Original authors: Bao Yilong, Zhang Yaqi, Li Jia

Original source: Wall Street News

A stronger-than-expected US jobs report in January quickly extinguished market hopes for an earlier rate cut by the Federal Reserve, with traders pushing back their expectations for the first rate cut from June to July, putting pressure on US Treasury prices. US stock indices initially gapped higher after the data release, but subsequently gave back gains due to weakness in technology stocks.

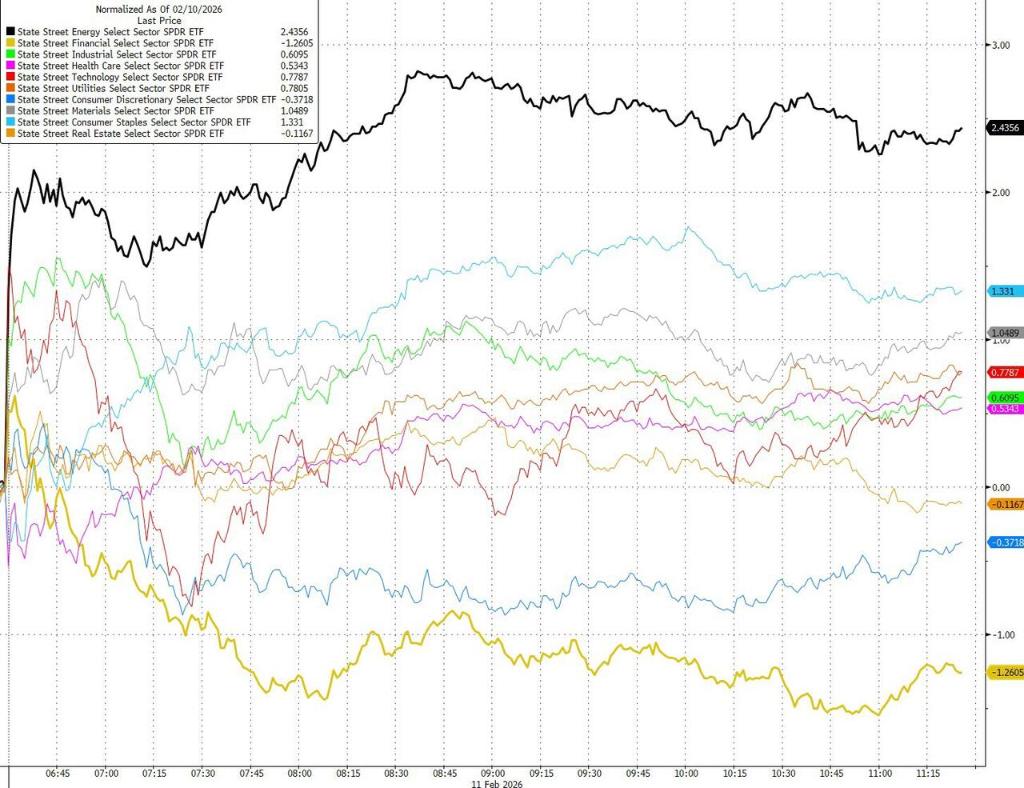

The S&P 500 was essentially flat on Wednesday, while the Dow Jones and Nasdaq closed slightly lower. Notably, the equal-weighted S&P 500 rose 0.2%, with nearly 300 stocks advancing. "Old economy" sectors such as energy, materials, and consumer staples outperformed. Funds continue to shift from overvalued growth stocks to the "real economy" and hard assets.

According to Wall Street News , the U.S. added 130,000 non-farm jobs in January, far exceeding market expectations of 65,000, and the unemployment rate unexpectedly fell to 4.3%. Although the employment data for the previous year was significantly revised downward, the rebound in January was enough to shatter the narrative that "the labor market is rapidly weakening."

Following the data release, expectations for an interest rate cut dropped significantly. The swap market postponed the next rate cut from June to July, and the probability of a March rate cut was almost completely ruled out. CME data showed that the probability of the Federal Reserve holding rates steady in March rose to over 94%.

The weakness of large-cap tech stocks dragged down the overall performance of US stocks. Traditional economic sectors, including energy, consumer staples, and materials, outperformed other sectors.

Kevin O'Neil of Brandywine Global stated:

While job growth remains concentrated in the healthcare sector, manufacturing has returned to positive growth, showing encouraging signs of improvement.

Mike Reid of RBC Capital Markets stated:

The January jobs report showed continued improvement in the U.S. labor market. Looking ahead, this report reinforces our previous view that the Federal Reserve will pause interest rate hikes for an extended period until 2026.

