Bitcoin has gained prominence as a safe-haven asset, but remains undervalued.

Original article: Bitcoin: A Unique Risk-Off Asset? (ARK Invest)

By: Yassine Elmandjra , Head of Digital Assets, ARK Invest

Compiled by: Luffy, Foresight News

Cover: Photo by Shubham's Web3 on Unsplash

Trust in governments and financial institutions declined as a result of the 2008 global financial crisis. Since then, events such as the European sovereign debt crisis, the Fed’s response to COVID19, and the collapse of major regional banks in the United States have exposed the drawbacks of relying on centralized institutions.

As the impact of technological innovation accelerates, the decline in trust calls into question the effectiveness of traditional safe-haven assets in protecting modern portfolios. Are government bonds less risky after events such as the European sovereign debt crisis? Is physical gold less effective as a hedge in the digital economy? Will the Fed's inconsistent policy threaten the dollar's status as a reserve currency? Traditional safe-haven assets may have a role to play in portfolio construction, but their limitations give investors reason to re-evaluate so-called safe-haven assets.

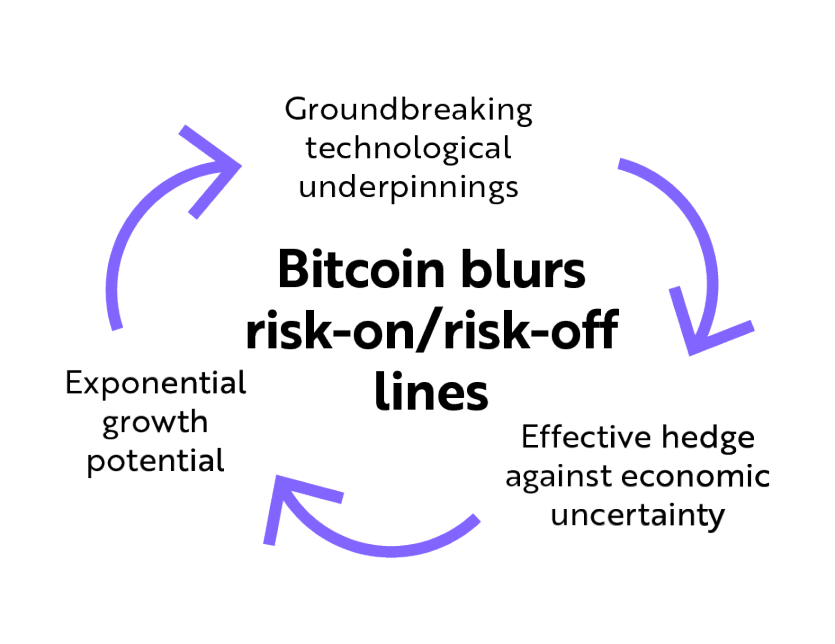

While the “risk appetite” and “risk aversion” characteristics of traditional assets are mutually exclusive, Bitcoin blurs the distinction between the two. Its revolutionary technology and novelty are risk appetite, while as a monetary asset, its absolute scarcity and its role as a “bearer instrument” are risk aversion.

Bitcoin presents an interesting paradox: with its groundbreaking technology, it can be an effective hedge against economic uncertainty and potentially enable exponential growth.

Bitcoin was created in 2008 as a response to the global financial crisis. Today, it has evolved from a fringe technology to a new asset class worthy of institutional allocation. As the network matures, investors may seriously evaluate the value of Bitcoin as a safe-haven asset.

