This article is machine translated

Show original

Understanding governance rights as contractual ownership is fundamentally flawed.

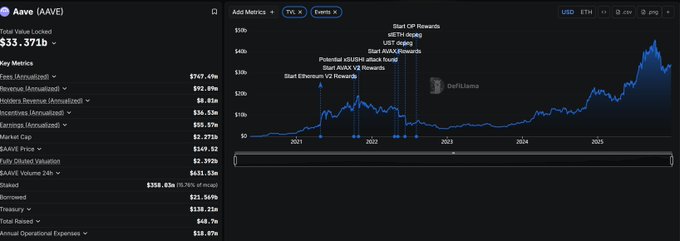

After reading the drama surrounding AAVE in the English-language timeline, and the even more dramatic retellings in the Chinese-language section, I thought AAVE was going to fail. But then I checked DeFillama and the TVL (Total Value Limit) was basically unchanged, indicating that zero AAVE users care. What does this say? A significant portion of DeFi users and communities are completely different. Some people therefore say, "Project teams don't need to issue tokens; equity is better."

From the perspective of a token holder, this sentiment is understandable. But if the project team fails to win in the market or liquidity, and hands over the entire project's IP and control to you, and you pass the test, now the project is yours—would you be happy?

This is the kind of haphazard reflection everyone had in 2018 about governance and ownership—they're not the same thing. Issuing cryptocurrency is completely different from the logic of equity; as I mentioned in my article about the Turkish lira yesterday, its ideal function is closer to a central bank's monetary policy toolbox, its purpose being to create a liquidity moat for its products. It's similar to how China has suppressed its exchange rate for years to maintain its export advantage.

When DeFi projects face competition:

1. Interest rate differentials can be quickly and cost-effectively created using tokens or token expectations.

2. Drive data, including volume, ranking, APY, etc., through a token Ponzi scheme.

3. By using external lending and derivative instruments for the coin, a low-cost financing channel can be formed, which can be scaled up and squeeze the market share of newcomers. An on-chain exchange token and derivative assets can, in extreme cases, support six sectors, including aggregators, lending, oracle, wealth management pools, and even spot DEX. Each of these can issue assets independently. Even if the LTV of an asset is only 30%, and the average FDV of an asset is 300 million, that is 540 million in liquidity. How can newcomers compete?

Yes, that's the logic behind @JupiterExchange. So guess why the central banks of most countries are called "central banks" instead of a decentralized power system?

The purpose of my research on the Turkish lira yesterday was to encourage everyone to re-examine the relationship between "coin, coin holder, and project team." For a project team that wants to do things well, simply holding onto the coin wholeheartedly isn't necessarily the optimal solution. Perhaps they'd prefer you to help them get the economic cycle going—just like Moutai distributors don't just stockpile inventory.

@cz_binance Update "If you can't hold on, you can't get rich" to "Buy when nobody's interested, sell when everyone's talking about it."

@heyibinance, the top influencer said, "If you're not bullish, you can short it."

What this actually reveals is a much deeper logic within the crypto ecosystem than what is literally said. Do you all understand it now?

It seems like aave first leeches off the community, then betrays them when it comes to splitting the profits, which is why he's getting all the criticism, haha.

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content