Written by Tia, Techub News

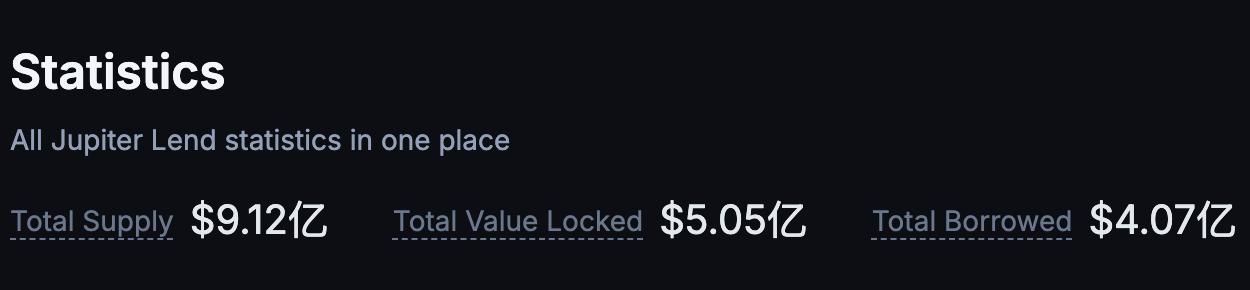

Less than 24 hours after its launch, deposits exceeded $500 million; just a week later, this figure rapidly jumped to $912 million. Jupiter Lend's successful start in the Solana lending market undoubtedly redefined the scale of the capital influx. Many established DeFi protocols often take months or even years to accumulate similar capital volumes. Jupiter Lend's rapid market explosion is inseparable from the technical support of its partner, the Fluid Protocol.

Solana has long been renowned for its leading DEX trading volume, but it has inherent weaknesses in lending, with a small market size and low user confidence, earning it the nickname "the poor man's money market." The powerful alliance between Jupiter and Fluid aims to fill this gap. Through Jupiter Lend, Jupiter leverages its deep foundation and user network within the Solana ecosystem, while Fluid leverages its successful experience integrating DEX and lending in the EVM market to provide the underlying technical architecture and liquidity solutions. Together, these two platforms create a truly robust environment for large-scale lending and borrowing for limited partners and users.

Fluid's design logic suggests it's more than just a single underlying tool for a single product; it has the potential to become a cross-ecosystem liquidity infrastructure. Through its shared liquidity layer and innovative mechanisms like Smart Debt, it has already demonstrated its ability to improve capital efficiency in the EVM market. The collaboration with Jupiter and the introduction of this architecture to Solana not only addresses long-standing lending shortcomings but also demonstrates Fluid's potential to scale horizontally across multiple public chains, becoming the foundation for diverse financial ecosystems.

