Introduction

This month, the BTC halving did not come as expected. Instead, it has been fluctuating downward since the beginning of the month. At the same time, the postponement of the expected US interest rate cut and the continuous outflow of BTC spot ETFs have made people more negative about the future market, and the market value and transaction volume of crypto assets have declined significantly. At the same time, the impact of the reduction in BTC miners' income began to appear at the end of the month. The stock prices of listed mining companies fell to varying degrees, and some mining machines were close to the shutdown price, which further weakened the momentum of the subsequent market rebound and delayed the expected time.

1. Macro perspective

1.1 The expected US interest rate cut was postponed, and the crypto market was affected and fell

On April 10, 2024, the U.S. CPI data was released. The U.S. core CPI has exceeded expectations for three consecutive months, both year-on-year and month-on-month:

- The unadjusted CPI annual rate in March was 3.5% (previous value was 3.2%, predicted value was 3.4%), and the seasonally adjusted CPI monthly rate in March was 0.4% (previous value was 0.4%, predicted value was 0.3%);

- The unadjusted core CPI annual rate in March was 3.8% (previous value 3.8%, forecast value 3.7%), and the core CPI monthly rate in March was 0.4% (previous value 0.4%, forecast value 0.3%);

After the data was released, the three major U.S. stock index futures fell, and the U.S. dollar index rose in the short term. CPI data is an important reference for when the Federal Reserve will cut interest rates this year. From the end of last year to the beginning of this year, the market has been optimistic about the Federal Reserve's interest rate cut earlier this year, but the continued stability and strengthening of the U.S. economy has repeatedly frustrated analysts' predictions of interest rate cuts.

At the beginning of the year, some people believed that the four halvings of BTC, coupled with the BTC spot ETF and the Fed’s interest rate cut expectations, would most likely create a new bull market cycle in the crypto market. However, the “stubbornness” of US economic inflation has also calmed the entire market to a certain extent. With the release of the US CPI data in April, the crypto market has no expectations for the possibility of a rate cut in May, which has also become an indirect factor in the continued volatility and decline in the market in April.

1.2 Hong Kong ETFs approved, physical subscription and redemption may become a competitive advantage

On April 15, China Asset Management (Hong Kong), Bosera Asset Management (International) Co., Ltd., and Harvest Investments issued an announcement stating that they had obtained conditional approval from the Hong Kong Securities and Futures Commission (SFC) to issue Bitcoin and Ethereum spot ETFs. Hong Kong has become the second region after the United States to approve a Bitcoin spot ETF, and it is also the first region to approve an Ethereum spot ETF.

Hong Kong's clear regulatory framework has made it possible to quickly pass BTC and ETH ETFs, which is Hong Kong's advantage in regulatory policy compared to the United States. More importantly, the attitude and actions of the Hong Kong Securities Regulatory Commission reflect its determination and action to make great strides in the crypto market, providing important support for Hong Kong to regain the confidence of global capital.

Although there is a big gap between the first-day trading volume of the six ETFs in Hong Kong and the first-day trading volume of the US Bitcoin spot ETF, the market is still optimistic and believes that ETFs, as a new channel for old money to enter the market, will attract more traditional institutional investors to enter. At the same time, the support of physical subscription and redemption for Hong Kong Bitcoin and Ethereum spot ETFs will also promote the overall growth of the market size, and it is possible to achieve unexpected overtaking.