Bitcoin as a safe haven asset

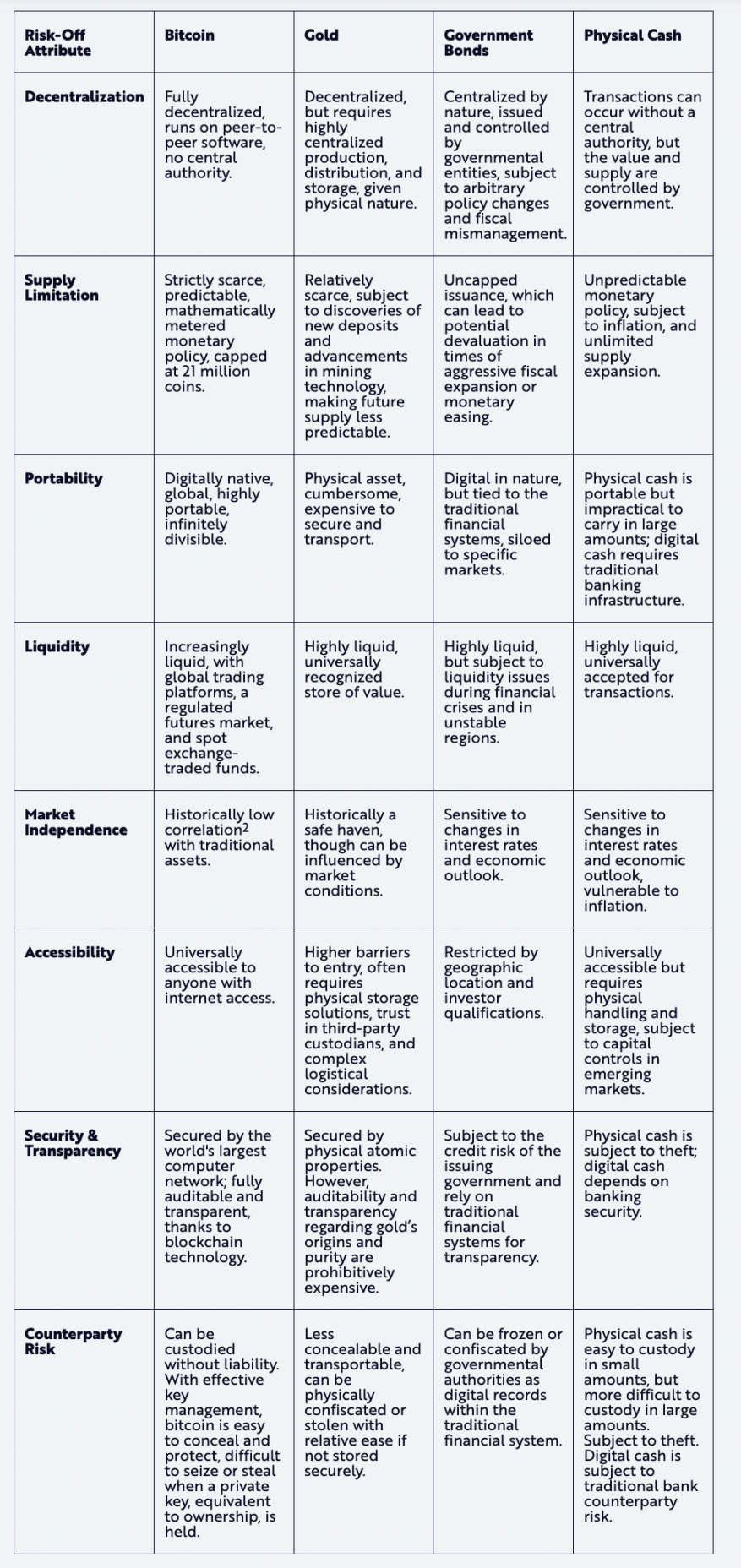

While Bitcoin’s explosive growth and price volatility have led many investors and asset allocators to view Bitcoin as the epitome of a risk-on asset, we believe that the Bitcoin network embodies safe-haven characteristics that enable financial sovereignty, reduce counterparty risk, and increase transparency.

Bitcoin is the first digital, independent, global, rules-based monetary system in history. By design, its decentralization should mitigate the systemic risks of the traditional financial system, which relies on centralized intermediaries and human decision-makers to create and enforce rules. Capital "B" Bitcoin represents a financial network used to facilitate the transfer and safekeeping of lowercase "b" Bitcoin, a scarce digital currency asset.

We believe Bitcoin is the purest form of money ever created. It has the following characteristics:

- A digital bearer asset similar to a commodity.

- An asset that is scarce, liquid, divisible, portable, transferable, and fungible.

- Auditable and transparent assets.

- Assets that can be held in custody entirely through title matching with no liability or counterparty risk.

Importantly, Bitcoin's properties derive from the Bitcoin network running on open source software. While many institutions coordinate functions in the traditional financial system, Bitcoin operates as a single institution. Rather than relying on central banks, regulators, and other government decision-makers, Bitcoin relies on a global network to enforce rules, transforming enforcement from manual, private, and opaque to automated, public, and transparent.

Given its technological foundations, Bitcoin has a unique position relative to traditional safe-haven assets, as shown below.

