Get the best data-driven crypto insights and analysis every week:

State of the Network’s Q1 2025 Wrap Up

By: Tanay Ved

Key Takeaways:

Macroeconomic pressures drove the crypto market cap down 19% to $2.65T in Q1 2025, with Bitcoin (BTC) declining 7%, while Ethereum (ETH) and Solana (SOL) posted steeper losses amid risk-off sentiment.

Total stablecoin supply surpassed $230B, with USDC and Ethereum as major beneficiaries, while new entrants race to launch products amid advancing stablecoin legislation.

Ethereum’s Layer-2 scaling strategy has created a temporary value disconnect, contributing to ETH’s underperformance. Scaling blob capacity and L2 demand, and attracting high-value use cases like tokenization and stablecoins to L1 may offer a viable path to restore value accrual.

Solana implemented key SIMD upgrades reshaping validator incentives and burn policy, while a cooldown in memecoin activity highlighted the need for more sustainable forms of network usage.

Introduction

In this special edition of State of the Network, we take a data-driven dive into the major developments, market performance, and network activity that impacted the digital assets industry in Q1 2025.

Market Performance: A Risk-Off Environment

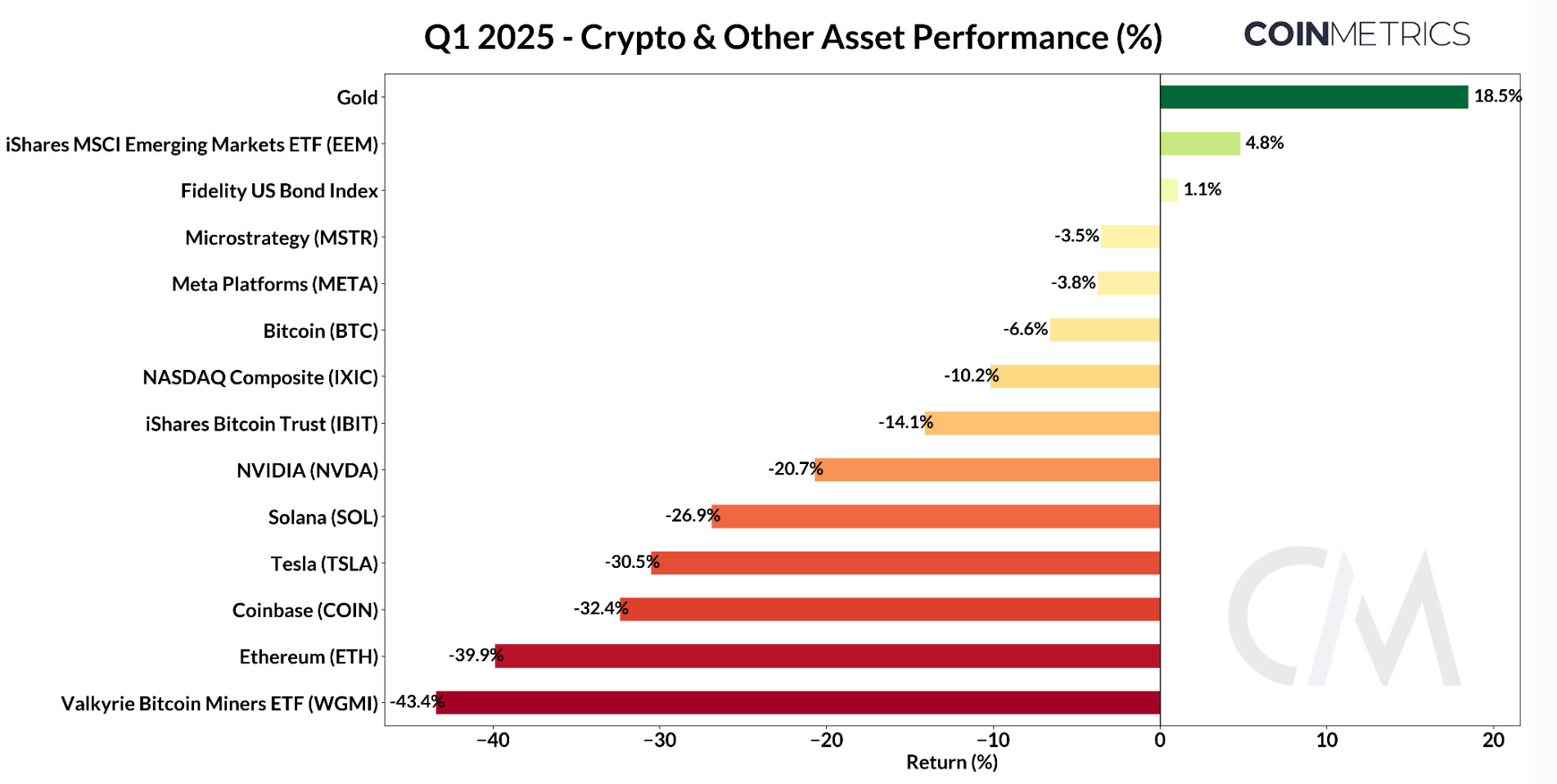

Q1 2025 was characterized by risk averse sentiment as macroeconomic pressures weighed on both digital assets and traditional markets. Uncertainty around trade policy, inflationary pressures, and a weakening economic outlook pushed investors toward safe havens—most notably gold, which outperformed all major asset classes with an 18% year-to-date return. Meanwhile, risk assets, including the NASDAQ Composite and the “Magnificent Seven” technology stocks gave back their pre-election gains.

Source: Coin Metrics Reference Rates & Google Finance

