Blend is short for "Blur Lending", the new lending platform of Blur.

If there's one thing we've learned over the past few months, it's that innovations like this always have multiple effects on the market as a whole.

Today, this short blog post will focus on how Blend works, what benefits & risks it brings, and what impact Blend might have on the NFT market.

But step for step:

1. How Blend works

Blend is a new mechanism on the Blur website.

Blur is rolling out Blend slowly. For now, only three collections are available for Blur Lending. People speculate that more collections might be added this month.

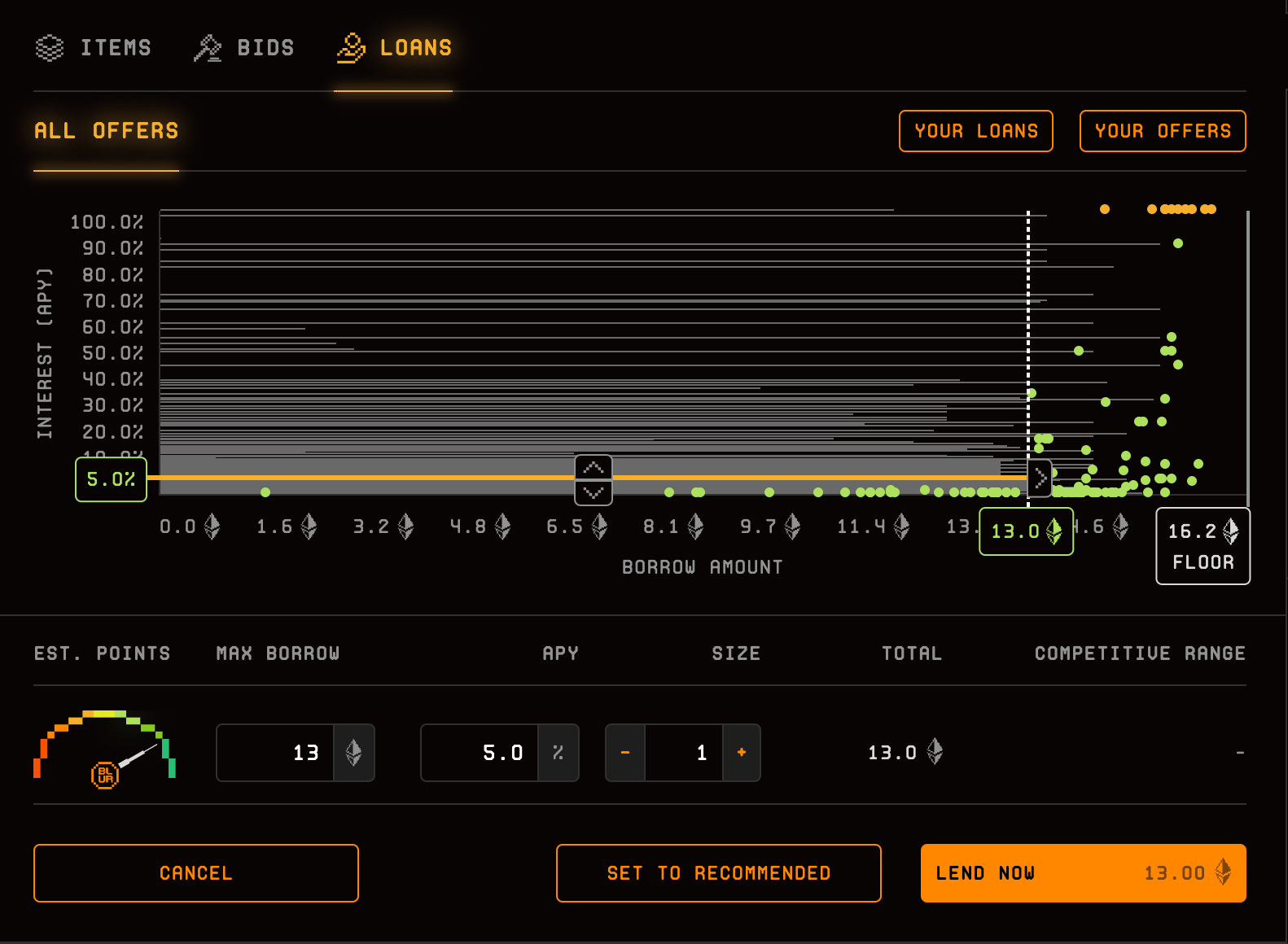

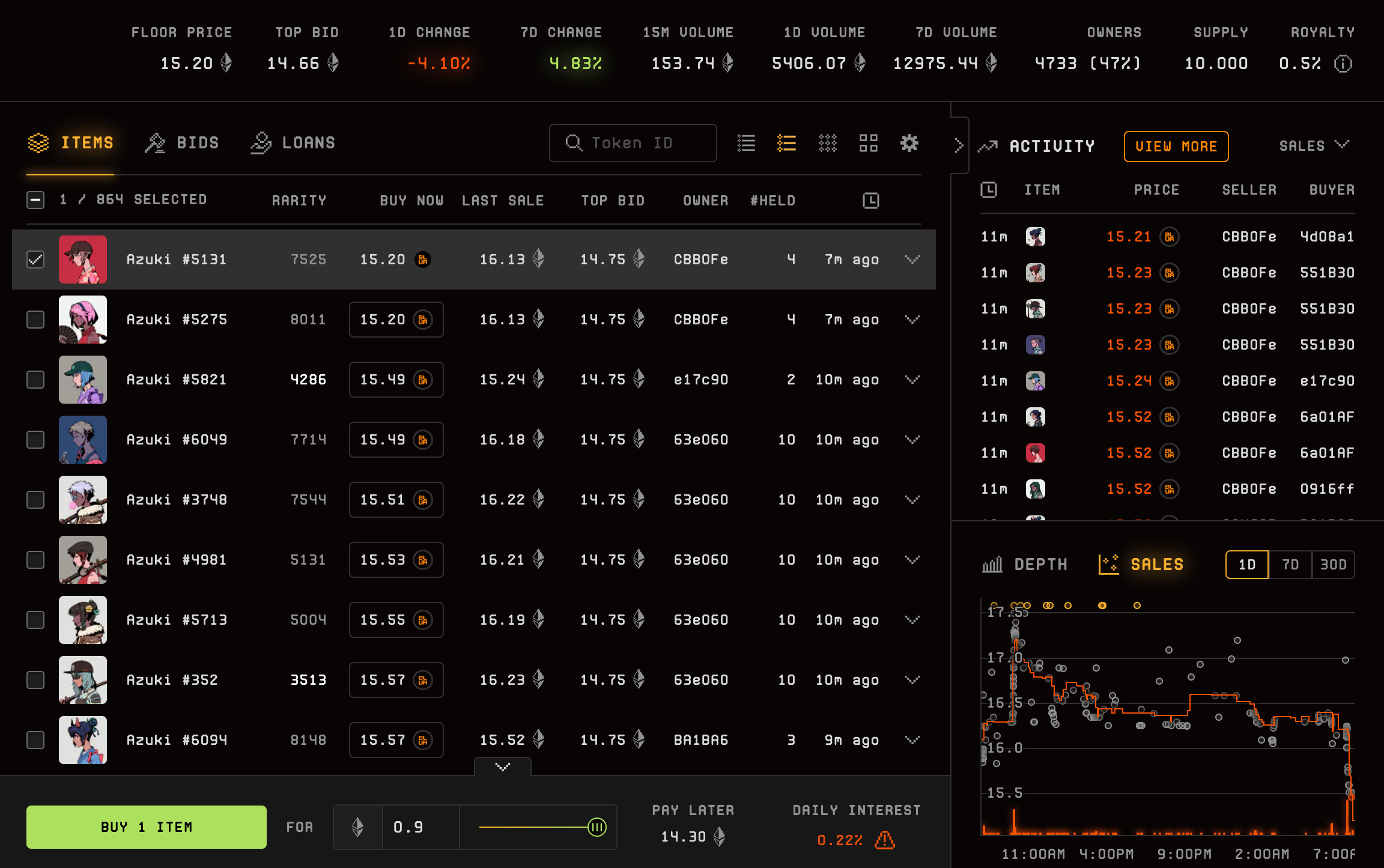

The first three collections are Azuki, Miladies, and Cryptopunks. You can now find the "Loans" tab next to the "Items" and "Bids" tabs.