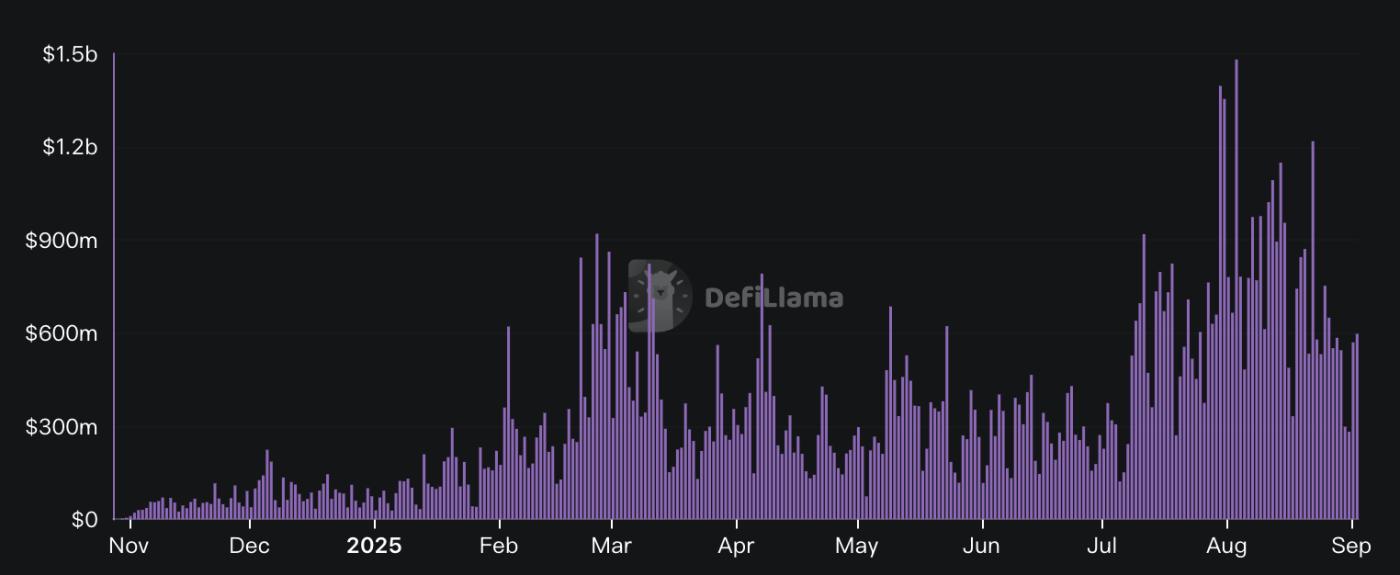

Even before partnering with Jupiter to launch Jupiter Lend, Fluid's performance was already impressive. From a lending perspective, Fluid was still several orders of magnitude behind the leading AAVE. However, from a DEX perspective, Fluid performed quite well, at one point surpassing Uniswap in 24-hour trading volume.

What is Fluid?

The Fluid Protocol isn't a single lending platform or exchange, but rather a combination of both. Its core concept lies in its shared liquidity layer: tightly integrating lending and decentralized exchanges into a single liquidity pool, avoiding the inefficient fragmentation of funds across different protocols and scenarios found in traditional DeFi models.

In most lending protocols, the lending logic is simple: users deposit assets and earn interest distributed by the platform. However, Fluid is different. It restructures lending itself into a shared liquidity layer.

By using lending liquidity as shared liquidity, Dex solves the cold start problem. Liquidity like Curve requires subsidies to attract LPs, while Fluid can cold start without subsidies.

Siphoning Liquidity: Smart Lending & Smart Collateral & Smart Debt

Fluid offers not only simple lending but also Smart Lending. Instead of depositing a single asset, you deposit a pair of tokens. This isn't just a "deposit," it's also providing liquidity for Fluid's DEX. This allows you to earn not only regular deposit interest but also transaction fees (Liquidity APR and Trading APR). The trade-off is potential Impermanent Loss, but currently, the primary supported pairs are stablecoins, which offer minimal volatility and negligible Impermanent Loss.

After shared liquidity solves the Dex cold start problem, Smart Lending can in turn provide a second subsidy to Lending users by using Dex transaction fees as subsidies, thereby attracting more users to engage in Lending.

The same approach extends to the Borrow module. In addition to conventional lending, Fluid also offers a more flexible "Smart" model. In Smart Collateral, collateralized assets no longer sit idle; instead, they enter the liquidity pool as LPs, earning fees while staking.

In the Smart Debt model , even the debt you lend out can be counted as LP shares and continue to generate transaction fee income. This means that in Fluid, even debt can become a tool to improve capital efficiency.

In a typical LP process, two tokens, A and B (e.g., ETH and USDC), are deposited into an AMM pool. When others trade the two tokens, the LP earns a commission. However, in a Smart Debt scenario, you don't deposit assets; instead, you lend A and B (e.g., -1000 A, -1000 B). This is recorded as a negative LP position on the ledger. When others trade, the debt position in the pool also changes with each trade.

For example, if a user exchanges 100 A for 100 B, your position changes from -1000/-1000 to -900 A / -1100 B.

Essentially, the amount of borrowed debt, like LPs, adjusts dynamically based on trading. When you eventually repay the debt, the amounts of A and B you need to return may differ from when you borrowed. If market prices are favorable, you may be able to repay more easily than expected. If they are unfavorable, your debt may increase, requiring more repayments. Throughout this process, transaction fees are still included in your LP share of the debt. Therefore, your debt is passively earning fees, which can offset a portion of the debt cost.

Smart Collateral and Smart Debt, while only minor changes, are highly attractive to both LPs and borrowers. Smart Debt can generate additional revenue for lenders, lowering their loan interest rates. Meanwhile, Smart Collateral can also increase the yield on users' collateral. This trade-off significantly reduces borrowing costs for users.

Highly efficient liquidation mechanism

Fluid's liquidation mechanism is orders of magnitude more efficient than traditional lending protocols. In traditional protocols, liquidation is peer-to-peer—liquidators must identify specific user positions that trigger risk and then liquidate those positions individually. This requires liquidators to track all positions and must either raise their own funds or initiate flash loan, creating a high barrier to entry and making it suitable only for professional liquidation bots.

In Fluid, however, all "bad debts" are pooled into a single "bad debt pool." Liquidators (or even ordinary traders) don't monitor specific positions; instead, they interact directly with this pool, effectively buying and selling bad debts within a trading pair, much like trading within the active liquidity range in Uniswap v3. Because bad debts are packaged as AMM-like liquidity, DEX aggregators (such as 1inch and Paraswap) can directly route users' regular transactions to the liquidation pool for liquidation. This design not only improves market efficiency but also significantly expands the scope of liquidation entities and the cost of liquidation.

