One-sentence summary: Short squeeze, seasonal factors, sentiment bottoming out, pension rebalancing, continuous retail buying, and potential monetary cash deployment may drive a rebound

As of March 20th, Goldman Sachs trading desk data:

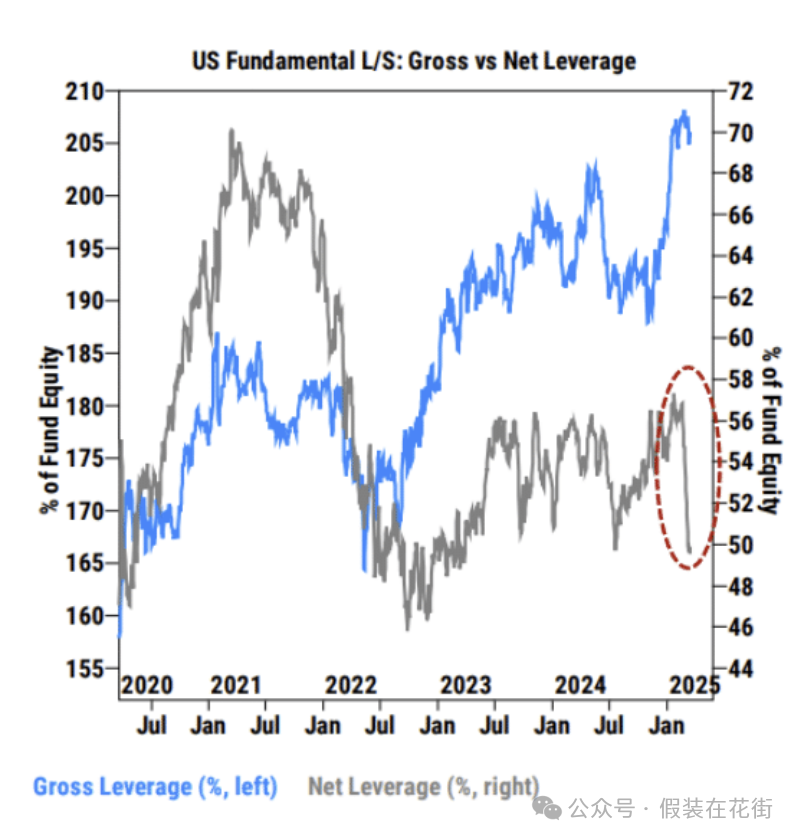

The net leverage ratio of US basic hedge funds (gray line) has sharply dropped to a two-year low of 75.8%;

However, the total leverage ratio (blue line) remains high at 289.4%, the highest in five years, which is clearly due to rising shorts;

