Author: RWA Group, Research Department, Peking University Blockchain Association; Group Leader: Owen Chen (X @xizhe_chan)

Group members: Huang Zhe, Zhang Kexin, Lionel, Alice D., Mo Junjie, Alan

summary

The Digital Asset Treasury (DAT) model is gaining popularity and evolving among listed companies globally. Particularly after the market correction in Q4 2025, the sustainability of this business model during a downturn has become a focus of market attention. This article, based on the market environment at the beginning of 2026, systematically dissects the operational mechanism of DAT companies, focusing on the dual dimensions of "financing structure × underlying currency" to deeply analyze the effective boundaries and potential risks of the "reflexive flywheel" in DAT companies.

The study points out that the DAT model is essentially proactive balance sheet management, with its value creation stemming from the synergy between asset-side returns (β) and capital-side operations (α). Regarding financing structure, the article demonstrates the high dependence of equity financing (such as ATMs and PIPEs) as the core driver of the flywheel on valuation premium (mNAV), and the maturity mismatch risk introduced by debt financing (such as convertible bonds) as a second-tier funding source while providing leverage efficiency. In terms of cryptocurrency selection, the article compares and analyzes the financing resilience of Bitcoin (BTC) due to its strong consensus, the compliance and transparency challenges of Ethereum (ETH) with its added interest-bearing attributes, and the aggressive liquidity transmission mechanism of smaller cryptocurrencies achieving "crypto-equity linkage" through SPAC channels.

Based on case studies from Strategy (formerly MicroStrategy), Core Scientific, and MARA, this paper proposes a sustainability assessment framework centered on "premium window—cash buffer—debt terms," and provides four trend predictions: First, the industry has entered a cross-cycle survival phase, where the key challenge lies not in book drawdowns, but in the liquidity pressure caused by companies' refinancing capabilities and debt repayment terms under a shrinking financing window. Second, valuation logic will shift from "channel premium" to "capability pricing." With the widespread adoption of compliant allocation tools such as spot ETFs, financing premiums for DAT companies will become scarcer and shorter-lived, and the differentiation in mNAV among companies will persist in the long term. Third, differences in underlying assets will further amplify corporate differentiation. BTC-DAT is more likely to form a financing anchor but is more sensitive to the pace of financing. The upper limit of ETH-DAT depends on the ability to continuously and clearly disclose the source of revenue and risk boundaries, and to establish a verifiable governance and execution record. Fourth, DAT will continue to be used as a capital market strategy, but the industry structure is likely to move towards concentration at the top and elimination at the bottom. This article provides a framework for DAT companies to assess sustainability during a downturn and offers a reference for the standardization evolution of the DAT industry.

Keywords : Digital Asset Treasury (DAT); Financing Structure; Currency Differences; mNAV; Sustainability Analysis

1. Introduction

DAT (Digital Asset Treasury) usually refers to the inclusion of crypto assets such as BTC and ETH in the balance sheet of enterprises (or DAO organizations) and their management and allocation in the form of "long-term reserves". Driven by the benchmark demonstration effect of Strategy (formerly MicroStrategy) and coupled with the support signal of the White House for the "Strategic Bitcoin Reserve", this strategy is gradually moving from case exploration to a wider range of listed companies' strategic options. The Bitwise report pointed out that as of Q3 2025, 172 listed companies worldwide held BTC, with a total holding of more than 1 million coins. [1] Therefore, based solely on the perspective of listed companies, the asset size of BTC-related DAT has exceeded US$100 billion (calculated according to the Bitcoin price at the time the Bitwise report was published); if other digital assets and unlisted corporate entities are further included, its potential coverage and size still have significant room for expansion.

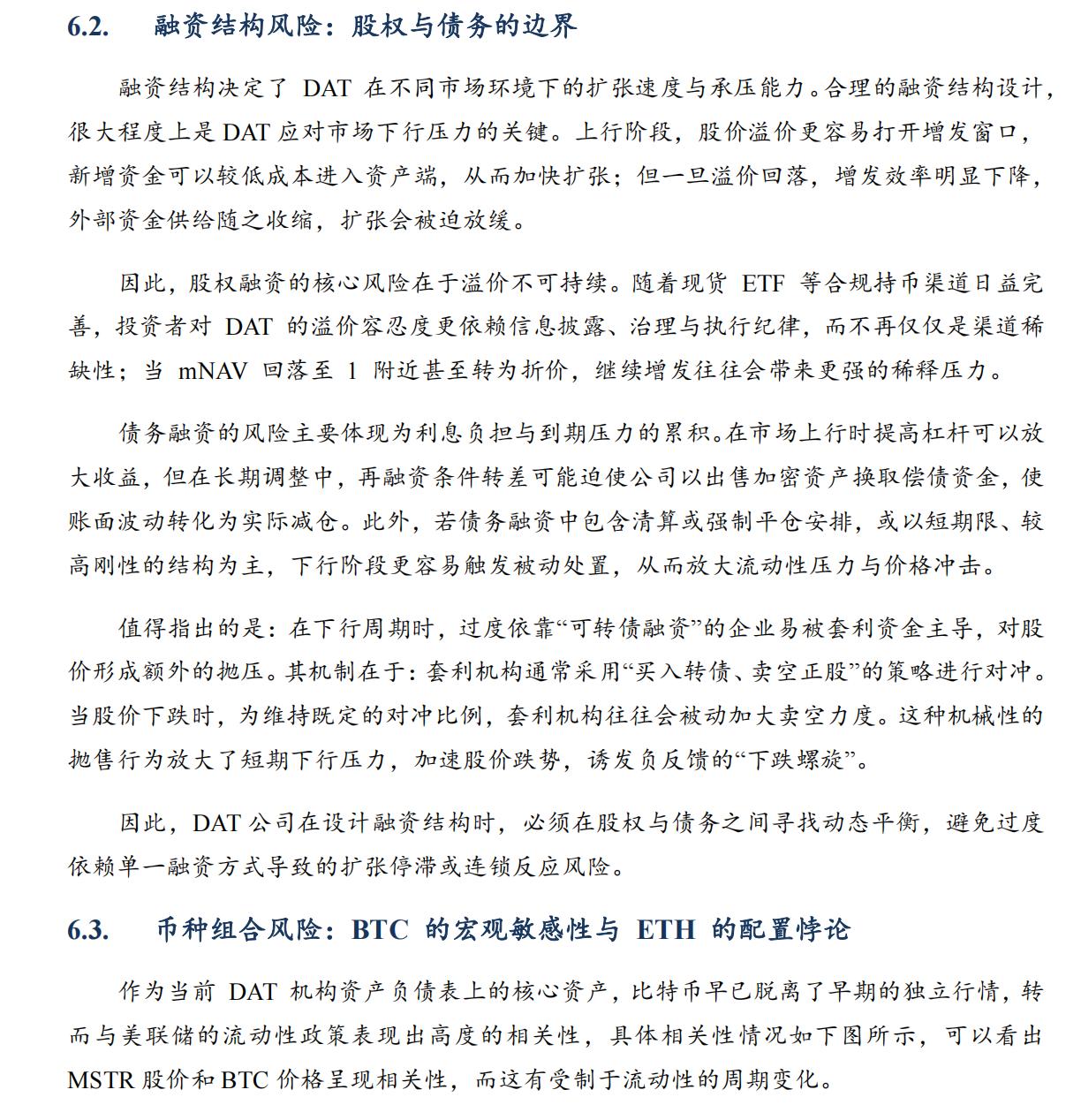

However, with the continued weakening of BTC and ETH prices since Q4 2025, the effectiveness of the DAT (Digital Asset Trust) approach has begun to be more widely questioned. There have been cases where entities using "equity + debt" financing have experienced financing model failures and been forced to adjust their strategies after stock price pullbacks: the stock price of MicroStrategy, the largest Bitcoin treasury, has fallen by more than 50%, and the stock price of Bitmine, the largest Ethereum treasury, has fallen by more than 80%. At the same time, some small and medium-sized DAT companies have also seen their strategies shrink or even suspend, such as Prenetics, a BTC treasury company endorsed by football star David Beckham, which stopped its treasury strategy. These changes have shifted the market's focus on DAT from "whether to hold the tokens" to "how to navigate pullback cycles": against the backdrop of price pullbacks, declining stock prices and debt pressures can create a double impact—in other words, the core variable determining whether a strategy can weather the cycle is "what financing method to hold the tokens + what tokens to hold."

