins, USDT and USDC, which account for 90% of the global stablecoin market, under regulation. FIT21 was passed in the House of Representatives with bipartisan support in May 2024 and is expected to be passed by the Senate and signed into law by 2025. GENIUS is planned to be voted on in the Senate this March. After the passage of these two bills, the US will form the most comprehensive crypto regulatory system in the world, which will significantly influence the direction of crypto industry innovation and market patterns.

Third, the attitude has shifted from severe crackdown to strategic asset-ization. The Trump administration plans to launch a 1 million BTC strategic reserve and incorporate it into the Treasury Department's Exchange Stabilization Fund.

In January this year, Trump signed the Executive Order on "Strengthening US Leadership in Digital Financial Technology", the main content of which includes preparing to establish a BTC strategic reserve (SBR) and prohibiting the establishment, issuance, and promotion of any form of central bank digital currency within or outside the US, thereby undermining any potential competitors to the US dollar stablecoin.

Here is the English translation of the text, with the specified terms preserved:Fourth, the industry has shifted from hesitant observation to a more positive response. A large number of star companies such as Apple, Tesla, and Microstrategy have already or plan to include crypto assets in their corporate asset allocation. Traditional large financial institutions (such as BlackRock, the world's largest asset management financial group) are also accelerating their holdings of Bitcoin. The global Bitcoin ETF fund assets have exceeded 1.1 million BTC. Among them, the BlackRock Bitcoin ETF (IBIT) accounts for 45% (with a market value of about $153 billion as of February 2025). Spot Bitcoin ETFs attracted over $108 billion in funds in 2024, and the crypto market and traditional financial market are accelerating their integration.

Fifth, adjustments to tax policies. In the 2025 temporary tax relief, the US Internal Revenue Service allowed taxpayers to flexibly choose the accounting method for crypto assets, which temporarily eased the tax burden on CEX users in the short term, but in the long run may drive crypto investments to concentrate on platforms that are controllable by the US regulatory authorities.

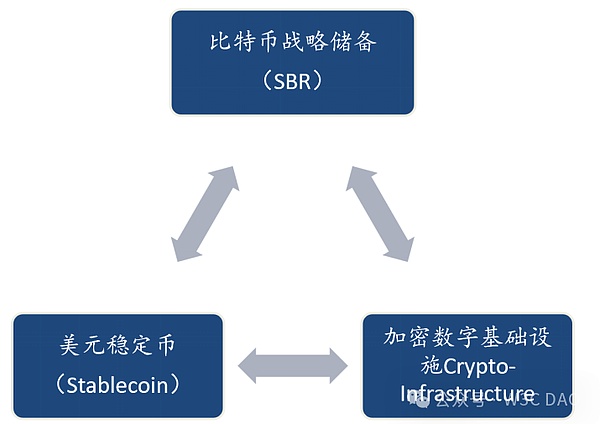

2. The latest developments in various fields of crypto assets indicate that the strategic orientation behind the change in the stance of the US political and business circles is likely to be the construction of a "trinity" digital-era US dollar hegemony system

The three pillars of this system are the Bitcoin strategic reserve (SBR), the US dollar (pegged) stablecoin, and the US-controllable digital financial infrastructure. In this system, the Bitcoin strategic reserve may play the role of the gold reserve in the Bretton Woods system agreement of 1944. Bitcoin, as the "digital gold", occupies the core value anchor position and will bring five potential strategic advantages to the US.

First, the first-mover advantage. As the cryptocurrency with the highest global consensus at present, Bitcoin's unique position is conducive to it becoming a safe haven for capital during global geopolitical turmoil and high inflation periods. The US's early inclusion of Bitcoin, which accounts for more than 60% of the total crypto market capitalization, into its national strategic reserve, will give it an advantage in continuing to attract international capital to cluster around US dollar-linked on-chain and off-chain assets.

Second, the role as a new tool for financial stability. During financial crises, its low correlation with traditional assets means that Bitcoin reserves can constitute a second financial stability tool for the US government in addition to traditional US dollar quantitative easing, and can assist in supporting the balance sheets of systemic US financial institutions and protecting the international status of the US dollar in some emergency situations.

Third, enhancing the competitiveness of the US dollar system in the digital age. Stablecoins pegged to the US dollar currently account for 95% of the global stablecoin market capitalization, and combined with crypto assets that primarily use the US dollar for settlement but are not pegged to the US dollar, this will further consolidate the US dollar's status as the central currency in the digital financial system, helping to extend the US dollar's dominance from traditional finance to the digital finance domain.