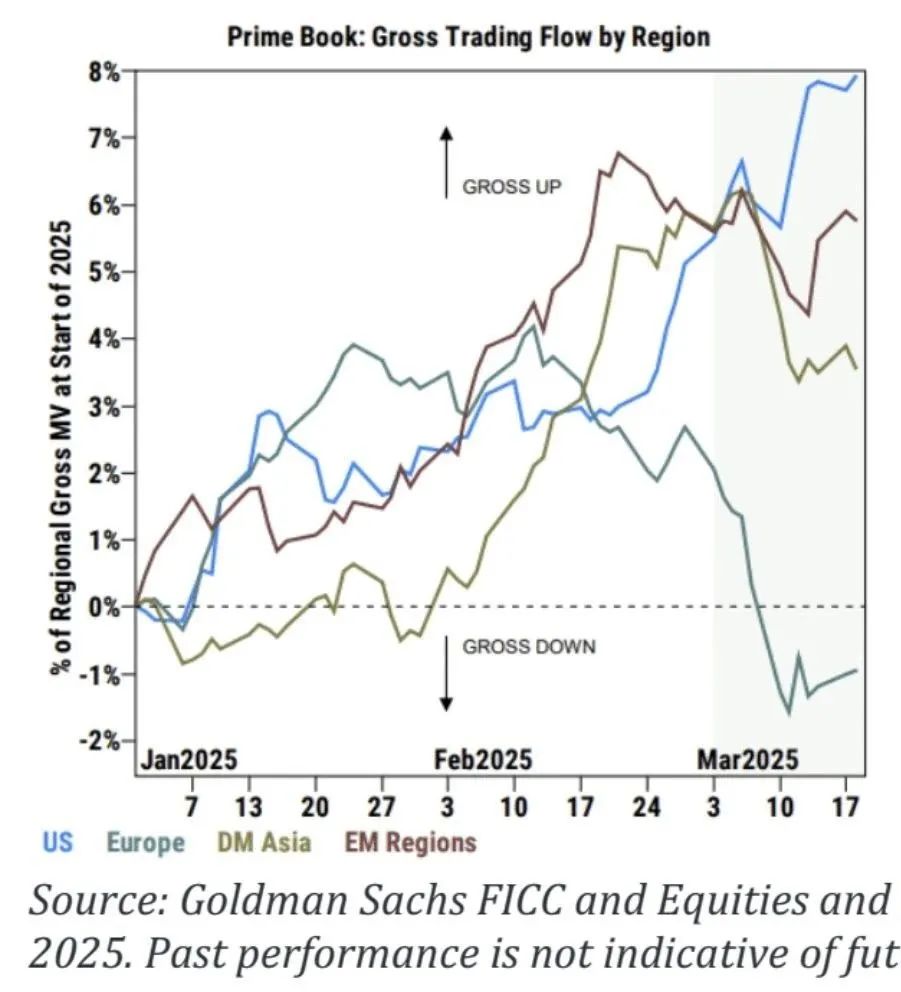

The chart shows that funds' total leverage ratio increased by 2.5% in March in the US, while deleveraging in other parts of the world;

