Tech giants and AI startups are forming a "revenue loop": investment funds flow back through cloud service contracts, generating new cloud revenue and profit growth. More than half of the $2 trillion in cloud orders from Microsoft, Google, Amazon, and others rely on OpenAI and Anthropic, resulting in a significant increase in book profits, but a marked deterioration in free cash flow. This investment-consumption loop amplifies the AI boom narrative but also raises questions about the authenticity of profits and the risk of a systemic bubble.

Article author and source: Wall Street News

A carefully orchestrated funding cycle between tech giants and AI startups is quietly underpinning the boom narrative of the entire AI industry.

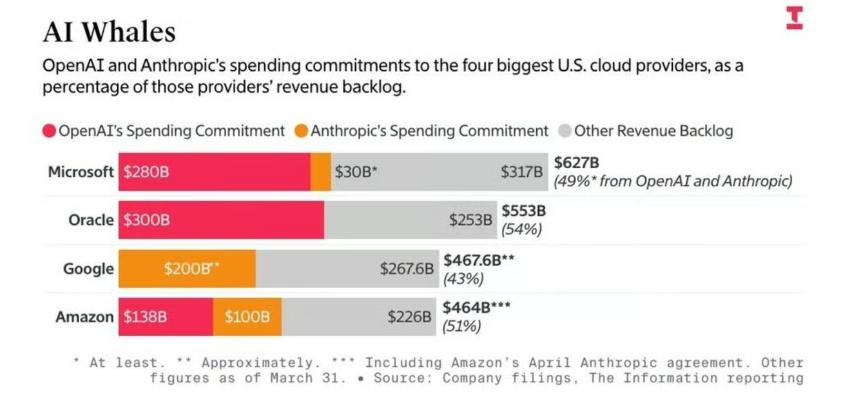

Of the $2 trillion in cloud business backlog that Microsoft, Google, Amazon, and Oracle have combined for, more than half come from two AI startups, OpenAI and Anthropic.

However, according to the company's latest financial report, behind this massive pipeline is an accounting operation known as the "recurring revenue loop"—tech giants inject funds into startups under the guise of "investment," but the contracts include clauses requiring the latter to return the same amount of funds to rent the former's cloud servers, thereby creating "new cloud revenue."

The ripple effects of this mechanism have permeated the profit statements of tech giants. In the first quarter of 2026, Alphabet recorded a record profit of $62.6 billion, of which $28.7 billion—nearly half—came from the book value increase of its investment in Anthropic; of Amazon's $30.3 billion profit in the same period, $16.8 billion also came from paper gains from Anthropic.

Meanwhile, Amazon's actual free cash flow plummeted by 95% to just $1.2 billion, as it had to use $44.2 billion of real funds to build data centers. This coexistence of apparent prosperity and depleted cash flow has led market observers to raise serious questions about the authenticity of the AI industry's fundamentals.

The operating mechanism of circular accounting

The core logic of this money cycle is not complicated, but it is extremely deceptive.

Take Microsoft and OpenAI as an example: Microsoft invested $13 billion in OpenAI, but this investment was not delivered directly in cash. Instead, it was distributed in the form of "cloud credits," which were specifically used for using Microsoft servers. OpenAI then used these credits to train AI models, and Microsoft recorded this server usage in its books as new cloud revenue from the "customer."

In essence, the tech giants are paying themselves with their own money and classifying it as a sale to an external party.

This mechanism has reached a considerable scale. OpenAI's annual cloud service bill has ballooned to over $60 billion, more than double its actual revenue of $25 billion, and this gap is almost entirely filled by the aforementioned revolving funds. Anthropic's situation is similar—it burned through $2.66 billion on Amazon Web Services (AWS) in just nine months, a figure that is roughly equivalent to its entire revenue during the same period.

Cash flow crisis hidden by book profits

Circular accounting not only creates inflated cloud revenue, but also creates a second layer of accounting effect—tech giants record large book gains on their profit and loss statements by adjusting investment valuations.

Whenever an AI startup completes a new round of financing and obtains a higher valuation, the tech giants holding its equity can correspondingly increase the book value of their investment and directly include this unrealized gain in their current profit.

This mechanism leads to a significant discrepancy between profit figures and actual operating cash flow. Amazon's case is particularly typical: in the same quarter it reported record profits, its free cash flow plummeted by 95% year-over-year because the company had to continue expanding its physical data center infrastructure with real capital expenditures. The impressive figures on paper contrast sharply with the pressure of cash burn.

Concentration risk: A fragile structure where one's losses affect the entire group.

This cyclical system has also accumulated highly concentrated counterparty risk across the business pipelines of tech giants.

According to financial reports, 49% of Microsoft's $627 billion future order backlog is directly linked to OpenAI; and a staggering 54% of Oracle's $553 billion pipeline relies on OpenAI as a single customer. This means that if OpenAI's funding cycle is disrupted, the core business metrics of both tech giants will face a severe impact.

This structural vulnerability has reminded some analysts of the dot-com bubble burst in 2001. At that time, Global Crossing and Qwest Communications exchanged equivalent fiber optic network capacity to inflate sales figures; Qwest was ultimately forced to write off $1.4 billion in fictitious revenue, while Global Crossing declared bankruptcy.

There is a key difference between the two: the exchange of internet capacity was deemed illegal back then, while the current circular accounting in the AI industry is fully compliant under the existing accounting standards framework.

Self-reinforcing market capitalization bubble

The impact of this mechanism has extended beyond corporate financial statements to the broader capital markets.

The circular accounting inflates the book profits of tech companies, which in turn drives up their stock prices. Rising stock prices then prompt passive retirement accounts and index funds to passively increase their holdings of related tech stocks, creating a self-reinforcing positive feedback loop. In this process, investment, sales, and stock prices all climb on paper, while AI technology itself has yet to generate real cash profits.

Historically, the duration of bubbles has varied—the South Sea Bubble burst within seven months, while the dot-com bubble lasted five years. How long can the underlying logic of the current AI boom sustain itself? This is becoming an increasingly pressing question for market participants.