Author: Sam @IOSG

TL;DR:

Using the stablecoin bill as an introduction, highlighting recent public attention and discussion on RWA, and then discussing RWA on Ethereum

Data analysis (zksync can be a highlight)

The impact of Etherealize on Ethereum

Ethereum's stablecoin issuance and DeFi have always had a strong moat. Combining the new US policies, can RWA organically connect traditional finance and DeFi? As the most credible and decentralized blockchain, where do we continue to be optimistic about Ethereum

Bill Catalysis and Market Attention

Against the backdrop of rapid evolution in traditional finance and regulatory environment, the recent passage of the GENIUS Bill has reignited market interest in RWA. Beyond stablecoins and major legislative progress, the RWA field has quietly achieved multiple important milestones: a sustained strong growth trend and a series of eye-catching breakthroughs—such as Kraken launching tokenized stocks and ETFs, Robinhood proposing to the SEC to grant token assets equal status with traditional assets, and Centrifuge issuing a $400 million decentralized JTRSY fund on Solana.

At a time of unprecedented market attention and imminent broader adoption by traditional finance, it is crucial to closely examine the current RWA landscape—especially the position of leading platforms like Ethereum. RWA based on Ethereum has shown an astonishing month-on-month growth rate, consistently maintaining double-digit highs; the growth rate in 2025 is even more accelerated compared to single-digit months in 2024. Another key factor driving this momentum is "Etherealize" as a catalyst for regulatory development, and the Ethereum Foundation listing RWA as a strategic priority. At this critical juncture, this article will delve into the development dynamics of RWA on Ethereum and its Layer-2 networks.

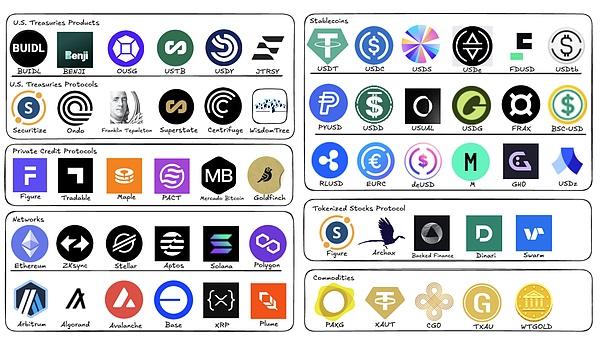

RWA Ecosystem Map, IOSG

Data Analysis: Comprehensive Growth of Ethereum RWA

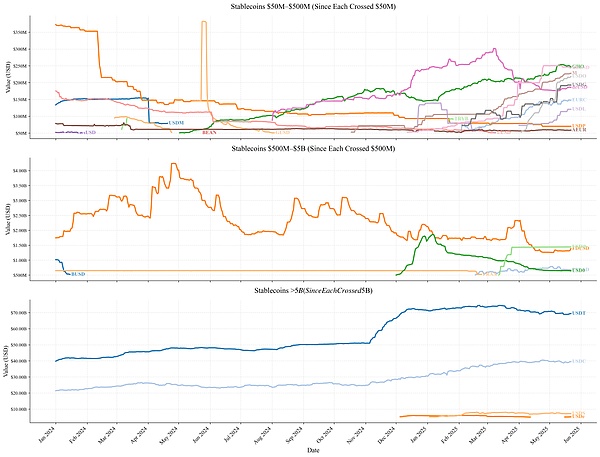

(The rest of the translation follows the same approach)In small projects (<$500 million), most projects experienced continued contraction in early 2024. However, towards the end of 2024, most project market values continued to rise, with GHO, M, and USDO market values growing continuously. Meanwhile, a batch of new stablecoin projects emerged, crossing the $50M market value, and the Ethereum stablecoin ecosystem became more diverse, with small market cap projects continuing to flourish since 2025.

In medium-sized projects ($500 million to $5 billion), only FDUSD and FRAX existed in 2024; BUSD, due to termination of issuance, plummeted from $1 billion in January 2024 to less than $500 million in March. However, in 2025, USDO and PYUSD both broke through the $500 million threshold, making medium-sized stablecoins more diverse.

Top stablecoins (>$5 billion) continued to be dominated by USDT and USDC: USDT remained stable at a $40 billion market value for most of 2024, jumped to $70 billion in early December, then gradually stabilized, until recently experiencing some market value decline; USDC steadily grew from $22 billion in January 2024 to $38 billion in May 2025. In early 2025, USDS and USDe both broke through $5 billion, but USDT and USDC still led by a wide margin in market share.