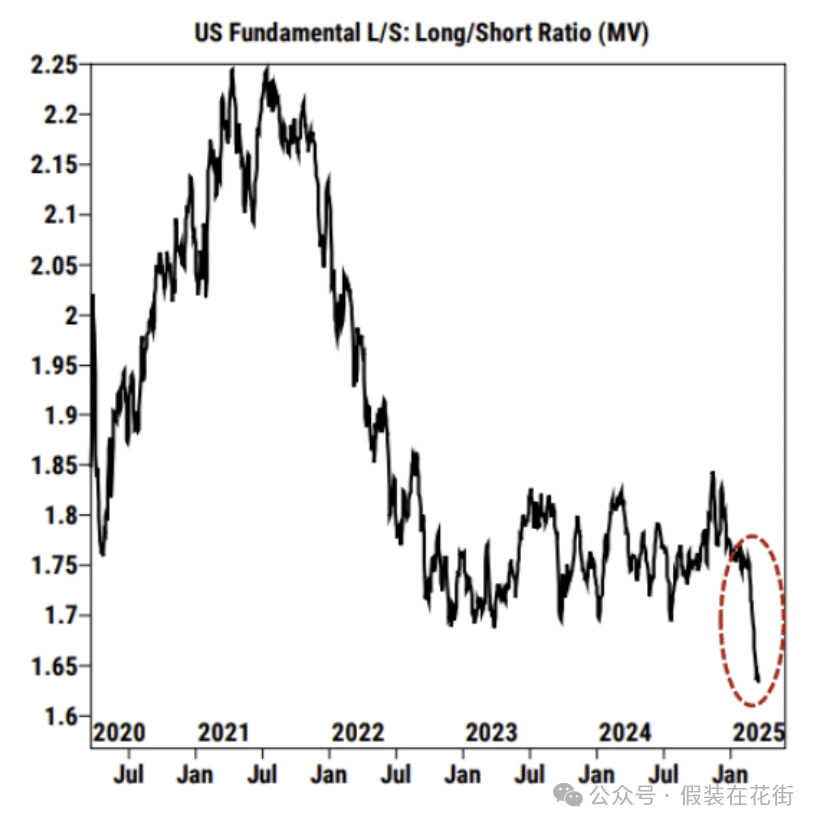

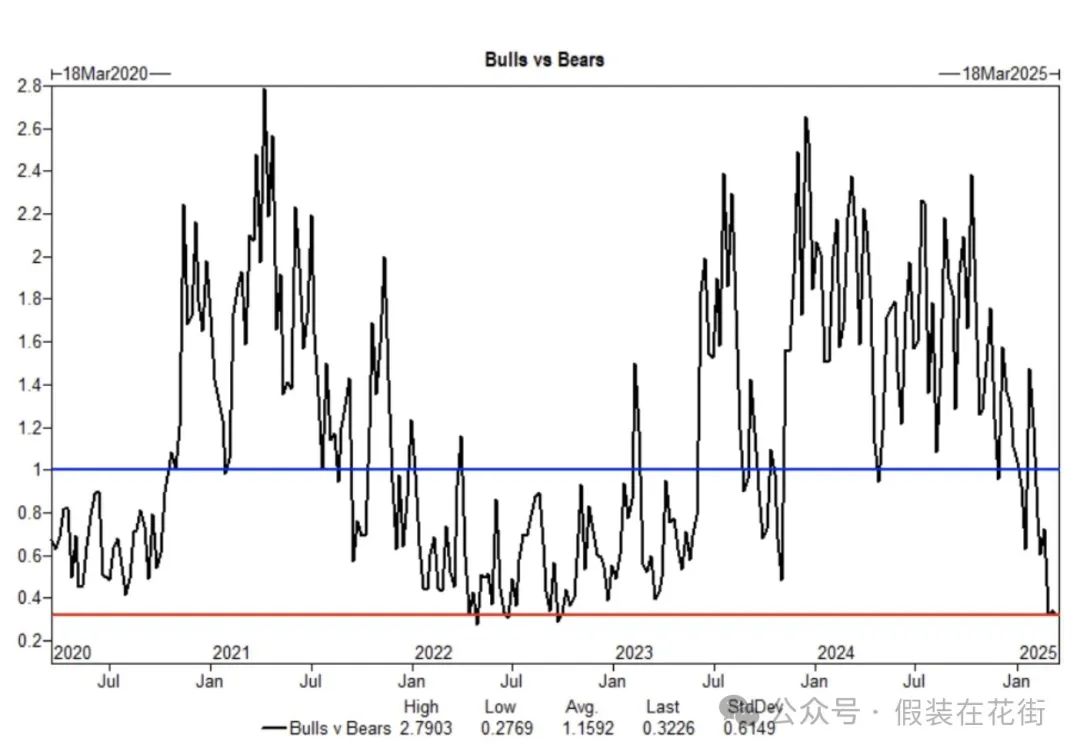

The long/short ratio (by market value) has dropped to the lowest level in over five years at 1.64;