Despite positive momentum within the crypto industry, such as the SEC’s dismissal of major enforcement actions, establishment of a Strategic Bitcoin Reserve and growing institutional interest in stablecoins and tokenization, sentiment was dragged down by the industry’s largest ever exploit, (the Bybit hack) and frustration over extractive memecoin launches. Caught in these forces, the total crypto market capitalization fell 19% to $2.65T. Bitcoin (BTC) ended the quarter down ~7%, while Solana (SOL) and Ethereum (ETH) saw steeper declines of 27% and 39%, respectively.

Among crypto equities, MicroStrategy remained active in Q1, raising capital through new instruments to expand its Bitcoin holdings. As of March 31st, Strategy’s holdings have reached 528,185 BTC. The firm issued two new classes of preferred stock—STRK and STRF—alongside a $2B zero-coupon convertible note offering. This playbook has inspired others, with GameStop recently announcing a $1.3B convertible bond raise, joining a growing list that includes Marathon Holdings and Metaplanet. Coinbase (COIN) and publicly traded Bitcoin miners, however, struggled under broader market pressures.

Stablecoins & Tokenization Gain Momentum

Stablecoins took center stage in a quarter full of volatility. With the total stablecoin market cap now surpassing $230B, the space is drawing a new wave of entrants looking to secure a slice of the rapidly growing market. With the GENIUS Act and STABLE Act introduced in the Senate and the House, stablecoin legislation is inching closer to reality, prompting institutions like Fidelity to launch their own stablecoin and tokenization initiatives.

Recognition of stablecoins is growing on multiple fronts. Payments firms like Stripe have called them “superconductors” of finance in their recent annual letter, while Tether has become the world’s seventh-largest holder of U.S. Treasuries, reinforcing their role in entrenching dollar dominance and supporting demand for U.S. debt.