RWA.xyz, IOSG

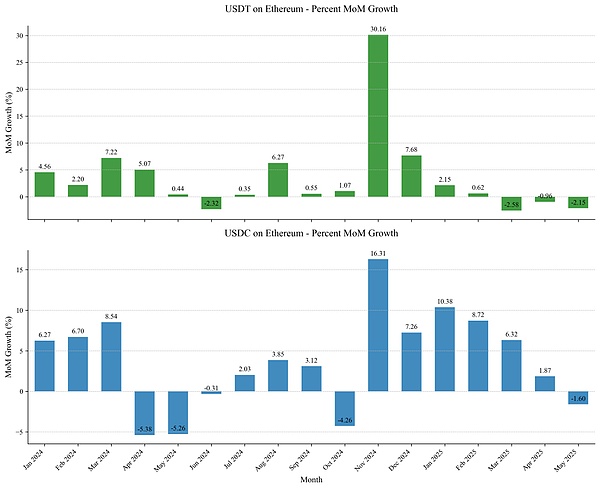

USDT and USDC occupy an absolute dominant position, directly influencing the entire stablecoin ecosystem.

The growth in November 2024 was particularly noteworthy: USDT surged by 30.16% month-on-month that month, while USDC achieved 16.31% growth. After this surge, growth continued for several months, with USDC showing more stable growth in subsequent months, all above 5%. According to issuer disclosures: Tether attributed this to "a tide of collateral assets flowing in from exchanges and institutional trading desks in anticipation of increased trading volume"; Circle emphasized "USDC circulation grew 78% year-on-year... besides user demand, this also stemmed from market confidence rebuilding and standard system improvement triggered by emerging stablecoin regulatory rules".

However, market momentum has recently changed significantly - in the past four months, USDT on the Ethereum chain has been stagnant in growth, and in May 2025, USDC experienced its first decline after months of growth. This phenomenon may signal that the market is transitioning to a new cycle stage.

RWA.xyz, IOSG

L2 Ecosystem

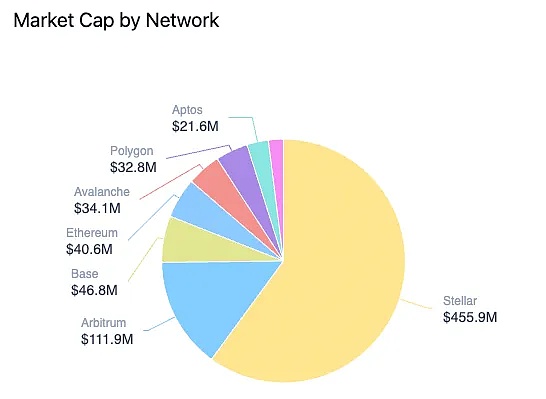

In the broader RWA ecosystem, Ethereum maintains absolute dominance with a 59.23% market share (excluding stablecoins), but still faces key challenges.

Screenshot from RWA.xyz

Notably, zkSync leaped to second place driven by a single Tradable project, while Stellar entirely relies on the Franklin Templeton BENJI fund (with a scale of $455.9 million) to occupy third place. Although the on-paper RWA data for both public chains is impressive, their structural deficiencies cannot be ignored: lack of asset diversity and dependence on single projects.

BENJI's Composition, screenshot from RWA.xyz

As demonstrated by zkSync and Stellar's ecosystem characteristics, most L2 networks currently face the challenge of insufficient ecosystem diversity - their RWA market value is highly dependent on 1-2 core projects. For instance, Arbitrum: out of the $256 million total market value, BENJI contributes $111.9 million (43.7%), and Spiko occupies $93.5 million (36.5%), together monopolizing over 80% of the market value; Polygon shows a similar distribution pattern, with core market value concentrated in two major projects: Spiko and Mercado Bitcoin.

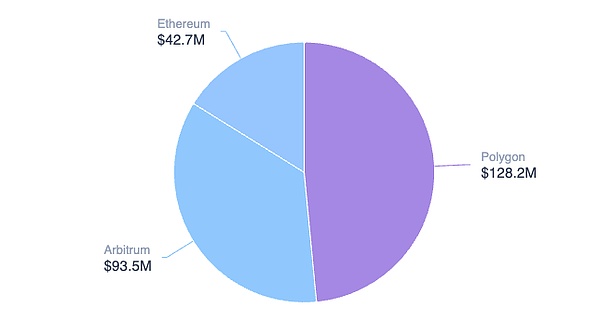

Spiko's Composition, screenshot from RWA.xyz

Expanding the perspective to the entire L2 ecosystem, RWA value and market share across networks show significant differentiation (see table below). Except for zkSync, only Polygon and Arbitrum have formed substantial scale effects, with other L2s still in early development stages. The success of Polygon and Arbitrum highly depends on the single driving force of Spiko - this project contributes about one-third of the total RWA value in both networks.

