KelpDAO suffered a $292 million cross-chain bridge attack, and the risk spread to Aave, causing the total value of DeFi locked in assets to evaporate by $13 billion within 48 hours.

If you deposit USDC into the money market and only earn 5% returns, the real key issue is not whether DeFi carries risks, but whether your returns match the risks you take.

This article will break down this problem using bond pricing logic.

Two weeks ago, attackers stole $292 million from KelpDAO. The stolen rsETH was subsequently deposited back into Aave V3 as collateral, directly causing Aave to incur approximately $196 million in bad debt. Within just three days, the total value of Aave's locked assets plummeted from $26.4 billion to $17.9 billion.

Two weeks prior, Drift Protocol, part of the Solana ecosystem, suffered a $285 million loss due to a social engineering attack on its administrator private key by North Korean hackers. The attack was planned as early as the fall of 2025.

The two major security incidents, occurring only three weeks apart, resulted in a combined loss of $577 million. Affected by the run on Aave's USDC lending market, the utilization rate reached 99.87% for four consecutive days, and deposit rates soared to 12.4%. Circle's chief economist, Gordon Liao, even initiated a governance proposal to quadruple the lending cap to alleviate withdrawal demand.

A month ago, many users deposited stablecoins in the DeFi currency market, earning only 4%–6% annualized returns.

Everyone now needs to confront a core question: Is this type of yield pricing itself reasonable? Weeks before the KelpDAO incident, Santiago R Santos raised this question on the Blockworks podcast: In DeFi, we have long assumed high risk but have never received adequate risk compensation. In the future, the reasonable risk-reward spreads for various assets should be redefined.

The yield of all corporate bonds is composed of multiple layers of risk compensation. The core pricing formula is as follows:

• Yield = Rf + [PD x LGD] + Risk Premium + Liquidity Premium

Rf is the risk-free rate, based on the yield of U.S. Treasury bonds with matching duration.

PD × LGD represents expected loss = probability of default × loss due to default, where loss due to default = 1 – asset recovery rate. The risk premium compensates for uncertainties beyond expected loss; even if two assets have identical PD and LGD, their pricing will differ if the risk outcome fluctuates within different ranges. The liquidity premium refers to the additional costs incurred from selling assets at a discount or exiting a position.

Based on Moody's long-term historical data since 1920, the following benchmarks are used as references:

• The long-term annualized default rate for U.S. speculative-grade bonds is 4.5%, with a recent 12-month average of 3.2%, and is projected to rise to 4.1% in the first quarter of 2026.

• The historical average recovery rate of high-order unsecured high-yield bonds is approximately 40%, corresponding to a default loss rate of approximately 60%.

• Long-term annualized expected loss of high-yield bonds: 4.5% × 60% = 2.7%;

In the private lending sector, KBRA forecasts a 3.0% default rate for direct lending in 2026, with an average recovery rate of approximately 48% for defaulted cases in 2023–2024.

• Historical recovery rates for high-level secured leveraged loans range from 65% to 75%.