On the Loans tab, individuals can submit loan offers for the respective collection.

You specify two things when creating a loan offer: The loan volume ("how much ETH do I want to lend?") and the APY rate ("what interest rate do I want to get?"). All loans are infinite, so you don't have to specify a time period.

Generally, the lower the interest rate and the larger the volume, the more bidding points you can earn:

Loan points (“estimated points”) are similar to bidding points, the more you collect the bigger the $Blur airdrop that you will receive.

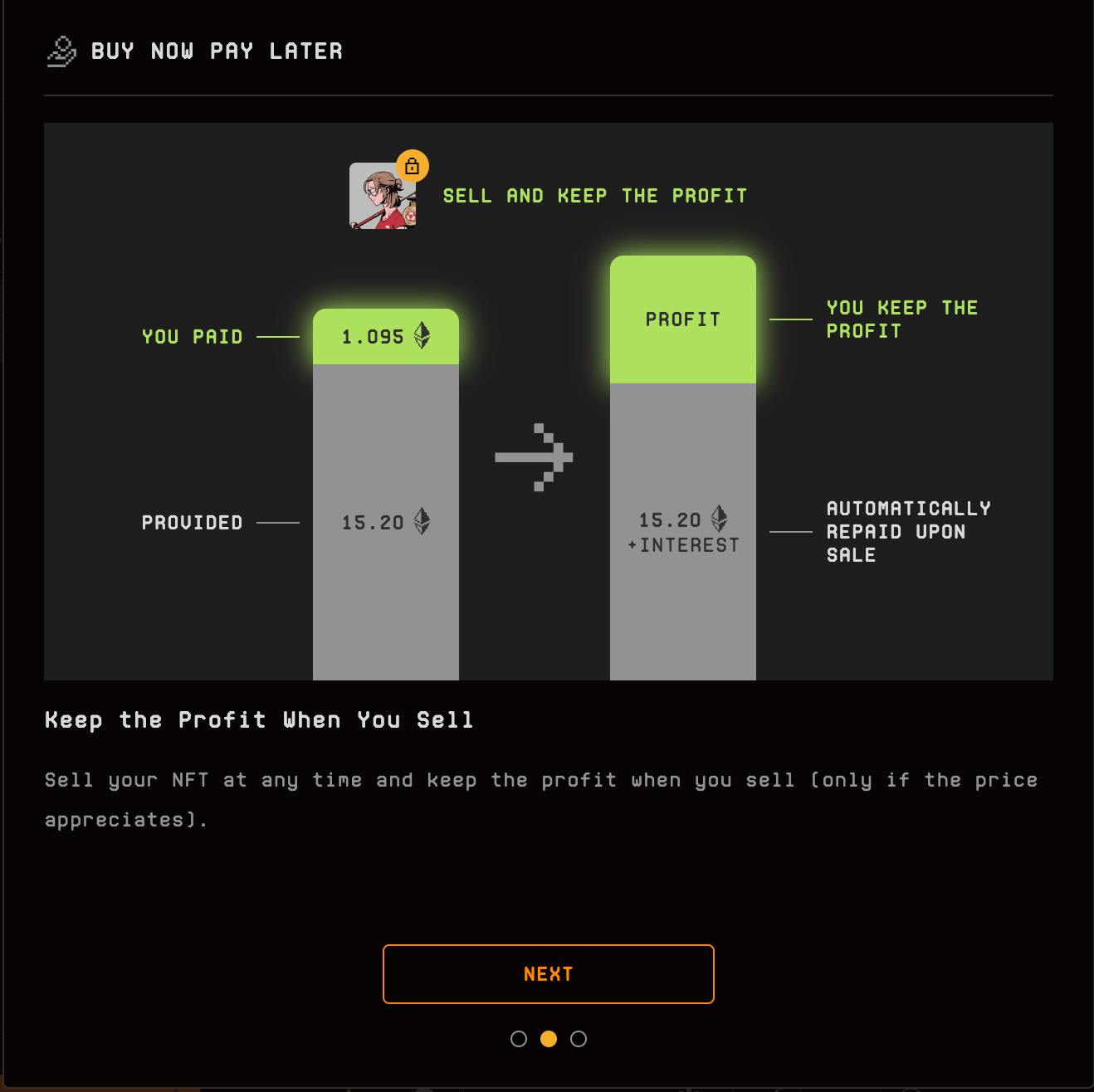

As a lender you can reclaim the loaned amount at any time. The other party then has 30 hours to either repay the amount directly or accept another loan offer, which will then be used to repay the first loan.

