Written by: Zhao Ying

Source: Wall Street News

Two major catalysts for declining inflation are developing simultaneously, providing ample justification for Federal Reserve Chairman Warsh to shift to a dovish stance at this week's Federal Open Market Committee (FOMC) meeting.

According to a report released by Citi Research on June 15, the planned reopening of the Strait of Hormuz will push oil prices down and eliminate the upside risk of energy prices to inflation. Meanwhile, the core CPI data released last week was significantly weak, with a month-on-month increase of only 0.21%.

The combined effect of these two developments has further weakened the case for the Federal Reserve to maintain a hawkish stance, ultimately bringing the path of interest rate cuts back to the forefront.

For the market, this assessment has direct pricing implications. The two-year US Treasury yield has fallen by about 13 basis points from a week ago, but is still more than 60 basis points higher than in February. The market currently has room to compress its pricing of interest rate hikes and further increase its pricing of interest rate cuts.

Energy price pressures have subsided, and the risk of upward inflation has diminished.

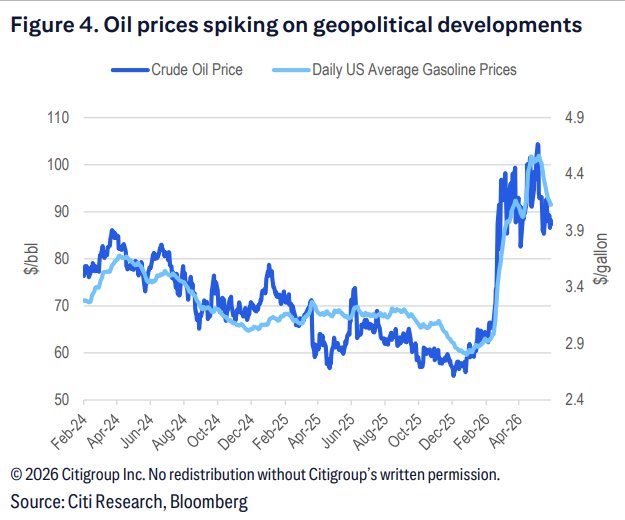

The expectation of the Strait of Hormuz reopening is one of the core drivers of this round of dovish logic. Once the strait resumes passage, increased crude oil supply will drive down oil prices and other energy prices.

Gasoline prices have declined for a month, with the national average falling from about $4.50 per gallon to $4.00. Citigroup expects prices to fall further, following other energy commodities. This trend will result in at least several months of negative headline inflation readings in the coming months and will prompt Federal Reserve officials to reclassify energy prices from "inflation risk" to "neutral or even deflationary factor."

Core CPI cools, inflation indicators diverge more sharply

At the core inflation level, although core PCE is expected to remain strong in May, core CPI has shown clear signs of cooling, with a month-on-month increase of only 0.21%.

Core PCE has increasingly become an "outlier" among various inflation indicators—both the cut-off mean PCE and core CPI are closer to the target level, and the downward trend is clearer. This divergence is being recognized more and more widely by the market and Federal Reserve officials, and it also provides data support for a dovish stance.

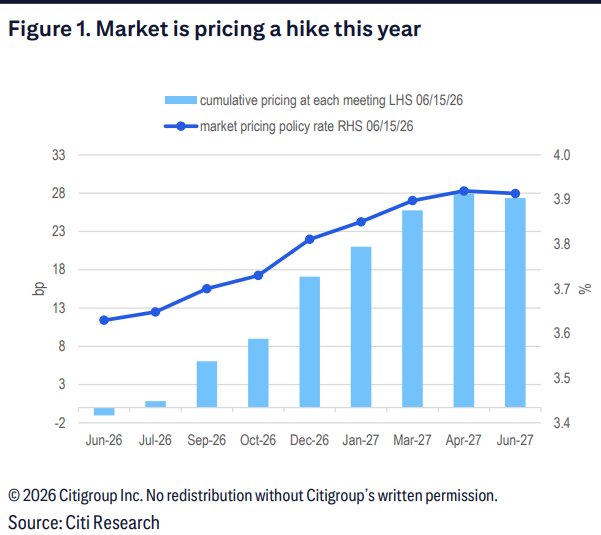

The FOMC's hawkish adjustments have been fully priced in, and there is room for upward movement in dovish statements.

The report anticipates that this week's FOMC statement will remove the phrase "dodging bias," and the median of the dot plot will show that interest rates will remain unchanged this year. However, this hawkish adjustment has already been fully priced in by the market and does not constitute new information.

The real variable lies in Warsh's rhetoric. Given the latest developments regarding the reopening of the Strait of Hormuz and the cooling trend in core inflation, the risk of Warsh releasing a dovish signal at this meeting is tilting upwards. If his rhetoric is more dovish than expected, the market's repricing of the interest rate cut path may accelerate.

US Treasury yields still have room to fall, and market pricing has room for adjustment.

From a market pricing perspective, the report believes that current interest rate futures still imply a high probability of an interest rate hike. Although the two-year US Treasury yield has fallen by about 13 basis points compared to a week ago, it is still more than 60 basis points higher than the level in February, indicating that the market has not yet fully digested the impact of the easing of inflation risks.

As the upside risks to inflation that previously supported hawkish expectations gradually dissipate, the market is expected to further compress interest rate hike pricing and simultaneously raise interest rate cut pricing, leaving room for further declines in US Treasury yields.