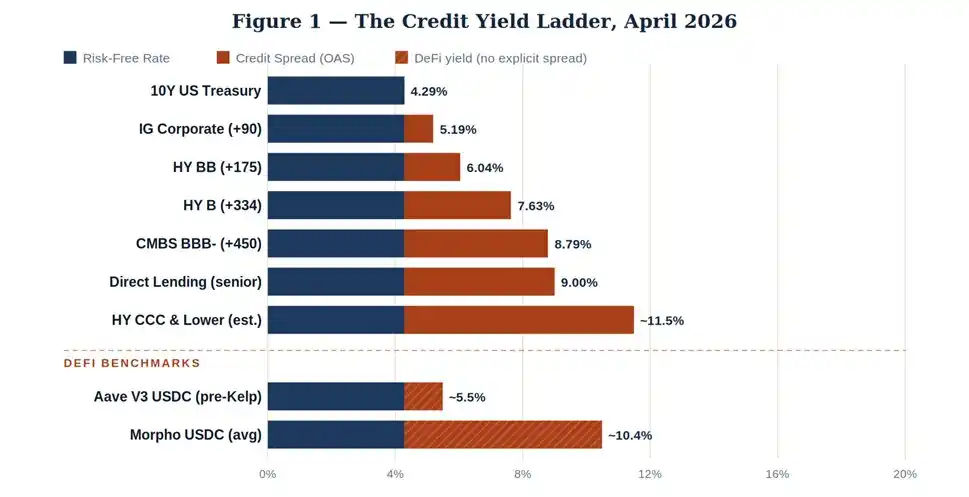

Let's look at the current data. The 10-year U.S. Treasury yield closed at 4.29% last Wednesday. We also extracted the ICE Bank of America All-Trust product option adjusted spread for April 2026.

The pricing logic is clear and in line with common sense: along the capital tier from government bonds, investment-grade bonds, speculative-grade bonds, to subprime commercial real estate assets, the yields rise in tandem to compensate for the ever-increasing probability of default and the magnitude of losses.

The yield on private equity direct lending remains around 9%, not because borrowers have a higher default rate, but because non-standard private equity assets have extremely poor liquidity and a significant liquidity premium.

In contrast, looking at the DeFi market: before the KelpDAO incident, Aave's USDC deposit rate was approximately 5.5%, a pricing level between investment-grade bonds and single-B high-yield bonds. Meanwhile, Morpho, relying on a curated vault and active management screening, offered a yield of approximately 10.4%. These two figures cannot simultaneously accurately reflect the same potential risks.

Traditional credit default processes are tedious and cumbersome. Borrowers fail to pay interest, bondholders trigger debt acceleration clauses, companies restructure, assets are liquidated and disposed of, and asset recovery is negotiated—a lengthy and negotiable process.

However, DeFi lacks a debt restructuring mechanism, and the main threat comes from protocol attacks, which are divided into three completely different failure modes, each with unique loss characteristics.

Code vulnerabilities, such as reentrancy attacks, invalid argument checks, and lack of permission control, can lead to cryptocurrency theft. Attackers can directly drain the cryptocurrency pool. Historical data shows that protocol attacks involving white-hat hackers have an average recovery rate of only 5%–15%; if a North Korean national-level hacking group is involved, the recovery rate is practically zero.

The full return of the $611 million stolen from Poly Network in 2021 was an extreme case; the $625 million stolen from Ronin and $325 million stolen from Wormhole were ultimately recovered entirely by the project team and market makers covering the losses themselves, rather than by market-based asset recovery, and were essentially shareholder compensation.

Malicious manipulation of price feeds through low-liquidity decentralized trading pools can artificially create bad debts; or attackers can hoard governance tokens and pass malicious proposals to drain public funds. The $182 million loss suffered by Beanstalk due to a governance attack in 2022 is a typical example. While some losses can be mitigated through protocol intervention, the assets and claims held by lenders often become worthless token holdings.

The KelpDAO incident falls into this category, representing the most dangerous and difficult-to-audit risk model. Protocol A issues liquid staking/re-staking derivatives, Protocol B accepts the asset as collateral, and Protocol C is responsible for cross-chain asset bridging and transfer.

An attack on any link in the chain will cause a cascading collapse of all downstream holdings. Attackers do not need to compromise Aave itself; simply breaching the underlying rsETH protocol upstream will directly force Aave lenders to assume massive bad debts.

These three types of risks share common characteristics, which are also the core differences between DeFi and traditional credit markets: risk outbreaks occur in minutes, not quarters. There is no contractual negotiation, no bankruptcy financing to cover losses; smart contracts execute automatically, and code is the rule. Once a vulnerability appears in the code, losses are almost entirely irrecoverable. Aave V3's rsETH bad debt surged from zero to $196 million in just about four hours. In contrast, the median cycle from risk warning to debt restructuring for BB-rated traditional high-yield bonds is as long as 14 months.