Bitcoin's relative performance

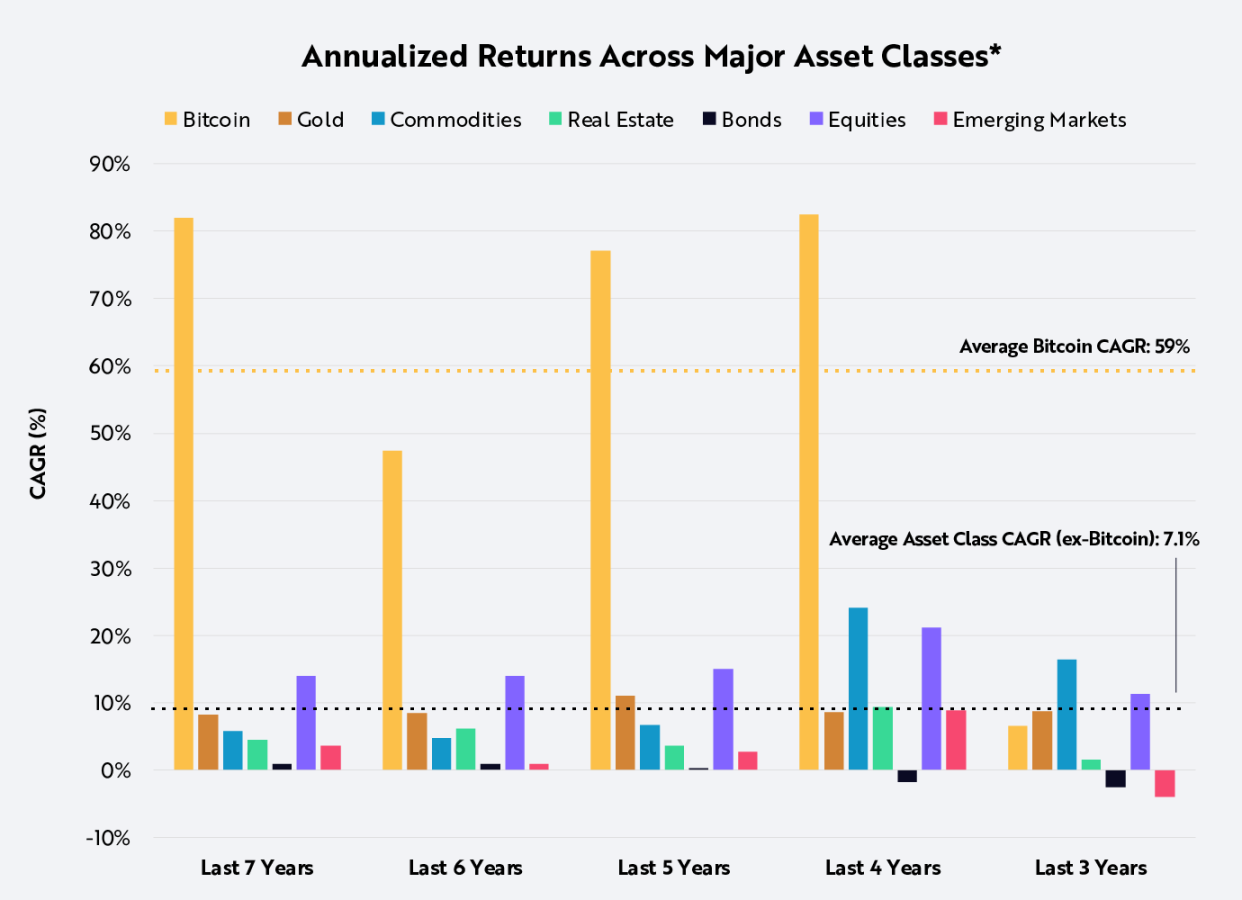

As an emerging asset, Bitcoin's speculative nature and short-term volatility have attracted much attention. 15 years after its birth, Bitcoin's market value has exceeded $1 trillion, increasing its purchasing power while maintaining its independence.

In fact, Bitcoin has outperformed all other major asset classes in both the short and long term. Over the past 7 years, Bitcoin has delivered an annualized return of nearly 60%, while other major assets have averaged only 7%, as shown in the chart below.

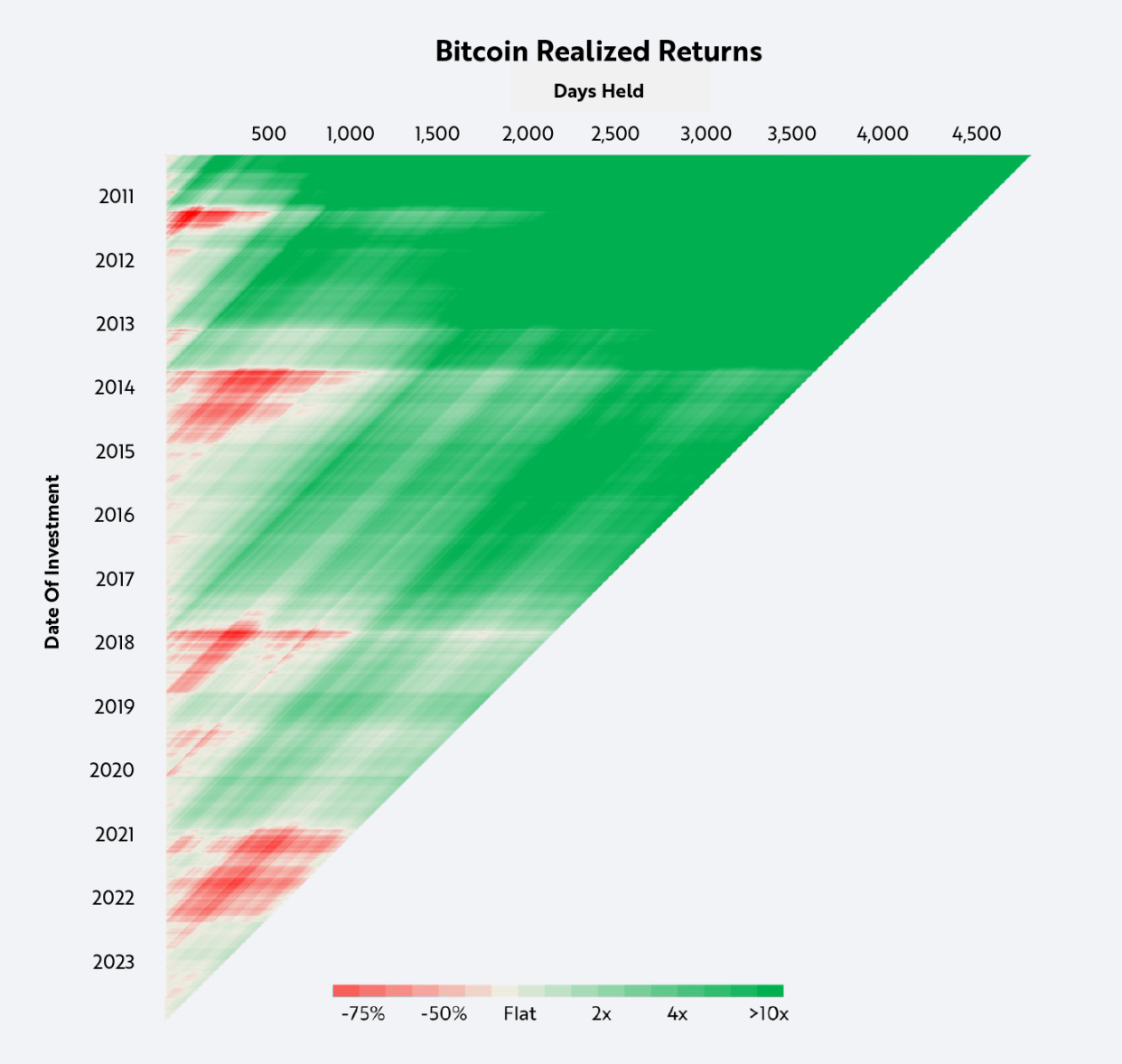

Importantly, investors who held on for 5 years have made a profit regardless of when they bought Bitcoin since its inception, as shown below.