Source: Coin Metrics Network Data Pro

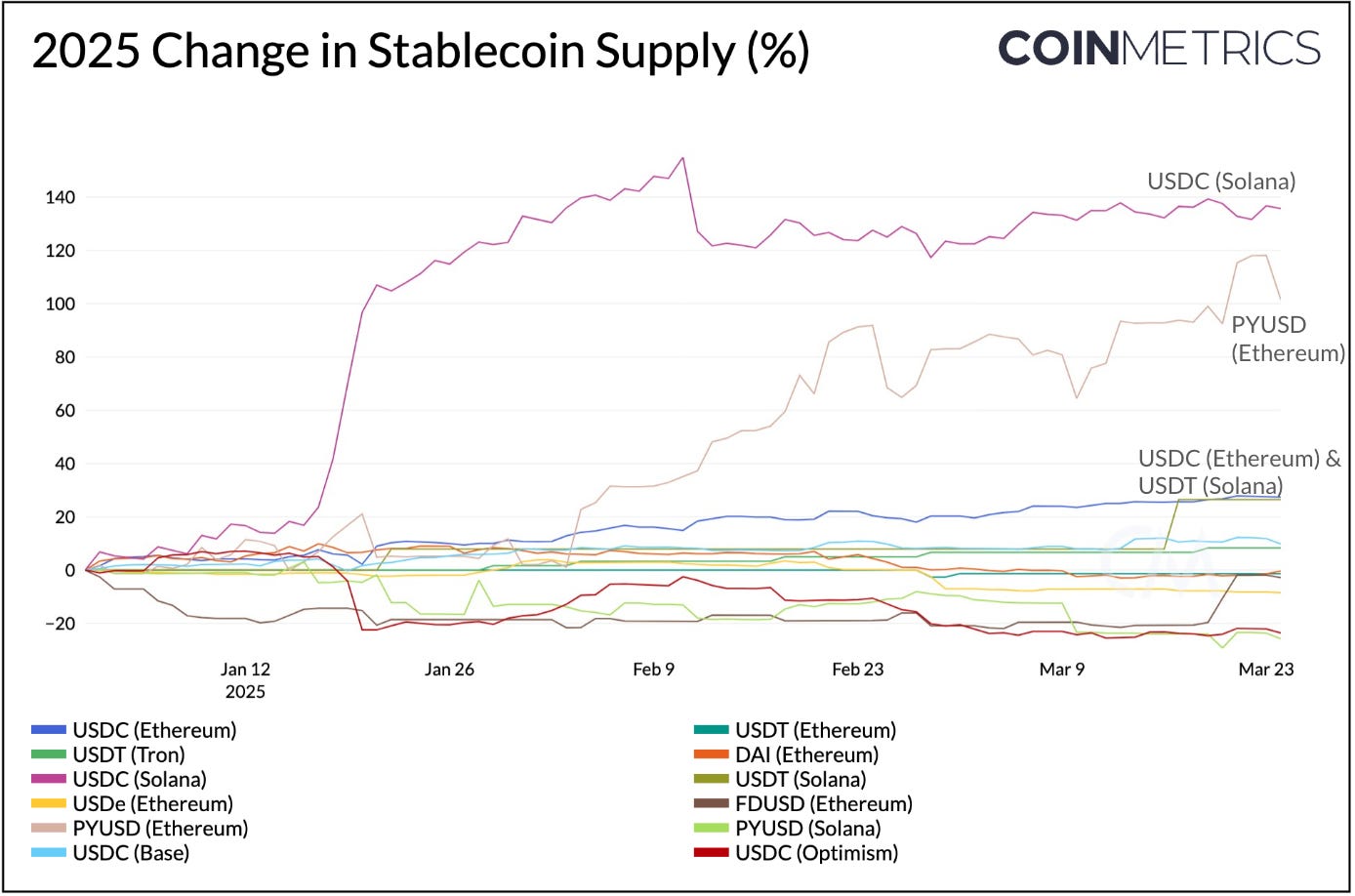

Among stablecoins issued on various blockchains, USDC on Solana experienced the largest increase in supply, growing 137% to $9.9B. This influx of liquidity into Solana’s ecosystem came alongside the launch of the TRUMP meme coin and has remained steady despite a broader cooldown in network activity. PayPal’s PYUSD on Ethereum grew by 105% to $670M in supply, while USDC (Ethereum) and USDT (Solana) also grew steadily by ~28%. Overall, Circle’s USDC was a major beneficiary of Q1’s stablecoin momentum, reaching a new all-time high of $60B in market capitalization.