If a borrower does nothing - neither repays the loan nor refinances it - the borrower either receives the NFT after the 30 hour period ended or it will be foreclosed.

2. Benefits

Loans allow holders of NFTs to get instant liquidity without having to sell the NFT directly. At low interest rates, it allows people to borrow money against their own NFT without any hassle.

This is good in theory. Although you should generally only buy NFTs with money you can spare, sometimes there are situations where you need money quickly. Blur is not the first platform that allows this, but probably on a completely new scale.

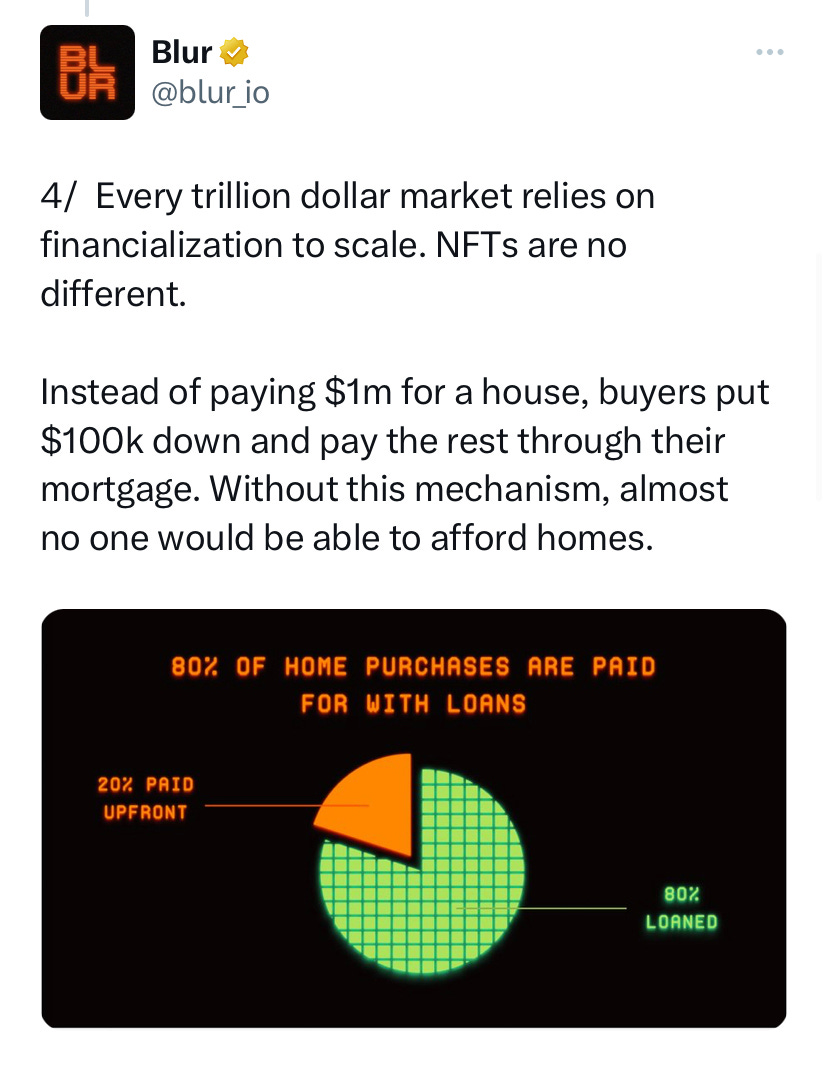

It also gives people the opportunity to finance NFTs. You don't have to pay 16 ETH directly for an Azuki, for example. You can buy it today for 2.5 ETH and take out a 13.5 ETH loan. This allows people with less financial resources to buy their favorite NFT.