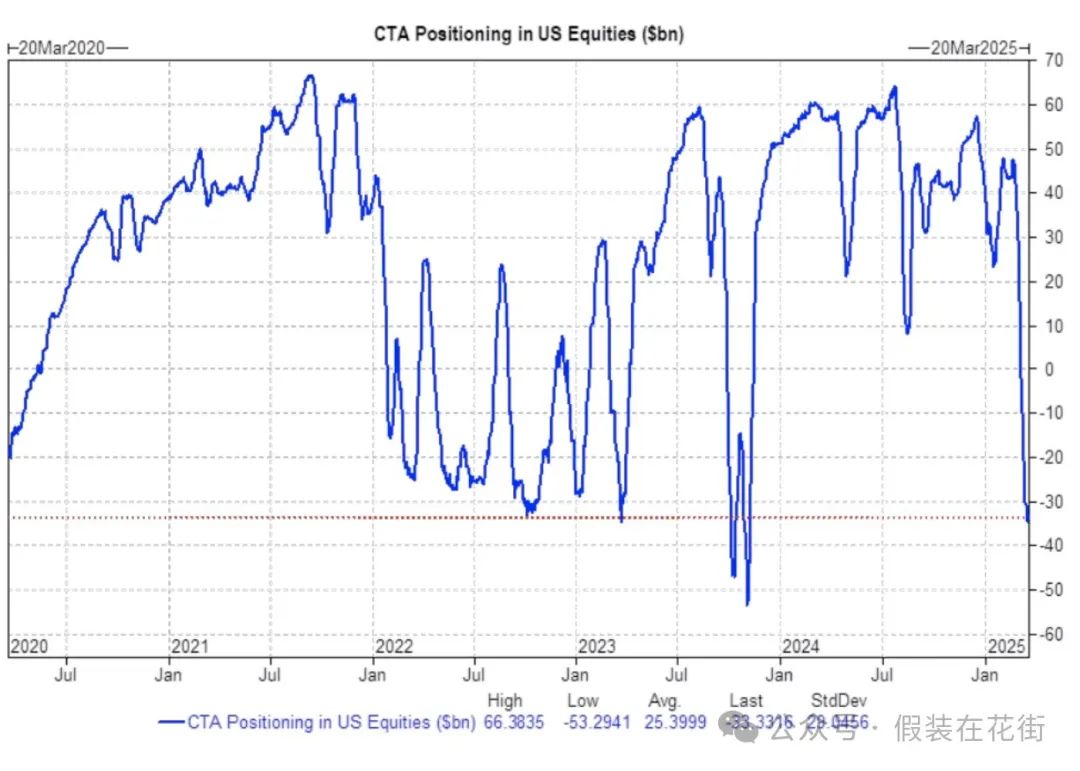

CTA funds have net shorted US stocks for the first time in a year and a half;

CTA funds have net shorted US stocks for the first time in a year and a half;

These show that some high leverage has been reduced, but there is still room for deleveraging before tariff implementation, and we are very close to a reversal.

The increase in total leverage is due to increased leveraged shorts, which might be a good thing. The data shows that hedge funds are reluctant to significantly reduce long positions and instead rely on externally financed leveraged shorts. When market volatility occurs, financing parties may issue margin calls, forcing shorts to close positions or sell other assets to supplement margins, significantly increasing the probability of a short squeeze. If funds choose to sell other assets, it may amplify market abnormal fluctuations.

However, note that this does not necessarily mean an inevitable rise, but rather that if a rise occurs, a short squeeze could help push it.

