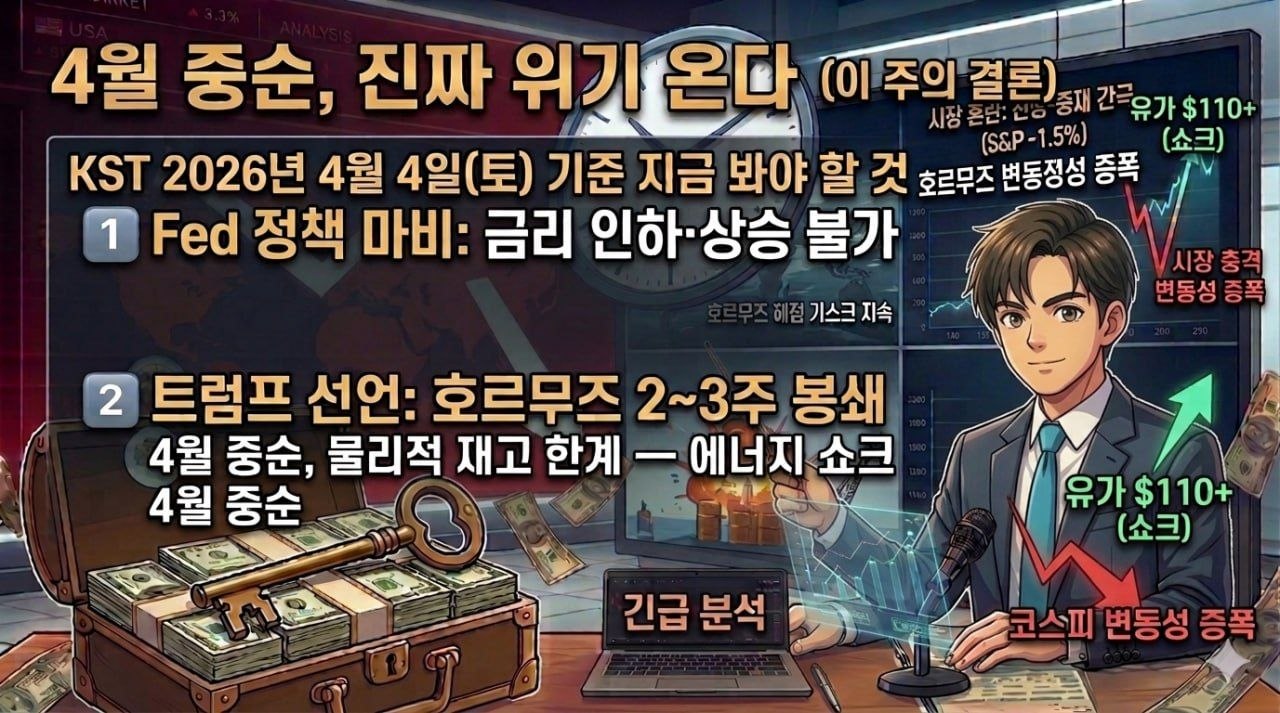

📕Hobby Life Room Research Written by "SB" 📌 Key Issues for the First Week of April - The Gap Between Optimism and Risk If the Strait of Hormuz does not open, the "real" will appear in mid-April. 1️⃣ NFP +178,000 (Non-Farm Employment Index) At 21:30 on April 3rd (KST), the March NFP was released. 178,000 jobs, three times the consensus estimate of 60,000. While this figure appears positive on the surface, as mentioned several times in the research, the majority are "strike returnees." Looking deeper, the healthcare sector contributed +76,000 jobs, of which 35,000 are Kaiser Permanente strike returnees. In other words, this is not new hiring, but the return of people who were absent in February. At the same time, the February figure was drastically revised downward from -92,000 to -133,000. The combined figure for January and February is -7,000. The three-month moving average is +68,000, falling to less than half of the monthly averages for 2023 and 2024. While the unemployment rate appears to have improved slightly to 4.3%, the data confirms the previously mentioned observation that "discouraged workers are not included in the unemployment figures." This is a result of an increase in discouraged workers as the actual labor participation rate dropped to 61.9%. Wage growth actually slowed to +3.5% annually. Due to this data, the Fed has lost its reason to act, and the probability of a policy freeze within 2026 has solidified at 77.5% according to the CME. It has become difficult to justify either a rate cut or a rate hike in the current situation. With energy-driven inflation emerging, this has become the worst-case scenario for the Fed, which has a weak employment base. Although Powell stated on March 30 that "supply shocks are temporary," the ISM price index of 78.3 demonstrated just how precarious the foundation of that judgment is. Today's 3.5% slowdown in NFP wages offers some relief regarding inflation concerns in the short term. However, with oil prices having surpassed $110, this wage slowdown also implies that real purchasing power cannot afford energy costs. 2️⃣ Trump Makes a Direct Declaration The most decisive event of this week was Trump's address to the nation. While the market wanted a path toward ending the war, what Trump brought up was: "We are going to strike Iran extremely hard for the next two to three weeks. We will send them back to the Stone Age. The war will continue until our military objectives are achieved." This statement implies that the Strait of Hormuz will remain blocked for at least another two to three weeks. According to calculations by TD Securities, if the war continues until the end of April, cumulative supply losses will reach approximately 1 billion barrels, comprising 600 million barrels of crude oil and 350 million barrels of refined oil. European diesel futures have surpassed $200 per barrel. This is greater than the energy shock caused by the 2022 Russia-Ukraine war. What the market has not yet fully priced in