Based on this, this paper reviews the current development status and latest stress tests of DAT companies at the beginning of 2026, and provides a framework analysis of the sustainability and key risk points of corporate DAT strategies from two main lines: financing structure and currency selection, in order to provide verifiable references for subsequent strategy design and risk control.

2. Concepts and Definitions

2.1. Definition of Concept: Treasury

This article studies DAT (Digital Asset Treasury), starting with a definition of the concept.

- Broadly defined: Any fund pool that incorporates crypto assets into its fund management system and intends to hold them for the medium to long term can be considered DAT. Classified by the treasury entity (i.e., the entity holding DAT): DAT can be divided into on-chain and off-chain categories.

(1) On-chain : mainly includes DAO organizations and project foundations;

(2) Off-chain : One type is DATCo (Digital Asset Treasury Company) which focuses on "hoarding coins", and the other type is companies with other main businesses but include crypto assets in their asset allocation (such as crypto mining companies).

(3) Backdoor listing: In recent years, a new path combining on-chain and off-chain has emerged. For example, project parties can achieve backdoor listing through shell companies (SPAC, special purpose acquisition company) to take over on-chain funds and off-chain capital market channels.

- In a narrow sense : In the current market context, DAT often refers to DATCo (Digital Asset Treasury Company), which is a company (mostly a listed company) whose main business is holding and managing crypto assets off-chain . [2]

Based on the above definition, the "DAT companies" referred to in this article mainly refer to DATCo, that is, companies (mainly listed companies) whose main business is off-chain cryptocurrency holding—with Strategy (formerly MicroStrategy) being the originator of this model . Companies with a clear main business and that only invest in crypto assets (such as mining companies) are not the focus of this analysis.

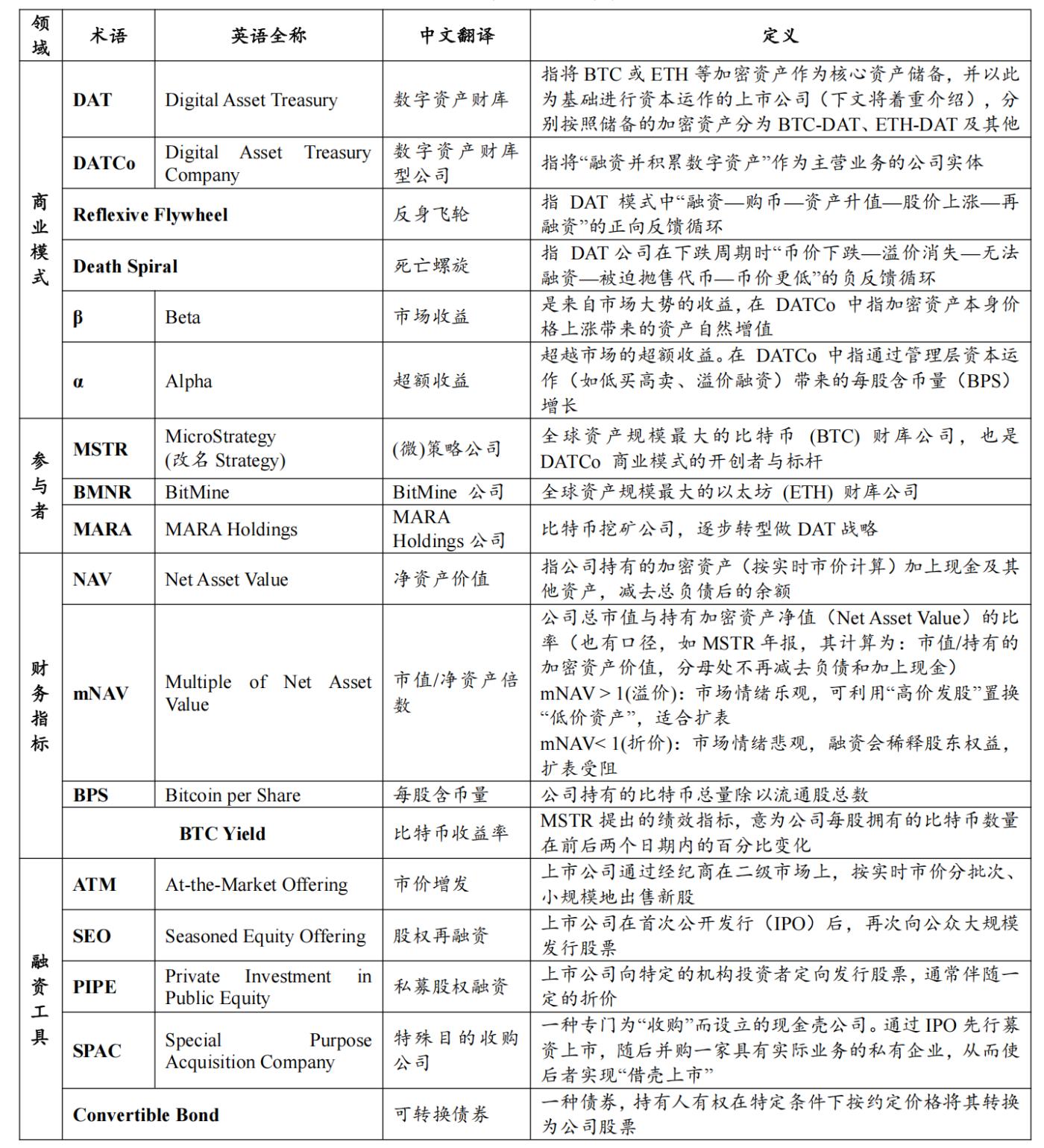

2.2. Terminology Explanation

Table 1: Explanation of Key Terms in the Article

Source: Compiled by PKUBA

2.3. Analysis of the Current Status of Digital Asset Reserves (DAT) of Global Listed Companies

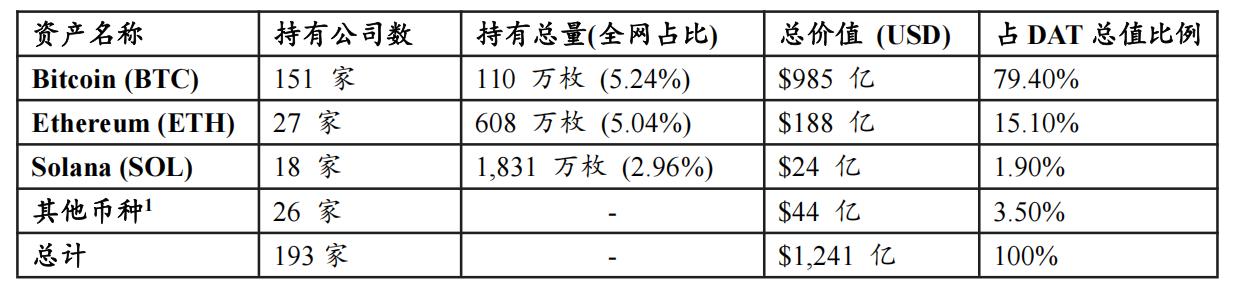

Based on Coingecko data (as of January 2, 2026), the following is a summary of the digital asset reserves (DAT) held by publicly listed companies worldwide. (Note: This statistic only covers data from publicly traded companies; holdings by unlisted companies are not included.)

