Terra's old case is being brought up again; why has Jane Street become the new villain in the crypto world?

Article author and source: Coinfound

In February 2026, a lawsuit filed in the Southern District of New York federal court reopened a three-year-old story from the crypto market.

The collapse of Terra in 2022 was once characterized as a disaster caused by the mechanism of algorithmic stability. Now, the liquidation lawyers have reconstructed the narrative with a single document: it was not an accident, but a meticulously calculated plunder, in which someone, with access to confidential insider information, precisely preemptively bought in the critical minutes before the collapse, turning the systemic crash into hedging profits in their individual books.

Even more bizarrely, just as the lawsuit was stirring up public opinion, the long-standing "ghost" in the Bitcoin market suddenly materialized: at 10 a.m. Eastern Time, the price plummeted precisely as if an alarm clock had been set, wiping out leveraged long positions within minutes, only to rebound as if nothing had happened. On social media, angry retail investors juxtaposed candlestick charts with court documents, highlighting the same name circled in red: Jane Street.

01 The whole story: Why was Jane Street thrust into the spotlight?

The source of this media storm stemmed from a legal counterattack in February 2026. Terraform's bankruptcy liquidation system formally sued Jane Street, reclassifying the 2022 systemic collapse as insider trading involving "someone jumping the gun at a crucial moment." The lawsuit's description of "secret information channels" and "minute-level trading windows" provided the public with a vivid causal chain, transforming the complex financial collapse into an easily understandable story of insider trading. When this news exploded on social media platforms like X, the community quickly created derivative works, elevating Jane Street from a low-profile TradeFi market maker to the position of the crypto world's "number one market manipulator."

Who exactly is Jane Street, the "villain" in this incident? In fact, Jane Street plays a pivotal role in the current Bitcoin ecosystem. As a leading global liquidity provider, it is one of the very few Authorized Participants (APs) with "in-kind creation and redemption" capabilities for top spot Bitcoin ETFs like IBIT. This deep-seated vested interest makes any rumors of market manipulation extremely damaging. Worse still, this isn't the first time this giant has been embroiled in such controversies. In 2025, the Indian regulator SEBI accused it of manipulating indices through derivatives and seized a large amount of "illicit gains." This "past record" creates a preconceived notion in the public: given its history of similar practices in other markets, structural exploitation in the Bitcoin market seems perfectly plausible.

Ultimately, this long-suppressed distrust found its outlet in the hotly debated "10am dump" phenomenon surrounding Bitcoin. Retail investors' long-standing experience of Bitcoin's fixed fluctuations at 10 AM Eastern Time, triggering widespread liquidations, found a concrete explanation at this moment. The originally complex and opaque ETF creation, redemption, and hedging mechanisms were simplified into a conspiracy theory narrative of "giants using black-box mechanisms to dump shares and cover their positions." Thus, the old Terra case, regulatory controversies in overseas markets, and Bitcoin's price patterns completed a logical loop, collectively placing Jane Street under intense scrutiny.

