BTC, ETH, SOL, XRP, DOGE, SHIB.

These names were included in SEC regulatory filings for the first time, with the words "not securities" added after them.

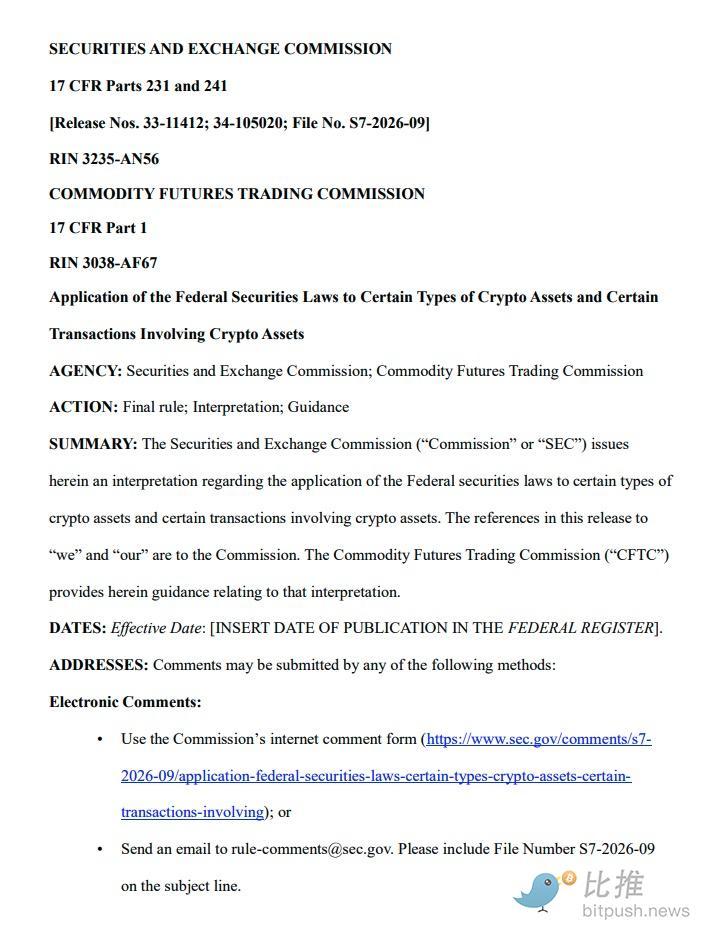

On the evening of March 17, 2026, the SEC and CFTC jointly released a 68-page explanatory document, formally defining the security attributes of crypto assets. This marks the first time at the U.S. federal level that a formal regulatory interpretation has been issued, naming specific tokens and providing classification conclusions. The document also replaces the SEC's old "Investment Contract Analysis Framework" released in 2019, which had been a primary reference for industry compliance assessments.

The release of this document follows a clear timeline.

In January 2025, Acting SEC Chairman Mark T. Uyeda established the Crypto Task Force specifically to clarify the applicability of securities laws to crypto assets. In July of the same year, the President's Working Group on Digital Asset Markets released a report recommending that the SEC and CFTC utilize their existing powers to provide regulatory clarity to the industry.

SEC Chairman Paul S. Atkins subsequently launched Project Crypto, which was upgraded to an SEC-CFTC joint project in January 2026. During this period, the Crypto Task Force received more than 300 public comments from issuers, investors, law firms, auditing firms, and other parties.

In other words, this document represents a "unified answer" from the two federal regulatory agencies after more than a year of industry negotiations and policy coordination.

Five lines to draw the entire map

In this document, the SEC categorizes crypto assets into five classes. The core criterion is the four elements of the Howey Test.

The first category is "Digital Commodities." This is the most attention-grabbing part of the entire document because the SEC provided a specific list. BTC, ETH, SOL, XRP, ADA, AVAX, DOGE, SHIB, LINK, DOT, LTC, BCH, HBAR, XLM, XTZ, and APT—a total of 16 tokens—are explicitly listed in the main text. The footnotes also mention that Algorand (ALGO) and LBRY Credits (LBC) belong to this category.

The SEC's reasoning is that the value of these tokens is intrinsically linked to the programmatic operation of the functional crypto system in which they reside, driven by supply and demand, rather than by the expectation of profit from the management efforts of others.

The second category is "Digital Collectibles." CryptoPunks, Chromie Squiggles, WIF (dogwifhat), and VCOIN were specifically mentioned. Memecoin found its place here; the SEC considers its value to be driven by "artistic, entertainment, social, or cultural significance," similar to physical collectibles, and therefore does not constitute a security.