Table 2: Statistics on Digital Asset Reserves (DAT) of Listed Companies

Source: Coingecko, data as of January 2, 2026

Note: Other currencies include XRP, BNB, TON, SUI, and other assets.

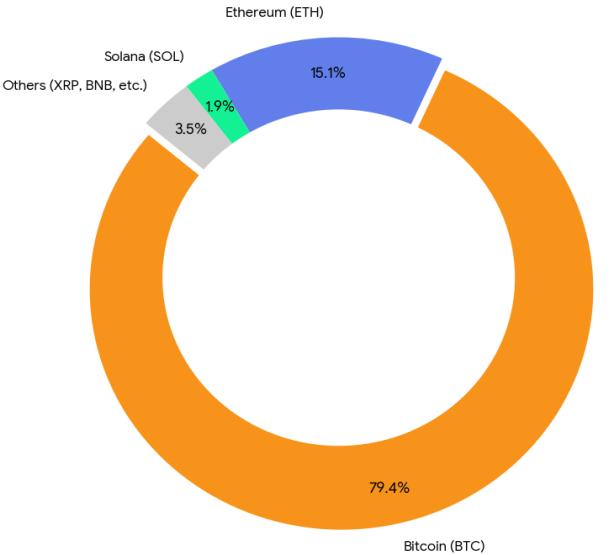

Figure 1: Value Share of Digital Asset Reserves (DAT) of Listed Companies

Source: Coingecko, data as of January 2, 2026

Based on the above, the basic structure of global listed companies DAT is as follows:

First, asset size and the leading effect: Statistics show that the total size of global listed companies' DAT has reached US$ 124.1 billion. In terms of value composition, Bitcoin (BTC) shows overwhelming dominance, accounting for as much as 79.4%; Ethereum (ETH) ranks second, accounting for 15.1%; Solana (SOL) and other long-tail assets account for only the remaining 5.5%.

Second, differences in allocation preferences and consensus : The penetration rates of various asset classes in corporate balance sheets differ significantly. BTC's total reserve value is approximately 5.2 times that of ETH and more than 41 times that of SOL. In terms of institutional coverage, as many as 151 listed companies hold BTC, far exceeding ETH (27 companies) and SOL (18 companies). This data strongly supports the fact that BTC remains the preferred asset for institutional fund allocation.

Third , the structural characteristics of long-tail assets: Within the "Other Assets" category (accounting for 3.5%), two main characteristics are observed:

- Established infrastructure category: Includes established public chain or exchange tokens such as XRP, LINK, TRON, and BNB, mostly held by listed companies in related business sectors;

- Capital Operation Category: Some emerging projects (such as 0G, Babylon, Pump.fun, etc.) exhibit obvious "crypto-equity linkage" characteristics, reflecting that some project teams are trying to achieve a deep binding between listed company equity and digital asset value through capital market operations.

3. DAT's business model

3.1. Business Model Positioning: A proactively managed balance sheet-based company

DAT companies have a relatively clear and replicable business model: they are essentially active operating companies with balance sheet management as their core, rather than ETFs or closed-end funds that passively track underlying assets.

Unlike traditional companies that rely on products and services to generate operating cash flow, DAT's core strategy is to raise funds through the capital market to purchase and hold crypto assets on a large scale for the medium to long term. Therefore, its asset portfolio typically shows a high allocation to digital assets such as BTC and ETH, while its liabilities and equity are mainly composed of equity and debt financing. Its operational goals are also primarily reflected in continuously accumulating digital asset scale on its balance sheet and increasing the asset content per unit of equity.

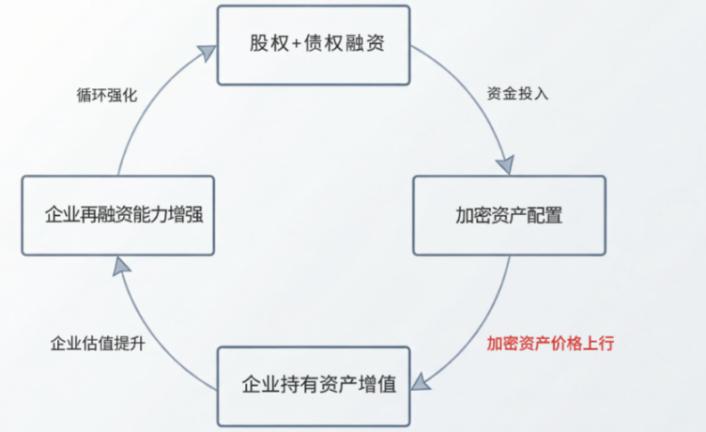

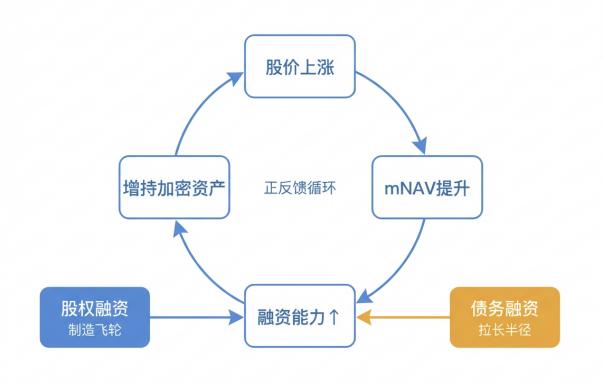

Figure 2: DAT Company's Value-Added Cycle Diagram (Reverse Flywheel Diagram)

Source: Compiled by PKUBA

This model is often summarized as a "reflexive flywheel": a positive feedback loop of financing—coin purchase—asset appreciation—market capitalization increase—refinancing. Its logical chain can be broken down as follows: the company obtains funds through equity or debt financing and allocates them to crypto assets; when the coin price rises, the increased value of the assets leads to a market revaluation of the company; rising stock prices further strengthen refinancing capabilities, thereby driving a new round of balance sheet expansion.