02 Old Case Resurrection: Terra Rekindles the Flames in 2026

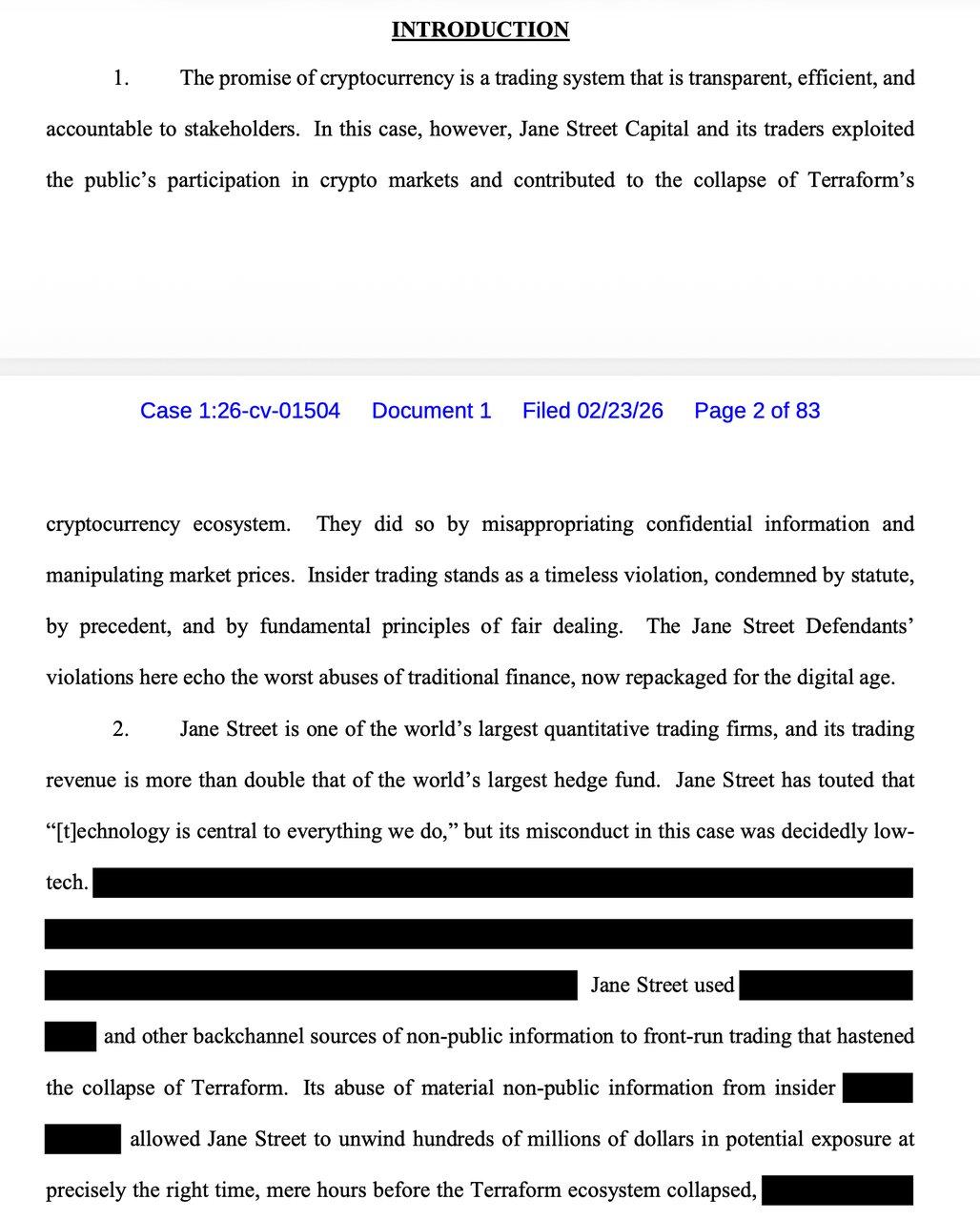

In February 2026, a lawsuit filed in the Southern District of New York federal court suddenly brought the long-dormant Terra crash case back into the spotlight. Todd R. Snyder, administrator of the Terraform bankruptcy liquidation firm Wind Down Trust, accused Jane Street, a top Wall Street market maker, of insider trading and securities fraud. The core of the lawsuit points to a very explosive proposition: the crash in May 2022 may not have been just a systemic failure of algorithmic stability, but a premeditated preemptive move.

The lawsuit paints a dramatic and conspiracy-ridden picture. Jane Street employee Bryce Pratt maintained clandestine communications with Terraform's research head on Telegram, with conversations even containing explicit confidentiality messages like "don't share pls." More dramatically, this Terraform executive was seeking a position at Jane Street at the time, and the ambiguous nature of their relationship provided fertile ground for the flow of "significant non-public information." The massive 85 million UST swap of May 7, 2022, which the lawsuit claims was the largest single swap in Curve 3pool's history, became the final straw that broke the camel's back for the Terra ecosystem. In this lawsuit, the plaintiffs are seeking to recover all unjust enrichment from Jane Street to compensate the victims, while Jane Street vehemently denies the allegations, emphasizing that the lawsuit lacks factual basis. Because crucial evidence is largely hidden in public documents, this Rashomon-like mystery is far from being solved.

Source: Snyder v. Jane Street Group, LLC, et al., No. 1:26-cv-01504 (SDNY Feb. 23, 2026) (Complaint), ECF No. 1.

However, the uncertainty within the courtroom did not prevent a conviction outside of it. The lawsuit's viral spread on social media was largely due to Jane Street's prior criminal record, which had already been a significant factor in another news story. Just six months prior, the Indian market regulator SEBI had levied a hefty fine against her for manipulating stock indices, restricting her access to the Indian securities market and seizing approximately $567 million. Although Jane Street defended the transactions as "basic index arbitrage," public opinion had already simplified it to a "manipulation history." When Terra's accusation of "using information advantage to trade at critical windows" echoed the SEBI case's claim of "profiting from influencing market prices," public prejudice was self-confirmed.

