Written by: @TradesMax

The core issue in Monday's trade was actually quite clear:

On one hand, Federal Reserve Chairman Powell released a dovish signal, or at least indicated that he was not in a hurry to turn hawkish, which provided some support to the bond market and risk sentiment.

On the other hand, the conflict in the Middle East continues to escalate, and oil prices have climbed back above $100. Market concerns about "high oil prices + high interest rates + slowing growth" have not been averted.

As a result, US stocks opened higher but then weakened throughout the day, eventually closing with a typical defensive performance.

Pre-market testing

The pre-market market wasn't too bad. After last week's continuous pullback, US stock futures initially rebounded modestly, with traders betting on two things:

First, the previous decline was already significant, and a short-term technical correction is possible;

Secondly, Trump's pre-market comments about discussions with a "more rational government" in Iran led some funds to trade temporarily based on the assumption that "the situation may not continue to escalate rapidly." This pre-market rebound was essentially a test of risk appetite.

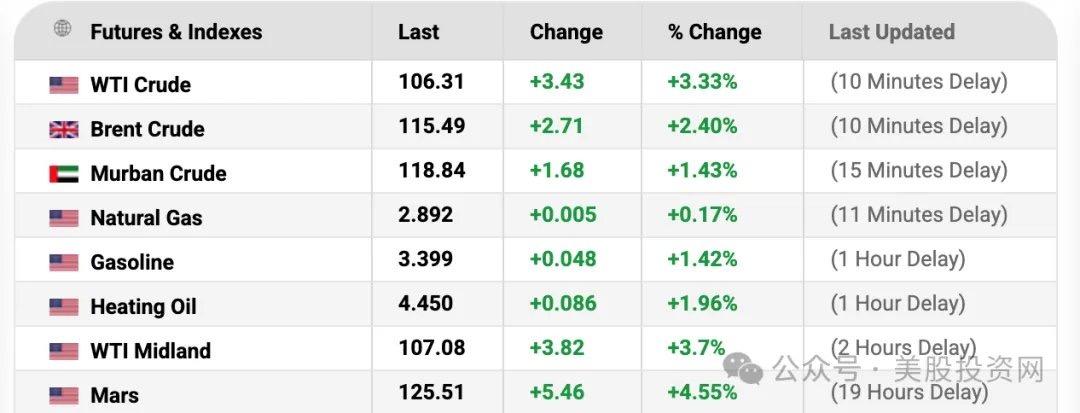

However, this test of risk appetite is extremely fragile because the most fundamental macro asset—crude oil—has not given any supporting signals. Pre-market WTI crude oil futures have already approached $102 again, while Brent crude has risen to a high of around $116.

Oil traders are still paying a very high risk premium for the potential blockade of the Strait of Hormuz. Without a substantial decline in oil prices, the rebound in futures indices lacks solid macroeconomic fundamental support and is destined to be short-lived.

Opening price surged

The Dow Jones, S&P 500, and Nasdaq all opened higher, with the S&P 500 rising nearly 0.9% at one point. This indicates that the market initially attempted to treat the previous continuous decline as an "oversold correction" during the opening phase. However, this rebound was short-lived.

According to US Stock Investment Network, the S&P 500 quickly gave back its gains after an early morning surge, and then entered a period of consolidation and weakness. In other words, Monday's market did not immediately plummet from the open, but rather there was an initial attempt to stabilize, which was later interrupted by stronger macroeconomic variables.

Key variables in the trading session

In his speech that day, Powell clearly conveyed a "no-hawkish stance" signal: he emphasized that current US monetary policy is "in the right place," and the Fed will not rush into a response to the supply-side energy shocks driven by war and rising oil prices. The Fed will remain "on the sidelines" until it assesses the long-term impact of the conflict on the economy.

This statement had an immediate calming effect on the US Treasury market, with the 10-year Treasury yield quickly falling back to around 4.34%. However, a highly alarming cross-asset divergence signal emerged: oil prices were soaring, while US Treasury yields were falling (bonds were being bought).

According to the classic macro trading framework, soaring oil prices typically drive up long-term inflation expectations, leading to bond sell-offs and rising yields. However, Monday's trading session showed the opposite. This reveals a shift in the logic of major Wall Street funds—bond market traders are no longer simply trading on an "inflation rebound," but have begun to pre-price the risk of "high oil prices backfiring on the real economy and triggering a recession."