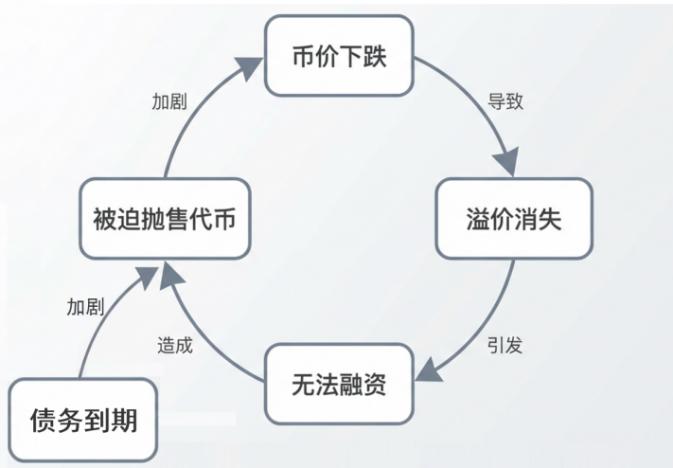

In contrast, DAT may fall into a "death spiral" during a downturn: a negative feedback loop of falling token prices—disappearance of premiums—inability to raise funds—forced token sales—further lower token prices. Specifically, the decline in the underlying asset (token price) first leads to a shrinking of the company's balance sheet; the loss of asset value causes the disappearance of the stock price premium and a sharp drop in valuation, resulting in the rapid closure of external financing windows; liquidity depletion or debt default risks force the company to sell tokens at low prices to repay debts, thereby further depressing the token price and exacerbating a new round of balance sheet shrinkage.

Figure 3: DAT Company's Declining Cycle Chart (Death Spiral)

Source: Compiled by PKUBA

This positive and negative two-way cyclical mechanism makes the DAT model exhibit a strong procyclicality in the highly volatile crypto market. The stability of its financial structure is extremely dependent on the price trend of the base token. Once it enters a downward channel, companies lacking external liquidity injections are easily caught up in irreversible asset sell-offs and valuation collapses.

Therefore, the pace of balance sheet expansion for DAT companies depends on the financing window, which is influenced by both the crypto asset cycle and the management's ability to complete financing and allocation during periods of favorable valuations. The ability to conduct forward-looking asset and liability management, maintain emergency liquidity, and dynamically adjust portfolio strategies becomes crucial for DAT companies to survive during cyclical shifts.

3.2. Value Creation Mechanism: Assets determine the outcome, financing determines the speed.

At the mechanism level, the value creation of DAT can be summarized into two main lines: the asset side β determines the direction and result of net asset value changes, and the capital side α determines the speed and efficiency of asset expansion.

- Asset-side beta: Income from changes in the price of crypto assets and holding gains such as staking (if applicable);

- Alpha from the capital side: comes from valuation premiums, resulting in more efficient financing and balance sheet expansion.

On this basis, the company also uses leverage tools (such as convertible bonds and mortgage financing) to improve capital utilization efficiency and liquidity—amplifying returns during upward phases, but at the same time increasing sensitivity to coin price pullbacks and refinancing conditions.

Table 3: Analysis of DAT Company's Value Sources and Mechanisms

Source: Compiled by PKUBA

Source: Compiled by PKUBA

In summary: β is more reflected in changes in NAV and cash holdings; the key to α lies in whether the company can steadily translate its valuation advantage into an improvement in BPS when mNAV is at a favorable level; while "tool layer" arrangements (debt, collateral, etc.) have more impact on execution flexibility and constraint strength.

3.3. Structural characteristics of business models: weakened profit and loss statement, concentrated assets, financing-driven, and valuation differentiation.

Within the framework of "β determines the outcome and α determines the speed," DAT's business model typically exhibits four structural characteristics, corresponding to the evaluation system, asset structure, financing structure, and valuation mechanism, respectively.

First, the evaluation framework has shifted from the income statement to the balance sheet. DAT's core operating activities do not rely on products or services to generate traditional revenue, but rather on balance sheet management centered around the holding and expansion of crypto assets. Therefore, indicators such as revenue, gross margin, and net profit have limited explanatory power for operating quality; more explanatory indicator systems tend to shift towards the amount of crypto held and its changes, the amount of crypto per share (BPS), and the market capitalization premium relative to net assets (mNAV) to measure whether balance sheet expansion is effective and whether the assets per unit of equity have achieved a substantial increase.

Second, assets are highly concentrated, and net assets are highly sensitive to cryptocurrency price fluctuations. DAT's asset structure is typically highly concentrated, with a high proportion of crypto assets, causing net assets to fluctuate significantly with cryptocurrency price movements. Cash primarily serves as a liquidity buffer, covering interest expenses, funding gaps, and operational safety during extreme market conditions. Therefore, the overall risk-return performance is more "non-linear": net asset elasticity amplifies during upward trends; during downward trends, net asset contraction, valuation compression, and decreased funding capacity often occur simultaneously.

Third, financing is primarily equity-based, supplemented by debt, and the structure determines the company's ability to withstand pressure across economic cycles. DAT's liabilities mainly consist of equity financing, debt financing, and a small amount of short-term borrowing or repurchase agreements. In practice, companies often expand their balance sheets through methods such as ATM (Asset-to-Money), SEO (Search-to-Earn), and PIPE (Private Partnerships) when valuations are more favorable, supplemented by convertible bonds, preferred shares, and notes to introduce a second layer of funding. These two types of financing are not simply substitutes: equity financing relies more on valuation and absorption capacity; debt financing is more constrained by currency pullbacks and refinancing conditions. Different terms and structures can significantly alter a company's financial pressure and risk exposure across economic cycles.

Fourth, valuations are sensitive to expectations, and the mNAV of similar assets may still diverge in the long term. DAT stock prices not only reflect the value of the underlying assets but also the market's overall expectations of its financing capabilities, management decisions, and the sustainability of its balance sheet expansion. Therefore, even with similar-sized and structured crypto assets, the mNAV of different DATs may still differ in the long term; these differences stem more from market sentiment, corporate governance, and financing path choices.

In summary, the risk-return characteristics of DAT are not determined by a single factor, but are often shaped by a combination of "asset concentration + financing structure + market expectations", which are amplified or weakened in different market environments.

3.4. Sources of Differences in Models: Financing Structure × Currency Attributes

From the perspective of business model structure, the differences between DAT mainly focus on two dimensions: financing structure and core asset selection.

In terms of financing structure, equity-dominated DATs can expand their balance sheets through share issuance when mNAV>1, but their financing capacity may weaken rapidly when valuations decline. DATs with a higher proportion of debt financing can improve asset expansion efficiency through convertible bonds, preferred shares, and other instruments, but they are more sensitive to currency price declines and deteriorating refinancing conditions. In particular, the term structure, interest rate level, and the presence of mandatory clauses will directly affect their survival ability in a bear market.

On the asset side, the choice of currency is another key variable determining the stability of the model. DAT, with BTC as its core asset, relies more on scarcity and market consensus; DAT with ETH or other platform tokens as its core assets, in addition to bearing the risk of price volatility, also faces uncertainties such as technological roadmap, ecosystem competition, and changes in revenue models. The differences in volatility, drawdown magnitude, and narrative stability among different currencies will be transmitted to the shareholder level through the balance sheet, significantly altering the risk curve.

Therefore, there is no single "optimal business model" for DAT; its sustainability depends more on the match between the financing method and the characteristics of the currency. The more aggressive the financing and the higher the uncertainty of the core assets, the stronger the dependence on the market environment. The following text can be developed along two lines: financing structure and currency differences.

4. Comparison of the core financing structures of DAT

Based on the above judgment that "financing structure determines the efficiency of balance sheet expansion and cross-cycle pressure", this section further breaks down common DAT financing tools and compares their applicability and constraints in different market stages.