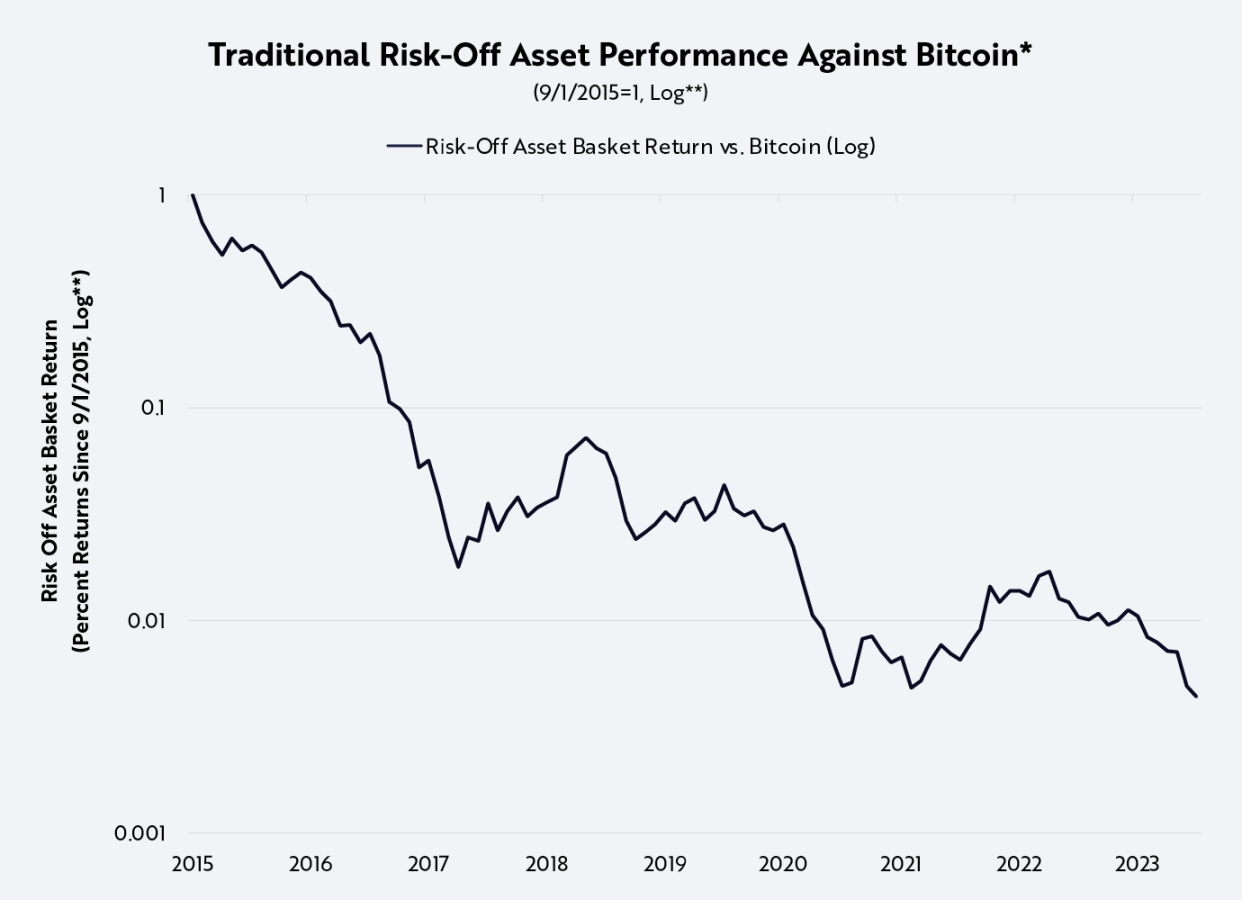

In contrast, traditional safe haven assets such as gold, bonds and short-term U.S. Treasuries have lost 99% of their purchasing power over the past decade, as shown below.

Is Bitcoin too volatile to be a safe-haven asset?

Paradoxically, Bitcoin's volatility is a function of Bitcoin's monetary policy, which highlights its credibility as an independent monetary system. Unlike modern central banks, Bitcoin does not prioritize price or exchange rate stability. Instead, by controlling the growth of Bitcoin's supply, the Bitcoin network prioritizes the free flow of capital. Therefore, Bitcoin's price is a function of demand relative to supply - which explains its volatility.

