Editor's Note: Amidst persistently weakening market sentiment, crypto assets have been repeatedly labeled as "end of the cycle." However, this article argues that the price decline is not due to fundamental failure, but rather a result of a temporary liquidity contraction. The rebuilding of the US fiscal account, the depletion of reverse repurchase facilities, the government shutdown, and the strengthening of gold have collectively drawn funds away from high-duration assets, putting pressure on Bitcoin and SaaS assets.

At the same time, the "false narrative" surrounding monetary policy is also worth noting. While Kevin Warsh is widely regarded as a hawk, statements from Druckenmiller suggest his policy approach is closer to that of the Greenspan era: allowing the economy to overheat and betting on productivity gains to alleviate inflation. Within this framework, future developments are more likely to involve interest rate cuts coupled with coordinated fiscal measures to release liquidity.

In a complete cycle perspective, time is often more important than price. In the short term, risk assets may continue to be under pressure; however, as liquidity constraints gradually ease, the current pessimistic narrative may be repriced.

The following is the original text:

Faulty narratives...and some scattered thoughts

I'd like to share some insights I gained while writing GMI this weekend, hoping to help you calm down and regain some confidence. Sit down, pour yourself a glass of red wine or a cup of coffee... I was originally going to save these for GMI and Pro Macro, but I know you really need some reassurance right now.

"Grand Narrative"

The prevailing narrative right now is: Bitcoin and the entire crypto market are broken. The cycle is over, everything is ruined, and we'll never have anything good again. It's completely decoupled from other assets—blame CZ, BlackRock, or someone else entirely.

To be honest, it is indeed a very tempting narrative trap... especially when you wake up every day to see prices plummeting and crashing again and again.

But yesterday, a hedge fund client of GMI sent me a short message asking: Is now the time to buy SaaS stocks? They've already fallen to a bargain price; or, as the current narrative suggests, has Claude Code "killed" SaaS?

So I decided to take a serious look. What I discovered completely destroyed both the narratives that "BTC is finished" and "SaaS has been terminated."

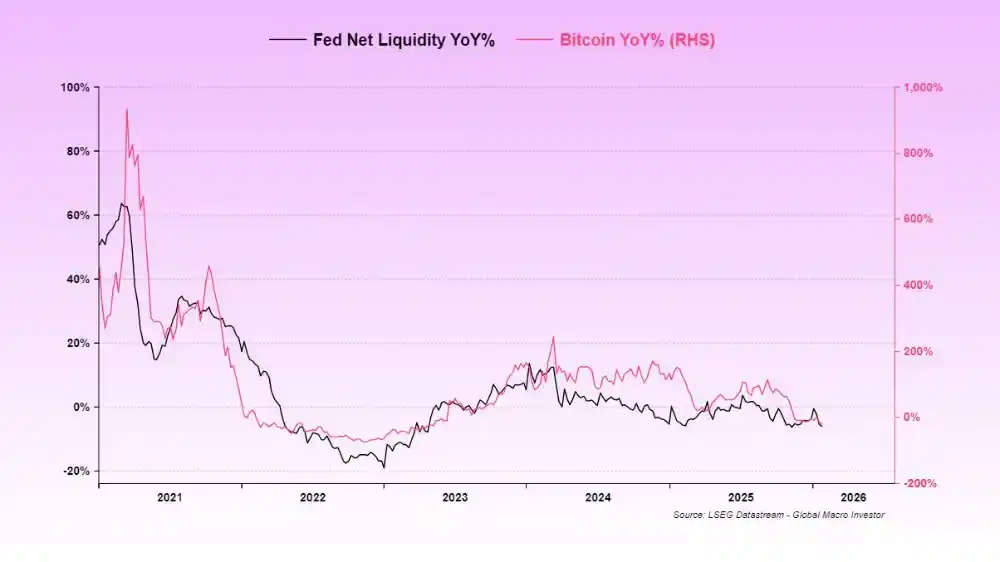

Because the price charts for SaaS and BTC are exactly the same.

This means there's another factor at play that we've all overlooked...

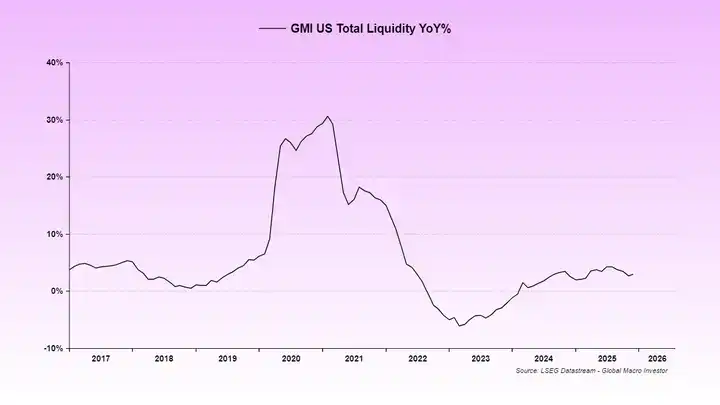

This factor is that, due to the two shutdowns and problems at the "pipeline" level of the US financial system, liquidity in the US has been consistently suppressed. (The "flooding" process of the Reverse Repo instrument was essentially completed by 2024.)