1.3 BTC miners’ income has dropped significantly, and the impact has begun to emerge

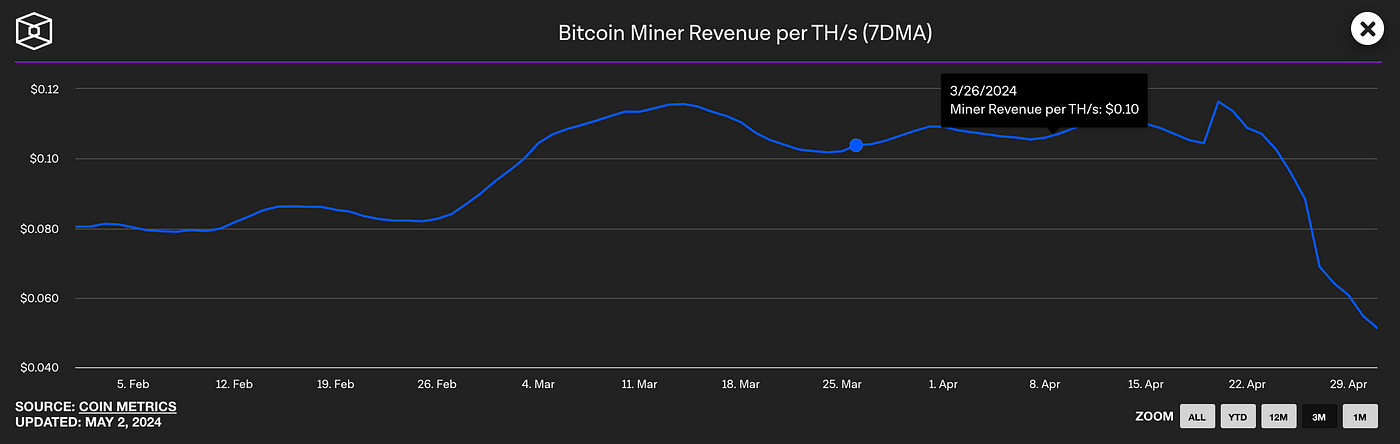

CoinShares' latest report: After the BTC halving, miners are facing a significant increase in costs, with electricity and overall costs almost doubling. Calculated at $0.06 per kWh, after the halving, Antminer S19, T19, Whatsminer M33S+, M30S+ and mining machines with lower energy efficiency are all close to the shutdown price. The average BTC production cost is estimated to be about $53,000.

In addition, according to Glassnode data, although Runes transactions have generated a total of about $117 million in Bitcoin network fee income after the halving, the Bitcoin fee income has declined significantly over time, with Runes transaction fees reaching $1.03 million on April 28. As the popularity of Runes decreases, miners' income decreases, and the electricity costs of the most advanced Bitcoin mining machines currently account for more than 50%.

To cope with the decline in income after production cuts:

- Bitfarms announced an investment of $240 million to upgrade its Bitcoin mining equipment, with the goal of maintaining profitability after the Bitcoin halving in 2024;

- Bitmain tweeted that the Antminer L9 will be released in May, supporting LTC, DOGE, and BEL mining, with a power consumption ratio of 0.21 J/M;

- Asher Genoot, the new CEO of Hut 8, said that the strategic cornerstone of Hut 8 is based on diversified revenue sources and huge Bitcoin holdings, and it is ready to acquire those miners in trouble;

- Mining companies have begun to turn to the field of artificial intelligence, trying to reduce costs by optimizing energy costs and mining efficiency. Mining companies such as BitDigital, Hive and Hut 8 have already earned revenue from the AI field;

Judging from the performance of mining companies, they are still optimistic about the market and are actively responding. They are increasing their profitability, improving their income structure and consolidating their market position through cost operation control, more efficient equipment and asset category expansion. Although the impact of the halving has not subsided, it is being hedged and absorbed.

2. Industry data

2.1 Market value & ranking data

In this month's volatile market, the market value of the top 10 tokens has dropped to varying degrees, and the ranking has also changed. USDC surpassed STETH and XRP to jump to the 6th place, and TON jumped to the 10th place. From the perspective of 30-day changes, DOGE fell 37.6%, the largest decline, followed by SOL's 36.6% and XRP's 21.6%. BTC ranked 6th with a decline of 14.1%.

The decline of this month started at the beginning of the month, with occasional rebounds (about 5 days per cycle), mainly driven by the decline of the market driven by BTC, especially after the announcement of the postponement of the expected interest rate cut in the United States, the slope and speed of the decline have increased significantly. Among them, although TON has declined, with the frequent actions and good empowerment of the TON ecosystem, it is the best performing token among the top 10 tokens except USDT and USDC, and is unanimously optimistic by the market.