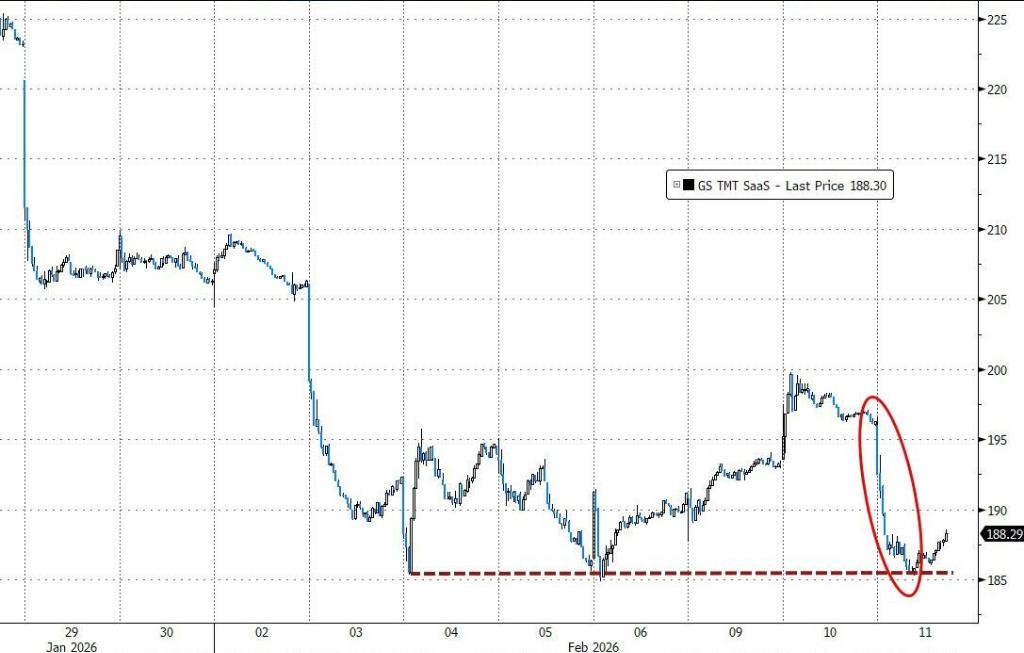

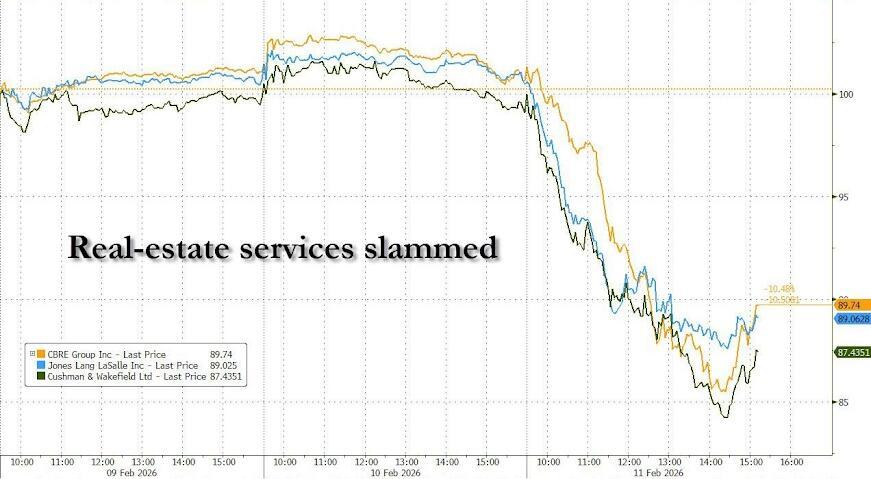

Concerns about the disruptive potential of AI continue to grow, first affecting software, then private lending, insurance brokerage, and securities firms, and now spreading to real estate services and financial intermediaries. Software stock ETFs fell 2.6%.

(SaaS stocks declined, with analysts believing the rebound in software stocks has ended)

(SaaS stocks declined, with analysts believing the rebound in software stocks has ended)

Real estate services stocks were sold off, with CBRE Group and Jones Lang LaSalle plunging 12%.

(Real estate services stocks plunge)

(Real estate services stocks plunge)

The Philadelphia Semiconductor Index rose 2.3%, continuing to attract capital. Micron surged 10% on expectations of HBM4 capacity release, as the market re-bet on the certainty of the AI infrastructure chain. Robinhood fell nearly 9% due to weaker-than-expected earnings, reflecting a cooling of retail trading activity.

(Semiconductor sector rises)

(Semiconductor sector rises)

The bond market also saw significant volatility. Long-term US Treasury yields had fallen before the non-farm payrolls report was released, but rebounded quickly after the data came out. The yield on the policy-sensitive 2-year Treasury note rose 6.4 basis points, while the 10-year yield increased by about 3 basis points.

(Intraday movement of benchmark US stock indices)

(Intraday movement of benchmark US stock indices)

The US dollar index fluctuated significantly throughout the day, closing up slightly by 0.08%, amid strong jobs data and hawkish Federal Reserve expectations. The Japanese yen rose for the third consecutive day, appreciating by more than 1% at one point. Cryptocurrencies weakened under pressure from expectations of "higher and longer" interest rates.