Source: Coin Metrics Network Data Pro, Stablecoin Dashboard

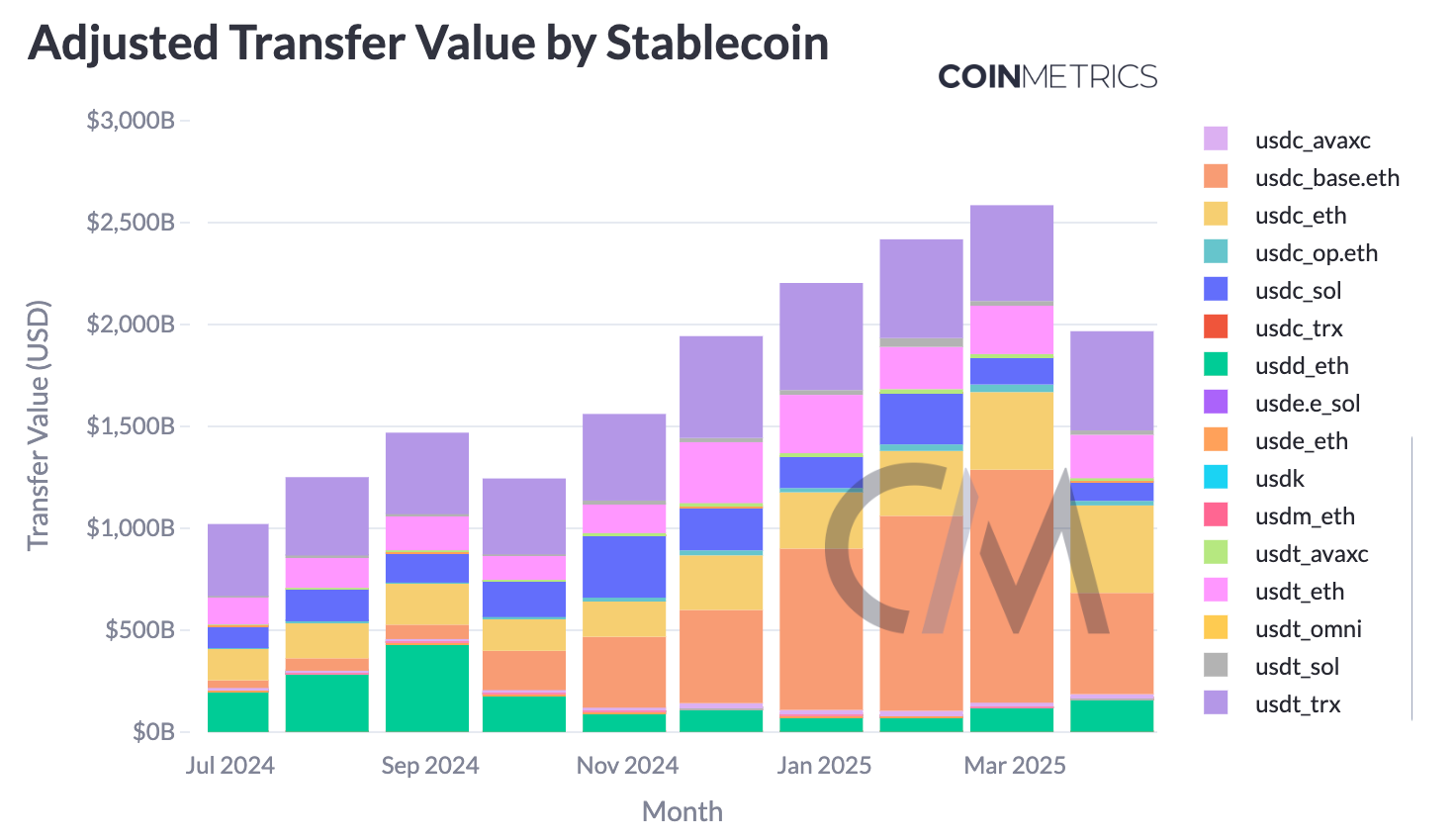

Total stablecoin transfer volume (on an adjusted basis) has continued to climb higher. Most notably, in Q1 a majority of this growth came from USDC on the Base Layer-2 network. Base facilitated $956B and $1.1T in USDC adjusted transfer volume in January and February, even surpassing USDT on Tron. This momentum on Base highlights its growing DeFi ecosystem and dominance in stablecoin usage among low-fee networks.

The Ethereum & ETH Disconnect

Ethereum’s lead in stablecoins and tokenization continued to grow, with stablecoin supply on the network reaching a record $130B and tokenized treasuries like BUIDL crossing $1.8B in assets. Despite this deep liquidity, activity on Ethereum has lagged behind prior years. ETH’s underperformance widened in Q1, with the ETH/BTC ratio falling to a five-year low. So what’s driving the disconnect between the Ethereum blockchain, its Layer-2 ecosystem and ETH’s performance?