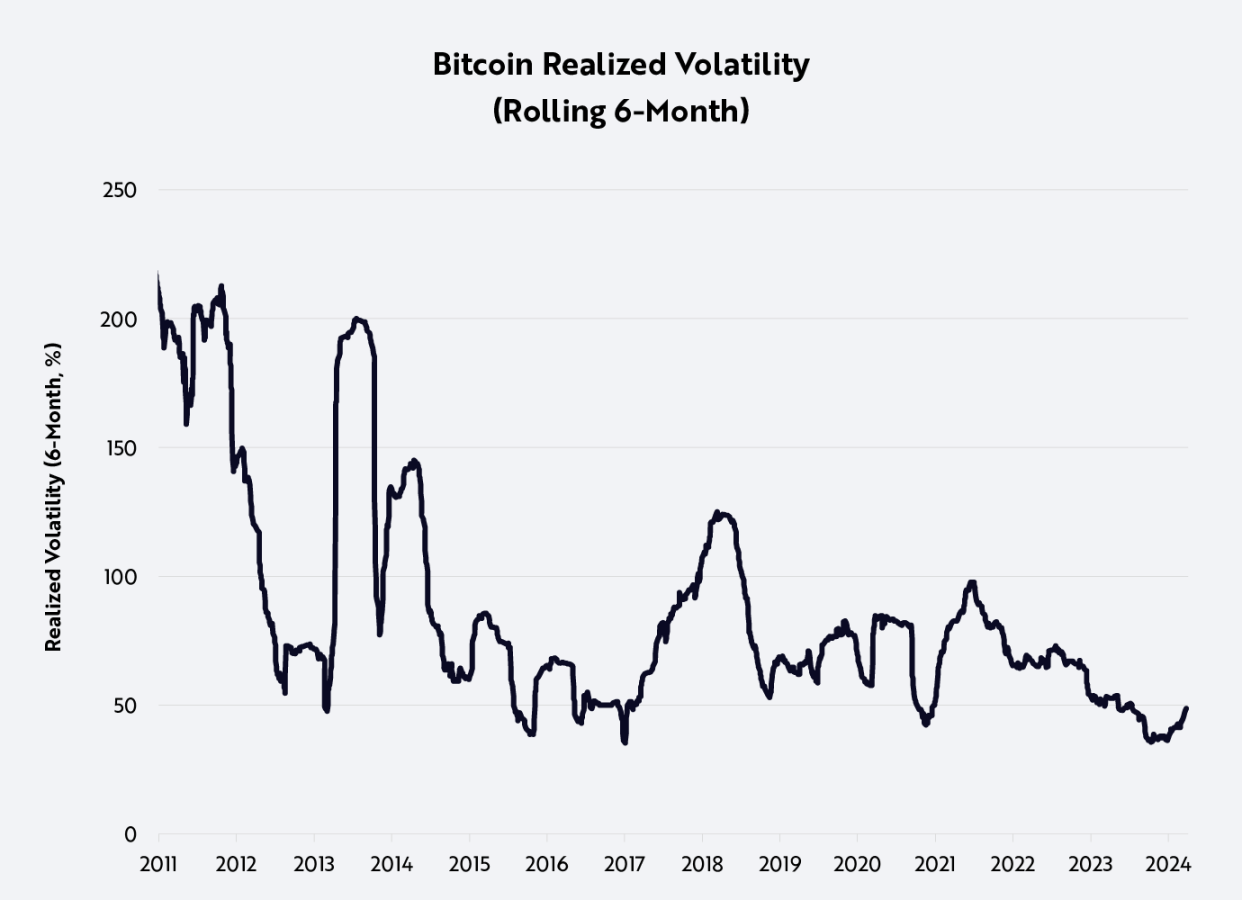

Despite this, Bitcoin’s price volatility has decreased over time, as shown below:

Why has Bitcoin's price volatility declined over time? As Bitcoin adoption has increased, the marginal demand for Bitcoin has decreased relative to its entire network value, reducing the magnitude of its price fluctuations. All else being equal, $1 billion in new demand for a $10 billion network value should have a greater impact on Bitcoin's price than $1 billion for a $1 trillion network value. Importantly, volatility should not hinder Bitcoin's role as a store of value in the context of a significant price increase.