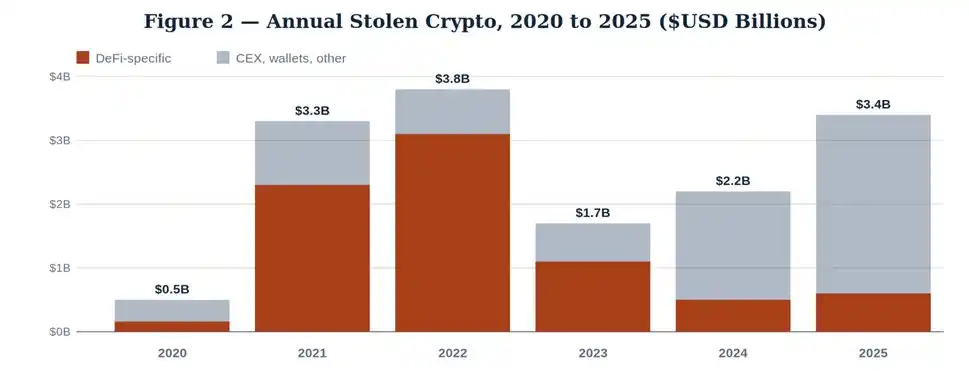

Chainalysis's mid-year report in December 2025 revealed a set of contradictory data: from the beginning of 2024 to October 2025, the total value locked in DeFi rebounded from $40 billion to a peak of $175 billion, but losses from DeFi-specific hacking attacks remained at the low level of 2023.

In 2025, the total amount of crypto assets stolen was $3.4 billion, with the risk highly concentrated in thefts of centralized trading platforms and personal wallets.

Looking at this data alone, it's easy to mistakenly conclude that DeFi security is continuously improving. However, objective facts do exist: the contract auditing industry is maturing, bug bounty platforms like Immunefi protect over $100 billion in user assets, and cross-chain bridges are gradually introducing time locks and multi-party verification mechanisms.

But the reality in 2026 was completely the opposite: Drift lost $285 million on April 1st, and KelpDAO lost $292 million on April 18th. Two massive financial crises within 18 days, both targeting composability vulnerabilities rather than the lending protocols themselves.

Based on the average annual locked assets, the annualized loss rate of DeFi in recent years was calculated as follows:

• 2024: DeFi-specific losses amounted to approximately $500 million, with an average locked value of $75 billion → annualized loss rate of 0.67%.

• 2025: Losses of approximately $600 million, average locked-in value of $120 billion → Annualized loss rate of 0.50%

• 2026 (Annualized Calculation): Losses from just two events in the second quarter reached $577 million, with an average locked-in value of $95 billion. → If the risk pattern continues, the annualized loss rate will reach 2.0%–2.5%.

Based on this calculation, the annualized default probability of leading DeFi lending businesses is approximately 1.5%–2.0%. Combined with a 90% default loss rate under extreme attacks (without external bailouts, the typical recovery rate from stolen tokens is only 5%–15%), the annualized expected loss is 1.35%–1.80%. This figure exceeds that of traditional high-yield bonds and does not yet account for uncertainty premiums, liquidity discounts, regulatory risks, or cross-chain contagion risks.

