Chainfeeds Summary:

Stablecoin issuers are now the 19th largest holders of U.S. Treasury bonds, holding assets that are essentially the same as the underlying assets that underpin your savings account. Whether they are allowed to distribute the returns generated by these assets to users is becoming one of the most critical issues in current crypto legislation.

Article source:

https://x.com/Delphi_Digital/status/2039039384910282832

Article Author:

Delphi Digital

Opinion:

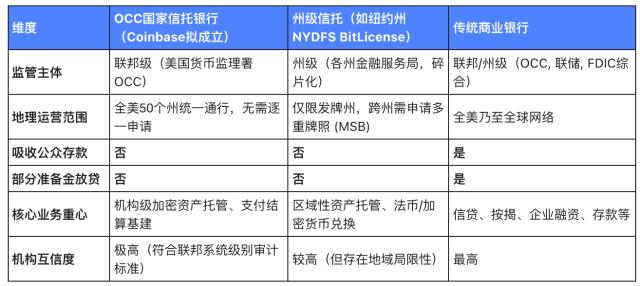

Delphi Digital: In recent months, fintech and crypto companies have been actively seeking banking licenses through direct applications or acquisitions. Following the global financial crisis, the US virtually halted the issuance of new commercial banking licenses for nearly a decade, with the number of new banks plummeting from approximately 132 per year to just 6. When licenses were scarce, the market opted to "build services around banks"; now, this trend is reversing, with more and more companies aspiring to "become their own banks." For crypto-native companies and stablecoin issuers, obtaining a federal license means access to FedNow and Fedwire, and direct control over the settlement layer; for traditional fintech companies, it means breaking free from dependence on third-party banks and achieving full-chain vertical integration. This integration is bidirectional. In December 2025, the Federal Deposit Insurance Corporation (FDIC) approved a proposal allowing regulated state banks to issue payment-type stablecoins through subsidiaries; in February 2026, the Office of the Comptroller of the Currency (OCC) also proposed similar rules. Once implemented, any qualified depository institution will have a legal path to issue stablecoins. Stripe is a prime example. By acquiring Bridge, Privy, and Metronome, and partnering with Paradigm to develop Tempo, Stripe is building a complete payment system from issuance to merchant settlement. This is not an isolated case. The stablecoin technology stack is mapping layer by layer with the traditional financial system: blockchain settlement replaces the RTGS system, stablecoin issuance corresponds to commercial bank deposits, on-chain liquidity and foreign exchange mechanisms replace correspondent banking networks, compliance logic replaces traditional anti-money laundering infrastructure, and payment applications are built on top of these foundations. In this process, major players in fintech, banking, and the crypto industry are all trying to control as many links as possible. Currently, Tether and Circle account for over 84% of the stablecoin market capitalization. The brief de-anchoring of USDC during the Silicon Valley Bank (SVB) incident demonstrated the true nature of concentrated risk: although Circle itself was solvent and its reserve assets were real, some funds were temporarily unavailable due to the bank's collapse. In the traditional banking system, payment risk is dispersed among different institutions, and credit risk is distributed across the loan assets of thousands of banks. In the stablecoin system, settlement risk between participants is eliminated, but the risk is concentrated at the issuer level. The system does not become risk-free; rather, risk undergoes a "vertical migration," shifting from dispersed counterparty risk to dependence on a few issuers. In just a few years, stablecoins have evolved from tools on exchanges to remittance infrastructure in emerging markets. The next phase of conflict will occur between them and the core funding sources of the banking system. The GENIUS Act has laid the basic framework, and the Office of the Comptroller of the Currency (OCC) is advancing specific implementation rules, expected to be completed in July 2026. The biggest variable going forward is whether the CLARITY Act passes. If passed, it will determine whether platforms can offer stablecoin yields to users in any form.

Content source