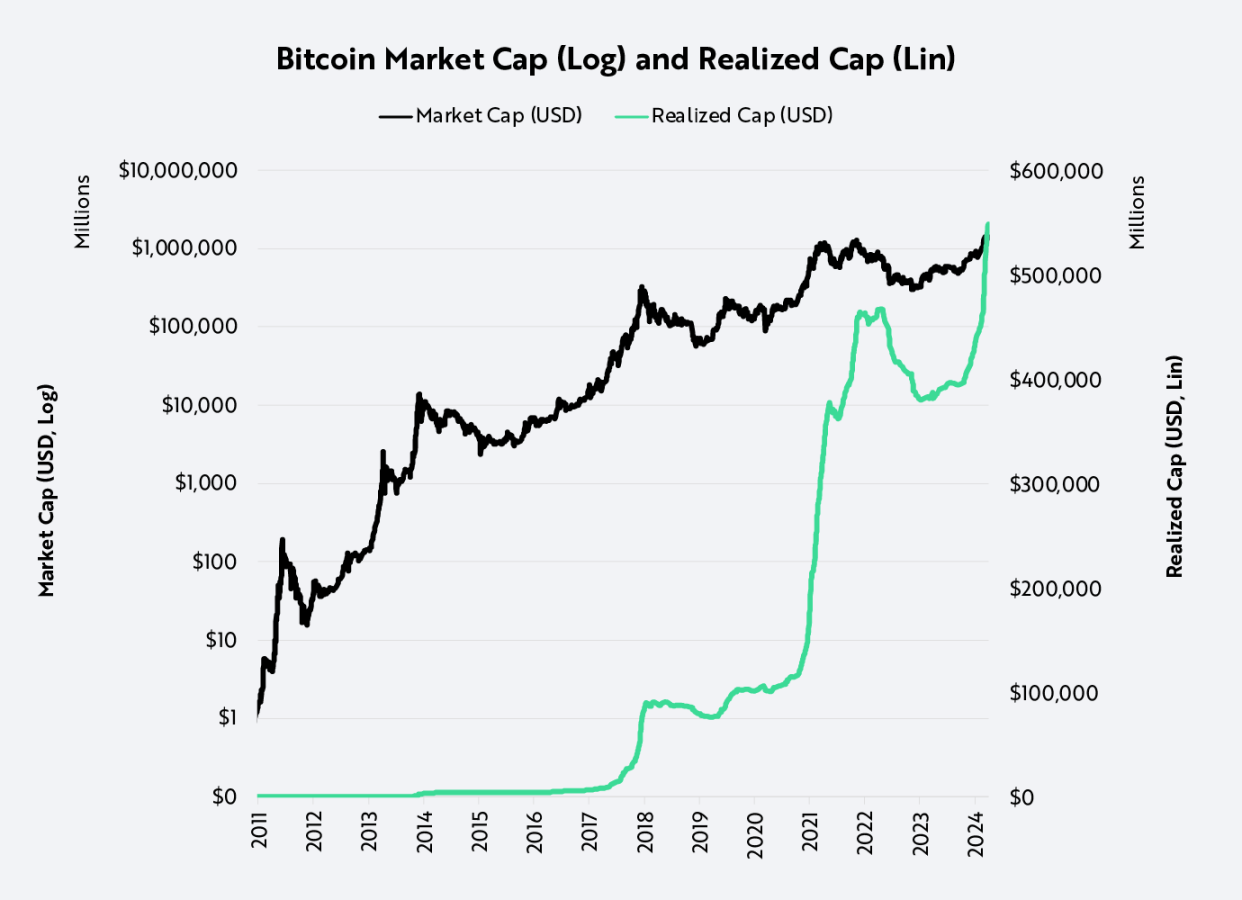

Perhaps a more relevant metric that demonstrates Bitcoin’s role in preserving capital and purchasing power is its market cost basis. While market cap aggregates the value of all circulating Bitcoin at its current price, market cost basis values each Bitcoin at the price it last changed. Cost basis provides a more accurate measure of changes in purchasing power. Fluctuations in cost basis are less pronounced than price fluctuations, as shown below. For example, while Bitcoin’s market cap fell by approximately 77% from November 2021 to November 2022, its cost basis fell by only 18.5%. Today, Bitcoin’s cost basis is trading at an all-time high, 20% above its 2021 market peak.

Bitcoin’s independence from other asset classes

Low correlation

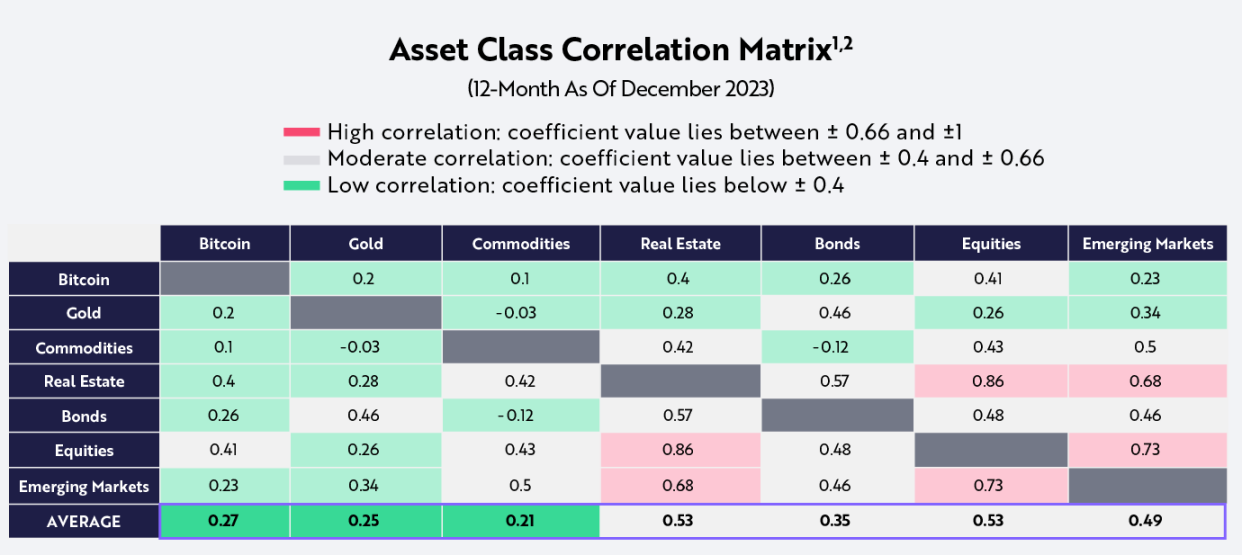

Another reason why Bitcoin is suitable as a safe haven asset is that its returns have a low correlation with the returns of other asset classes. Bitcoin is one of the few assets that has a consistently low correlation, as shown below. Between 2018 and 2023, the correlation between Bitcoin returns and traditional asset classes averaged only 0.27. Importantly, the correlation between bonds and gold (traditionally considered safe haven asset classes) is relatively high at 0.46, while the correlation between Bitcoin returns and gold and bond returns is 0.2 and 0.26 respectively.