Faced with such recessionary expectations, Powell's verbal reassurances seemed weak and ineffective. He admitted that it was "too early" to assess the geopolitical impact, meaning that the Federal Reserve was merely holding back and had not truly begun a new easing cycle.

According to the latest pricing in the interest rate swap market, funds have clearly withdrawn their bets on a rate cut this year, and have even begun to re-indulge in the possibility of another rate hike this year.

Oil price-driven

What truly brought the index down from its highs was the Middle East. On Monday, while continuing to express his willingness to negotiate, Trump also reiterated that if the Strait of Hormuz issue was not resolved, the United States might strike Iranian oil wells, power generation facilities, and key export infrastructure.

In the afternoon, as Trump reiterated his strong threat to "completely destroy" Iranian oil and gas facilities, coupled with the Iranian parliament's tough response to the Strait of Hormuz toll bill, the market completely gave up resistance. The market's main theme shifted unilaterally from "Fed dovish stance" to "oil shock," and the stock index subsequently weakened in a one-sided oscillation.

From a broader perspective, Monday's market also presented a new and more noteworthy signal: verbal reassurances are becoming increasingly ineffective in altering price direction on their own.

Finance Minister Bessant stated that the global oil market remains well-supplied and that control over the Strait of Hormuz will be gradually restored to achieve freedom of navigation, with US or multinational escort options available. However, judging from asset price reactions, traders did not significantly lower their risk premiums. Oil prices did not fall noticeably, and US stocks did not see a significant rebound.

This indicates that what the market truly lacks is not rhetoric, but rather policy actions that can substantially reduce risk premiums. The market is gradually shifting from simple headline trading to trading based on whether or not intervention will be taken as the final step.

Sector Performance

Looking at sector performance, technology stocks were the heaviest drag on the overall market throughout the day, with the Philadelphia Semiconductor Index plunging over 4.2%. Besides the valuation pressure from high oil prices, the impact of Google's new storage technology potentially significantly reducing reliance on hardware led to a plunge in memory module spot prices, triggering deep panic on Wall Street regarding a possible peak in the AI hardware cycle. High-duration, high-valuation memory chips were hit hardest, with Micron Technology ($MU) plummeting nearly 10% and Western Digital ($WDC$MU$WDC) plunging 8.6%.