Source: Coin Metrics Network Data Pro

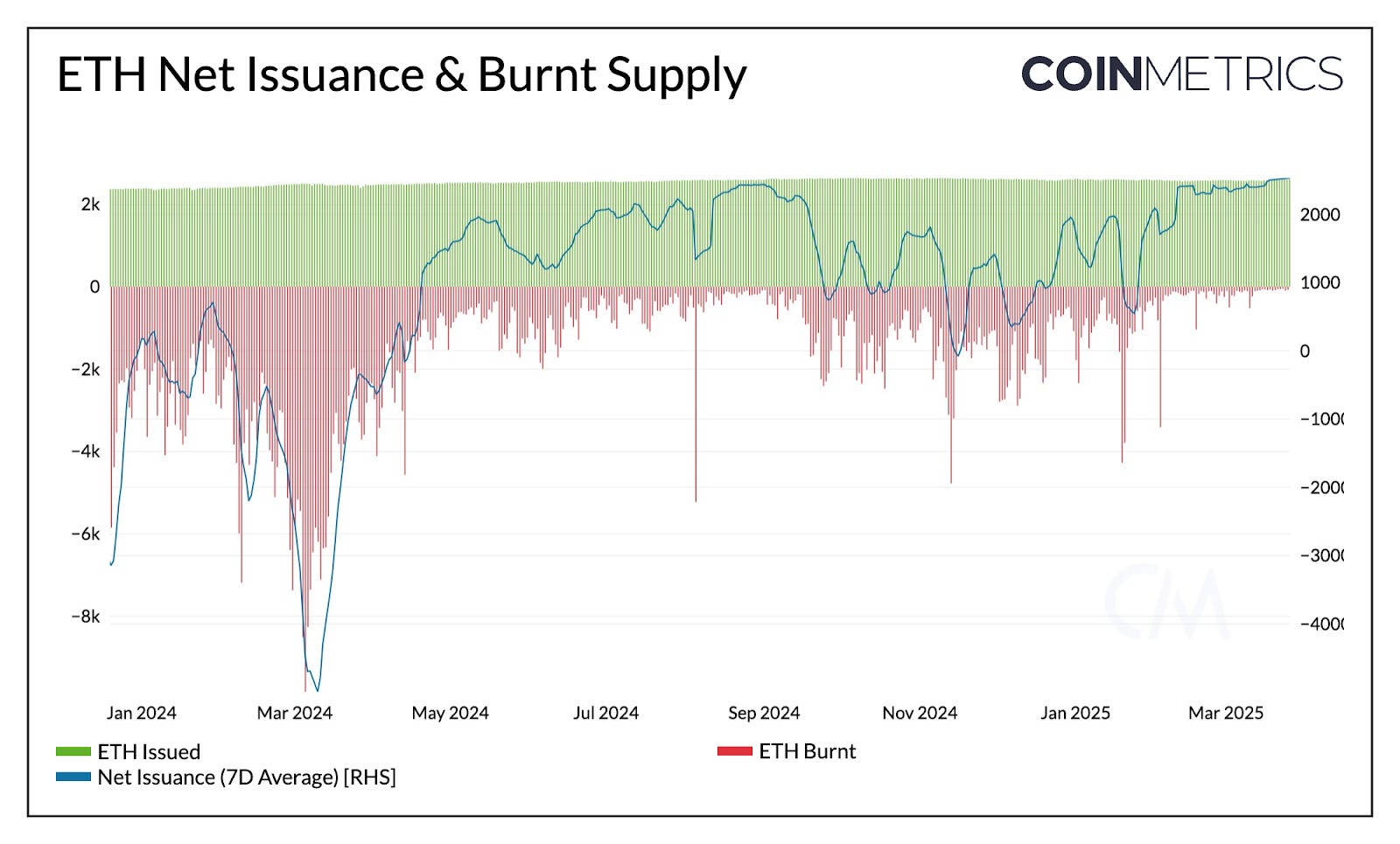

This disconnect appears to stem from multiple factors, particularly Ethereum’s roadmap of scaling via Layer-2s and the current lack of meaningful value accrual to ETH through fees. With the implementation of EIP-4844 in the Dencun upgrade, the introduction of blobspace brought a noticeable shift in network economics. In March 2024, Ethereum generated nearly $30M in total fees; one year later, that figure has dropped to around $500K.