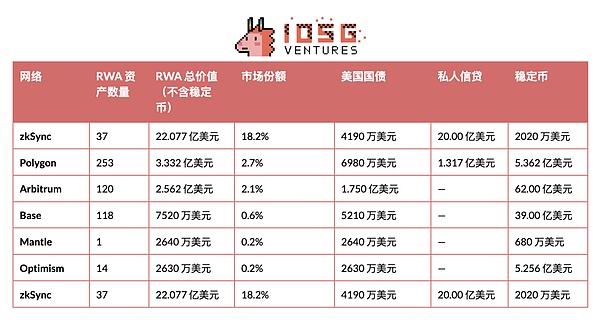

RWA.xyz, IOSG

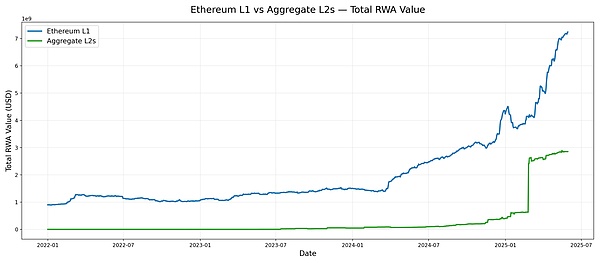

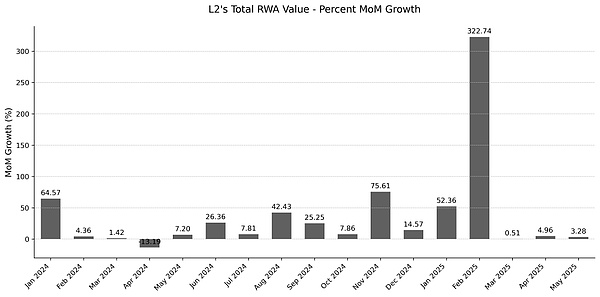

Looking at the overall RWA market value evolution of Layer-2 networks, its growth cycle is not entirely synchronized with Layer-1: it did not start growing in mid-2024. zkSync's access to the Tradable project brought a $2 billion market value growth. But even excluding this influence, the L2 growth trend is still established - since September 2024, L2 networks have maintained double-digit month-on-month growth. In contrast, the previous stage showed sporadic and weak RWA expansion. In summary, the end of 2024 marks a turning point in L2 ecosystem RWA development: entering a robust growth cycle.

RWA.xyz, IOSG

Etherealize: A New Engine for Ethereum RWA

(The rest of the translation continues in the same manner, maintaining the specific terminology as requested.)Ethereum's RWA Strategic Moat

First-Mover Advantage

Traditional financial institutions' decision-making processes differ from DeFi: regulatory review, pilot verification, and Proof of Concept (PoC) significantly extend deployment cycles. In the early stages, institutions typically adopt a cautious strategy, initiating expansion only after pilot results are validated. Although top Ethereum project BUIDL dominates, it still took nearly a year of accumulation before experiencing explosive growth. Ethereum's core advantage lies in its ecosystem's early positioning—having completed experimental collaborations with multiple top financial institutions before the RWA wave emerged.

Ecosystem Accumulation

Beyond institutional cooperation, RWA ecosystem maturity requires long-term sedimentation. Ethereum maintains its leadership position by:

Breadth: Covering diverse asset issuers and protocol architectures

Depth: Multiple projects breaking through billion-dollar market capitalization, forming scale effects

The integration of traditional finance and DeFi continues to deepen. Most RWA projects prioritize deployment on Ethereum mainnet, directly utilizing mature decentralized lending, market-making, and derivatives protocols to enhance capital efficiency. Recent examples include Ethena using BUIDL as 90% of USDtb stablecoin reserves. The 'GENIUS Act' mandating stablecoin reserves to shift towards US Treasury bonds is driving the fusion of US Treasury bonds, on-chain Treasury products, and stablecoin protocols. Simultaneously, mainstream DeFi protocols are incorporating BUIDL into their core collateral system.

Ethereum maintains an advantage in RWA liquidity: leading in active addresses, token varieties, and liquidity depth. While Layer2 ecosystem has collaboration mechanism uncertainties, it remains the core expansion path.

Security

Security is the cornerstone of the RWA ecosystem, with smart contract technological maturity being crucial. As RWA project logic becomes more complex, smart contract requirements increase. In May 2025, the Cetus protocol on Sui chain was hacked (losing $223 million), exposing fatal risks of oracle manipulation and contract vulnerabilities. Although $162 million was recovered through on-chain freezing, such passive emergency mechanisms highlight risk management limitations. In contrast, Ethereum's core advantage lies in its more decentralized architecture, reliable operational record, and thriving developer ecosystem.

Technical Evolution

Ethereum's technical roadmap will accelerate RWA development. First, improving L1 performance to bridge core gaps with high-performance public chains. Second, promoting L2 interoperability and focusing on the application layer to connect traditional finance with on-chain RWA.

Simultaneously, Ethereum's privacy roadmap strengthens security standards and privacy protection mechanisms (such as integrating privacy tools into mainstream wallets, simplifying anti-censorship transaction processes), providing guarantees for RWA transactions and constructing an asset confidentiality system meeting institutional requirements.