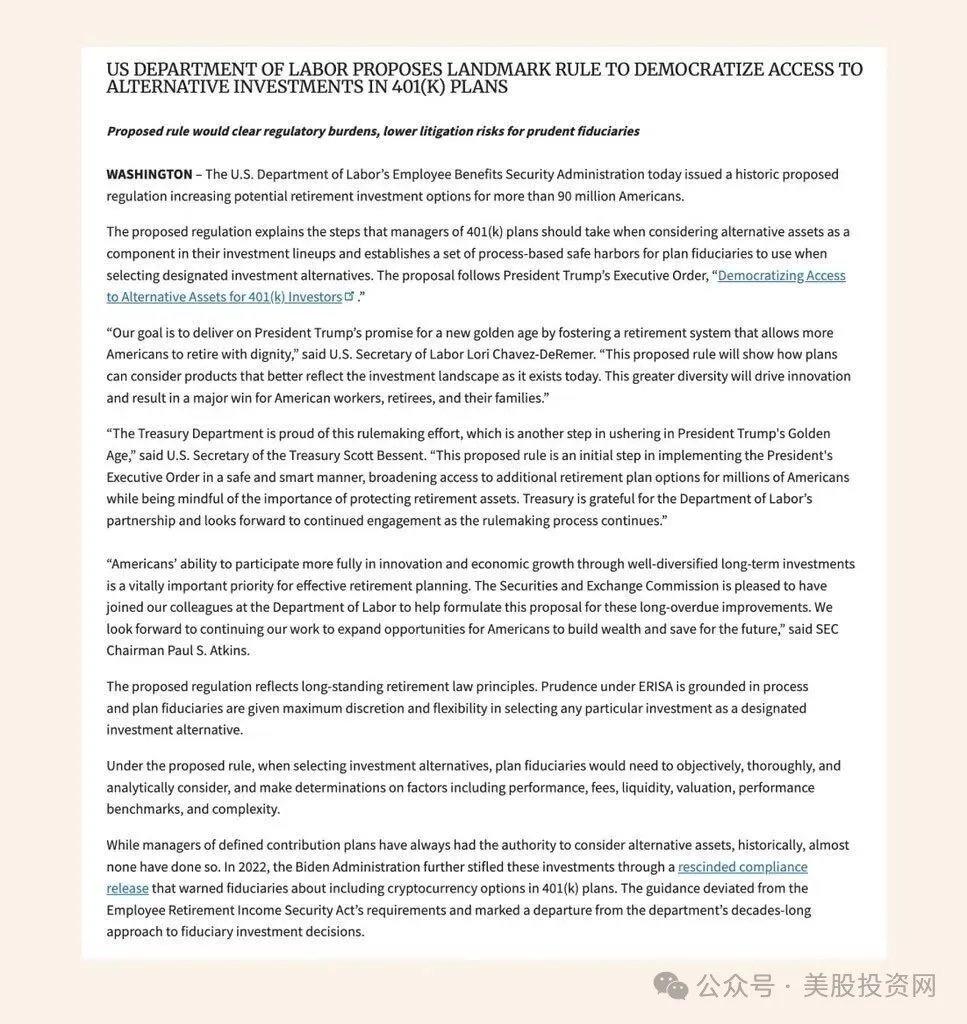

A relatively bright spot was the financial sector (which closed up 1.1%). Its core driver came from a significant draft guidance released by the U.S. Department of Labor—clarifying that trustees can add alternative assets to 401(k) retirement plans. (This policy exposure is also expected to benefit assets such as Bitcoin in the future).

This means that pension funds, amounting to trillions of dollars, are about to open their doors to private equity and credit. Asset management giants surged in response, with Blackstone Group ($BX) closing up 3.3% and KKR ($KKR) closing up 2.1%.

Furthermore, stimulated by Bill Ackman's bullish remarks, Fannie Mae ($FNMA) and Freddie Mac ($FMCC$FNMA$FMCC) surged by over 51% and 47% respectively, staging a rare short squeeze.

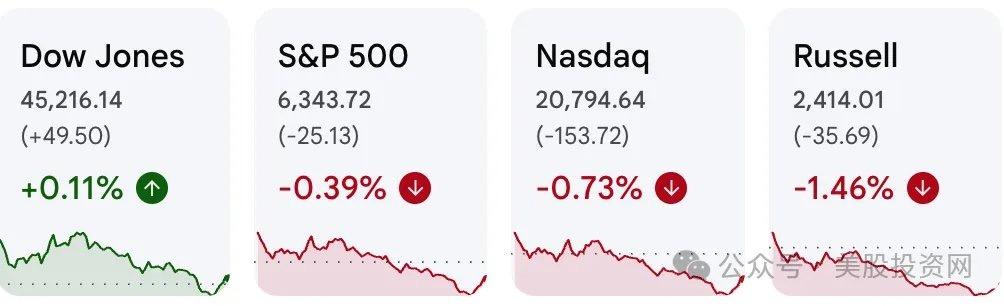

At the close, the Dow Jones Industrial Average rose 0.11%; the S&P 500 fell 0.39%; the Nasdaq Composite fell 0.73%; and the Russell 2000 fell approximately 1.5%.

According to US Stock Investment Network, the S&P 500 has fallen about 9.1% from its year-to-date high, and major indices including the Dow Jones, S&P 500 and Nasdaq have all fallen more than 10% from their respective highs. The market as a whole is still in a technical adjustment zone, and the recovery in risk appetite is far from solid.

Divergence on Wall Street is intensifying. Wolfe Research recommends holding defensive positions; Morgan Stanley believes the sell-off is nearing its end and market concerns about growth have been overblown; Goldman Sachs is relatively optimistic, believing that as long as the conflict doesn't spiral out of control, the S&P 500's 12% earnings growth benchmark for this year remains solid. US Stock Investment Network analysts believe Monday's market action conveyed a reality: Powell may be able to temporarily curb a "more hawkish Fed," but he cannot suppress "more expensive oil" out of thin air. Until the Middle East conflict reaches a substantial and clear conclusion, market pricing power lies not in the Fed's hands, but in supply expectations in the oil market.

Before the Q1 earnings season truly reveals corporate profitability in mid-April, maintaining sufficient cash reserves and avoiding overvalued technology companies lacking cash flow support remains the safest strategy at present.