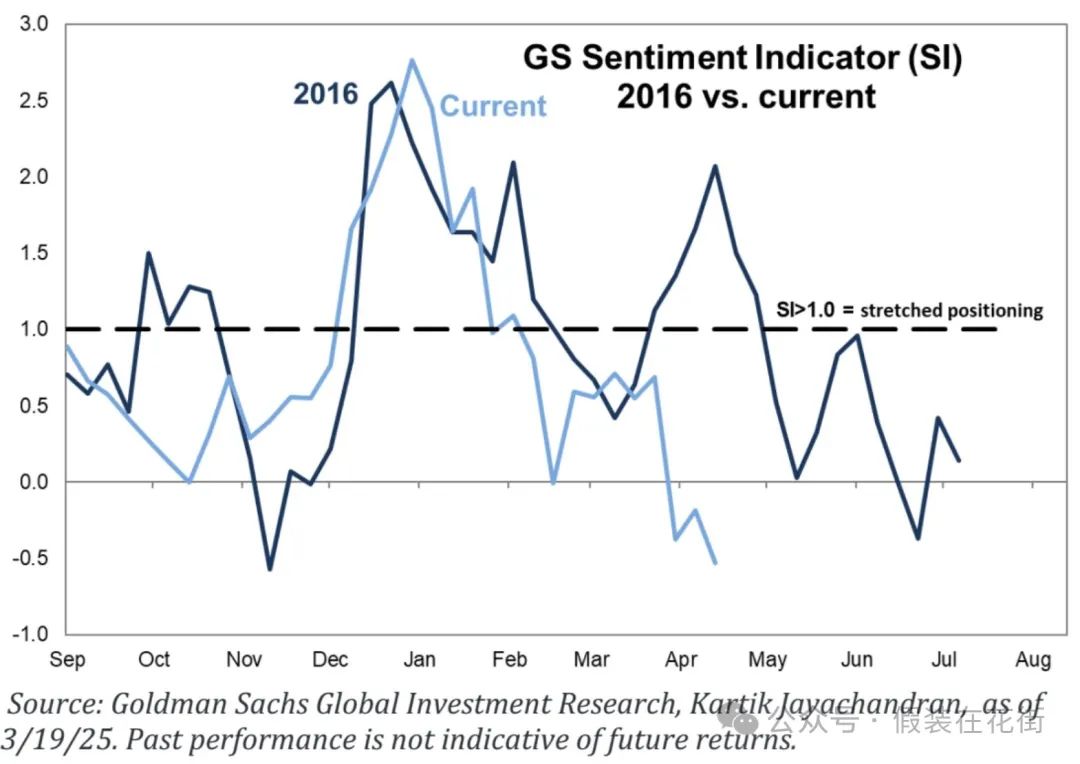

Market sentiment has reached rock bottom, and the market has returned to an environment where "good news is good news", with potential for sentiment recovery:

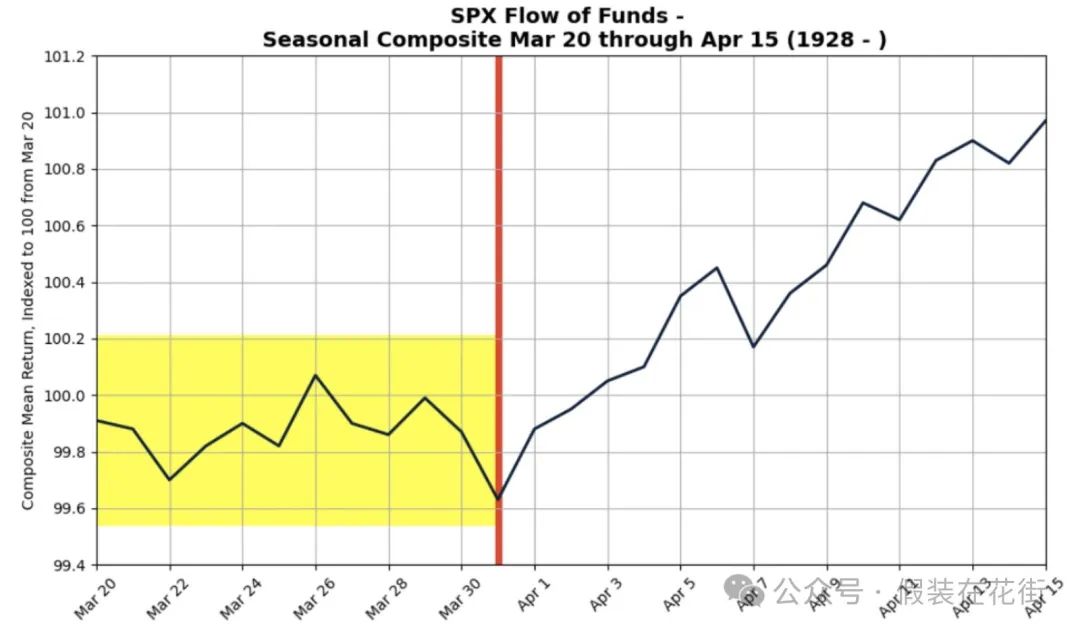

Seasonal negative factors approaching their end:

According to data since 1928, the second half of March is usually volatile, and this year is no exception.

However, the S&P 500 index averages a 0.92% increase from March 20 to April 15, and averages a 1.1% increase from late March to April 15.

This suggests potential for a seasonal rebound in April, but with limited magnitude. After April 2, the market may stabilize without major unexpected events.

