Author: Dong Jing Source: Wall Street News

Global markets are gripped by a dangerous collective anxiety, and perhaps only Nvidia can break this deadlock. The $4.5 trillion chip giant will release its third-quarter earnings report after the US stock market closes on Wednesday (early Thursday morning Beijing time), a report that will determine the direction of global markets in the final weeks of the year.

Currently, market anxiety is spreading: from Bitcoin to tech stocks, from gold to government bonds, from private equity to corporate bonds, almost all asset classes are experiencing selling pressure. Against this backdrop, investors are focusing their attention on Nvidia, a move driven by both hope and desperation. The company's performance will directly reflect the true returns on the tech giants' hundreds of billions of dollars invested in AI.

Currently, Wall Street analysts are generally optimistic about Nvidia's upcoming earnings report, expecting both net profit and revenue to grow by more than 50%.

Analysts point out that if investors are satisfied with Nvidia's third-quarter results and fourth-quarter guidance, bulls will drive the market to an optimistic close; otherwise, the market may face a deeper correction. As Wall Street insiders have said, "This is a report where the market moves in tandem with Nvidia."

It's worth noting that amidst a highly concentrated market risk, Nvidia, as the largest constituent stock in the S&P 500 and the center of AI trading, is of unprecedented importance in terms of its performance. However, some market analysts point out that while concentration risk can be exciting during market upturns, it can turn into a nightmare during downturns.

Nvidia: The only savior in the current market?

A more somber mood is spreading through the market, and only Nvidia can break the gloom.

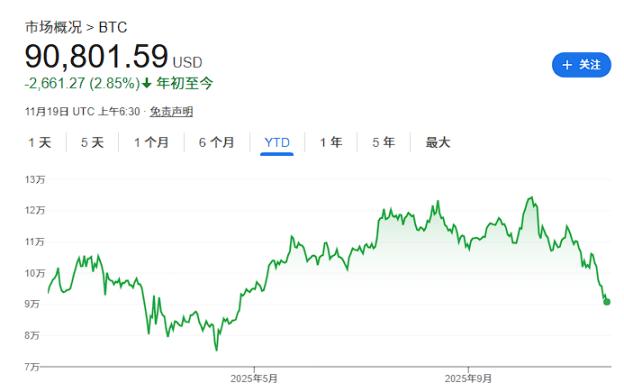

The most speculative sectors in the financial markets are currently under pressure. Bitcoin—perhaps the purest measure of speculative fervor—has fallen 29% from its peak and is now in negative territory for the year.

Companies that hold and store Bitcoin have seen their stock prices plummet. Strategy (formerly MicroStrategy), the largest of these, has seen its stock price fall by more than 30% this year, and more than 50% from its summer high.

The stock prices of unprofitable U.S. tech companies have been sluggish for weeks, indicating that investors, even risk-taking retail investors, are beginning to lose patience with the hype.

Even more unsettling is that the turmoil isn't limited to the more aggressive sectors of tech stocks. Meta, Facebook's parent company, has seen its share price flat this year and has wiped out a quarter of its market capitalization since August, as investors grow uneasy about its seemingly endless spending on artificial intelligence.

While pressures in the private equity market are not always easily detected, a series of defaults in the past few months have already rattled the market. An index compiled by Absolute Strategy Research that tracks companies like Blackstone and KKR has fallen 13% this year, a stark contrast to the S&P 500.

Analysts point out that the sharp rise in benchmark U.S. stock indices has clearly masked numerous problems. Beneath the surface, investors are becoming increasingly difficult to please. A significant risk is that this could escalate into a full-blown sell-off of the market, which has been brimming with hope since the spring.

In this market environment, the importance of Nvidia's financial reports is becoming increasingly prominent.

Despite recent sell-offs, Nvidia's stock price is still up 35% this year, more than double the Nasdaq 100's gain of about 17%.

Meanwhile, the decline in share price makes the company's valuation relatively attractive. Nvidia's current forward price-to-earnings ratio is approximately 29 times, well below its 10-year average of 35 times, and slightly higher than the Nasdaq 100 index's level of approximately 26 times.

"Given Nvidia's growth rate, a P/E ratio of 30 doesn't seem unreasonable at all," said Scott Martin, chief investment officer at Kingsview Wealth Management.

Wall Street analysts expect Nvidia's net profit and revenue to both grow by more than 50% in the upcoming earnings report.

Data compiled by Bloomberg shows that Microsoft, Amazon, Google, and Meta together account for more than 40% of Nvidia's sales, and their AI spending is projected to grow by 34% to $440 billion over the next 12 months. Therefore, the company's performance will directly reflect the real return on its hundreds of billions of dollars in AI investments.

Analysts point out that if investors are satisfied with Nvidia's third-quarter results, bulls will drive the market to an optimistic close; otherwise, the market may face a deeper correction. As Martin said:

"This is a earnings report where Nvidia's performance determines the market's direction. If Nvidia's performance is strong, with expected sales and larger-scale activities, then everything will be fine."

Wall Street bets on earnings reports "exceeding expectations again".

Wall Street investment banks are generally optimistic about Nvidia's earnings report.

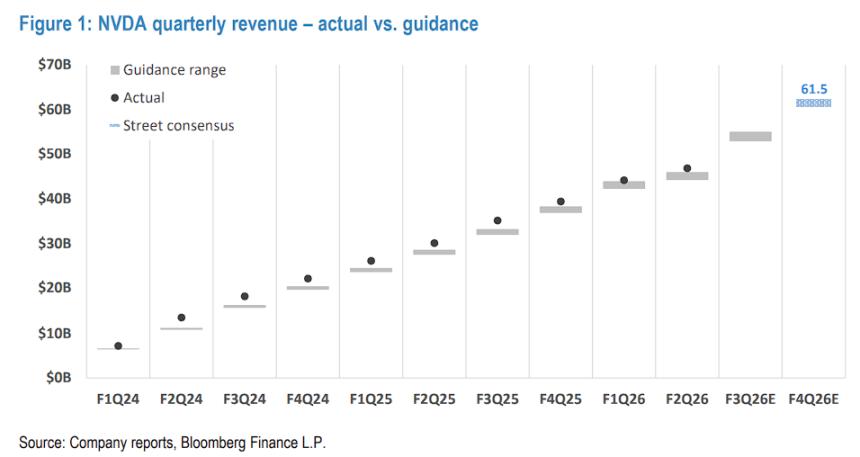

According to Hard AI, JPMorgan Chase stated in its latest research report that Nvidia is highly likely to repeat the "beat-and-raise" scenario. The bank expects third-quarter revenue to exceed the market consensus of approximately $55 billion and has given a performance guidance of $63 billion to $64 billion, significantly higher than the market expectation of $61.5 billion.

JPMorgan Chase states that Nvidia's current growth rate is not driven by demand, but rather by the capacity limits of its massive supply chain. AI computing power demand continues to significantly exceed supply, and Nvidia's largest customer base, including hyperscale cloud service providers, emerging cloud computing companies, and AI labs, still faces computing power bottlenecks.

Supply chain capacity is expanding rapidly. JPMorgan Chase expects Blackwell/Blackwell Ultra rack shipments to achieve approximately 50% quarter-over-quarter growth in the third quarter, reaching approximately 10,000 racks, and this growth momentum is expected to continue into the fourth quarter. The bank projects Nvidia's total rack shipments for fiscal year 2026 to reach 28,000 to 30,000 units.

More importantly, according to information disclosed by Nvidia at its GTC conference in October, its order backlog for calendar year 2026 has exceeded 70,000 racks, surpassing its maximum production capacity for the entire year of next year. Based on this, JPMorgan Chase maintains its "overweight" rating on Nvidia with a target price of $215.

JPMorgan Chase also stated in its research report that investors should pay close attention to how management responds to four core concerns:

First, there's the production ramp-up trajectory of Blackwell/Blackwell Ultra, especially the rate of capacity expansion in the first half of 2026 (i.e., the first half of Nvidia's fiscal year 2027).

Secondly, there's the sustainability of AI spending. A recent report by JPMorgan Chase's global team concluded that funding for AI will remain ample through 2030.

Thirdly, there is the impact of power constraints. Globally, approximately 120 gigawatts of data center power capacity is expected to come online over the next five years, but the delivery cycle for new natural gas turbines has surged to 3-4 years, while the construction cycle for nuclear power plants exceeds 10 years, making power a real bottleneck.

Finally, there's the impact of component cost inflation on gross margin. JPMorgan believes that rising LPDDR memory prices pose a greater pressure point than HBM memory. Nevertheless, the bank believes Nvidia is still capable of achieving its mid-range gross margin target of 70% by the end of fiscal year 2026.

According to TrendForce, Morgan Stanley is even more optimistic, raising its target price for Nvidia to $220. Analyst Joseph Moore stated in a report on November 14th that industry research shows a substantial acceleration in demand, Nvidia has fully resolved early rack-related issues, and demand continues to surge.

Morgan Stanley's industry research shows that demand signals from Nvidia's customers and suppliers in the third quarter both point to accelerated growth, which contrasts sharply with the market's general expectation that Nvidia's various growth indicators have peaked.

At the customer level, third-quarter capital expenditures for cloud services are expected to increase by $142 billion, with the four major hyperscale cloud service providers each increasing their expenditures by more than $20 billion. The current dollar growth rate compared to 2025 is $115 billion, 60% higher than a quarter ago.

From a supplier's perspective, ODM manufacturer Quanta expects its AI server revenue to accelerate in the first quarter of 2026, with year-on-year growth exceeding 100% in 2026. To support this demand, Quanta plans to double its AI server production capacity next year, as order visibility extends into 2027.

Morgan Stanley raised its revenue forecast for Nvidia's October quarter to $55 billion from $54.4 billion, and its revenue forecast for the January quarter to $63.1 billion from $61.2 billion. Analysts pointed out that achieving $8 billion in sequential growth in both the October and January quarters would set a new industry record.

However, deep-seated concerns in the market are difficult to dispel.

Despite Wall Street investment banks' generally positive outlook on Nvidia's earnings, market concerns about AI investments are deepening, and these concerns are already reflected in investor behavior.

As previously reported by Wall Street News, Peter Thiel's hedge fund sold all of its Nvidia shares in the third quarter. SoftBank Group also exited its holdings to fund other AI investments.

Michael Burry, known as the "Big Short" for short the real estate market during the 2008 financial crisis, has disclosed that his Scion Asset Management has purchased put options on Nvidia. Burry warned that there is a bubble in AI.

Meanwhile, a Bloomberg analysis of 909 hedge fund 13F filings found that the number of funds increasing and decreasing their Nvidia positions was almost equal in the three months ending September 30. Michael O'Rourke, chief market strategist at Jonestrading, stated:

"These players in the AI field have been relentlessly raising the bar for expectations. Now they not only have to deliver on their numbers, but they also have to continue to meet the market's ever-increasing expectations. This is a dangerous game for publicly traded companies."

Moreover, a key risk currently facing the market is that these figures could become unreliable if major AI spenders, particularly the privately held OpenAI, are forced to scale back their commitments.

Melissa Otto, head of technology research at Visible Alpha, noted, "I think what the market is really grappling with right now is the total potential market size of all these AI infrastructures."

Jake Seltz, portfolio manager at Allspring Global Investments, said the firm holds a large position in Nvidia and he will be closely watching the next quarter's guidance. While revenue guidance may exceed market expectations, "it's hard to know how conservative they will be in their guidance."