Once this cross-market "pattern recognition" was established, it quickly found its most concrete manifestation in the crypto market: the "10am dump" phenomenon that had plagued bulls for months!

Jane Street, with its dual identity spanning both traditional finance and the crypto market, suddenly made an "aha" moment when the lawsuit revealed that its employees were suspected of using informational advantages to preemptively trade within minute-by-minute windows. Traders on Twitter suddenly realized that the strange selling pressure that appeared precisely at 10 a.m. every day and the instantaneous crashes that accurately harvested liquidity might just be the same logic being repeated in different markets.

This narrative of "post-hoc attribution" quickly took shape in several viral tweets. Crypto community KOL Bark ( @barkmeta ) described Jane Street as a dumping machine that started precisely at 10 a.m. every day, claiming that this pattern "magically disappeared" after the lawsuit was exposed, and Bitcoin subsequently rebounded strongly. Bull Theory, AshCrypto, and others further constructed a complete "market manipulator playbook": accumulation, dumping, and buying back at low prices, juxtaposing the "early bird" crash of Terra in 2022 with the current "10 AM manipulation."

The "Bryce's Secret" in the lawsuit was simplified into meme material, and the "accusations" in court were compressed into "concrete evidence" on social media. When the slowness of the legal process met the urgency of the trial by public opinion, Jane Street had already lost this "witch hunt" on Twitter.

03 10am dump: From pattern observation to the spread of conspiracy theories

In the whispers of crypto traders, the "10am dump" is like a cursed alarm clock. Every day at 10 AM Eastern Time, the Bitcoin market experiences a bizarre plunge: the price drops sharply by 1% to 3% in a short period, precisely triggering a liquidation waterfall for leveraged long positions. This highly regular fluctuation, when the account "Negentropic," jointly maintained by Glassnode co-founders Jan Happel and Yann Allemann, recorded "The Monday 10am Slam" on December 15, 2025, finally transformed this previously scattered feeling into a spreadable meme, quickly evolving from a trading sensation into a nationwide witch hunt.

The "ironclad evidence" of this witch hunt first came from the bizarre coincidences in timing. When prominent accounts like Negentropic aligned screenshots of minute charts from multiple days, proving that the declines almost always occurred within the same time window, the community's anger was ignited. This extreme synchronization is difficult to explain as random fluctuations; it's more like some algorithm pressing the sell button at a fixed moment. The frenzy reached its climax when the Terra lawsuit was made public in February 2026. Bloggers like Bark pointed out that since Jane Street's lawsuit was exposed, the "10 a.m. dump," which had lasted for months, miraculously disappeared. This narrative of a natural experiment—a "post-event pattern change"—convinced countless people that Jane Street was the culprit behind the "10 a.m. dump."