Therefore, the TGA (U.S. Treasury General Account) reconstruction in July and August did not have a corresponding currency hedging mechanism.

As a result, market liquidity was directly withdrawn.

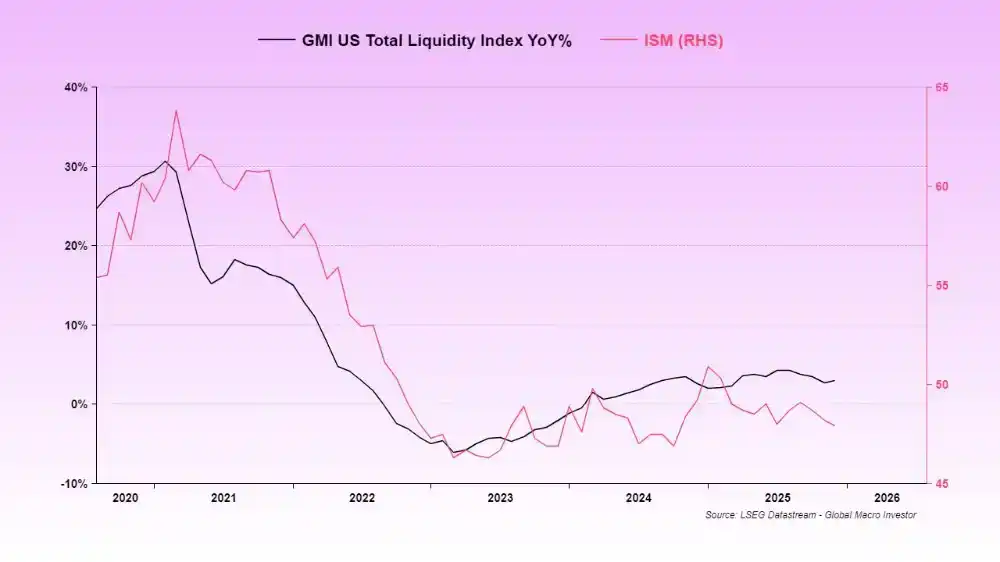

The persistently weak liquidity is precisely why the ISM index remains at a low level.

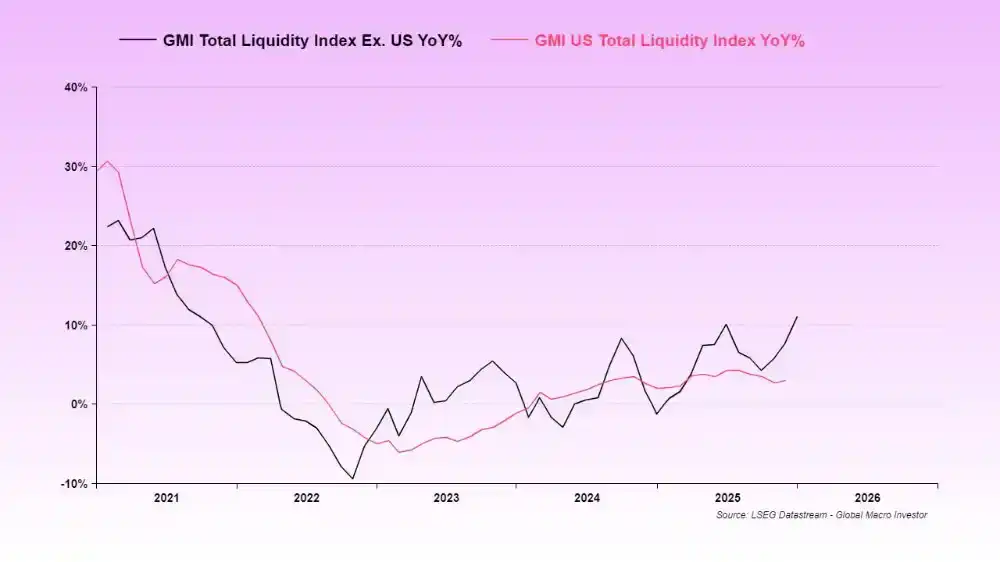

We typically use Global Total Liquidity (GTL) because it has the highest correlation with BTC and the Nasdaq (NDX) index in the long run.