Blur also has a massive war chest to incentivice competitive bids leveraging their $Blur points.

Blur compared it to buying a house in their thread:

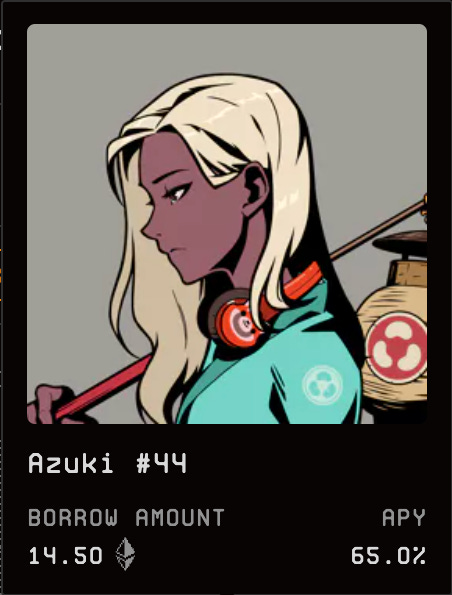

And people are already doing it. On day one, an individual “bought” an Azuki for only 0.04 ETH equity.

3. Risks

However, as always, not everything is as good as it may look at first glance.

3.1 NFTs are not houses

One of the logical problems is: NFTs are not houses to begin with, but highly volatile assets. This can obviously become problematic.

Because while houses in 99.9% of the cases do not lose 50% of their value in a week or are traded ten times a day, it is different with NFTs.

Especially if one recalls the mechanism described above:

Imagine I want to buy a second Azuki, but I currently only have 3 ETH available.

So I take out a 13 ETH loan to finance the NFT. Azuki floor price is at 16 ETH and currently on the rise, there are many loan offers and I find a loan with just 0.1% daily interest. Sounds good, I think Azuki will perform well in the next few months, so why not.

I take the loan and use it to buy an Azuki.

But what’s that? A Blur airdrop farmer just dumped 20 Azukis into bids? Floor is only at 15.5? Okay no problem, I am here for the long-term.

But wait, the lender wants his money back? In 30 hours? Okay, I will just look for a re-financing.

Hmm the loan offers have gotten significantly worse. Now I have to pay 2.5% daily interest for 12 ETH? That's too much interest for me. Meanwhile the floor dropped further, 14.5 now. The rates are getting worse and worse.

And before I know it, the 30 hours are up and "my" Azuki is foreclosed to 14.3 WETH, minus my loan I get back only 1.3 ETH of my 3 ETH and the NFT is also gone.

Admittedly the example is a bit contrived, even though something like this happened a few hours ago. Someone dumped a lot of Azukis and floor price went down 2 ETH in less than an hour:

Of course it can also go the other way. If the floor goes up, then I can sell the NFTs and keep all the profit.

But if a look at the past has shown us anything, it is that things don't always work out great and that things that go up in value most of the time go down sooner or later.

But regardless of wether floor prices go up or down: The promise of "instant liquidity without having to sell the NFT" is nonsense in the sense that you need to be online 24/7 to be ready in case someone withdraws their loan and you need to re-finance quickly.

3.2 Volatility

This is also one of the reasons why volatility will increase immensely. Pumps will be faster and much stronger. Dumps will be all the more dramatic for it.

It is the volatility we already know in the NFT space, on steroids.

Pumps are also likely to last much shorter in the future. More profit in less time will be possible, but only if you get out in time.

In short, it makes NFT space and especially trading even more unpredictable and short-winded. We will see price action that normally takes place over weeks in a single day. Price action that normally takes place in one day, in one hour.

3.3 Predatory Loans

The ability to re-call loans with 30 hour notice is dangerous because it puts people who borrow money into a dependency relationship for predatory loans.