4.1. Equity Financing: The Core Driving Force of the DAT Flywheel

Among the main financing methods, equity financing is the most strategically crucial for DAT: under specific valuation conditions, equity financing not only does not necessarily dilute the value of each share, but may even increase the number of crypto assets corresponding to each share. This is predicated on the company's stock price being higher than its intrinsic net asset value (mNAV), i.e., mNAV > 1. In this case, the company can issue new shares to raise funds, which can then be used to allocate BTC/ETH at a relative "discount" on the asset side, forming a structural condition of "exchanging valuation advantage for asset size," and constituting the core positive feedback source in the flywheel.

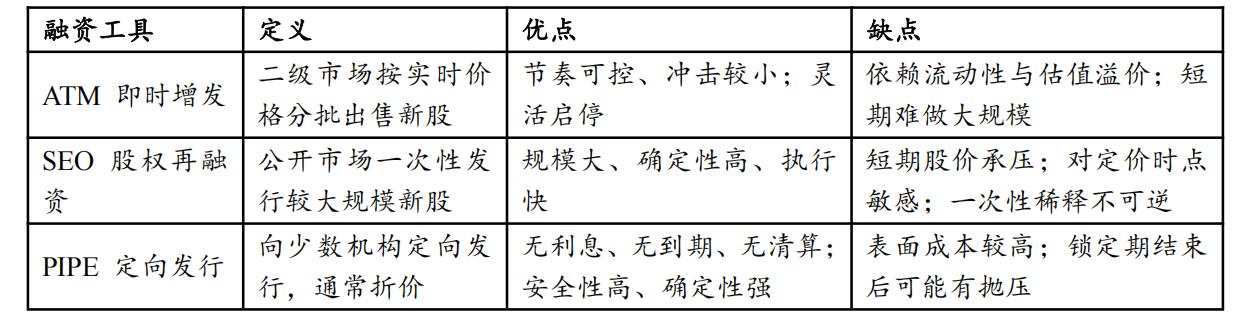

At the tool level, based on different financing methods, they can be divided into three approaches: ATM (At-the-Market Offering), SEO (Seasoned Equity Offering), and PIPE (Private Investment in Public Equity).

Table 4: Comparison of the Three Major Equity Financing Instruments

Source: Paramita Venture [3]

ATM (Instant Monetary Offering) is considered the most ideal equity financing tool. Its advantage lies not in the scale of financing, but in the highly decentralized pace of financing, allowing it to move in sync with secondary market trends. By continuously and decentralizedly issuing new shares in the public market, DAT can convert the increase in stock price into the ability to buy BTC/ETH without significantly disrupting the stock price. However, this model is extremely dependent on market conditions; once trading liquidity declines or valuation premiums converge, the viability of ATM quickly disappears.

SEO (equity refinancing) is more of a phased choice. By completing a large-scale financing in one go, DAT can significantly increase its BTC/ETH holdings in a short period of time, but at the cost of short-term stock price pressure and a high dependence on the timing of the issuance. If the market rises rapidly after the issuance, the opportunity cost of SEO will be amplified.

PIPE (Private Placement of Assets) are often issued at a discount. Although this superficially increases financing costs, from a balance sheet security perspective, PIPE is one of the most stable sources of funding for DAT (Digital Assets and Technologies). Because there is no interest burden, maturity pressure, or liquidation mechanism, PIPE transfers all uncertainty to equity investors, allowing DATs to maintain ample time options even in volatile environments. DATs using PIPE financing typically do not face passive deleveraging due to market fluctuations. This is why PIPE often becomes a practical choice for DATs during periods of unstable valuations and market uncertainty.

4.2. Debt Financing: Second Layer of Funding Sources and Time Constraints

Compared to equity financing, debt financing usually does not directly bring positive feedback, but it can significantly expand the scale of available funds at certain stages, thereby improving the efficiency of asset expansion, and can be regarded as a "second source of funds".

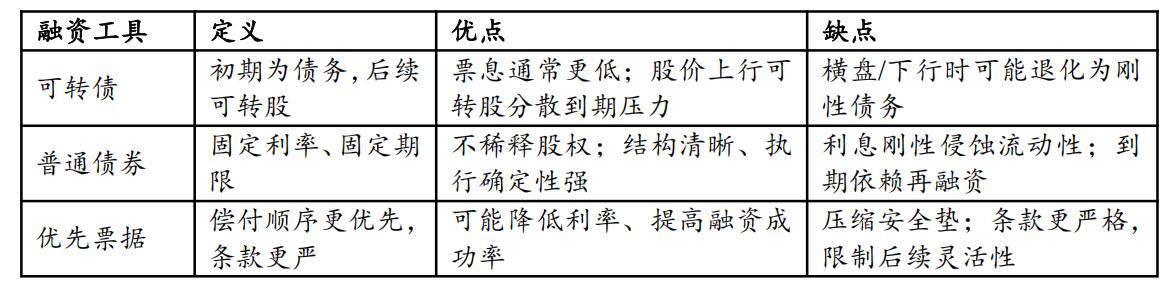

Convertible bonds are widely used in DAT financing structures, offering the advantage of combining the certainty of debt with the upside potential of equity. When the stock price performs well, convertible bonds can absorb debt repayment pressure through conversion; when the market performs poorly, their interest costs are usually lower than ordinary debt, providing a buffer for DAT. However, if the cryptocurrency trades sideways for an extended period and the stock price fails to meet the conversion criteria, the convertible bonds will ultimately become a rigid debt repayment burden.

In addition, heavy reliance on convertible bond financing may trigger a further "downward spiral" dominated by arbitrage institutions—that is, institutions hedge bond risks by short stocks—and when stock prices fall, in order to maintain the hedging ratio, these institutions will mechanically increase short efforts, thereby accelerating the stock price collapse and closing the financing window. This short selling mechanism embedded in the capital structure will passively amplify the decline in DATCo's downward cycle, deepen the "death spiral" and cause the financing capacity to reach zero before the asset value. [4]

Note: The "downward spiral" mentioned here is not the same as the "death spiral" under the reversal of the "reverse flywheel", but it will act as an accelerator, further deepening the degree of the "death spiral" and accelerating its collapse .

The risks of debt instruments such as ordinary bonds and senior notes do not stem from short-term price fluctuations, but rather from the time dimension. Unlike on-chain leverage, DAT creditors typically do not have the power to directly dispose of BTC/ETH, meaning the company will not be immediately liquidated due to a drop in the price of the coin. The real risks lie in the structural pressures brought about by accumulated interest expenses, concentrated debt maturities, and deteriorating refinancing conditions.

Table 5: Comparison of Debt Financing Instruments

Source: Compiled by PKUBA

Source: Compiled by PKUBA

4.3. The combination of equity and debt: flywheel formation and survival boundaries

Ideally, DAT does not rely on a single tool, but rather gradually builds and strengthens positive feedback through the phased coordination of equity and debt: rising stock prices drive up mNAV, enhancing financing capabilities; the proceeds from financing are used to increase holdings of BTC/ETH, further improving resilience to price increases, ultimately reflected in a further rise in stock prices.

In this process, equity financing is responsible for "building the flywheel," while debt financing is responsible for "lengthening the flywheel radius." The former determines whether DAT has a structural advantage, while the latter determines whether it can survive long enough before the flywheel is fully built and whether it can expand the flywheel's scale.