But at this stage, US Total Liquidity is clearly more dominant – because the US remains the core supplier of global liquidity.

In this cycle, global aggregate liquidity (GTL) has already moved ahead of US aggregate liquidity (USTL), and the next liquidity rebound is approaching—the ISM will also recover accordingly.

And this is precisely the key reason affecting SaaS and BTC.

These two types of assets are essentially the longest-lasting assets; when liquidity experiences a temporary pullback, they will naturally be discounted and revalued as a whole.

At the same time, the rise in gold prices has absorbed almost all marginal liquidity in the system—funds that might have flowed to BTC and SaaS have been "hijacked" by gold.

When liquidity is insufficient to support all assets simultaneously, the riskiest segment is the first to be hit.

This is the reality of the market.

Now, the US government has shut down again.

The Treasury actually hedged against this: after the last shutdown, it did not use the funds in the TGA (Treasury General Account), but instead continued to add money to it—which was equivalent to further draining market liquidity.

This is precisely the "liquidity vacuum" we are currently facing, and it is also why price movements are so brutal.

There is currently no liquidity flowing into our beloved crypto market.

However, signs indicate that the shutdown is likely to be resolved this week, which will be the last liquidity hurdle to overcome.

I have mentioned the risks of this shutdown many times before. Soon, it will become a scene in the rearview mirror, and we can truly enter the next stage—a period of liquidity flood driven by factors such as eSLR adjustments, partial release of TGA, fiscal stimulus, and interest rate cuts.

Ultimately, it all revolves around the midterm elections.

In a complete cycle of trading, "time" is often more important than "price." Yes, the price may be hit hard; but as long as time goes on and the cycle continues, everything will correct itself, and the "crocodile mouth" will eventually close.

This is why I repeatedly emphasize "patience".

Things take time to unfold, and staring at P&Ls every day will only harm your mental health, not improve your portfolio performance.

The "Misleading Narrative" about the Federal Reserve

Speaking of interest rate cuts, there is a widely circulated misconception in the market: that Kevin Warsh is a hawk.

This is complete nonsense.

These claims are largely based on statements made 18 years ago. Warsh's role and mission are to replicate the operational script of the Greenspan era. Trump has said this, and so has Bessent.

Going into the details would be too lengthy, but the core message is simple: lower interest rates to fuel the economy, while assuming that productivity gains from AI will suppress core CPI, just like in the period of 1995–2000.

Warsh certainly doesn't like expanding the balance sheet, but the system is now hitting reserve constraints, so it's almost impossible for him to change the current path. If he were to force a change, the credit market would be completely destroyed.

So the conclusion is simple: Warsh will cut interest rates, but he won't do anything else.

He will make way for Trump and Bessent to push liquidity through the banking system. Miran, on the other hand, will likely push for a broad reduction in the eSLR, further accelerating the process.

If you don't believe me, then believe Druck.

I know that when everything seems so bleak, listening to any overly optimistic narrative will sound incredibly jarring. Our Sui position now looks like a pile of dog shit, and we're starting to lose track of what to believe and whom to trust.

But first of all, we've experienced this situation many times before.

When BTC drops by 30%, it's not uncommon for smaller cryptocurrencies to drop by 70%; and if they are high-quality assets, they tend to rebound even faster.

Admitting fault (Mea Culpa)

Our mistake with GMI was that we failed to realize in time that "US liquidity" was the real dominant variable at the current stage.

In previous cycles, global aggregate liquidity typically dominated, but this time it wasn't. Now everything is clear—the "Everything Code" is still in effect. There is no "decoupling."

However, we failed to anticipate, or rather underestimated, the cumulative effect of this series of events: the Reverse Repo was drained → the TGA was rebuilt → the government shut down → gold prices soared → another shutdown.

This combination of attacks was extremely difficult to predict in advance, and we certainly underestimated its impact.

But all of this is nearing its end. Finally. Soon, we can return to "normal business operations".

We can't be right about every single variable, but we now have a clearer understanding of the situation.

Moreover, we remain extremely bullish on 2026—because we are very clear about the script that Trump/Bessent/Warsh will follow.

They've told us this repeatedly. All we have to do is listen and be patient.

In a full-cycle investment, what truly matters is time, not price.

If you are not a full-cycle investor, or if you cannot tolerate this level of volatility, then that's perfectly fine.

Everyone has their own style.

But Julien and I have never been short-term traders, and frankly, we're terrible at it (we don't care about the ups and downs within a cycle).

However, when it comes to investing over a complete cycle, our verifiable and traceable long-term track record over the past 21 years is among the best in history.

Of course, a disclaimer must be added: We also make mistakes. 2009 is a painful example of this.

So now is not the time to give up.

Good luck, let's have a fucking epic 2026 together.

The mobile cavalry is on its way.