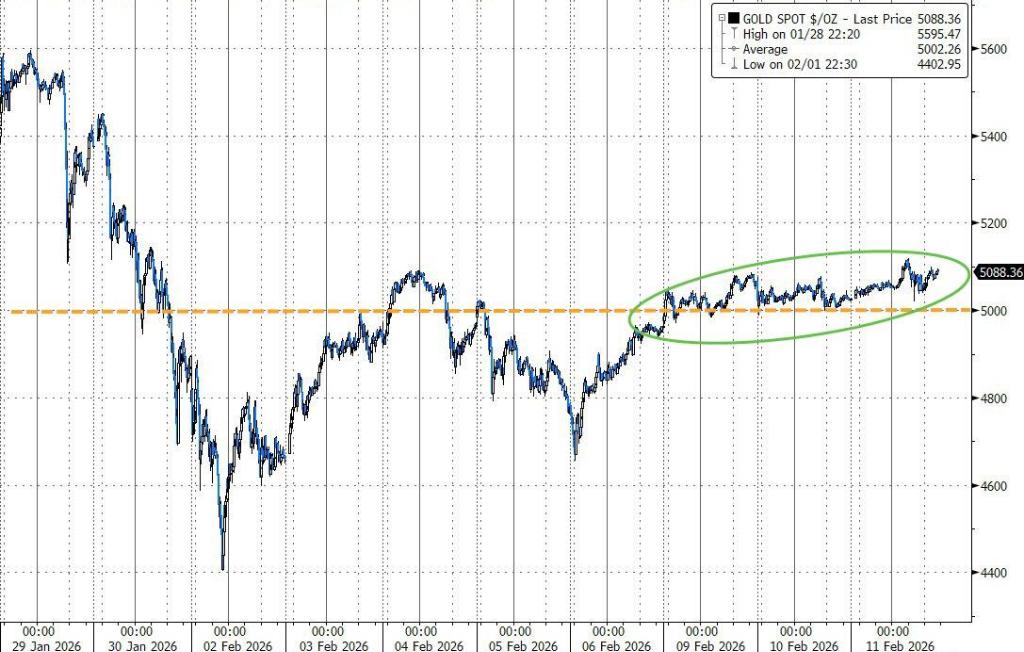

Spot gold rose 1.3% in a volatile session, remaining above $5,080. Silver, however, rose initially before retreating, but still gained over 4%.

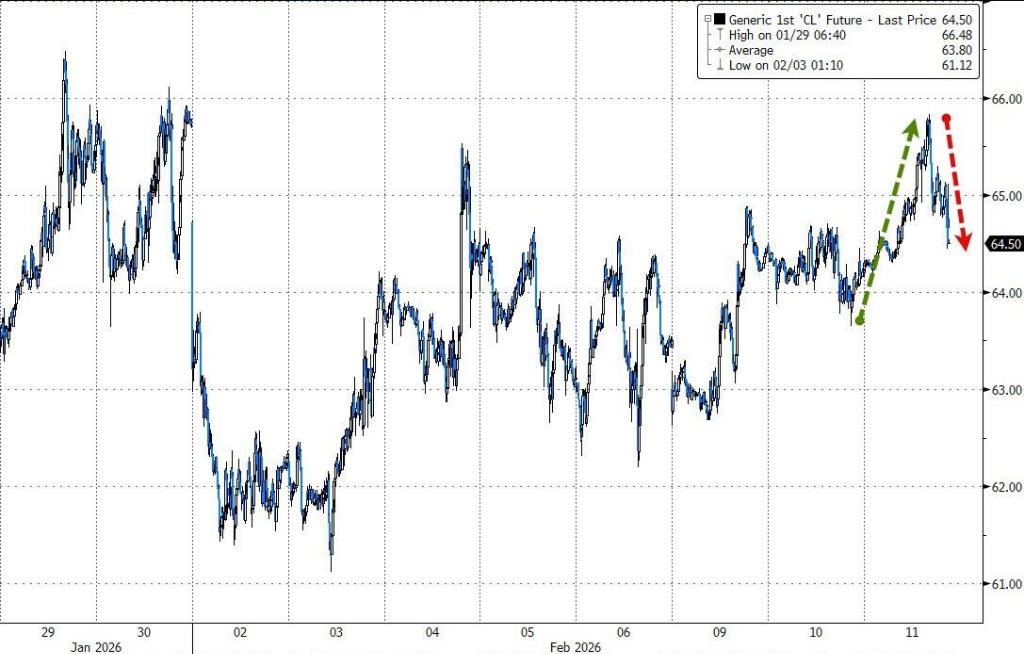

Wall Street News reported that reports indicated Trump was privately considering withdrawing from the USMCA (United States-Mexico-Canada Agreement), causing crude oil prices to rise by more than 2% intraday. However, a significant increase in crude oil inventories and a rebound in US production led to a narrowing of the price increase to 1%.

U.S. stocks rallied and then retreated on Wednesday, with the S&P 500 essentially flat and the Dow Jones and Nasdaq closing slightly lower. Concerns about AI disruption continued to simmer, with software ETFs falling 2.6% and real estate services stocks also being sold off due to AI worries, with CBRE Group and Jones Lang LaSalle plunging 12%.