Figure 4: Flywheel formation diagram of DAT Company

Source: Compiled by PKUBA

From a risk-return-cost perspective, the difference between different financing methods lies not in their good or bad, but in their impact on the survival margin. PIPE-financed DATs are less likely to fail due to structural problems because their costs are clear and there is no mandatory exit mechanism; debt-financed DATs typically do not exit immediately because creditors lack the right to dispose of core assets. What truly needs to be guarded against is the introduction of short-term financing structures with liquidation or forced liquidation clauses, as such arrangements directly undermine the DAT's control over time.

Overall, DAT's financing structure does not simply pursue high leverage or high elasticity, but rather revolves around a core objective: in a highly volatile crypto market, through reasonable capital structure design, to extend the holding period of core crypto assets as much as possible and amplify their return potential within an appropriate cycle window.

5. Currency Analysis: How Core Assets Reshape DAT's Revenue Sources and Resilience

Within the framework of "financing structure × currency attributes," asset selection is far more than simply betting on which asset will rise the most. It actually determines three things simultaneously: first, the volatility of the asset's net asset value; second, the ease and cost of the company obtaining funding; and third, the market's tolerance for the company's valuation premium. Therefore, when the market focus shifts from simply "whether to hold currency" to "how to navigate economic cycles," currency allocation becomes a key variable determining the success or failure of a strategy.

Figure 1 shows the current cryptocurrency allocation of mainstream DAT institutions: Bitcoin accounts for approximately 80%, Ethereum for approximately 15%, and other cryptocurrencies for approximately 5%. This concentration at the top reflects the continued strong preference of institutional funds for assets with high interpretability and liquidity. Based on this, this section divides the evolution path of DAT into BTC-dominated and ETH-dominated (yield-generating) models. After a thorough analysis of the operational logic of these two core asset types, we will further explore typical cases of "crypto-stock linkage" among smaller cryptocurrencies.

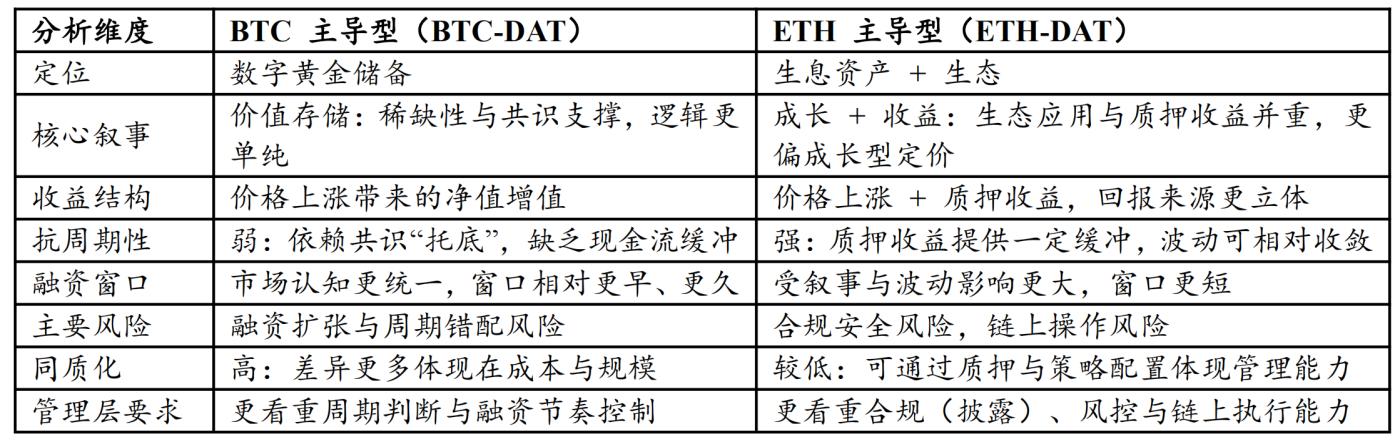

Table 6: Comparison of Characteristics of BTC-Dominated and ETH-Dominated DAT Companies

Source: Compiled by PKUBA

Source: Compiled by PKUBA

5.1. Bitcoin (BTC): Consensus Advantage Traded for a More Resilient Funding Window

The core logic of BTC-type DATs lies in their extremely low interpretation cost. The market tends to define BTC as a digital gold reserve. Even if the company itself lacks operating cash flow, investors can easily establish a clear pricing model through the size of their holdings, the rate of increase in holdings, and the net assets per share. This strong consensus characteristic creates two major financing advantages for the company:

- The asset-side pricing framework is clear, thus offering a long window of opportunity during upward cycles : due to the clear asset attributes, the market's acceptance of BTC reserves is highest in the early stages of a bull market. This allows the company to obtain a valuation premium more quickly, thereby securing ample time and operational space for subsequent refinancing (such as additional share issuance or convertible bonds).

- With lower uncertainty on the asset side, the discount during a downturn is manageable: when the market retraces, although the premium will be compressed, based on BTC's positioning as a mainstream asset, investors' evaluation logic will still remain within the framework of "net asset value - premium - financing capability," and they will not easily question the asset's risk of going to zero. This clear valuation anchor can effectively prevent narrative collapse.

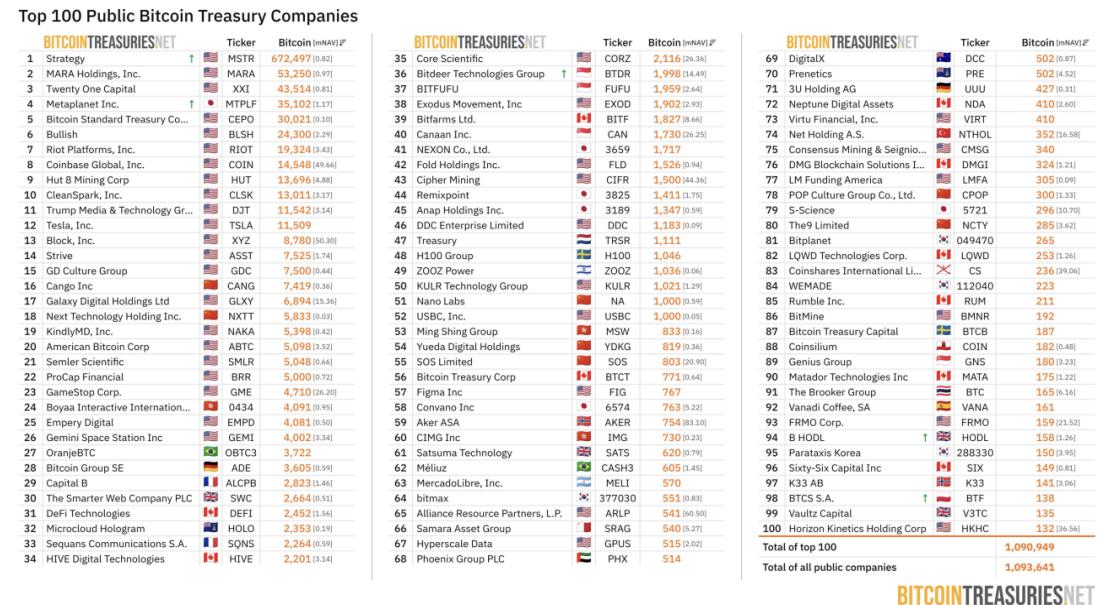

Figure 5: Statistics of the Top 100 Global BTC Treasury Companies on the Bitcointreasuries Website

Source: Bitcointreasuries, data as of January 2, 2026

However, BTC-type DATs are not a natural safe haven; their "high beta" attribute also brings hidden structural risks.