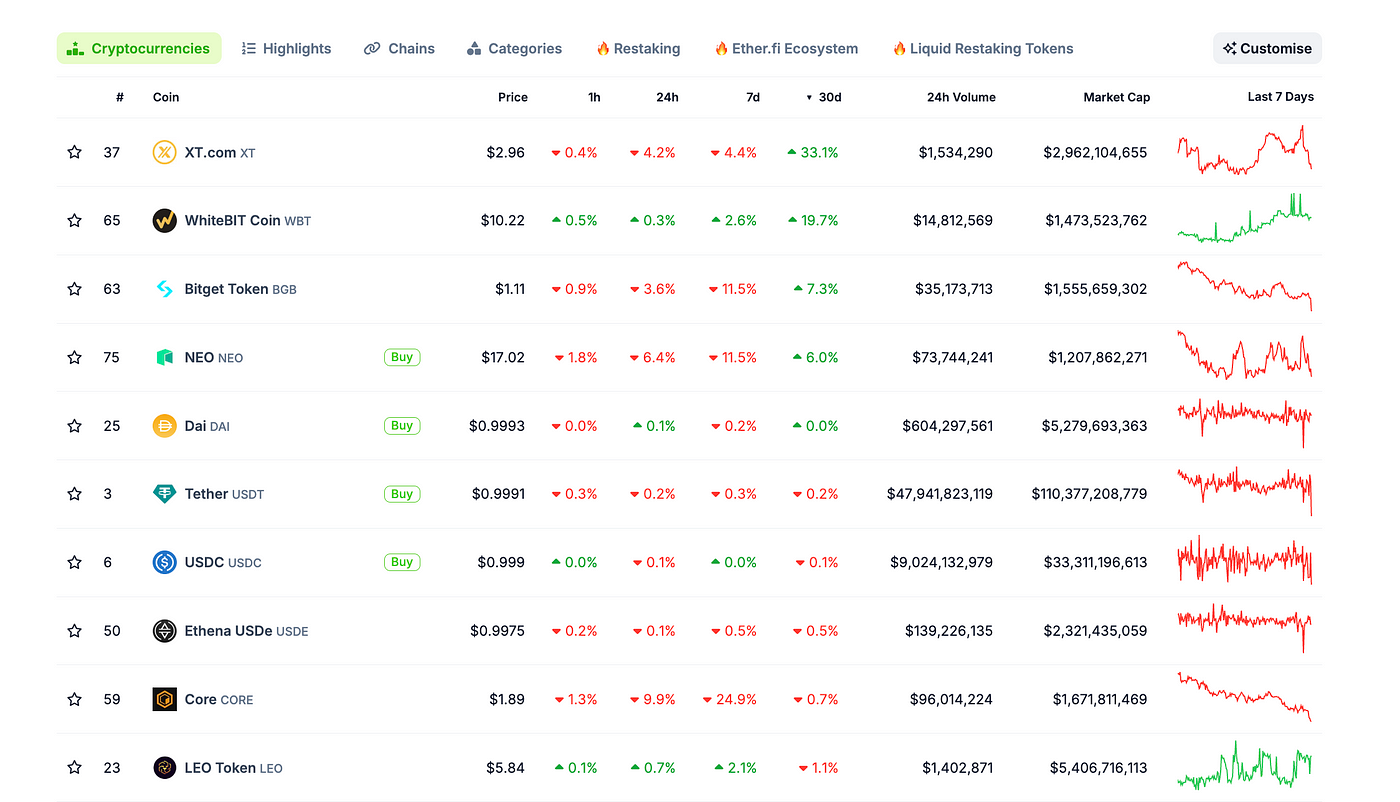

Among the top 100 tokens by market capitalization, the tokens with the highest growth in March were XT (+33.1%), WBT (+19.7%), and BGB (+7.3%). ZT, WBT, and BGB are all CEX platform tokens. Currently, ZT and WBT are still maintaining an upward trend, among which WBT is particularly strong, while BGB is showing a downward trend. It is expected that its growth rate and trend will be close to the overall market trend in May.

