Author: Chase Devens, Messari analyst; Translation: Jinse Finance 0xjs

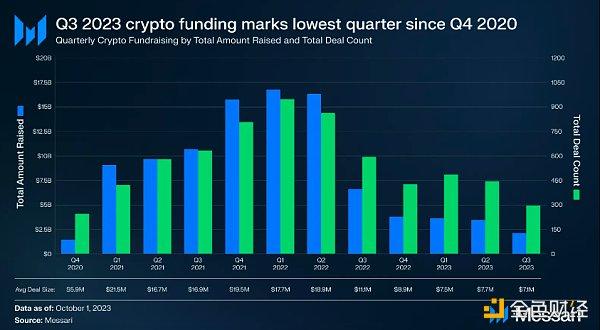

The cryptocurrency industry’s financing data may be the best representation of the current bear market. The third quarter of 2023 was no exception, continuing the downward trend we have witnessed for multiple quarters since the beginning of 2022. The third quarter set new lows in overall financing amount and deal number since the fourth quarter of 2020. Total financing in the third quarter was less than $2.1 billion, involving 297 transactions, a 36% decrease from the previous quarter.

Financing round analysis

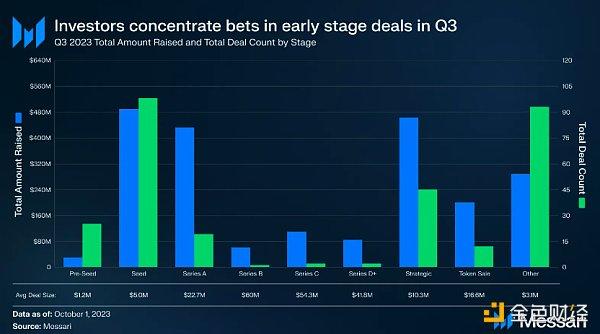

Breaking down Q3’s deals by funding round, we can see that most deals are concentrated in the early stages. Seed rounds accounted for the largest total, raising $488 million across 98 rounds. The trend in the number of transactions shows that in the past three years, the focus of transactions has shifted significantly from late-stage projects to early-stage projects.

The share of early-stage deals (consisting of Pre-Seed, Seed and Series A) increased from 37% in Q4 2020 to 48% in Q3 2023. Meanwhile, late-stage rounds (Series B or higher) fell from 8% in Q4 2020 to 1.4% in Q3 2023. This suggests that investors are strategically adjusting their bear market positioning in an attempt to fund projects that can provide larger multiples of returns in a new bull market.

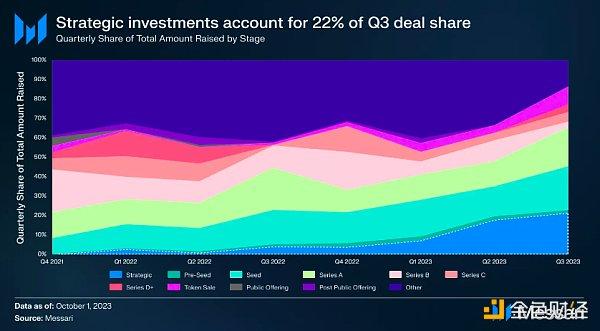

The third quarter also saw significant strategic investment, including corporate and private equity transactions, such as a $200 million investment in Islamic Coin. Strategic financing transactions steadily increased during the bear market. At the peak of the bull market, in Q4 2021, strategic rounds accounted for only 0.2% of total funding. In the third quarter of 2023, this share increased to 22%, indicating that tough market conditions forced projects to pursue short-term bridge financing rounds or eventually be acquired by larger projects.

Financing track analysis

track trends

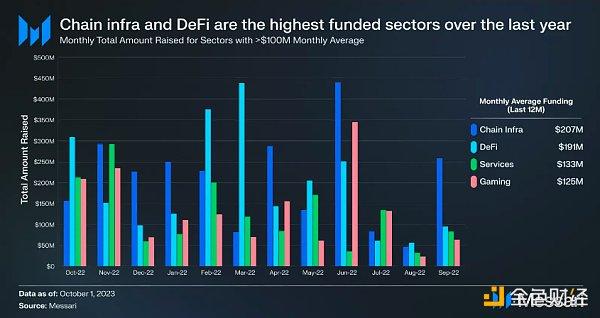

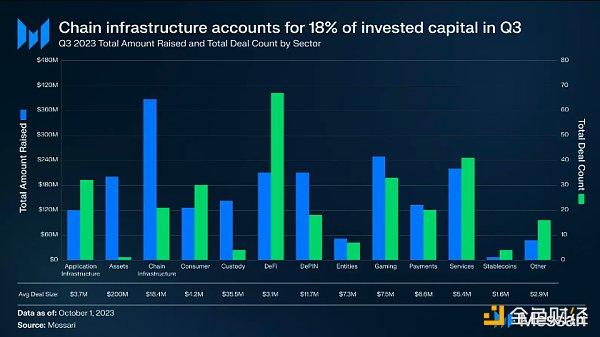

The distribution of track funding in the third quarter of 2023 is similar to the pattern seen over the past 12 months. The public chain infrastructure, DeFi and gaming fields have been the most abundant areas of financing during this period. The services segment, which includes business functions such as marketing, incubators, security and legal services, is the only other track to have raised an average of more than $100 million in the past 12 months. While other areas are also important to the growth of the overall crypto industry, these four areas continue to attract the attention of most investors.