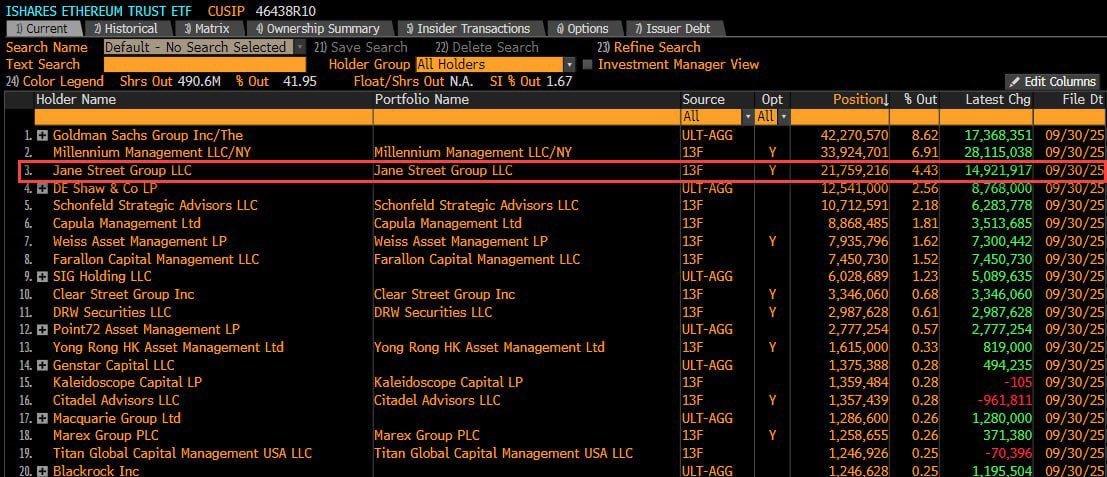

In the "10am dump" controversy, Jane Street's 13F filings were repeatedly cited as a key piece of the puzzle because they grounded the abstract notion of "possible institutional activity" into quantifiable public figures. According to publicly available 13F information, in the fourth quarter of 2025, they disclosed holding 20,315,780 IBIT shares, worth approximately $790 million, and added 7,105,206 shares, worth approximately $276 million, during the same quarter, bringing their total holdings to nearly $2.5 billion. In a market rife with distrust, this data was quickly interpreted as an extremely sinister profiteering logic: market makers, leveraging the access advantages of AP institutions, would first create sell-offs at fixed times to trigger liquidations, amplifying panic and forcing retail investors to sell their shares at a loss, then quietly buy back at lower prices, ultimately presenting the financial statements as "institutions accumulating shares on dips."

Source: WhaleFactor

However, this detective-fiction-like closed loop of motivation is seen by professional institutions as a huge misinterpretation of common sense. The 13F report is like a photograph taken from only one side; it mandates disclosure of long positions in stocks like IBIT, but never requires disclosure of corresponding hedging positions such as options, futures, or swaps. In other words, those seemingly huge holdings are most likely "Delta-neutral" inventories held simply to hedge derivatives risk; the institutions have no intention of betting on price movements. Macro trader Alex Krüger went even further, presenting statistical backtesting: the so-called 10 AM crash is, in data, closer to a risk repricing of Bitcoin following the Nasdaq index, rather than a systemic, targeted sell-off.

Even acknowledging the existence of the phenomenon, alternative explanations are far more mundane than "market manipulation": 10 AM coincides with the peak period of liquidity restructuring after the US stock market opens. If the leverage ratio in the derivatives market is too high and the order book depth is insufficient at this time, any medium-sized sell order, whether it's a hedging flow from ETF creation and redemption or cross-asset rebalancing, could trigger a chain of liquidations. The structure itself creates a waterfall.

In addition, there's the factor of flow. The shift of funds between spot and derivatives alters the demand-side slope for the day. This isn't used to attribute "who is selling," but rather to characterize whether the demand side provided stronger support that day. For example, on February 25, 2026, CoinFoundry data showed a net inflow of approximately $664 million into crypto ETFs, with about $507 million into BTC and about $157 million into ETH. Placing this type of fund flow and price behavior on the same timeline allows for a clearer distinction between two explanatory paths: "stabilization due to increased demand" and "behavioral changes triggered by a single event."

Source: WhaleFactor

However, this detective-fiction-like closed loop of motivation is seen by professional institutions as a huge misinterpretation of common sense. The 13F report is like a photograph taken from only one side; it mandates disclosure of long positions in stocks like IBIT, but never requires disclosure of corresponding hedging positions such as options, futures, or swaps. In other words, those seemingly huge holdings are most likely "Delta-neutral" inventories held simply to hedge derivatives risk; the institutions have no intention of betting on price movements. Macro trader Alex Krüger went even further, presenting statistical backtesting: the so-called 10 AM crash is, in data, closer to a risk repricing of Bitcoin following the Nasdaq index, rather than a systemic, targeted sell-off.

Even acknowledging the existence of the phenomenon, alternative explanations are far more mundane than "market manipulation": 10 AM coincides with the peak period of liquidity restructuring after the US stock market opens. If the leverage ratio in the derivatives market is too high and the order book depth is insufficient at this time, any medium-sized sell order, whether it's a hedging flow from ETF creation and redemption or cross-asset rebalancing, could trigger a chain of liquidations. The structure itself creates a waterfall.

In addition, there's the factor of flow. The shift of funds between spot and derivatives alters the demand-side slope for the day. This isn't used to attribute "who is selling," but rather to characterize whether the demand side provided stronger support that day. For example, on February 25, 2026, CoinFoundry data showed a net inflow of approximately $664 million into crypto ETFs, with about $507 million into BTC and about $157 million into ETH. Placing this type of fund flow and price behavior on the same timeline allows for a clearer distinction between two explanatory paths: "stabilization due to increased demand" and "behavioral changes triggered by a single event."

