Written by: Long Yue

Source: Wall Street News

The more the market rises, the harder it is to find a reason to fall—but the risks haven't disappeared, they've just become more deeply hidden.

On May 14, Bloomberg market analyst Jon-Patrick Barnert wrote that while the current US stock market rally has clearly accelerated, the cost and timing of short remain difficult to grasp. Even more problematic is that the very rationale for short has become unclear.

The core contradiction in this market rally is that while positions are extremely crowded, fundamental narratives—especially AI—continue to support market sentiment. Which will collapse first?

Position: The market is nearing "fully long" status.

From a purely price trend perspective, the pullback signal is already quite obvious.

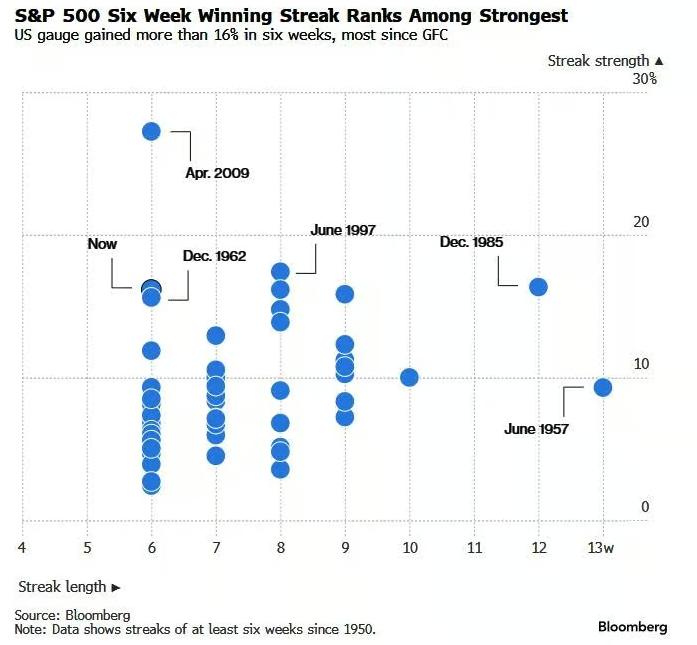

The S&P 500's six-week winning streak is not only one of the longest in over 70 years, but also among the strongest in history. Barnert stated that "taking a breather" is perfectly normal for this market.

Goldman Sachs' Risk Appetite Indicator has risen back to 1, the first time since the beginning of the year. A reading above 1 is extremely rare and historically often foreshadows a potential pullback. The last time this threshold was breached was in 2021, after which the market entered a bear market.

Looking at the most popular thematic stocks, Barnert describes this as a market where "everything is overbought," with some of the hottest sectors reaching extreme levels of overbuying. Coupled with mechanical capital inflows—currently appearing to be at or near maximum long positions—the overall picture is one of limited upside potential and significant potential pressure to reposition.

However, short is not easy. Barnert points out that position adjustments can be completed within a single day, making it extremely difficult to time short positions. Furthermore, if the market chooses to "fall slowly," volatility positions will quietly become ineffective in a mild environment. A more likely scenario is that overall sentiment remains bullish, and once short sellers are forced to cover, it could trigger a new round of short squeeze, rising faster than anyone expected.

The fund flows of some popular ETFs have begun to show subtle changes—a tendency to "lock in profits" rather than "chase highs." However, Barnert also admits that this trend has been going on for several weeks and has not yet had a substantial impact on market movements.

Narrative: Without AI, the market is nothing.

If position size is a potential technical concern, then the narrative itself appears to be more stable at present.

Barnert points out that there is currently a lack of clear signals to trigger a fundamental bear market. Corporate profits remain strong, and inflation expectations have risen slightly but not to extreme levels. The market has already priced in the impact of high oil prices and the situation in the Middle East, and the latest US employment data has eased recession fears. As for interest rate hike expectations, they are no longer a catalyst suppressing the stock market.