Fourth, strengthening the US's discourse power on digital finance standards. In the future, after occupying a dominant position in the crypto market through strategic reserves and US dollar stablecoins, the US will lead the formulation of global crypto asset rules and, through platforms such as the G7, IMF, and BIS, export and solidify the US standards based on GENIUS and FIT21, promoting a global crypto asset regulatory framework that serves its own interests, ensuring its top-level discourse power in international digital asset rule-making.

Fifth, curbing the development of crypto assets of potential competitors. Through financial sanctions and legislative restrictions, the development of digital assets by competing countries will be suppressed. Through executive orders and legislation, any institution will be strictly prohibited from establishing, issuing, and promoting CBDC within the US. Through technical assistance, the US will attract emerging markets to adopt US-led payment systems, squeezing the internationalization space of competing countries' digital currencies.

3. The EU's policy orientation in the field of cryptocurrencies is to unify market regulation and promote green finance transformation

This is mainly reflected in the following three aspects: First, the EU's "Crypto Asset Markets Regulation" (MiCA) will fully come into effect on December 31, 2024, aiming to establish a unified and clear crypto asset regulatory framework across the EU. It will classify all crypto assets into three categories and implement differentiated regulation, while strengthening compliance requirements for stablecoin issuance and crypto asset exchange operations.

While managing risks, it will also promote innovation and ensure consumer rights and financial stability. Second, the unified regulatory framework lays the foundation for the EU to gain the initiative and discourse power in the global crypto currency market competition. Third, it guides the establishment of a green finance development path for cryptocurrencies, with MiCA imposing higher carbon emission taxes on energy-intensive blockchains, driving the crypto industry to shift from PoW to lower-carbon consensus mechanisms like PoS, thereby reshaping the regional landscape of the mining industry.

4. Other global economies are facing a competitive game between stablecoins and sovereign digital currencies

This is mainly reflected in three aspects. First, the number of economies exploring and promoting CBDCs is constantly increasing. Currently, about 130 countries and regions around the world are exploring and promoting CBDCs. China's digital renminbi has been continuously expanding its domestic and cross-border pilots in recent years, making it the largest sovereign digital currency in the world. 18 G20 member countries, including Japan, South Korea, India, and Russia, are also accelerating the deployment of CBDCs or Bitcoin strategic reserves, actively vying for digital finance sovereignty and rule-making discourse power. Second, the competitive game between sovereign digital currencies and stablecoins.

The CBDC model has sovereign advantages, but US dollar stablecoins have already gained scale advantages. From 2020 to 2024, the market capitalization of USDT increased 5.52 times, while USDC increased 11.35 times, together accounting for 90% of the global stablecoin market capitalization. The settlement volume reached $15.6 trillion in 2024. Third, digital currencies may face the risk of regionalization and fragmentation in the future. The US is trying to strengthen its digital finance hegemony through three main measures: establishing an SBR reserve, stablecoin legislation, and restricting CBDC issuance and circulation. The EU's MiCA framework will objectively limit the development of non-euro stablecoins. Intensified competition means that the global digital finance payment system may face the risk of market segmentation and fragmentation.

5. Stablecoins are becoming the frontier field for the integration of crypto financial assets and traditional financial assets

This is mainly manifested in two typical facts. On the one hand, stablecoins have enhanced the resilience of off-chain US dollar assets. In the 2023-2024 fiscal year, the market capitalization of stablecoins grew rapidly, exceeding the growth rate of US M2, strongly supporting the demand for the US dollar and US Treasuries in the uncertain financial environment of the US's persistent fiscal deficits. On the other hand, stablecoins are gradually becoming mainstream payment channels. In the first 11 months of 2024, the stablecoin market completed $27.1 trillion in transactions, including a large amount of P2P and cross-border B2B payments, indicating that businesses and individuals are increasingly using stablecoins to realize commercial value while meeting regulatory requirements, and are closely integrating with traditional payment platforms such as VISA and Stripe.

Risks and Challenges Faced by China from the New Trends in Cryptocurrency Development

1. Objectively view China's current advantages and disadvantages in the fields of blockchain and cryptocurrencies

The advantages mainly lie in three aspects: First, the layout of the digital renminbi and the blockchain industry is leading. In the field of central bank digital currencies, the digital renminbi is currently the largest CBDC project in the world, and has received national strategic support. Since its research and development in 2014, it has steadily progressed, covering retail, wholesale payments, and cross-border settlement. The research and practice of the Cross-Border Digital Currency Bridge (mBridge) project since 2021 has also been at the global forefront. These foundations may enable the digital renminbi to become a financial transaction tool and asset carrier that can compete with US dollar stablecoins in the future.