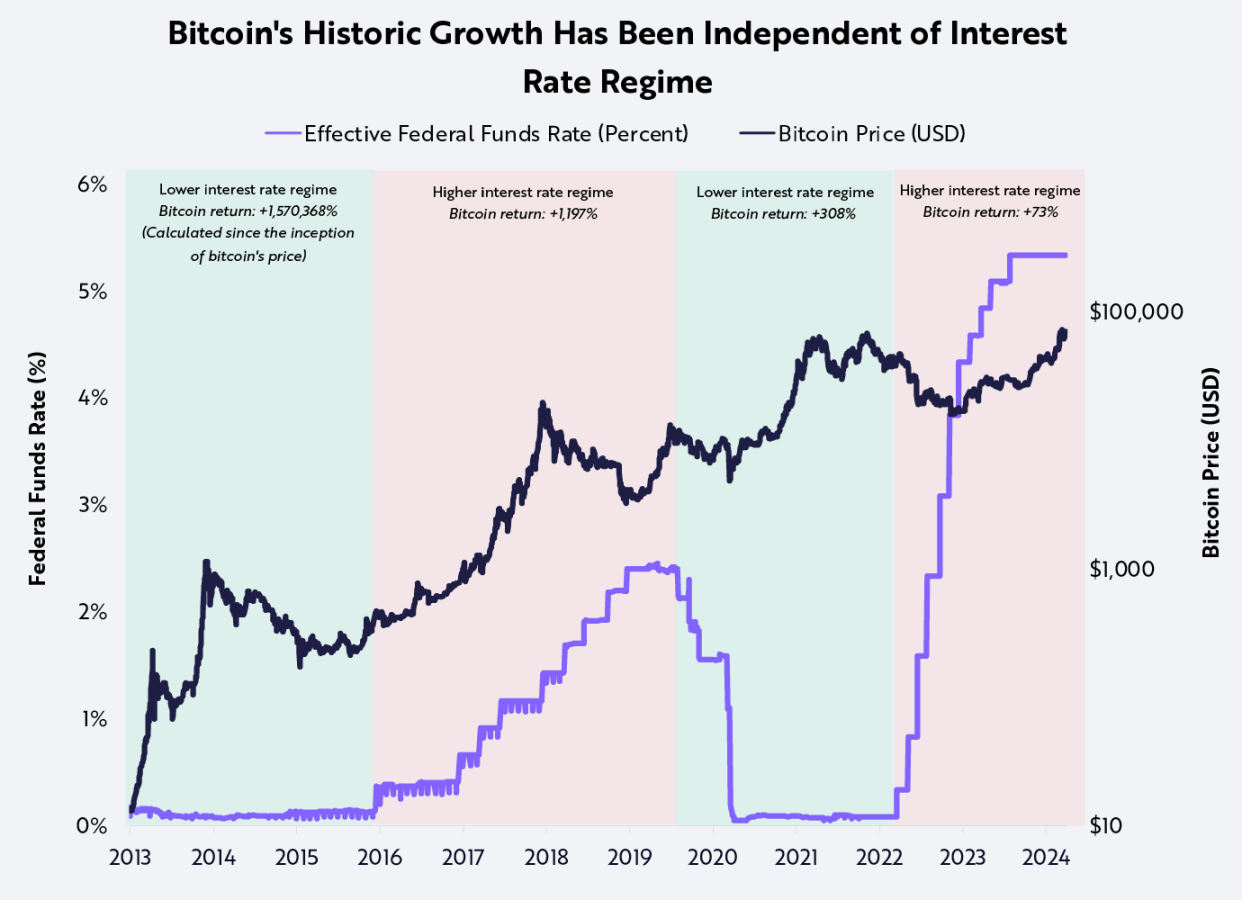

Adapting to changing interest rate policies

Furthermore, comparing Bitcoin’s price to the Federal Funds Rate shows its resilience across different interest rate and economic environments, as shown below. Importantly, Bitcoin’s price has risen significantly in both high and low interest rate regimes, as shown below.

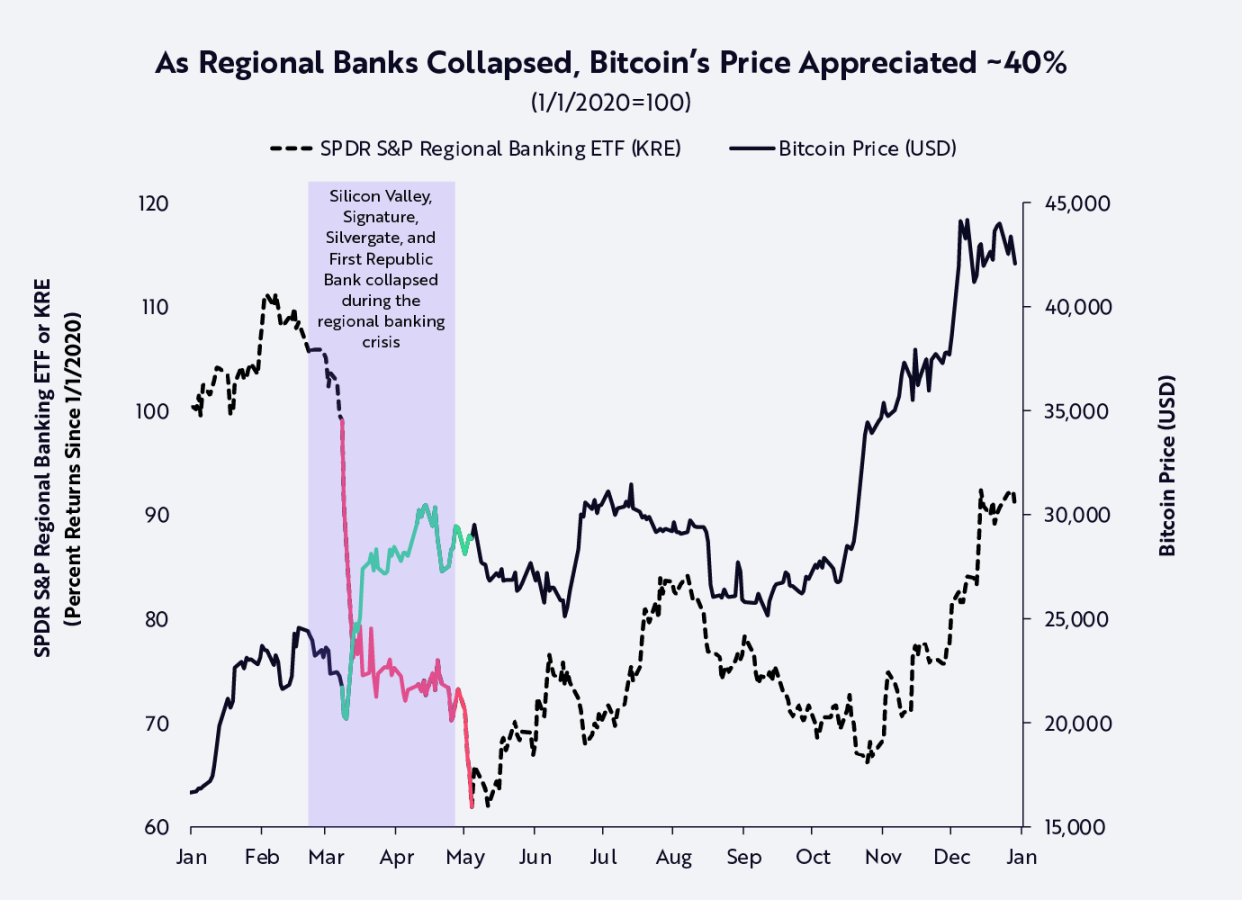

Over the past decade, Bitcoin’s price has performed well during periods of risk aversion. As of the time of writing, Bitcoin’s price has risen after each crisis event, as shown in the chart below.

