Compiled by: Block unicorn

Why would I hold stocks on the blockchain when I already own IBKR (the ticker symbol for Interactive Brokers LLC, a global electronic brokerage platform offering trading in stocks, options, futures, forex, and other assets)? Why should I mix my stock holdings with my crypto asset holdings?

These are all valid questions, and I believe the answers will become clearer over the next year. In this article , I will outline my views on the future direction of on-chain spot equities, particularly considering two recent developments :

Substantial improvement in the regulatory environment , and

The emergence of faster and cheaper large-scale blockchains has made the minting, transfer, and use of on-chain shares increasingly feasible.

Analogy of stablecoins

Stablecoins have become the most compelling example of bringing traditional off-chain assets into the blockchain. Most stablecoins are used to access the US dollar on-chain (although other currencies, such as the Euro, are also increasingly important), and their early adoption was driven by a specific user group: users already operating on-chain. For these users, stablecoins addressed their immediate needs. They facilitated transactions between crypto assets, allowed the storage of yields without offshore payments, and simplified peer-to-peer payments. Over time, more advantages have emerged, such as earning yields through stablecoin lending and products that pass on the underlying government bond yields to users, creating higher-yielding savings accounts.

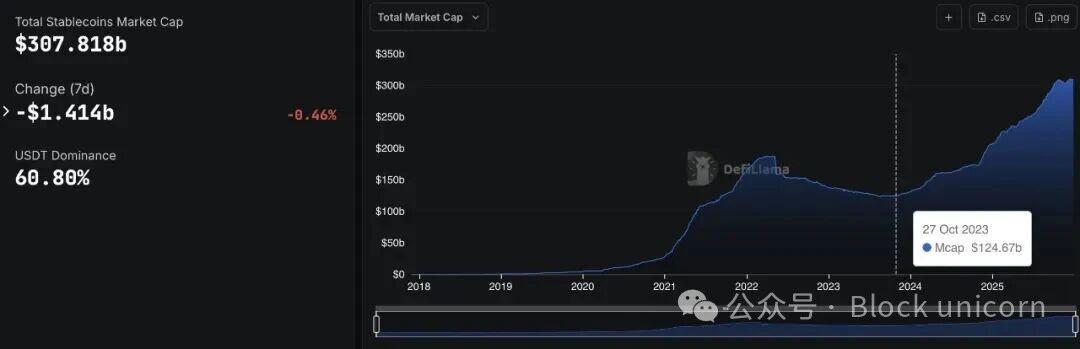

A recent shift is that stablecoins are no longer just a native tool of the cryptocurrency space. They are increasingly recognized as a more efficient, economical, and large-scale global dollar transfer mechanism. This shift has driven a significant increase in the supply of stablecoins. In 2021, the total market capitalization of stablecoins was approximately $26 billion. In the past year alone, their supply has grown from approximately $190 billion to over $300 billion, more than tenfold in less than five years.

Growth of circulating stablecoins - Defillama

This growth has spawned new business models such as Rain Cards, Felix Pago, and OpenFX, which utilize stablecoin platforms but do not position themselves as "cryptocurrency" products. In many cases, the abstraction layer of the blockchain is invisible to the end user.

Stablecoins offer a better, faster, and cheaper way to transfer and store US dollars. But what does this have to do with stocks?

Two key differences between on-chain spot stocks

The investment arguments for on-chain spot stocks are similar to those for stablecoins, but there are two key differences.

First, the growth of on-chain spot equities is closely correlated with the growth of stablecoins. As more individuals and institutions begin holding their preferred currencies (primarily USD) on-chain , it becomes increasingly natural to make more asset purchases on-chain. We are already seeing this phenomenon today: the users most likely to buy crypto-native assets are also those holding stablecoins. Bringing the unit of account on-chain inevitably pulls investment activity onto-chain as well .

If stablecoins fail (which I believe is unlikely), the potential market size (TAM) of on-chain spot equities will also shrink significantly. (Unless there is a broader collapse of the underlying fiat currency, in which case the overall value of equities may still exist, and the adoption of on-chain transactions may continue to accelerate, but this is a black swan event and is beyond the scope of this article.)

Secondly, on-chain spot equities not only bring convenience but also unlock new practical value. Their value proposition extends beyond faster settlement speeds or global accessibility . On-chain equities enable functionalities that most traditional brokerage users currently cannot truly benefit from, particularly in the lending and borrowing sectors.

In the lending sector, securities lending has become a massive business, but the majority of the economic benefits flow to intermediaries rather than end users . For example, Robinhood's Q3 2025 financial report showed that net interest income increased by 66% year-over-year to $456 million, primarily driven by interest-earning assets and securities lending. However, eligible users can only receive a maximum of 15% of the income generated from lending securities on the Robinhood platform. For reference, this is similar to the Felix protocol taking $85 from every $100 of interest lent by borrowers—undoubtedly an extremely high commission rate.

To give another example, Interactive Brokers earned approximately $314 million in revenue through securities lending in the third quarter of 2025 alone, but most of this revenue was not distributed to users. On Felix, making this revenue accessible to users is very simple: by configuring a Felix Vault on Felix Vanilla, users can lend out tokens such as HOOD, and other users can borrow them at any time without permission.

Stock-backed lending follows a similar pattern. On traditional brokerage platforms, margin trading requires application, approval, and strict loan-to-value (LTV) limits, and is typically limited to margin transactions. On-chain lending, however, with approved collateral, requires no permission (but is subject to sanctions), and borrowers have complete control over the borrowed funds.

Securities lending and mortgage lending are both large and mature markets. On-chain transactions make them cheaper, faster, and more accessible.

Open access?

Regarding spot stock trading, one point needs clarification: putting spot stocks on the blockchain is not primarily for the purpose of popularizing the US stock market; most individuals in developed economies already have access to securities accounts and such trading opportunities. The aim is to meet the growing demand for capital: namely, trading on the blockchain.

As capital continues to flow on-chain, spot equities offer a more convenient way to buy, hold, and use stocks. On-chain spot equities are a natural extension of the same forces that drove the adoption of stablecoins, forces that are now also applied to the stock market.