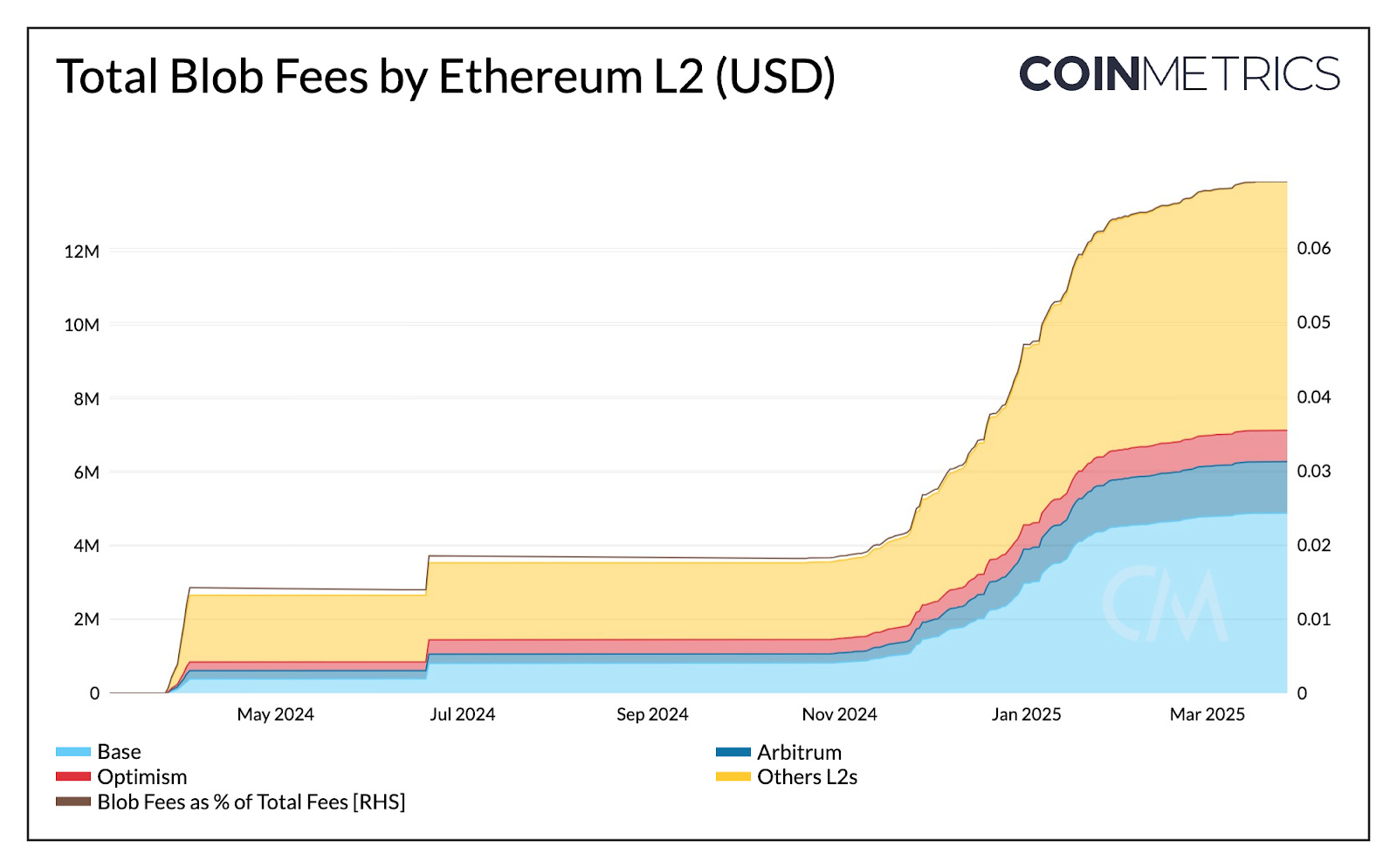

This decline is largely due to execution migrating to L2s, with minimal value flowing back to the L1. Layer-2s like Base, Arbitrum, and Optimism have collectively paid just $13M in blob costs, while maintaining profit margins over 90% through sequencer revenue. This dynamic has raised concerns around value leakage, where Ethereum bears the cost of security while L2s capture a disproportionate share of economic value. Blob fees now account for only 0.07% of total fees, and with lower base fees, less ETH is being burned. Over the past week, only ~70 ETH was burned per day, increasing net issuance and raising the annual inflation rate to 0.79%.

Source: Coin Metrics Network Data Pro

While this dynamic is currently weighing on ETH’s valuation, Ethereum’s long-term strategy of scaling through L2s may take time to bear fruit. Due to the commoditization of blobspace, and the profitability of Layer-2 business models, the number of L2s and blob transactions in Ethereum’s ecosystem are expected to grow. With ~21K blobs posted daily, blob transactions are consistently hitting target capacity (3 blobs per block).

The upcoming Pectra upgrade (and Fusaka afterward), aims to incrementally scale blob capacity further (EIP-7691), making costs cheaper, driving more demand for transactions on L2s and therefore higher blob fees in aggregate. In parallel, scaling the L1 through gas limit increases and attracting high-value use cases to the base layer—such as stablecoins, tokenization, and DeFi—may offer a viable path to restore long-term value accrual to ETH. In the upcoming quarter, attention around Ethereum’s staking ecosystem may come to the fore as Pectra brings new improvements and issuers seek to launch staked Ether ETFs.