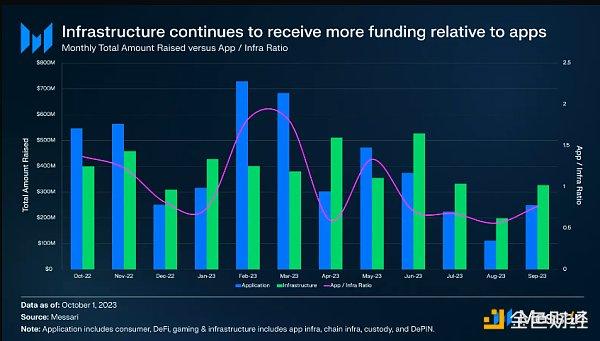

Another notable trend from the past year is that infrastructure projects have received more funding than user-facing applications. This is best demonstrated by categorizing the consumer, DeFi, and gaming domains into “Applications,” and the application infrastructure, public chain infrastructure, custody, and DePIN domains into “Infrastructure.”

When looking at the share of funding in each category, we see a subtle shift away from user-facing applications and toward infrastructure projects. In contrast to the application class, this relationship is funded by ongoing infrastructure projects. However, this trend may not last long, as more and more investors are beginning to realize that without successful user-facing crypto applications, infrastructure investments are unlikely to achieve the returns they expect.

Leading the track

Financing in the third quarter was relatively scattered across various tracks. Public chain infrastructure accounted for 18%, and DeFi led in terms of number of transactions with 67 transactions. Finally, the gaming sector attracted nearly $250 million in investment during the quarter.

Public chain infrastructure

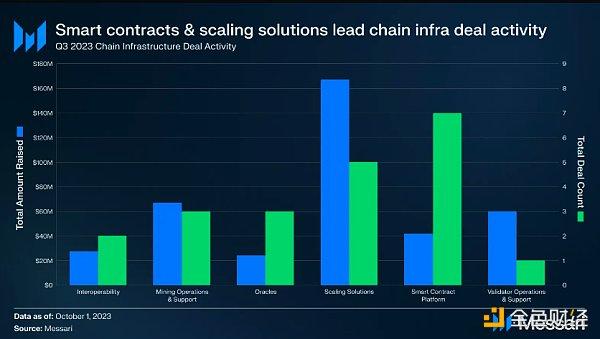

Despite only 21 transactions, the public chain infrastructure track accounted for the largest share of funds in the third quarter. A third of these transactions occurred in the smart contract platform subcategory, one of which was Fhenix’s $7 million funding round to build fully encrypted smart contracts.

Scaling solutions accounted for 43% of the funds raised in this track. This represents an ongoing shift in funding away from smart contract platforms and toward scaling solutions. Funding for scaling solutions exceeded funding for smart contract platforms for the first time in the first quarter of 2022, when Polygon raised $450 million for its suite of scaling solutions. In three of the past four quarters, the ratio of funding for scaling solutions to funding for smart contract platforms has surpassed the previous high ratio of Q1 2022. This ratio even reached 7 times in the fourth quarter of 2022, mainly due to less investment activity in the smart contract platform category during that quarter.

In the third quarter of 2023, more than 40% of the US$387 million in financing for public chain infrastructure came from the approximately 116 million OP tokens sold by the Optimism Foundation in late September. Other standout deals in the track include Flashbots’ $60 million Series B round to continue development of SUAVE, and Bitmain’s $54 million strategic investment in Core Scientific, a leading Bitcoin mining company.

DeFi

DeFi was the area with the most projects receiving funding in the third quarter, with a total of 68 transactions. Investment in this area is concentrated in the exchange category, which accounts for 38% of all invested capital and a total of 33 transactions. Overall, DeFi projects raised $210 million, with an average deal size of $3 million.

Binance Labs is an active investor in the DeFi space, with seven transactions in Q3, including strategic investments of $10 million each in Helio Protocol (a liquidity staking platform on BNB Chain) and Radiant Capital (a money market on LayerZero). The largest DeFi deal of the quarter came from a $16.5 million Series A round from Brine, an order book DEX built on Starkware.

