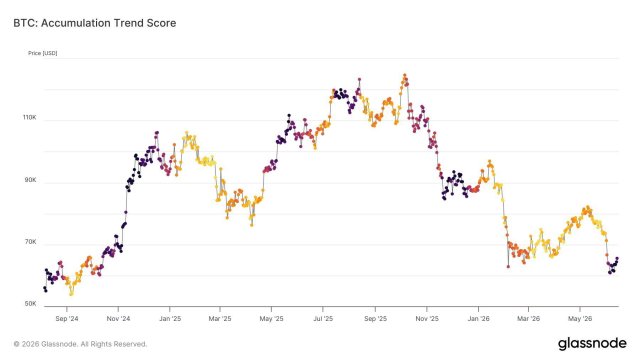

1⃣ Bitcoin rebounded from a low of $60,900 to $63,300 over the weekend, initially recovering the losses triggered by Friday's non-farm payroll data.

2⃣ The Hyperliquid ETF saw a net inflow of $160 million in the first few days after its listing, while BTC and ETH ETFs continued to experience outflows during the same period.

3⃣ Iran launched its first direct missile strike against Israel since the April ceasefire and warned of expanding the strike range, making geopolitical risks a new variable in the pricing of risky assets.

4⃣ CPI data will be released this Wednesday. The consensus expectation for Q2 inflation is around 6%, and the market is generally betting that the Federal Reserve will not cut interest rates.

5⃣ As the Iraq War enters its 100th day, Brent crude oil is fluctuating at high levels above $90, with analysts warning of continued stagflation risks.

6⃣ Goldman Sachs, citing a stronger-than-expected US labor market, has stopped predicting a Federal Reserve rate cut in 2026 and has postponed the timing of the last two rate cuts to June and December 2027.

7⃣ New Federal Reserve Chairman Warsh's hawkish stance and Trump's public pressure for interest rate cuts have exacerbated market divergence in monetary policy.

8⃣ SpaceX's IPO window officially opens this week; amid high inflation, expectations are rising for pressure on overvalued technology stocks.

9⃣ OpenAI is preparing to launch ChatGPT in the coming weeks, marking its biggest overhaul since its 2022 release. This overhaul will fully integrate Codex into ChatGPT and allow access to external applications.

10. The RWA sector continues to expand: Euler Finance's daily active users have increased by 200% since VBILL was included as collateral, and Provenance's TVL has reached $25.8 billion.