Solana’s Stress Test & Network Upgrades

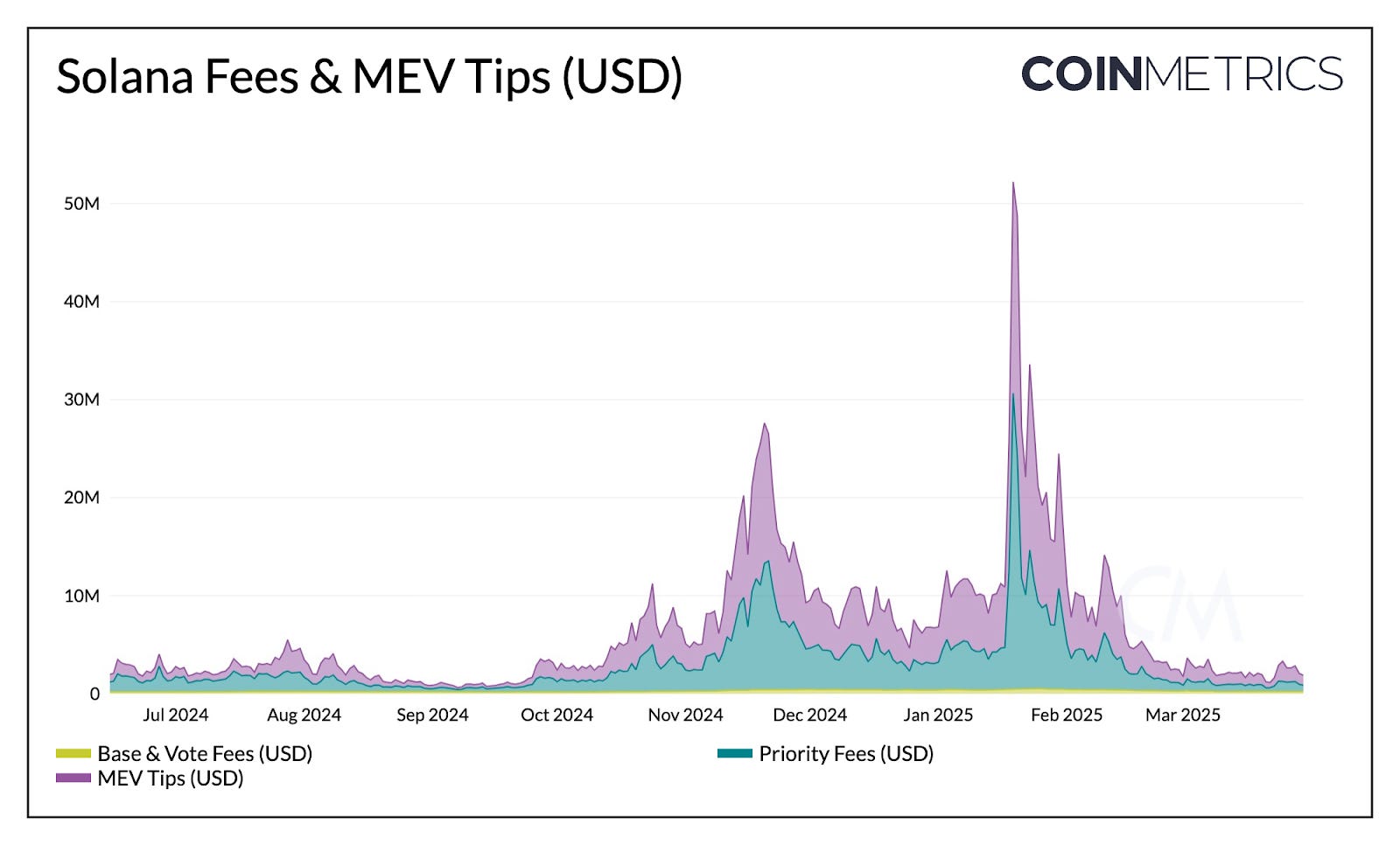

Q1 was an eventful quarter for Solana. Early in the year, the network was put through an important stress test with the launch of the TRUMP memecoin. For a period, network activity rose to unprecedented levels, driving network congestion, fees and MEV tips (out-of-protocol tips for transaction prioritization) higher. The event also brought a spike in non-vote transactions, which reached 112M, and active wallets, which briefly rose to 5.6M. However, this burst of activity was short-lived, as memecoin activity cooled and broader market conditions deteriorated.

Source: Coin Metrics Network Data Pro

This quarter was also important for Solana from a network development standpoint. Three key Solana Improvement Documents (SIMDs) were put to vote, impacting network economics and validator incentives. Chief among them was SIMD-0228, a proposal to implement a dynamic issuance rate based on staking participation (% of SOL supply staked). With Solana’s current annual inflation rate at ~4.5% (reducing 15% annually), the goal was to curb issuance and reduce reliance on inflationary rewards, shifting validator revenues towards priority fees and MEV tips.

However, the proposal ultimately failed to garner majority support, as concerns around smaller validator profitability and potential for validator centralization emerged. While priority fees and MEV tips have dropped from their peak, they collectively represent 87% of Solana’s economic value.