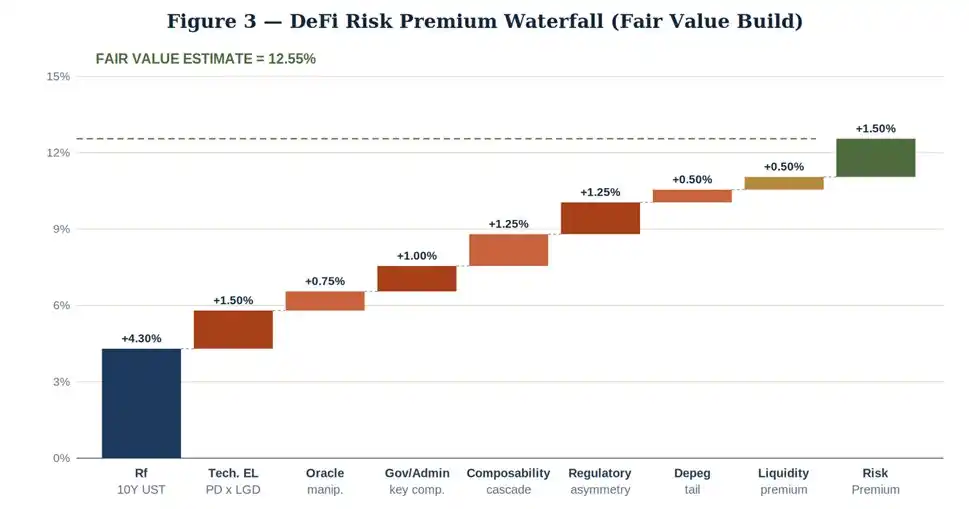

Based on bond pricing logic, we calculated the fair yield of leading DeFi stablecoin deposits: benchmarked against leading Ethereum mainnet protocols (Aave, Compound), fully overcollateralized, and USDC lending products targeting retail and quantitative borrowers.

Constructing fair value yield upwards from the 10-year Treasury bond yield benchmark.

Using the 10-year US Treasury bond as a benchmark, premiums are added layer by layer:

• Risk-free benchmark (10-year US Treasury yield): +4.30%

• Expected fixed loss: +1.50%

Oracle manipulation risk premium: +0.75%

• Governance/Administrator Private Key Risk Premium: +1.00%

• Cross-agreement portfolio cascading risk (Kelp similar risk): +1.25%

• Regulatory asymmetry risk premium: +1.25%

• Stablecoin tail risk: +0.50%

• Asset liquidity premium: +0.50%

• Risk premium: +1.50%

The final fair and reasonable annualized rate of return is 12.55%.

Therefore, ideally, the reasonable interest rate for leading compliant DeFi stablecoin deposits should not be lower than 13%. For assets with insurance coverage and protocol reserves as a safety net, the interest rate can be appropriately lowered; long-tail protocols, newly launched markets, and assets involving re-staking and cross-chain underlying assets require a higher risk premium.

First, strive for fair compensation. If you provide USDC to DeFi at a 5% yield, you are effectively accepting BB-rated credit risk pricing, which is actually higher than CCC-rated in terms of technology and composability risk. Morpho-style select-vault markets, with interest rates between 9% and 12%, are closer to fair returns, but they also raise issues regarding manager selection and transparency.

Secondly, it's crucial to improve the capital structure. Over-lending secured by high-quality collateral (ETH, wBTC, and the tried-and-tested LST), supplemented by oracle redundancy and protocol-level insurance layers, and free from cross-chain risks, carries a risk premium far lower than the aforementioned framework. These fall under the category of "investment-grade assets" in the DeFi space.

Third, it is crucial to properly assess tail risks. The KelpDAO vulnerability was not a black swan event, but rather a predictable failure mode of restaking primitives connected to increasingly fragile multi-chain architectures. The situation with Drift is similar, only the participants are different.

The company recorded a permanent loss of $577 million in the second quarter of 2026. A DeFi portfolio with a yield of 5.5% is completely unable to cover the risks of extreme crashes and a chain reaction of defaults.

DeFi is not uninvestable; it's just currently mispriced. Institutional-grade allocation opportunities do exist, but investors must either demand a reasonable risk premium or conduct thorough due diligence on individual protocols using the rigorous standards of private lending.

Simply depositing money into top-tier cryptocurrency markets and passively accepting low-yield listings is a high-risk, interest rate arbitrage strategy disguised as risk-free investment.

Related reports

Related reports

S&P Global 2022 Global Credit Outlook Report: DeFi Will Not Replace the Traditional Financial System