is the time physical inventory can hold. When combining current tanker inventories and onshore reserves, if the Strait of Hormuz is not opened until mid-April, the supply shortage originating in Asia will spread in a chain reaction to Europe. Trump's remarks were in the exact opposite direction of the March 31 reports regarding Pezheshkian's willingness to end the war. The market had driven the S&P up 2.91% for two consecutive days by pricing in two-way signals that "Trump wants an end to the war, and Iran is willing to end it," but then experienced an 11% surge in WTI following a single speech by Trump. The core risk in the current market is the lifespan of optimism. If Trump’s timeline of two to three weeks becomes reality, mid-April will be the true turning point. 3️⃣ Structures Currently in Action Behind the market moving headlines up and down, there are three structural changes actually underway. First, the ISM price index at 78.3. This figure represents the most underestimated data in the week. As energy costs skyrocket, manufacturing input costs are rising explosively. At the same time, the ISM employment index stands at 48.7, placing it in the contraction zone. It is a structure where costs are rising while employment is shrinking. If this solidifies, second-quarter corporate earnings will begin to be pressured. Second, the realization of risks regarding hyperscaler infrastructure in the Middle East. The IRGC has declared 18 companies, including Apple, Google, Microsoft, and Nvidia, as legitimate targets for attack within the Middle East. The strike on AWS Middle East data centers in early March already serves as a precedent. A significant portion of the $600 billion in hyperscaler CapEx forecasts for 2026 is concentrated in the regions currently targeted by the IRGC. This marks the point where the geopolitical risks associated with the AI infrastructure investment thesis are turning into tangible costs. Third, the Fed's policy paralysis. There is a 77.5% probability that interest rates will remain frozen by 2026. Neither raising nor lowering rates is feasible. Rate cuts are difficult due to energy inflation, while rate hikes are difficult due to a weak employment base. With the Fed unable to do anything, the market cannot expect a policy safety net. This is not merely a matter of interest rate direction; it means that an environment of heightened market volatility will persist. 💡Summary The NFP came out well. However, it is not the NFP that is currently driving the market. If the Strait of Hormuz is not opened by mid-April, physical inventory will reach its limit. Trump stated, "I will strike for another two to three weeks." Iran is enacting tolls into law and institutionalizing its sovereignty over the Strait of Hormuz. The market opening on April 6 is the day when all the accumulated uncertainties are processed simultaneously for the first time. #International

This article is machine translated

Show original

Telegram

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content