First, the lack of a native revenue stream makes companies extremely sensitive to financing timing : Because BTC lacks a native staking reward mechanism, the company's performance is entirely dependent on price fluctuations. This deprives companies of a means to smooth out cycles, making precise timing of "financing-buying" extremely crucial. If a company's assets are at a high level at the peak of financing, and subsequently experiences a price drop, it will face severe maturity mismatch risk—the gap between the interest on rigid debt and the depreciation of its assets.

Second, homogeneous competition weakens pricing power : When most DAT companies adopt a single strategy of "hoarding coins," their business models inevitably become homogeneous. The market is unlikely to award higher management premiums to specific companies, and their stock prices may ultimately become mere shadow ETFs of BTC. This places higher demands on management: how to create alpha through "financial tricks" in a homogeneous competitive environment by using precise macro timing or innovative financing structure design.

In summary, while BTC provides a stable narrative foundation, if a company lacks a buffer mechanism for generating income and misjudges the financing cycle, it will be very likely to fall into a passive contraction predicament once the valuation falls and financing dries up.

5.2. ETH: The combination of ecosystem and revenue variables places higher demands on transparency.

Unlike BTC's pure reserve attribute, ETH possesses a dual attribute of "interest-bearing mechanism + ecosystem governance." This means that ETH-type DATs face a more complex pricing model—the market not only focuses on price trends but also incorporates the prosperity of the network ecosystem, the technology upgrade roadmap, and on-chain yield into valuation considerations.

This complexity provides DATCo with a tool to smooth out cycles and creates opportunities for differentiation among companies. Companies can stake a portion of their ETH or participate in on-chain DeFi to generate stable holding returns. This upgrades the treasury narrative from simply holding tokens to a "manageable portfolio of interest-bearing assets," providing a cash flow buffer during bear markets. Furthermore, this model gives companies room for "active management"—the allocation of staking ratios, the deployment of node verification, and the design of liquidity release mechanisms can all become key indicators for horizontal comparison.

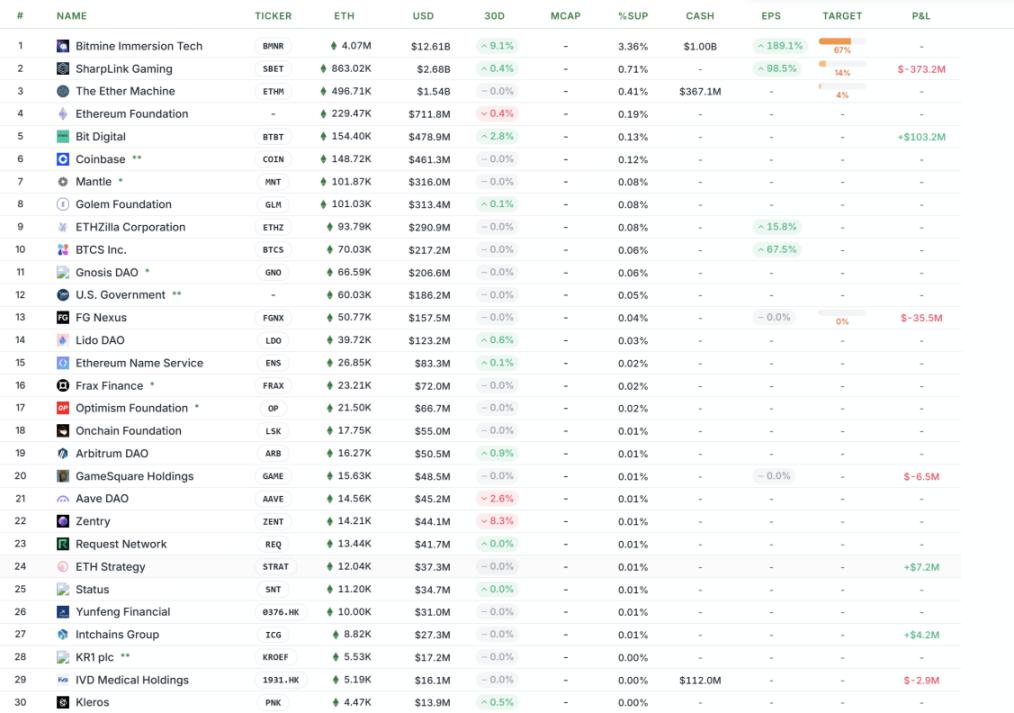

Figure 6: Strategicethreserve Official Website: Global Top 100 ETH Treasury Listed Companies Statistics Chart

Source: Strategicethreserve, data as of January 2, 2026

However, the other side of the coin is the extreme demand for risk control and transparency: given that ETH's staking mechanism may touch a nerve with securities regulators (such as the US SEC), and that on-chain interactions involve complex auditing issues, if a company cannot clearly disclose the source of its revenue or prove the independence of its asset custody, the market will struggle to assign a fair price, resulting in a significant valuation discount. Only by completing a highly transparent audit can investors' compliance concerns be eliminated.

Finally, compared to the strong cyclicality of BTC, ETH exhibits more pronounced volatility, resulting in a "narrow and rapid" financing window. This window often opens and closes quickly, and the ability to complete financing and allocation within a short period directly shapes the balance sheet structure for the following quarters. In other words, the ETH treasury operates on an "opportunity window strategy": inadequate execution and governance can amplify its complexity and uncertainty.

5.3. The "Crypto-Stock Linkage" Model for Minor Cryptocurrencies: Asset Mapping and Liquidity Transmission under the SPAC Channel

Beyond mainstream assets, small-cap cryptocurrencies are exploring a more aggressive "crypto-stock linkage" path. Unlike the traditional model where business revenue supports stock prices, this model utilizes SPACs (Special Purpose Acquisition Companies) as listing vehicles, combined with financing tools such as PIPE and ATMs, to construct a transmission mechanism connecting US stock market liquidity with on-chain assets.

In short, this is not a simple "backdoor listing", but rather the encapsulation of the on-chain token "buying plan" into tradable Nasdaq stock assets, thereby achieving a deep binding between the project's assets and secondary market funds.

5.3.1. Core Mechanism: Liquidity Transmission After Backdoor Listing

On the surface, this appears to be a "backdoor listing" for the project, but a deeper analysis reveals it to be a liquidity transfer mechanism centered on capital operations—allowing funds from the stock market to be rapidly and directly transferred to the token market. This operation comprises two key elements:

- SPAC provides compliance access: Utilizing shell companies to resolve compliance issues and open up access to dollar liquidity.

- Financing instruments provide new funds: Through instruments such as PIPE (private equity investment), convertible bonds, or ATM (market-based issuance), listed companies can continuously obtain low-cost funds, forming a continuous buying pressure on on-chain tokens.

Under this architecture, the pricing logic of stock prices changes: the market no longer anchors itself to the price-to-earnings ratio (P/E), but instead focuses on the token's net asset value (NAV) and refinancing capabilities. The stock price effectively becomes a leveraged reflection of the token price.