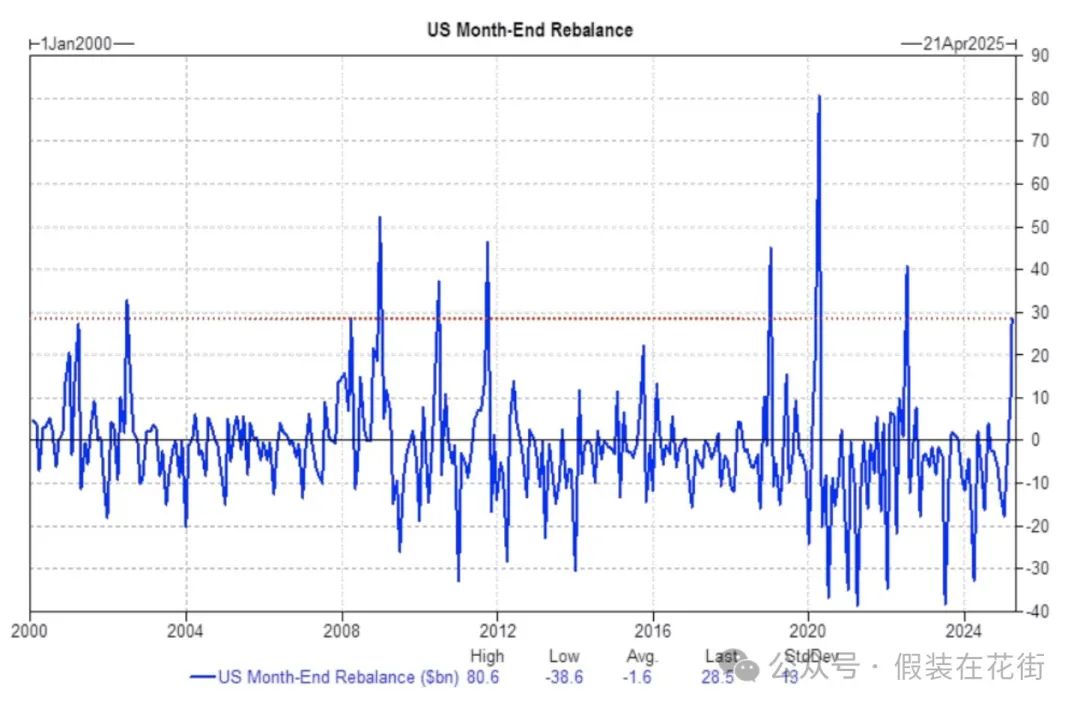

US pensions are expected to buy $29 billion in US stocks at the end of the quarter, ranking in the 89th percentile of absolute value estimates over the past 3 years, and the 91st percentile since January 2000. This may provide some market support:

