These past few days, after immersing myself in development, I've gained a new understanding of the market... that is, trading based on candlestick charts inherently has disadvantages... Candlestick charts are information output after market interaction, processing, and rendering; essentially, they are equivalent to an indicator. The true raw data exists at a much deeper level, which is why high-frequency quantitative trading only uses ticker data. Although I've completely abandoned high-frequency trading, this understanding can be applied to the overall market: A single 4-hour candlestick chart contains an astonishing amount of information, but the chart forcibly reduces this multi-dimensional state to two dimensions... This is similar to the difference between Newtonian classical mechanics and microscopic quantum mechanics. Low-frequency traders can still predict and bet on macroscopic price movements through minute market patterns, but the same strategy is completely useless at the microscopic level... Therefore, given the extremely limited personal computing power, our trading is essentially a "classical mechanics" deduction leaning towards the macroscopic world. However, because this is so easy to calculate, stable profit alpha based on candlestick chart systems is almost nonexistent in the market... Ten years ago, when computing power was insufficient, many simple quantitative strategies could make a lot of money, but now, they're a dead end... So where does our way out lie? Observing successful traders, one very difficult factor to quantify is "luck," and almost no strategy can clearly describe what this so-called luck is. Perhaps this could be an interesting direction? Once this genetic algorithm is finished, my next idea is to use pi as the random source for trading decisions, add a coefficient, and perform historical analysis to find the coefficient that performs well, thus identifying a seed of market luck... I wonder if this is verifiable? I'll have the agent quickly run a prototype first, and I'll update tomorrow~

This article is machine translated

Show original

Crypto_Painter

@CryptoPainter

04-02

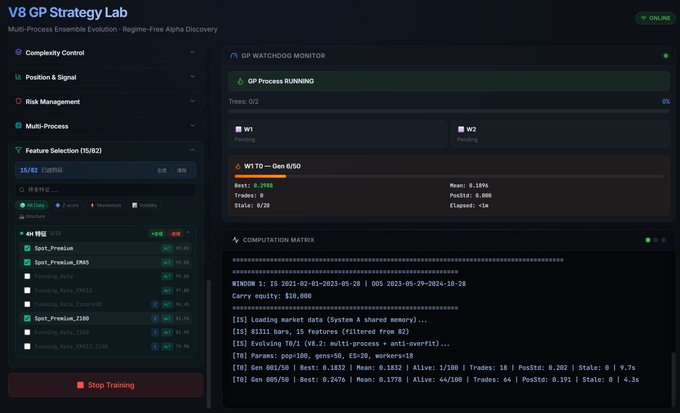

又更新了一版,这次把遗传算法可用的特征变量也暴露到前端了,现在可以针对自己想要迭代的策略类型进行自定义了。

比如我想生成一个震荡短线策略,那就只选波动率与线性回归相关的指标或参数作为特征库,如果想要生成趋势策略,那就选均线或动能类特征。

不知不觉之间,搞出来了一个炼丹炉...好玩~ x.com/CryptoPainter/…

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content