Bitcoin’s performance during the regional banking crisis is a notable example. In early 2023, during the historic collapse of regional banks in the United States, the price of Bitcoin rose by more than 40%, highlighting its role in hedging counterparty risk, as shown in the figure below.

While Bitcoin has experienced declines, the setbacks it has experienced have been industry-specific and idiosyncratic, including the Mt. Gox exchange hack in 2014, the initial coin offering (ICO) bubble in 2017, and the FTX fraud collapse in 2022. In each of these cyclical declines, Bitcoin has proven its antifragility.

Looking ahead

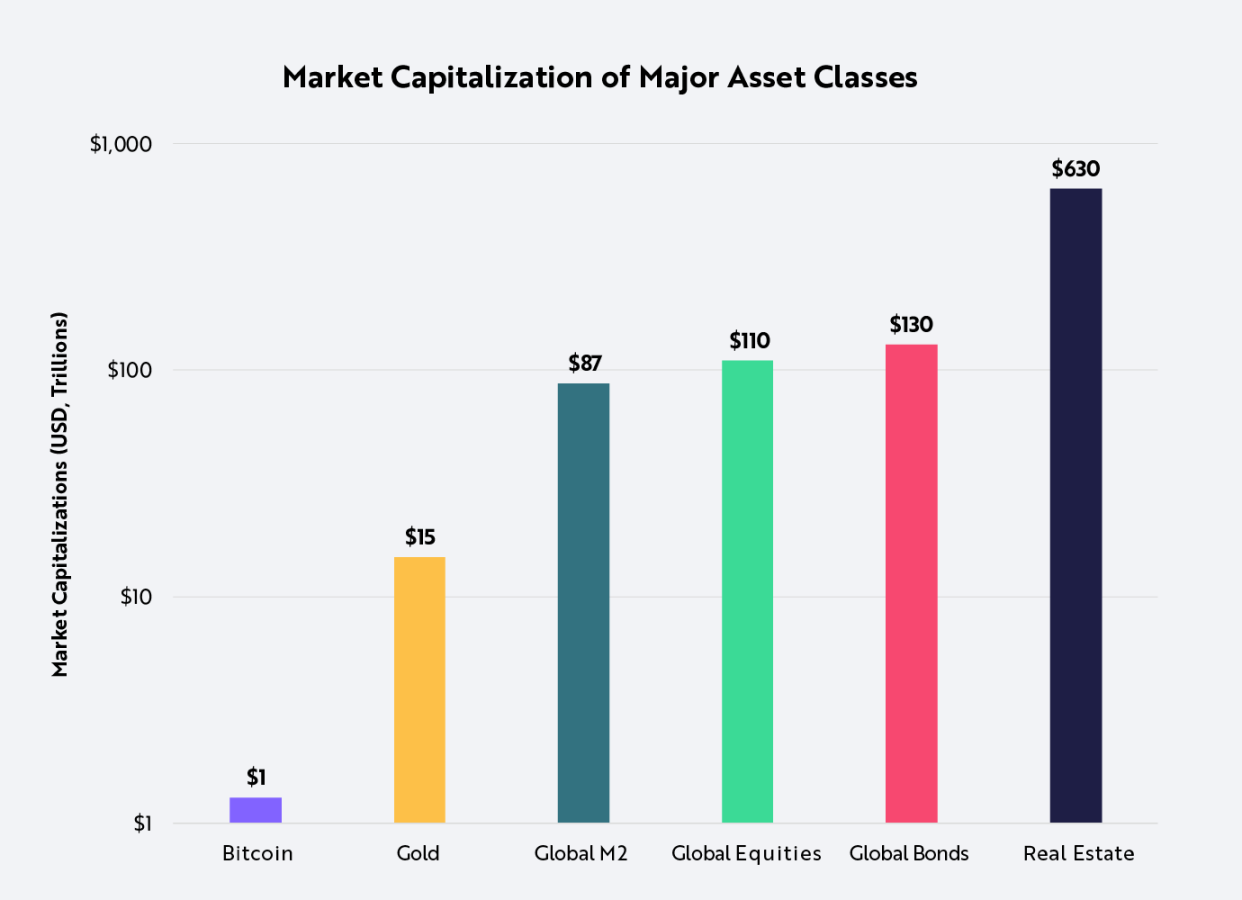

In its short history, Bitcoin has gained significant status as a safe-haven asset, but remains undervalued. As the global economy continues to shift from a physical economy to a digital economy, the use of Bitcoin’s global decentralized monetary system should continue to increase, potentially making Bitcoin comparable to traditional safe-haven assets. Recent events have increased this likelihood, such as the approval of a spot Bitcoin ETF in the United States, the adoption of Bitcoin as legal tender by nation-states such as El Salvador, and the allocation of Bitcoin reserves by companies such as Block, Microstrategy, and Tesla. With Bitcoin currently valued at approximately $1.3 trillion and fixed income assets valued at $130 trillion, the global safe-haven asset appears ripe for disruption.

Summarize

Bitcoin is a relatively new asset class and the Bitcoin market is rapidly changing and full of uncertainty. Bitcoin is largely unregulated and Bitcoin investments may be more susceptible to fraud and manipulation than regulated asset classes. Bitcoin is subject to unique and significant risks, including large price fluctuations, lack of liquidity, and theft.

Bitcoin's price fluctuates wildly, influenced by the actions and statements of influential people and the media, changes in the supply and demand for Bitcoin, and other factors, making it difficult for Bitcoin to maintain its value over the long term.

Disclaimer: As a blockchain information platform, the articles published on this site only represent the personal opinions of the author and guests, and have nothing to do with the position of Web3Caff. The information in the article is for reference only and does not constitute any investment advice or offer. Please comply with the relevant laws and regulations of your country or region.