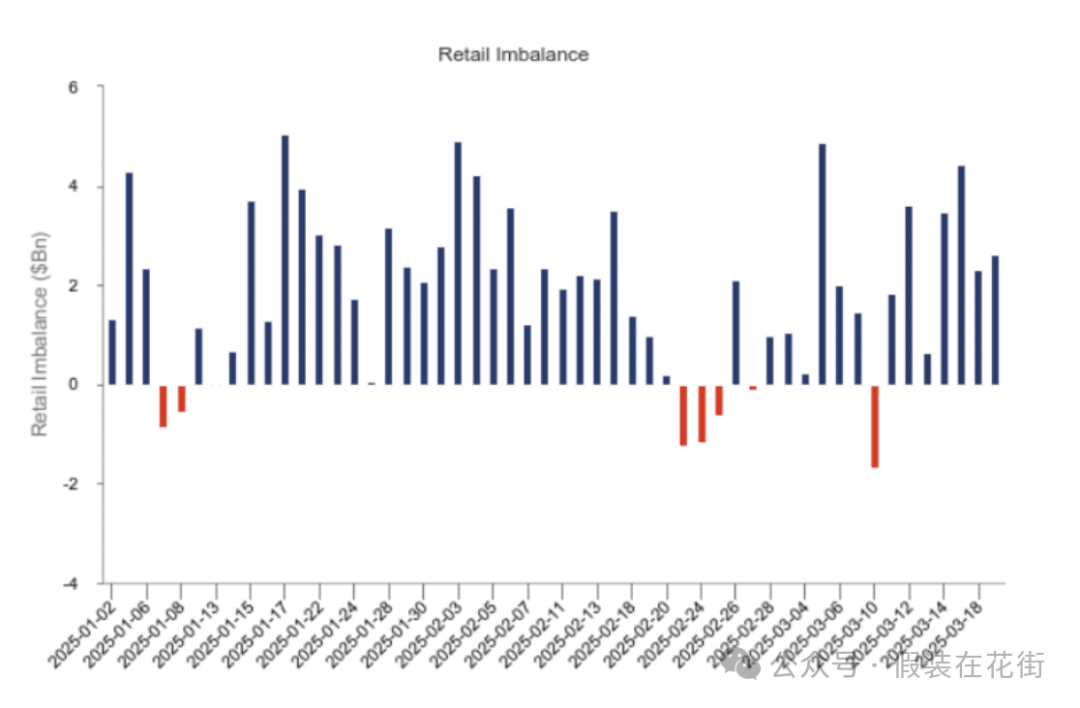

Despite market volatility, retail investor participation remains stable. In 2025 so far, retail investors have only had net selling on 7 trading days, with cumulative net buying reaching $1.56 trillion.

Additionally, money market funds (MMFs) continue to grow, reaching $8.4 trillion in the US. These funds represent cash reserves for retail and other investors, which could quickly convert to stock market buying once market sentiment improves or investment opportunities emerge.

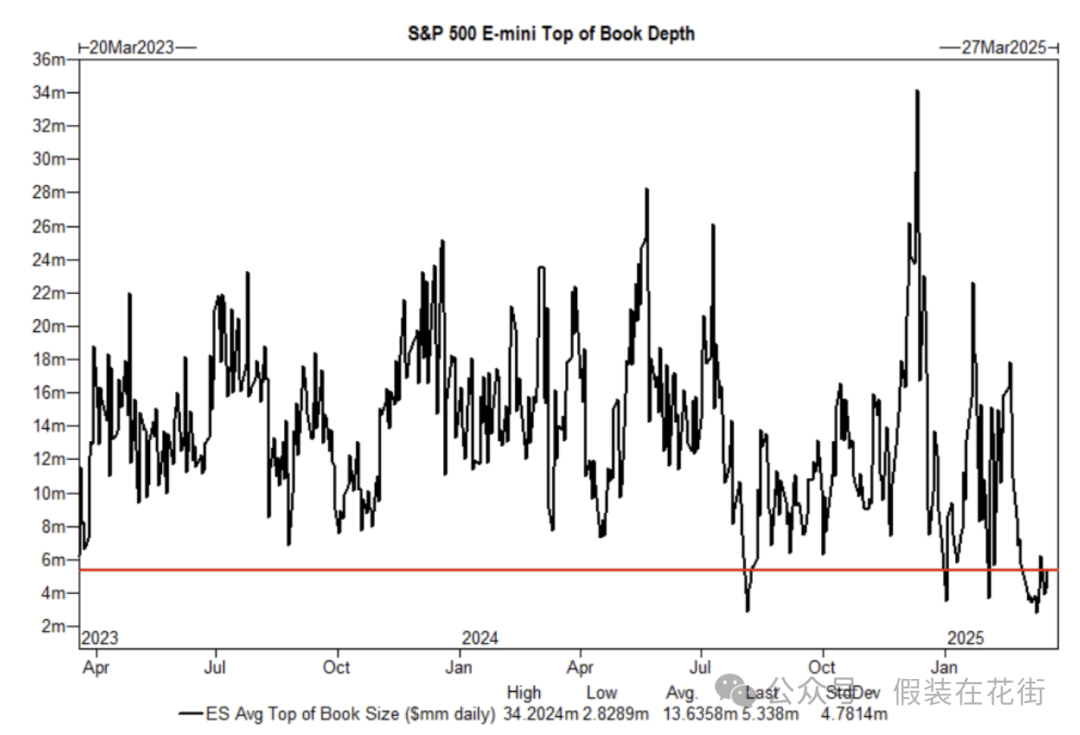

Market liquidity remains thin, which is why intraday volatility is often significant. Risks should be noted: