Author: blocmates

Compiled by: Luffy, Foresight News

If you've been active in the cryptocurrency market recently, you've probably noticed a trend: the airdrop craze is gradually fading, initial coin offerings (ICOs) are making a strong comeback, and the market is shifting from a venture capital-led financing model to decentralized fundraising.

ICOs are not a new phenomenon; some of the most popular cryptocurrencies (such as Ethereum and Augur) completed their initial offerings through ICOs. However, we must acknowledge that after a long "quiet period" from 2022 to 2024 (during which project financing was mostly completed through closed-door venture capital transactions), ICOs experienced a strong resurgence in 2025.

Why is ICO making a comeback?

One argument supporting the resurgence of ICO-style fundraising is that since the initial ICO boom of 2014-2018, the number of cryptocurrency participants has more than tripled, representing a compound annual growth rate of 4.46%, and the average level of expertise among participants has significantly improved. Furthermore, the increased supply of stablecoins has naturally expanded the pool of available funds, making more people willing to purchase discounted tokens before Token Generation Events (TGEs).

While this argument is appealing, increased market participation is not the primary driver of the ICO mechanism's resurgence. To find the core reasons for the recovery, we need to examine the inherent flaws in the current financing model.

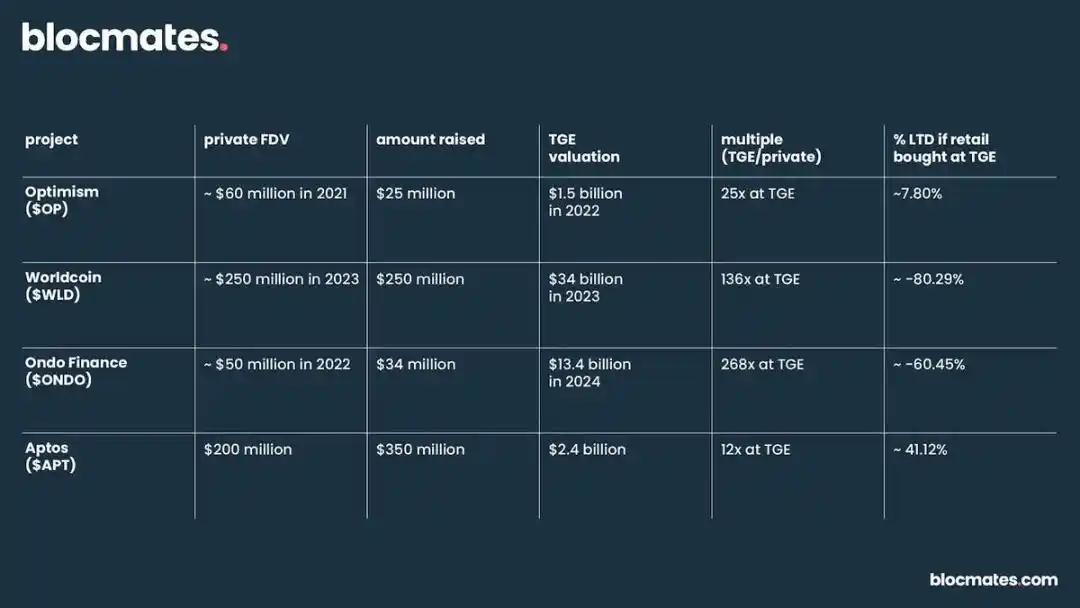

A close look at the market cycle from 2022 to 2024 reveals that many projects raised funds from venture capital funds with low total diluted value (FDV), but by suppressing the initial circulating supply, they made the tokens achieve a much higher FDV at the time of public listing than at the time of fundraising.

The following are some case studies from 2022-2024:

As the table shows, insiders captured the majority of the profits, severely compressing the profit margins for retail investors.

In layman's terms, profit opportunities in Altcoin are mainly concentrated in the hands of insiders. Retail investors either buy tokens at inflated prices or sell them quickly after receiving airdrops. This is largely because airdrops are often seen as "free money," which triggers immediate selling pressure.

This situation has led to widespread fatigue among retail investors: as the risk-reward ratio continues to deteriorate, they are gradually losing confidence in traditional Altcoin investments.

Subsequently, retail investors turned to memecoin, an asset with low barriers to entry, high volatility, and no venture capital involvement, which fueled the memecoin craze and the rapid rise of memecoin issuance platforms.

Ultimately, this has led to a growing misalignment of interests among retail investors, project teams, and venture capitalists, with increasingly divergent incentive goals among the three parties:

- Retail investors crave a fairer entry opportunity.

- Project owners need sustainable communities, not short-term speculation.

- Venture capitalists often pursue asymmetric returns in the early stages.

The resulting tensions have created an urgent need for a new model to recalibrate the incentive culture of the entire ecosystem, and the resurgence of ICO-style financing is a manifestation of this shift.

The appeal of ICOs lies not only in providing an alternative financing method, but also in their clearer incentive structure, which allows retail investors to participate on a fairer basis.

Reasons why ICOs might replace airdrops

Based on the above reasons, we have reason to believe that the market incentive culture may shift to a "benefit-sharing" model, replacing the traditional "task-for-reward" airdrop model with ICO discounts.

Signs of this are beginning to emerge. MegaETH and Monad have both used a portion of their previous venture capital investments for public sales. While these moves are not pure ICOs, distributing tokens to the public based on venture capital valuations is a step in the right direction.

ICOs are generally seen as a more natural token distribution method that emphasizes "shared interests": participants invest their own funds at a benchmark valuation, which can be a single round of financing or a tiered structure with multiple pricing levels.

In theory, this could create a stronger psychological and economic bond between users and the project.

Because participants purchase tokens directly rather than acquiring them for free, they are generally more inclined to hold them for the long term. This helps to reverse the recent trend of continuously shortening on-chain asset holding times.

Furthermore, ICOs are expected to reshape the profit potential of the Altcoin market: public fundraising is usually more transparent, with circulating supply and valuation readily apparent, and its FDV is often more reasonable compared to venture capital-driven token models.

This structure increases the likelihood of early retail participants gaining substantial profits, rather than competing with insiders who enjoy significant discounts for allocated shares.

In contrast, many airdrop projects, due to poor incentive design, have fostered a widespread "receive and sell immediately" culture. ICOs, on the other hand, offer a more rational and sustainable option in terms of both token distribution and early community building.

The Rise of Early-Stage Funding Platforms and Its Implications for ICOs

Last month, the cryptocurrency industry witnessed a major acquisition: Coinbase acquired Echo, an on-chain funding platform, for $375 million. This acquisition included Echo's Sonar product—a tool that allows anyone to launch a public token sale.

At the same time, Coinbase also launched a native in-app launch platform, with its first partner project being Monad.

Besides Echo and Coinbase, early-stage fundraising platforms have become a trend. Kaito launched its dedicated launch platform, MetaDAO, redefining the meaning of ICOs.

MetaDAO is particularly noteworthy. The platform's emergence clearly reflects market fatigue with the "insider-driven, high FDV issuance" model. Its goal is to help projects achieve long-term growth through early-stage launches with high-liquidity ICOs.

This indicates that the market is fully prepared for the return of ICOs, but not any form of ICO. Rather, it refers to a well-planned and executed fundraising model that can create a positive alignment of interests between the team, the community, and the overall market.

How to create a good layout?

To be fair, as we have previously pointed out, the resurgence of ICO fever reflects a rethinking of incentive culture in the market, the core of which is to create a fairer opportunity for retail investors.

This means that project teams and retail investors need to align their interests and cultivate a more resilient community composed of active users and steadfast token holders. In fact, this also foreshadows the possible end of the "free token" era.

Looking back at some successful airdrops that have had a profound impact on the ecosystem (such as HYPE), we can see room for improvement in distribution design:

Taking Hyperliquid as an example, genuine users (rather than speculative "miners") participate by paying transaction fees and taking real risks, and the rewards they receive are truly tied to the product's success.

This case demonstrates that when the incentive structure is designed properly, retail investor participation can be both meaningful and sustainable, rather than a short-lived speculative activity.

We believe this idea will permeate the operating model of ICOs: in the future, ICOs may offer discounts to users with "more mature and trustworthy on-chain behavior," thereby replacing traditional airdrop distributions.

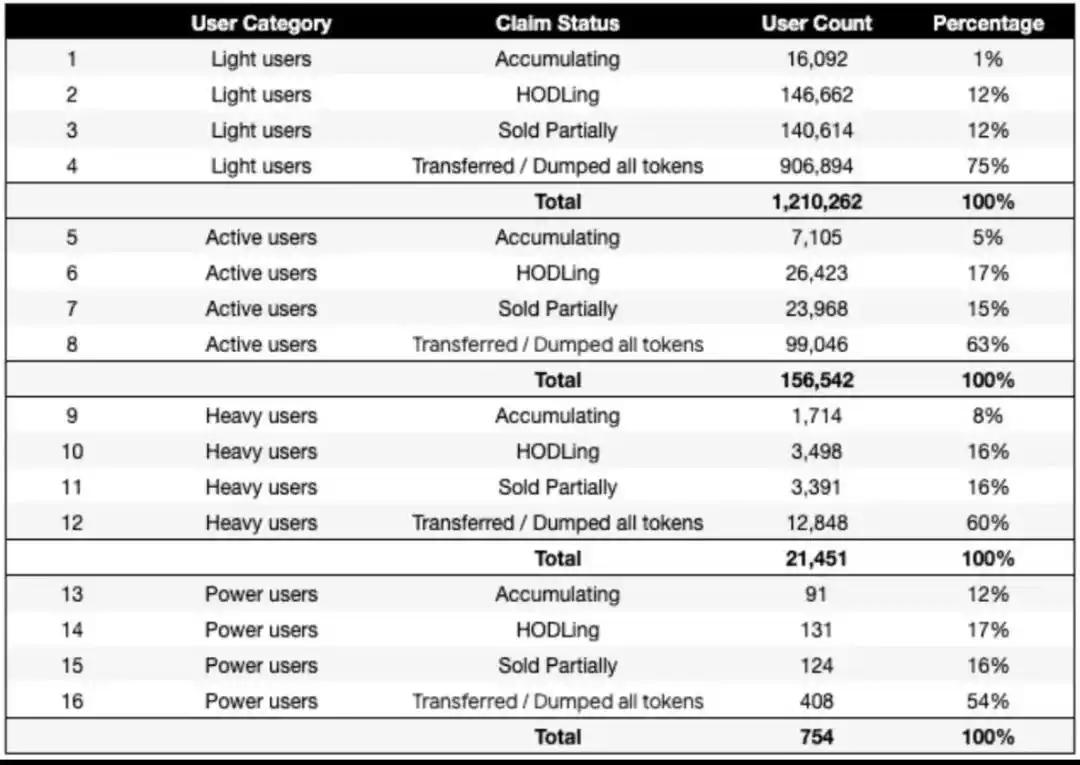

A set of data from 2024 is quite telling: after the tokens were airdropped, more than 80% of light users tended to sell them within 7 days, while the proportion of heavy users was only 55%.

To succeed in the envisioned future, participants need to develop a long-term mindset and adjust their actions accordingly.

This means cultivating user loyalty to specific wallet addresses to build credibility and demonstrate consistent, coordinated on-chain behavior.

Such activities may include meaningful on-chain activities such as trying out various protocols, deploying liquidity in liquidity pools, and contributing to public goods such as Gitcoin.

Despite differing opinions on projects like Kaito, we expect them to play a significant role in shaping the next phase of the market.

For example, the yap threshold, combined with verified on-chain behavior, could become a key criterion for ICO participation eligibility or discounted token allocation, rewarding participants who demonstrate sustained commitment and stake in the deal.

If the above model becomes the norm, one way to increase returns is to use products like INFINIT or Giza to allocate funds across multiple ecosystems.

While this approach may be less effective in scenarios where wallet age and historical behavior are given high weight, its advantages will still be significant if on-chain activity is used as the sole criterion for judging ICO participation or discount allocation.

Potential problems and challenges

ICOs still face many challenges in becoming the default method for fundraising and reward distribution in the cryptocurrency industry.

A key challenge is that, as with venture capital-led fundraising, a poorly designed ICO token economic model can lead to failure.

If a project prices its tokens too high, especially relative to current market valuations (which are often influenced by low circulating supply and high FDV manipulation), then those tokens may still struggle to gain acceptance in the open market.

Furthermore, regulatory and legal considerations also pose significant obstacles. While regulatory transparency for cryptocurrencies is increasing in some jurisdictions, ICOs still operate in many gray areas in potentially high-capital regions.

These legal uncertainties could become a bottleneck to the success of an ICO, and in some cases, could even push projects that are struggling to gain sufficient attention back to venture capital firms.

Another interesting challenge facing ICOs is the possibility of market saturation. As multiple projects often raise funds simultaneously, participants' attention can be scattered, potentially diminishing overall enthusiasm for ICOs. This could lead to widespread "ICO fatigue," thereby inhibiting broad participation and market momentum.

In addition to these challenges, as the market may shift towards ICOs, projects have many other key considerations, including incentive coordination, community engagement, and infrastructure risks, all of which must be addressed to ensure sustainable success.

Conclusion

Currently, the market's demands are very clear: people crave fairer project issuance and a reduction in venture capital scams. The current state of the Altcoin market reflects this – spot holdings are decreasing, while perpetual contract trading volume is increasing.

We believe this clearly demonstrates that retail investors have largely abandoned long-term returns in favor of more speculative investment methods.

From the perspective of attention economics, this situation is even more serious: it not only harms the entire industry, but also hinders innovation.

The return of ICOs seems like a step in the right direction. However, it's unlikely to completely replace the airdrops we know, but rather to act as a driving force, fostering hybrid models where long-term stakes become central to any project's marketing strategy.