Source: Coin Metrics Network Data Pro

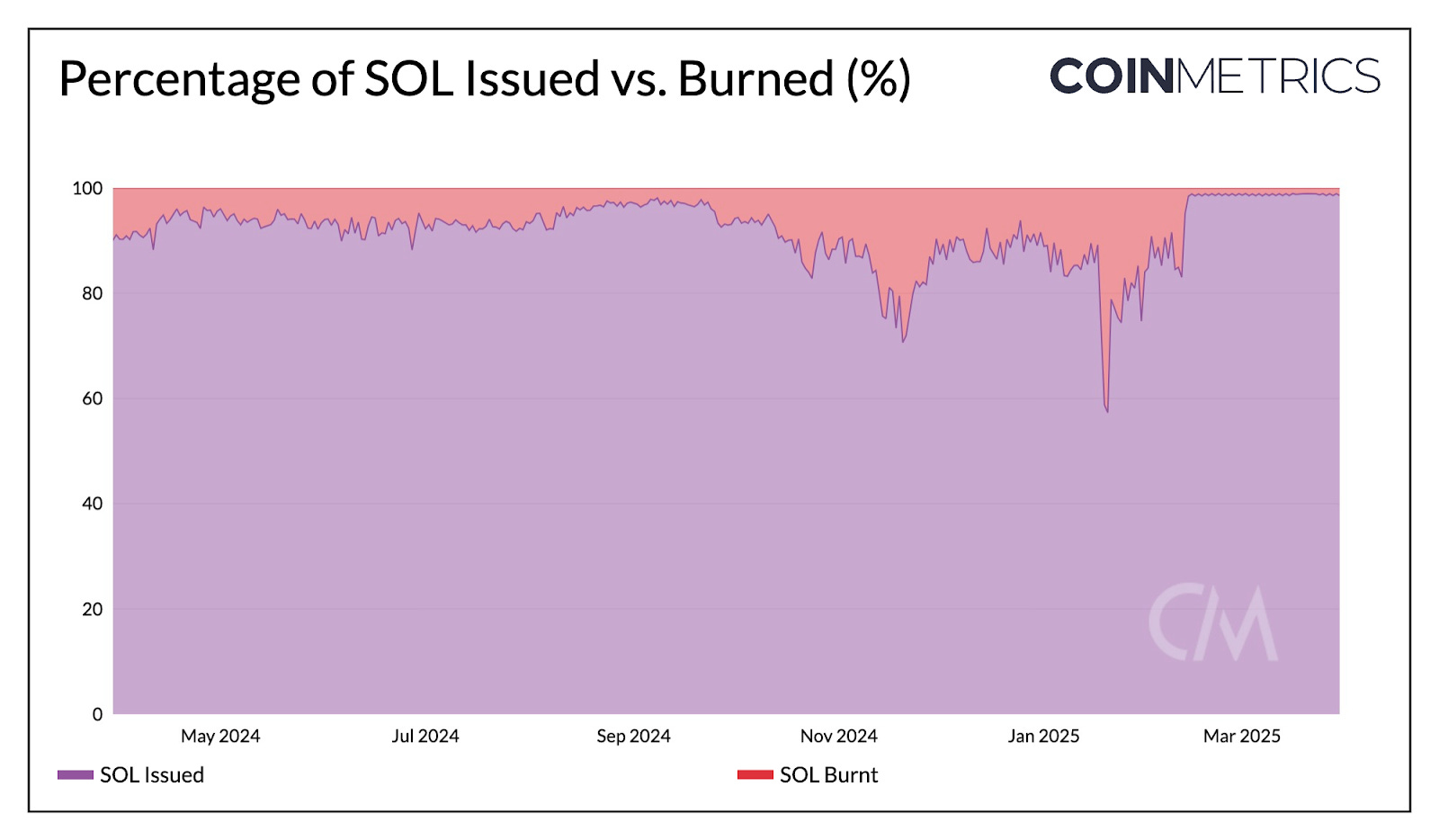

On the other hand, Solana SIMD-0096 passed, directing 100% of priority fees to validators. This eliminated the previous policy that burned 50% of priority fees, boosting validator and staker rewards. This change incentivizes the use of Solana’s native priority fees, reducing reliance on out-of protocol tip systems like Jito. Since being implemented, the average amount of SOL burned has dropped from ~15.9K to ~950, creating inflationary pressure on supply. Alongside this, SIMD-0123 passed, creating a mechanism for validators to distribute priority fees with stakers.

As the Solana network matures, the coming quarters will reveal its ability to foster more sustainable forms of activity. Meanwhile, signs of institutional traction are emerging, with SOL futures now live on the Chicago Mercantile Exchange (CME), potentially paving the way for SOL spot ETFs.

Conclusion

While this quarter was plagued by macroeconomic uncertainties, structural catalysts like regulatory clarity and institutional adoption continue to advance. Bitcoin and stablecoins were major beneficiaries, extending their dominance as foundational anchors of the crypto ecosystem. Simultaneously, incremental network upgrades like Ethereum’s Pectra upgrade and Solana’s recent SIMDs proposals, despite being at different stages of growth, promise to strengthen on-chain infrastructure, improving utility for builders, users, and network stakeholders. Though near-term volatility may persist, the medium-term outlook remains constructive, as a shift in macro conditions could bring renewed liquidity and risk appetite back to crypto markets.

Coin Metrics Updates

This quarter’s updates from the Coin Metrics team:

Coin Metrics is hiring for a Research Analyst and Backend Software Engineer. Find more information about the roles and apply here!

This quarter, we introduced Coinbase Exchange Flows data and launched new network and asset profiles.

We’re excited to share that Coin Metrics has received a grant from dYdX to deliver institutional-grade analytics for dYdX v4. Read the full announcement.

Follow Coin Metrics’ State of the Market newsletter which contextualizes the week’s crypto market movements with concise commentary, rich visuals, and timely data.

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.