In real life there is regulation on these types of loans and rightly so.

Here is a definition of Predatory Loans:

“Predatory lenders often use aggressive sales tactics and exploit borrowers' lack of understanding of financial transactions. Through deceptive or fraudulent actions and a lack of transparency, they entice, induce, and assist a borrower in taking out a loan they will not reasonably be able to pay back.”

No matter what you think of Blur, this applies here without question:

“Aggressive sales tactics”? Yep, don't worry it's like buying a home. You can buy an Azuki now with just 1 ETH!

“Lack of understanding of financial transactions”? Yep, 90% of the people in this space are gamblers.

“Assist a borrower in taking out a loan they will not reasonably be able to pay back”? Yep, if you buy 15 ETH NFT with just 0.04 ETH in your wallet that's crazy.

Do you enjoy this post so far? If yes, please share it with your friends!

“Okay Wale”, some might say, “but anyone can make loan offers, which means they are always competitive. If one person wants the 0% APY loan back, then other people will provide new loans at the same terms”. But will they?

Again, the only incentive to offer “competitive” loans right now is the $Blur airdrop. No one in their right mind would lend $20k USD with 0.0% interest rates.

It's like with the Blur bids. As long as it rains rewards, everything is fine. But God save us from the day when the music stops and a) there are either no more rewards or b) $Blur goes so far down in value that farming $Blur points is no longer worth it.

3. Impact on the market.

Azuki, Cryptopunks and Miladies all pumped after the introduction of the Blend loans, in some cases by more than 20%.

It brings more liquidity to the market, so the same could be true for other collections where Blur introduces loans next, especially mid and large cap collections could profit from that in the short term.

However, this will eventually stop. As much as I would like to see Azuki at a 100 ETH floor price, the run won't continue indefinitely. Same goes for Cryptopunks and Miladies. At some point there will be a downturn and the people who took loans they couldn't afford in the first place will be in deep sh*t.

This could result in another downward spiral. We started to see this earlier today with Azuki, where a single airdrop farmer dumped his Azukis into bids and caused a panic of people liquidating their NFTs to pay back the money they owed.

And don't get me wrong, there is nothing per se bad about loans. They provide liquidity, I have mentioned the advantages above. And it’s also nothing new. Nftfi and others been doing this for months if not years.

However, in the case of Blend, it is poorly designed in my opinion. 30 hour notice is too little. Financing with virtually no equity is ridiculous. It puts people at risk and has more to do with a casino than it has with investing. The $Blur lending points incentive higher risk bids with the promise of a future airdrop.

Blur's "liquidity at any price" could once again negatively affect mainly the people who let themselves be seduced by marketing slogans or crooked comparisons like "NFTs are like houses" to do something stupid. The "pro-traders" will most likely benefit and exploit it. This is not how we get more people interested in our space, but how we drive people away. The number of active traders has declined since Blur introduced Blend.

In general, I think Blend in its current form is more likely to be another nail in the coffin of the NFT space as many of us know and like it. The hyper-financialization is advancing and predatory loans are the extreme of it. With stuff like this, we are literally begging for regulation to come in.

I don't think this is all going to end well. Sure, floors are pumping right now, everyone is happy and is anticipating a bull market. But I don’t trust the euphoria yet. People said the same thing back when Blur introduced bidding points.

If it makes you money in the short term, then God bless you. But "more liquidity" shouldn't be the only metric when it comes to improving the NFT space.

You have to give Blur credit, though. They are once again bringing a feature to market that leaves the competition in the dust. Blur is on its way to becoming the only relevant marketplace, in part because Opensea & Co. have virtually nothing to counter Blur's innovation. Instead of presenting the NFT space with a counter to Blur's vision of hyper-financialization, they simply copy some parts of it (royalties to 0% etc.) and over time become nothing more than a bad Blur copy.

So whether we like it or not, Blur and therefore Blend will not go anywhere. So why not embrace it and enjoy while it lasts.

Thanks for reading! If you enjoyed this newsletter, feel free to share it on Twitter and tag me so I can retweet it :)

Wale

If you haven’t already, please subscribe now!