5.3.2. Typical Path Analysis: Static Treasury and Dynamic Market Making

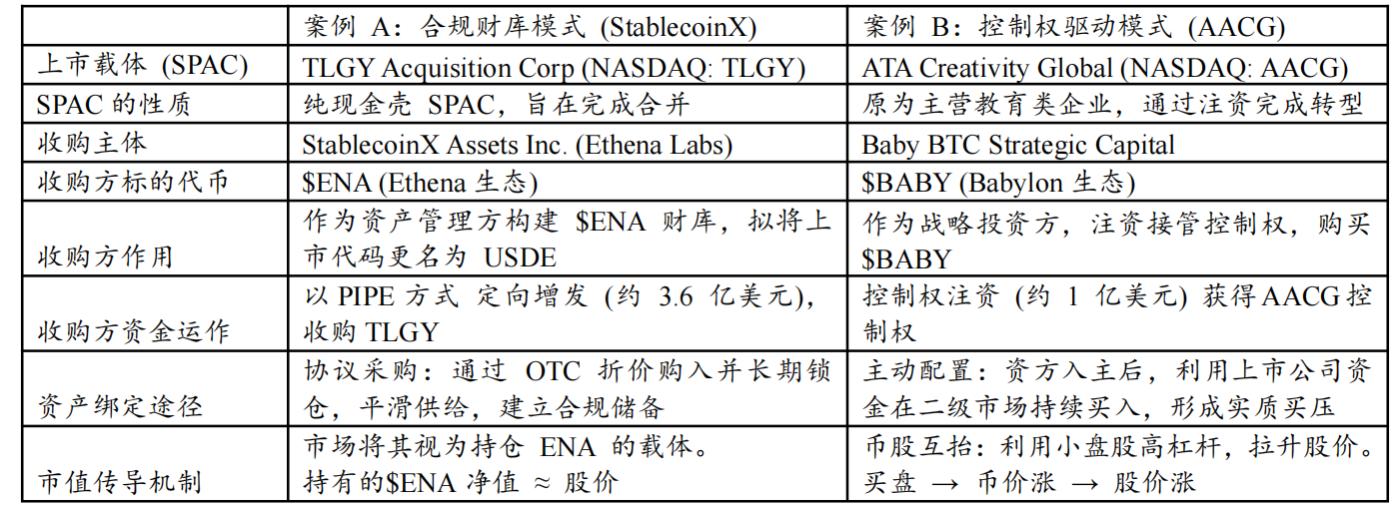

Depending on the degree of involvement of the project team in the listed company and the different operational goals, the linkage model of small cryptocurrencies presents two different paths: one is the compliant treasury model, which focuses on asset holding; the other is the control-driven model, which focuses on capital games and subjective market making.

As analyzed in the table below, StablecoinX (TLGY) adopts a structured asset mapping model. Essentially, it establishes a highly transparent token vault on Nasdaq. Funds are primarily used to purchase and lock tokens at a discount off-exchange, thus avoiding direct impact on the secondary market. Under this model, stock price fluctuations are relatively smooth, mainly reflecting the true net asset value (NAV) of the underlying assets. The project aims to leverage the compliance of the US stock market to provide traditional institutional funds with a low-threshold channel to allocate core crypto assets, facilitating auditability and supply locking.

Table 7: Comparison of Typical Paths for Cryptocurrency-Stock Linkage Between Smaller Cryptocurrencies

Source: Compiled by PKUBA

Source: Compiled by PKUBA

The AACG (Baby) case represents actively managed capital market making, i.e., capital-driven liquidity management. External capital gains control of listed companies through investment, quickly converting on-balance-sheet funds into token purchasing power. Due to the small circulating supply of altcoins, concentrated purchases by listed companies can significantly improve the supply and demand of tokens, thereby driving up the price and leading to a revaluation of the stock price. This is a more aggressive strategy that attempts to use the liquidity premium of the capital market to support on-chain assets.

While the two models described above differ in their approaches, they essentially both utilize the listing channel to securitize asset allocation. However, this logic is not without flaws. The key risk of cryptocurrency-equity linkage lies in whether the positive cycle between the asset side and the financing side can be closed. If listed companies merely become one-way buying machines, the high premium will quickly collapse once the secondary market financing window closes or the cryptocurrency price experiences a sharp correction.

Therefore, the most prudent outcome should be that listed companies are not only buyers of tokens, but also builders of the ecosystem. Only by binding corporate strategies with the long-term value of the ecosystem through governance structure can stock prices transform from mere speculative leverage into a compliant indicator that measures the prosperity of the ecosystem.

6. DAT Risk Analysis

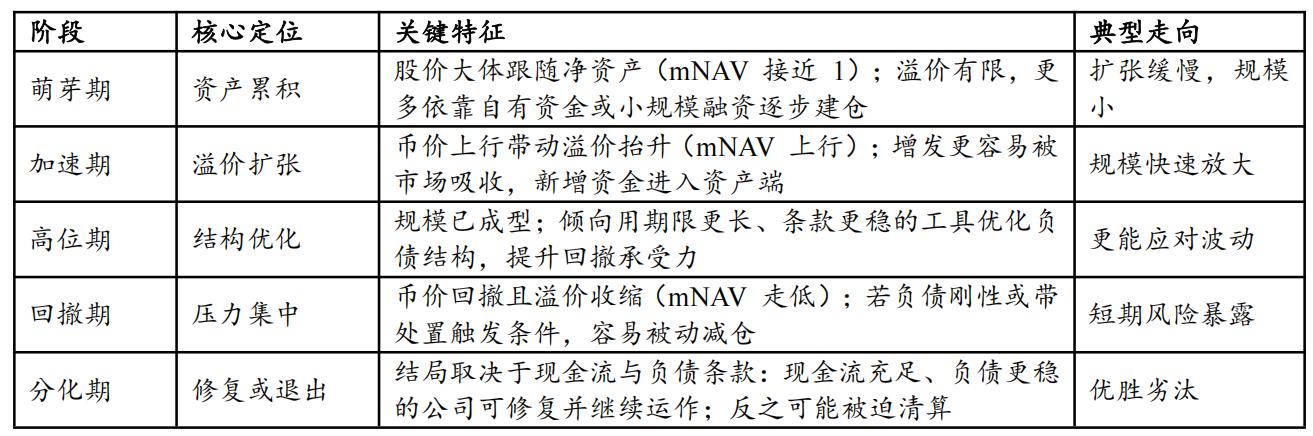

6.1. The Cyclical Stages and Differentiation Paths of DAT

The operation of DAT is not a static model, but is simultaneously influenced by two major factors: (1) the cyclical fluctuations in the price of crypto assets, and (2) the premium level of companies holding DAT in the secondary market. Therefore, the key to judging whether a DAT company is sustainable is not "whether it holds DAT", but rather which stage of its life cycle it is in and whether its balance sheet has reserved sufficient safety margin for the next stage.

The table below illustrates the complete lifecycle of DAT. From a lifecycle perspective, the key to success or failure often lies not in the ability to expand during a pro-cyclical period, but in the divergent outcomes after a downturn: During a pro-cyclical period, premium financing is easier to access, and DAT companies can generally expand their balance sheets by leveraging market absorption capacity; however, once a pullback begins, the decline in coin price and the contraction of premiums often occur simultaneously, narrowing or even closing the financing window. At this time, only companies with more stable debt structures and lower short-term rigid debt repayment pressure are more likely to withstand volatility and remain viable; conversely, companies with weaker cash flow and potential disposal triggers may be forced to reduce their holdings in unfavorable price ranges to meet debt repayment or contractual requirements, thus amplifying cyclical fluctuations into liquidation risks.

Table 8: Comparison of DAT Cycle Stages

Source: Compiled by PKUBA

Source: Compiled by PKUBA