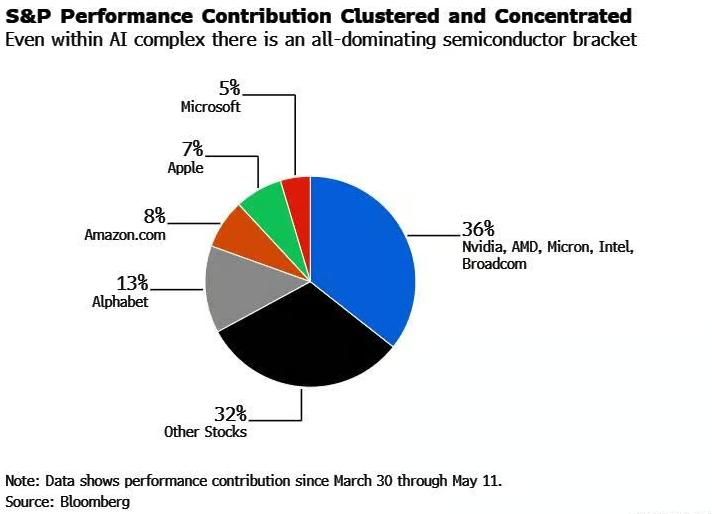

However, one issue cannot be ignored: the concentration of this round of market activity has become highly concentrated on "concentration itself".

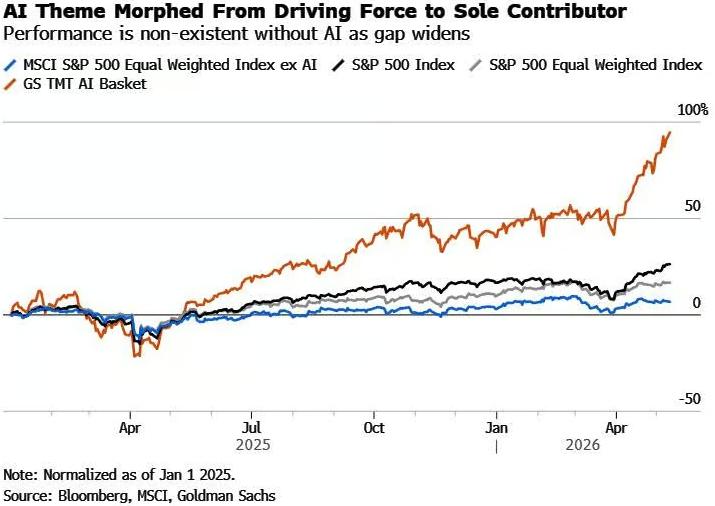

Barnert points out that whether comparing the performance of indices with and without AI, or analyzing the contributors to the gains since March, the conclusions all point to the same thing: without AI, the market's performance can only be described as "mediocre." More notably, the semiconductor sector alone contributed nearly 40% of the gains since March.

The market narrative surrounding AI has once again entered a "greedy mode" rather than a stage of rationally pursuing reasonable returns. Concerns that were hotly debated just a few months ago—whether AI computing costs can be covered by savings from layoffs, data center energy supply bottlenecks, AI pricing wars eroding profit margins, new competitors disrupting the existing landscape with lower costs, a significant increase in capital expenditures while stock buybacks stagnate, and AI security risks—now seem to have been collectively forgotten by the market.

The risk of a repeat of the "DeepSeek moment"

Nomura Securities strategist Charlie McElligott issued the most direct warning on this matter.

He stated, "Given the current market structure and the high degree of overlap in themes, if another 'DeepSeek-like' shock catalyst were to emerge one day, it could very likely trigger a Nasdaq Level 1 limit-down trading event."

McElligott further points out that in this scenario, the semiconductor ETF could easily fall by 15% in a single day—because "the hypothetical reversal of reflexive mechanical fund flows will result in a large-scale overshooting decline."

In other words, it is precisely those mechanical funds that continuously buy in during the upward trend (such as CTA strategies, risk parity funds, etc.) that, once a reversal is triggered, will become amplifiers that accelerate the decline.

This round of AI bull market faces two major risks: one is technical (overly crowded positions), and the other is narrative-based (whether the AI story can be sustained). The former could be triggered at any time, while the latter, if it breaks down, will have a deeper impact. The combination of the two constitutes the most alarming structural vulnerability in the current market.