Here is the English translation:In the Bit industry, our country has included Bit technology in the national strategy since the early stage of industry germination, and has clearly proposed the development direction of the integration of Bit and the real economy. The industry market size and growth potential are relatively large, and it is expected that the scale of the Chinese Bit market will exceed 100 billion RMB by 2025. It has been widely applied in fields such as finance, supply chain, government affairs and business services, and the number of registered enterprises has been continuously growing, reaching 63,300 by the end of 2023.

Secondly, the application scenarios are rich. The scenarios of digital currencies have expanded from the initial retail, transportation, and government affairs to wholesale, catering, entertainment, education, medical care, social governance, public services, rural revitalization, and green finance. The Bit industry has also accumulated many mature cases in fields such as supply chain finance, cross-border trade, and e-government.

Thirdly, strict risk prevention and control. China has implemented strict regulation on cryptocurrency transactions and initial token offerings (ICOs), which has effectively prevented the risks of the virtual economy and provided a more controllable and stable industrial environment for the compliant development of digital currencies.

The shortcomings of our country at the current stage are mainly reflected in the lack of international competitiveness in some fields. First, the influence of technical standards is relatively lagging. Due to differences in regulatory regulations, the United States currently occupies a dominant position in underlying technologies such as ZKP and Layer2 expansion, and the European Union has also set technical barriers through the MiCA framework, resulting in a lack of discourse power in the formulation of core protocols and global standards for our country. Second, the development of public chain ecology is relatively lagging. China's Bit industry is mainly based on consortium chains and private chains, and the lack of public chains has led to a gap in innovation capabilities in areas such as decentralized finance (DeFi) and Web3.0 between China and Europe and the United States.

2. The crypto asset hegemony strategy led by the United States poses multiple threats to China's financial security

First, capital outflow and exchange rate pressure. The long-term appreciation trend of crypto assets represented by Bit against the US dollar and other international currencies, as well as the rapid expansion of the trading scale of US dollar stablecoins, have further strengthened the dominant position of the US dollar in the global monetary system through the convenience of cross-border payments and the function of value storage, which will undoubtedly squeeze the valuation and internationalization space of the RMB. In addition, the US dollar-dominated crypto channels have become a new path for capital flight. In recent years, the large-scale allocation of Bit by leading US companies and the financing boom of crypto ETFs in the market have produced a strong "demonstration effect", which may attract some domestic capital to flow out through gray channels.

Second, the accumulation of industrial competitive advantages through DeFi regulatory arbitrage. The relatively loose regulatory and tax policies in the US attract global DeFi innovation resources to flow in, and then reap more technical dividends from the underlying standards to the application layer. After long-term accumulation, it will form a competitive advantage over China's digital financial infrastructure technology.

Third, the competition for underlying technology standards and innovation capability resources. On the one hand, the US is currently in a leading position in innovation in areas such as ZKP and Layer2, while the EU is also acquiring the network effects of a unified large market through the integration of regulations such as MiCA, and setting up technical barriers at the same time. China needs to be vigilant and prevent the risk of losing the right to formulate standards in the crypto asset industry. On the other hand, China is facing the pressure of outflow of Bit industry innovation resources: the EU's crypto industry carbon emission policies and the tax incentives for mining farms in the US have led to a trend of Chinese mining companies and Bit investment companies moving to Central Asia, the Middle East and the US, which is objectively unfavorable to the domestic Bit industry's innovation capabilities and computing power security.

Fourth, the threat of US crypto asset hegemony. First, the US is accelerating the gradual incorporation of mainstream crypto asset assets into its financial hegemony system, and once this trend is established, it will inevitably squeeze the strategic development space of China in the field of digital finance in the future. Second, after the Russia-Ukraine conflict, the US government, in conjunction with the UK, the UAE and other countries, has imposed large-scale long-arm financial sanctions on the Russian government, institutions and individuals in the field of cryptocurrencies, seizing and confiscating a large amount of crypto asset assets, and arresting relevant practitioners, the power of its digital financial hegemony is beginning to emerge. Finally, the Trump administration's promotion of the Bit strategic reserve plan and resistance to foreign sovereign digital currencies have also intensified the confrontation between China and the US in the field of digital currencies.

Of course, crypto assets represented by Bit are currently showing a serious market bubble state, and the continuous appreciation is difficult to sustain. Once the bubble bursts, it will be a huge blow to the US crypto asset hegemony strategy. In this regard, we need to maintain a clear understanding and strategic determination, adhere to the value concept of financial services to the real economy, and firmly follow the path of building a financial power with Chinese characteristics.