The third category is "Digital Tools." ENS domains and CoinDesk's Microcosms NFT tickets are cited as examples. These assets are characterized by performing practical functions, such as membership credentials, identity markers, and property certificates; many are soul-bound and non-transferable.

The fourth category is "stablecoins." Under the passed GENIUS Act, "payment stablecoins" issued by compliant issuers are explicitly excluded from the definition of securities. However, the SEC retains jurisdiction over stablecoins that do not meet the standards of the Act.

The fifth category is "Digital Securities." This is the only category explicitly identified as securities. However, the SEC did not name any specific tokens that fall into this category in its filings.

The boundaries between these five categories are not absolute. The SEC itself acknowledges the existence of hybrid assets that cross categories, as well as crypto assets that do not belong to any category. However, the significance of this classification framework lies in the fact that, for the first time, it has brought the question of "what is a security and what is not" from courtroom debate to the level of regulatory enforcement.

Four types of on-chain behavior, uniformly defined

Beyond token classification, another major contribution of this document is the unified definition of four core on-chain behaviors: mining, staking, packaging, and airdrops.

Protocol mining does not constitute a securities offering. Whether mining individually or in a mining pool, the mining activity itself is a network maintenance activity, and the newly produced tokens are programmatic rewards at the protocol level, without involving an investment contractual relationship.

Protocol staking does not constitute a security offering. This determination covers four scenarios: individual staking, staking with a third party while retaining the key, staking with a custodian, and liquidity staking. The SEC clarifies in its filings that staking yields derive from a programmatically pre-defined allocation within the protocol, not from the operational efforts of a management team. Regarding LST (such as stETH) generated from liquidity staking, the SEC considers them merely "receipts" of the underlying staked assets, not derivatives, and not securities.

Asset wrapping does not constitute a securities offering. Wrapping BTC into WBTC for use on Ethereum is merely a technical interoperability operation and does not change the nature of the underlying asset.

Airdrops do not constitute a security offering. Free token distributions do not meet the "contribution of funds" requirement of the Howey Test unless the recipient provides funds, goods, or services as consideration.

The direct impact of these assessments on the industry is that the core mechanisms of DeFi protocols—staking, wrapping, and airdrops—have all been removed from the scope of securities laws. The concerns that every project operating a staking service or issuing airdrops has been worried about for the past three years now have a unified answer from federal regulators.

Securities identity is not a permanent label

The most noteworthy part of this document is likely the SEC's explanation of the "separation" mechanism. The document explicitly states that a crypto asset that is not inherently a security can be subject to securities regulation due to its issuance method (such as offering it through an investment contract). However, when the conditions of the investment contract are no longer met, this asset can be "separated" from its security status.

The SEC outlined two scenarios for delisting. The first is when the issuer fulfills its promise. For example, if a project promises to develop a decentralized network during its ICO, and once the network is launched and operates in a decentralized manner, investors no longer need to rely on the management efforts of the issuing team to profit. The core requirements of the Howey Test are no longer met, and the tokens "graduate" from the investment contract.

The second scenario is more interesting: the project owner "abandons" the investment. If the issuer ceases to fulfill its promises and statements in the investment agreement, the investor's reasonable expectation of "profits generated by the efforts of others" is shattered, and the investment agreement terminates. However, the SEC emphasizes that this does not mean the issuer can escape liability; they may still face charges of fraud.

The true significance of this "stripping" mechanism lies in providing a compliant path for crypto projects. From ICOs to mainnet launches to full decentralization, it's no longer an adventure in a legal gray area, but a regulatory tunnel with a clear destination. Once you've completed it, you're out.

68 pages. Nine chapters. 18 named tokens, 6 defined on-chain behaviors, and 2 "graduation" paths. The SEC spent over a year collecting more than 300 submissions, and finally, in collaboration with the CFTC, delivered this report. It's not perfect; the boundaries of stablecoins remain ambiguous, no specific examples are given under the "digital securities" category, and the criteria for judging hybrid assets are also left open to interpretation.

But for an organization that has been criticized in the past for "replacing regulation with enforcement," this document has at least done one thing: it puts the rules on paper instead of in a lawsuit.

Click to learn about BlockBeats' job openings.

Welcome to the official BlockBeats community:

Telegram subscription group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Official Twitter account: https://twitter.com/BlockBeatsAsia