When such institutions are deeply embedded in the BTC ETF ecosystem, they become the most typical point of conflict between TradeFi and Crypto. On the one hand, ETFs need them to provide liquidity and arbitrage opportunities to ensure that ETF prices do not deviate from their net asset value in the long term. On the other hand, crypto traders naturally regard them as representatives of "black box systems" because their risk management does not occur publicly on-chain.

privileged access

The creation/redemption mechanism of ETFs was originally designed for arbitrage. Authorized participants (APs)—such as Jane Street, JPMorgan Chase, Macquarie, and Virtu, listed in the IBIT disclosure list—can exchange a basket of Bitcoin for ETF shares, or vice versa, thereby eliminating the discrepancy between the ETF price and its net asset value. This mechanism has operated unchallenged in the stock market for years, but it has sparked unusual outrage in the Bitcoin world.

The conflict stems from a lack of transparency. Crypto culture is built on the belief in "on-chain verifiability," while the AP mechanism is essentially a black box off-chain. Especially after the SEC approved "in-kind" in July 2025, AP's risk management path became even more untraceable. They can hedge with futures instead of real-time spot trading, settle in batches via OTC, and use inventory and lending tools to smooth out shocks. When retail investors see a sharp drop and rebound at 10 o'clock on the market, they see "manipulation"; while AP only sees the execution of arbitrage orders. As for which exchange the shock occurred on and at what pace, it is all locked in TradeFi's confidentiality protocol.

This "legitimate black box" has become a breeding ground for misunderstandings. In the 24-hour trading market with no price limits, AP's normal hedging logic is naturally translated as "structural manipulation"—not because the evidence is conclusive, but because it is the only narrative that crypto natives can understand, used to explain those recurring fluctuations that cannot be verified on-chain.

A more subtle informational advantage stems from AP's "perception" at the forefront of liquidity. Compared to the raw insider information reliance on Telegram private chats in the Terra case, the advantage in the ETF era is more like a structural "traffic advantage." As the gatekeeper of the creation and redemption channels, AP feels the pressure of capital inflows and outflows earlier and more directly than the market. This advantage doesn't require predicting any news; simply being a few seconds faster than others in handling risk hedging can create huge profit margins at the execution level. In the crypto culture, which highly values "code is law" and "ledger transparency," AP's operating method of moving between multiple markets while keeping the execution details in an off-chain black box is a natural breeding ground for conspiracy theories.

This lack of transparency explains why 13F reports have become the epicenter of misinterpretations. Market makers' large-scale increases in IBIT holdings don't necessarily mean they are "bullish" on Bitcoin; it's more likely they're simply fulfilling their market-making needs with "nominal inventory." As former hedge fund manager Michael Green stated, interpreting such positions as directional bets is unreasonable because market makers' books are always two-sided: you see them holding a lot of spot, but you don't see them locking in risk with short positions on the other side. As long as disclosure rules allow for this "semi-transparency," the public will never be able to distinguish between legitimate risk hedging and deliberate price manipulation. This cognitive gap is precisely the root cause of the weakness and ineffectiveness of those holding the "non-manipulation" viewpoint.

05 The Logical Chain of the Market Opponent's "Non-Manipulation Theory"

As this extreme asymmetry of information power continues to fester, Jane Street seems to have fallen into a vicious cycle from which it cannot prove its innocence. However, outside the clamor of public opinion, numerous analysts and professional institutions offer a completely different perspective. They believe that the current accusations regarding the "10am dump" are more like forcibly escalating an observable fluctuation into an unproven conclusion of manipulation. They do not deny the existence of institutional advantages in the market, nor do they deny that selling pressure is more likely to occur at certain times; their only point of contention is the lack of a closed chain of evidence.

The first hurdle is the attribution threshold. To prove that an institution systematically dumped shares at a fixed time, at least three questions must be answered: who was selling, how much was sold, and through what path was the price transmitted to the spot market? Most of the materials circulating in the community currently only involve price action and liquidation screenshots, which can show "the price dropped during that period," but cannot identify "who the sellers were." Manipulation allegations require transaction-level evidence, such as attributable order flows, account-level attribution, or regulatory filings that match. Without these, it remains merely speculation and "urban legend."

This also corresponds to the fact that professional media are generally more restrained. When sorting out this controversy, CoinDesk emphasized that social media pieced together multiple fragments into a story, but the evidence was insufficient to draw conclusions about specific institutions, especially the point that "Jane Street must be the seller".

Another opposing argument is based on statistical evidence. Macro trader Alex Krüger's response, cited in numerous reports, directly examines window returns, concluding that the narrative of a "fixed sell-off at 10 am" is inconsistent with the data. His statistical analysis shows that since January 1, 2026, IBIT's cumulative return was +0.9% between 10:00-10:30 and -1% between 10:00-10:15. This does not indicate a systemic decline. More interestingly, the performance pattern in these two windows closely resembles that of the Nasdaq index. Therefore, he argues that the overall trend is closer to noise and a synchronized repricing of risky assets.