Liquidators no longer need a massive clearing infrastructure—running full nodes and tracking positions across the entire network—which further lowers the barrier to entry and makes the market more decentralized. Simply accessing the bad debt pool allows for easy participation in liquidation.

This allows Fluid to offer very low liquidation penalties (the fees users pay to liquidators when liquidating). While mainstream lending protocols typically offer liquidation penalties of 5–10%, Fluid’s liquidation penalties can be as low as 0.1%, reducing user losses by 50–100 times.

Fluid liquidations also have very low gas costs. Since liquidations don't require complex arbitrage by liquidators and are handled natively, this significantly reduces gas costs. Overall, Fluid's Vault protocol liquidations only require approximately 150k gas, while other protocols often require 300k–1M gas. Furthermore, Fluid can liquidate any number of positions simultaneously in a single transaction, with virtually no additional gas costs. The same operation in other protocols requires multiple transactions, with linearly increasing gas costs.

Fluid's "partial liquidation" logic also avoids over-liquidation in traditional lending protocols. While protocols like Aave and Compound typically liquidate in batches, for example, liquidating a maximum of 50% of a position at a time, liquidators, driven by profit, may sell far more collateral than is needed to restore the position to health in a single liquidation, often resulting in over-liquidation. Fluid, on the other hand, only liquidates to the Liquidation Threshold ("safety zone"). The system calculates the collateralization ratio and risk level of a user's position in real time. When a position falls below the liquidation threshold, Fluid calculates the minimum collateral required to return to the safe zone. Liquidations only involve selling this small portion of assets (most liquidations liquidate closer to 5%). This portion of assets goes into a bad debt pool, eliminating the need for liquidators to monitor positions. Liquidation execution is logical and modular, rather than relying on manual judgment.

Since only necessary assets are liquidated, the ecosystem also benefits significantly. If all users in the ecosystem use the Vault protocol to manage their debt positions, the negative externalities caused by forced sell-offs and ripple effects can be reduced by 5-10 times, making the entire ecosystem more efficient and stable.

Buyback

Since Dex does not need to provide incentives to LPs and a portion of transaction fees will flow into the Fluid treasury, Fluid also plans to use this portion of funds for buybacks. The proposal was released to the community for discussion on August 20.

The proposal proposes three buyback models: 1. Model 1 is a dynamic buyback based on FDV. In this model, the percentage of revenue allocated to buybacks will depend on FLUID's FDV. If the FDV is below $500 million, 100% of revenue will be used for buybacks. As the FDV increases, the allocation to buybacks will decrease according to a specific function curve. 2. Model 2 is a buyback based on the 30-day time-weighted average price (TWAP). If the current price is below the 30-day TWAP, 100% of revenue will be used for buybacks; if the current price is above the 30-day TWAP, no buybacks will be made. 3. Model 3 is a hybrid mechanism. In bull markets, the protocol minimizes buybacks and retains revenue. In bear markets, the function curve of Model 1 will be applied to adjust the buyback size based on FDV, ensuring more aggressive buybacks when the token is severely undervalued. 4. The proposal also supports the option of not having buybacks, retaining more revenue for growth and reinvestment.

Fluid DEX v2

Following the launch of Jupiter Lend, Fluid will soon release version 2. The core of Fluid DEX v2 is a singleton contract built on top of the Fluid liquidity layer. This unified structure enables infinite composability, significantly improves capital efficiency and gas usage, and allows cross-collateralization to expand the inclusion of long-tail assets.

DEX v2 will support four main DEX types at launch: DEX v1 Smart Collateral, DEX v1 Smart Debt, Smart Collateral Range Orders, and Smart Debt Range Orders.

The latter two types of DEX V2 allow limited partners to provide liquidity at different price points. Smart Debt and Smart Collateral can optionally create range orders, allowing them to be placed anywhere on the curve when providing liquidity. For Fluid, which already offers amplified capital efficiency, the integration of range orders will make it even more attractive to professional limited partners.

Furthermore, DEX v2 is built with modularity and permissionless scalability in mind. In the future, Fluid will enable fully permissionless smart collateral and smart debt, allowing users and protocols to create any type of collateral and debt positions.

summary

For Fluid, if it wants to truly expand its scale, having a strong product architecture is one aspect of competition, but on the other hand, having a strong partner/distribution network will bring great ecological support to the protocol.

Fluid has already demonstrated strong product competitiveness. Its partnership with Jupiter Lend has successfully validated Fluid's potential for potential distribution networks. As more protocols integrate with it, we may see a new DeFi liquidity network gradually take shape across different chains.