Three of the top four DeFi investors by transaction volume in the third quarter were ecosystem entities. Binance Labs, Base Ecosystem Fund and Polygon completed a total of 16 transactions.

game

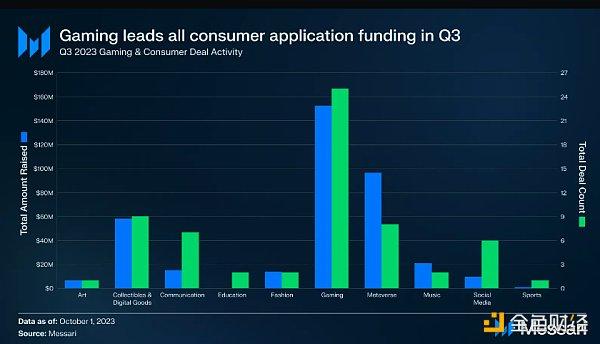

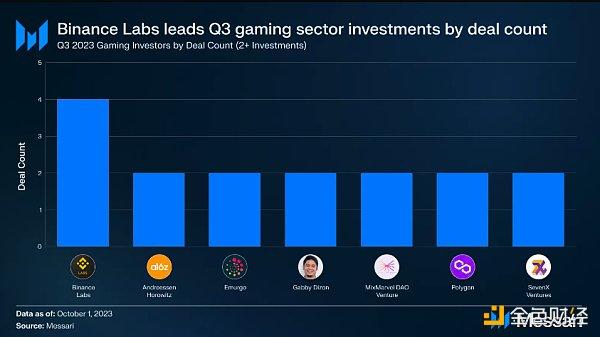

The gaming space accumulated a number of early-round deals, helping it become the third-highest-funded space in the third quarter, with 33 deals raising $249 million. Compared with other user-oriented consumer areas, gaming accounted for 67% of financing in the third quarter.

Most deals in gaming come from long-tail investors. Only seven entities have deals with two or more projects, while 104 investors have invested in single projects within the sector.

The biggest deal in gaming was a $54 million Series A funding deal for Futureverse, a platform that combines artificial intelligence with the world of the Metaverse. Other Metaverse gaming projects in the space, such as Mocaverse and Mahjong Meta, also received funding during the quarter. Finally, Proof of Play raised $33 million in seed funding from lead investors a16z and Greenoaks. The on-chain gaming studio, founded by Amitt Mahajan, one of the original co-creators of the popular Zynga game Farmville, hopes blockchain-based games can recreate the growth trajectory of early free-to-play mobile games.

Investor analysis

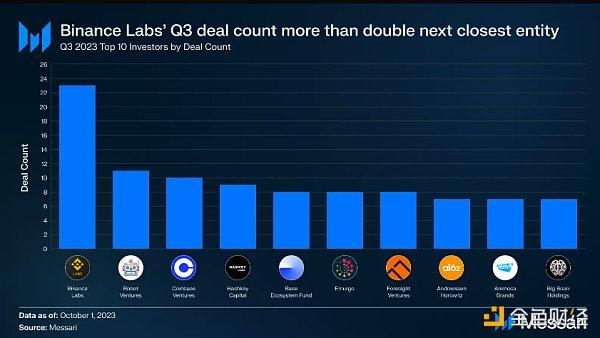

In the third quarter of 2023, the top ten most active investors in the crypto industry made 98 investments. Despite this activity, they accounted for only 7% of all investor trades, indicating that crypto investing is still dominated by more tail investors.

Binance Labs is by far the most active investor: its 23 transactions in the third quarter were more than double those of the second-place investor, Robot Ventures. As we highlighted in August, Binance Labs has been actively investing in 2023, with a focus on DeFi and gaming. In addition, projects that are developing zero-knowledge and privacy technologies are also investment targets of Binance Labs. Notably, 12 of Binance Labs’ 23 transactions were projects participating in its accelerator program. But even if these projects are excluded, Binance Labs’ 11 other investments still put it tied with Robot Ventures for third-quarter deal activity.

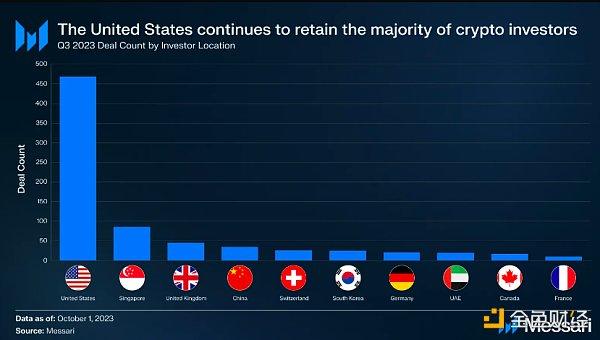

Finally, 54% of active investors in Q3 2023 were located in the United States. This figure is consistent with the quarterly average over the past four years (55%). Although project founders are gradually leaving the United States for more regulatory-compliant jurisdictions, the United States is still home to the majority of professional crypto investors.