Original title: "Q4 Huge Loss of $667 Million: Does Coinbase's Financial Report Foreshadow a Difficult Year-End for the Crypto in 2026?"

Original author: Mach, Foresight News

On February 13, the US stock market experienced a sudden plunge, with the Dow Jones Industrial Average closing down 1.34%, the Nasdaq Composite Index down 2.03%, and the S&P 500 Index down 1.57%. Gold once fell by more than 4%, and silver plummeted by 11%. Bitcoin's price fell to $66,000, and Ethereum fell to $1,900.

Shares of Coinbase, the largest cryptocurrency exchange in the U.S., plummeted to around $140 after the company released its Q4 and full-year 2025 financial results. Despite strong full-year performance, the net loss in Q4 and slowing trading volume were the immediate triggers for investor selling.

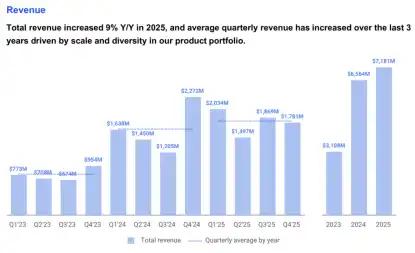

In 2025, Coinbase's revenue reached $7.181 billion, an increase of approximately 9% from $6.564 billion in 2024, with net income of $6.883 billion. Despite a net loss of $667 million in Q4 due to book losses in its crypto asset portfolio, the company still achieved a net profit of $1.26 billion for the full year.

Coinbase stopped directly disclosing its "total number of verified users" in its financial reports starting in Q4 2022 (when it was 110 million). According to the latest data from DemandSage, Coinbase's total number of verified users worldwide is expected to reach approximately 120 million by the end of 2025.

Furthermore, its stock performance has been heavily criticized. COIN's stock price has now fallen to its lowest level since March 2024.

Meanwhile, Matthew Sigel, head of digital asset research at VanEck, stated that Coinbase CEO Brian Armstrong sold another 40,000 shares of COIN on January 5th, worth approximately $10.16 million at the time. VanEck's chart further indicates that Brian Armstrong sold over 1.5 million Coinbase shares between April 2025 and January 2026, realizing approximately $550 million.

Transaction volume in Q4 2025 was 1.8 billion, but it has slowed down.

On February 13, Coinbase released its financial report, which detailed its financial data for the full year of 2025 and Q4, showing a pattern of both growth and hidden concerns.

For the full year, Coinbase's total trading volume (including spot and derivatives) increased by 156% year-over-year to $5.2 trillion, and its market share of crypto trading volume doubled to 6.4% (up from 3.2% in 2024 and 1.8% in 2023).

Subscription and service revenue also hit a record high of $2.328 billion for the year, a 65% increase from $1.407 billion in 2024.

Among them, the stablecoin business stood out, with the market capitalization of USDC rising to $76 billion (a significant increase from $38 billion in 2024 and $25 billion in 2023). The average USDC holding in Coinbase products reached $8 billion in Q4 (the full-year trend showed fluctuations but an overall upward trend, rising from $3 billion in Q4'23 to $18 billion in Q4'24, and then to $8 billion in Q4'25).

The number of paid Coinbase One subscribers reached 971,000, a significant increase from 733,000 in 2024 and 266,000 in 2023, with added value through new tiers and products such as the Coinbase One Card.

Q4 total revenue was 1.8 billion, but a loss of 667 million triggered a sharp drop in the stock price.

The company revealed in its financial report that 12 of its products have annualized revenues exceeding $100 million, half of which exceed $250 million and two exceed $1 billion.

Coinbase's transformation from a simple trading platform to an "Everything Exchange" covers areas such as crypto, derivatives, stocks, and prediction markets. However, the specific data for Q4 revealed short-term pressures, becoming the core driver of the stock price plunge.

Q4 total revenue was $1.8 billion, showing growth both year-over-year and quarter-over-quarter, but fell short of Wall Street's expectations of $1.95 billion.

Even more glaring is the net income: a loss of $667 million, turning into a deficit compared to the same period last year and Q3. This loss was mainly due to unrealized losses on strategic investments, volatility in crypto asset prices (assets such as Bitcoin retreated at the end of Q4), and increased operating expenses, including acquisition integration costs and regulatory compliance expenses.

Excluding these non-core factors, adjusted net income was $178 million and adjusted EBITDA was $566 million. Although these figures are positive, they represent a 12% decrease compared to Q3, indicating that core profitability is under pressure.

Trading fee revenue was $1.05 billion, and the company's cash and cash equivalents totaled $11.3 billion. Trading revenue, a traditional pillar, contributed approximately $1.05 billion in Q4 (accounting for about 55% of the full year), but trading volume slowed sequentially: while total trading volume reached $5.2 trillion for the full year, Q4 only saw about $1.2 trillion. Both retail and institutional trading were affected by market volatility, with average trading volume per trade decreasing by 15%. Spot trading volume declined by 10% year-over-year. Although derivatives trading was boosted by the Deribit acquisition, it failed to offset the user loss caused by bearish sentiment—monthly active trading users decreased by 800,000 sequentially to 9.5 million.

Subscription and service revenue reached $730 million in Q4, up 18% year-over-year but down slightly by 2% quarter-over-quarter. Breaking it down, stablecoin revenue (primarily USDC) was $380 million, benefiting from Base Chain integration and developer tools, but staking rewards fell to $120 million, declining 18% quarter-over-quarter due to lower network yields; interest and financial income was $65 million, and other service revenue was $165 million.

The balance sheet shows that the company's cash and cash equivalents reached $11.3 billion, an increase of $800 million from Q3, thanks to the accumulation of profits throughout the year. However, loan issuance and crypto investments (such as Bitcoin holdings) in Q4 resulted in a net decrease of $300 million in dollar resources.

The company's Bitcoin holdings were not updated in Q4, but the full-year trend shows a total holding of over 12,000 Bitcoins, with a total cost of approximately $800 million, an average price of $66,000 per Bitcoin, and a present value that fluctuates with the price of Bitcoin to approximately $1.1 billion (calculated based on a Bitcoin price of $90,000 at the time of the financial report). If calculated based on the Bitcoin price on February 13th, there would be a slight unrealized loss.

While SEC regulation has eased, a new round of competition in derivatives has intensified, with Binance expanding globally and Robinhood's crypto products eroding market share.

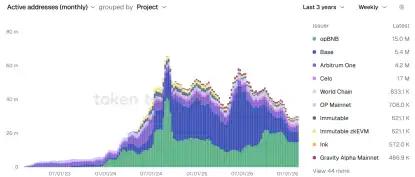

The financial report shows that Coinbase's 2026 priorities include expanding Everything Exchange, expanding stablecoin payments, and building on-chain finance. Coinbase's active addresses surpass those of Optimism and Arbitrum, and its TVL reaches $3.5 billion.

According to the latest data from token terminal, Base's weekly active users are now second only to opBNB.

The latest data from DefiLlama shows that Base's TVL has risen to $3.905 billion.

Overall, Coinbase's earnings report reveals the duality of the crypto giant: innovation-driven diversification throughout the year, but Q4 losses and weak trading expose its dependence on asset prices. The sharp drop in stock price is not just an emotional reaction, but also a test of the market's sustainability. Without a strong recovery or favorable regulatory environment in 2026, Coinbase will face even more severe challenges.