Source: Alex Krüger

Professional institutions, however, chose to refute the "manipulation theory" using market mechanisms. CryptoQuant pointed out that many funds buy spot while simultaneously selling futures to create delta neutrality, earning basis or managing risk. This approach is common in institutional trading and is not exclusive to any particular company.

The key point of this explanation is that the price shocks seen externally are not equivalent to "someone dumping in the spot market." Institutions can first change their risk exposure through derivatives, and then gradually execute delivery in the spot or OTC markets. For retail investors, the same result may be seen: a sudden fluctuation around 10 o'clock, increased liquidation, but the underlying trading path may be completely different.

However, when market liquidity is insufficient and order books become thin, these normal arbitrage and rebalancing pressures will be amplified exponentially.

06 Conclusion

The media storm that erupted in early 2026, when Terra's liquidation lawsuit came to light, struck not only at the root of discontent with the opaque mechanism, but also at the long-simmering collective anxiety within the crypto market and the pent-up market sentiment stemming from the "10am dump" phenomenon. Those leveraged long positions repeatedly liquidated within fixed time windows, and retail investors passively forced to take losses during market volatility, were already searching for a "systemic explanation." Thus, when Negentropic wrote, "After the lawsuit was made public, the 10am dump miraculously disappeared," the fragility of the logical chain became irrelevant. In the desert of complexity, humanity's thirst for "conspiracy" far outweighed its tolerance for "randomness."

If we shift our perspective beyond "whether a certain company is manipulating the market," this controversy is more like a structural friction arising from the integration of TradeFi ETF infrastructure into Crypto, rather than the independent will of a single institution.

First, APs are essentially infrastructure entities. They are not a channel accessible to everyone in the market, but rather a limited number of approved institutional seats responsible for completing ETF creation and redemption, thereby maintaining the alignment of ETF prices with net asset values. For example, in the IBIT filing, only four authorized participants were authorized, including Jane Street.

Secondly, AP's profit model is closer to structured arbitrage and risk hedging. Their goal is usually to use price differences and execution advantages to pull prices back to a reasonable range and manage exposure through cross-market hedging, rather than "betting on the direction." However, when this mechanism is applied to a 24-hour high-leverage market like BTC, external observers only see price shocks and liquidation waterfalls, not the hedging path, inventory management, and order splitting. Therefore, "arbitrage and hedging" can easily be interpreted as "structured market crash."

More importantly, the institutional changes have further amplified the potential for misinterpretation. Especially after the SEC approved "in-kind" transactions in 2025, the implementation of APs (In-Kind) became more flexible, making it harder for outsiders to deduce the true path from the surface appearance of the commodity. This set of rules has been operating smoothly for many years on traditional stock ETFs because trading hours, volatility structures, and regulatory disclosure practices are more mature. However, transferring it to Bitcoin will trigger a stronger clash of values: the crypto world emphasizes transparency and verifiability, while the ETF mechanism emphasizes efficiency and mediated execution. Therefore, the points of conflict will persist for a long time.

The real lesson from this is that we are undergoing an infrastructure migration. Institutional funds are entering BTC not simply by buying spot on exchanges, but through traditional financial channels like ETFs, bringing with them a complete and mature system of market making, hedging, subscription and redemption, and risk management. This brings stronger capital absorption capacity, but also greater opacity and explanation costs.

Therefore, it is even more important to ask whether the price discovery mechanism is sufficiently explainable and auditable. As long as the market remains in a combination of "high leverage + multi-market execution + delayed disclosure," any seemingly regular fluctuations will be quickly attributed to a few institutional seats, and conspiracy theories will periodically resurface.

The truth behind this controversy remains shrouded in the gray area where TradeFi and Crypto intersect. While the community has pieced together a seemingly logically closed-loop "manipulation model," the lack of exchange-level order flow attribution and auditable execution ledgers renders these accusations legally and statistically untenable. Conversely, although professional institutions have offered explanations such as "normal hedging" and "risk pricing," these explanations are insufficient to fully quell market concerns about structural exploitation given the inherent lag in disclosure mechanisms and the highly centralized nature of AP authority.

Before the next "10 o'clock" hour begins, what we really need is an auditing logic that is more scientific than conspiracy theories and more transparent than market makers' explanations.