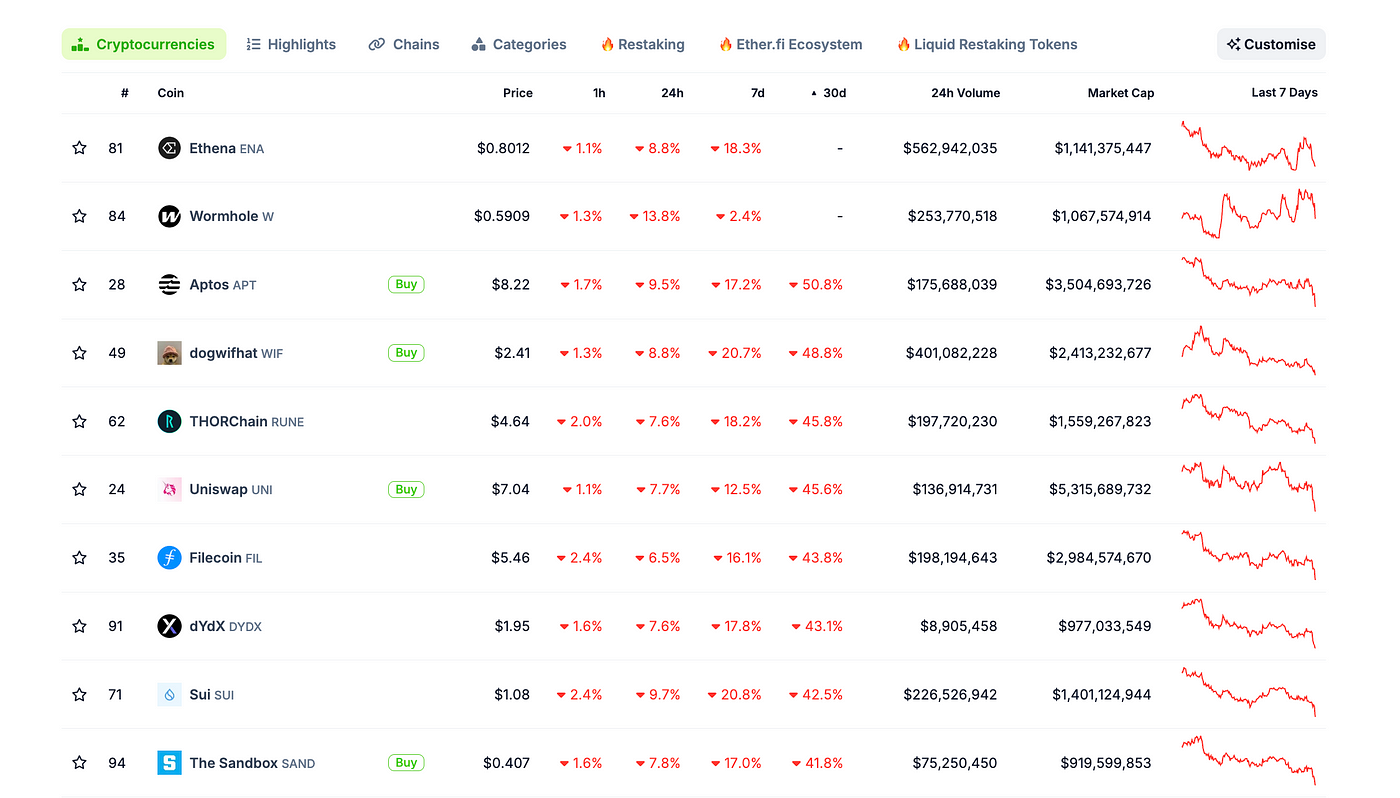

Looking at the overall rise and fall of the top 100 tokens by market value, APT’s 50.8% decline ranks first in the decline. The main reason is that APT welcomed a large amount of token unlocking of about 330 million US dollars this month. While the market fluctuated downward, the expectation of a large number of tokens entering the market has led to a continuous decline in the price and TVL since the beginning of the month. As of April 30, the price was $8.22, and the rebound force was almost zero. Investors are advised to pay close attention to the dynamics of token unlocking. In a volatile and downward market, large-scale unlocking may lead to a large proportion of short-term losses, so they need to be especially cautious.

2.2 Stablecoin Inflow and Outflow

The total amount of stablecoins in April was close to $160B, an increase of about $10B compared to March. Judging from the slope of the curve, this growth is gradually slowing down. Combined with the current market trading activity, the growth in the short and medium term is already weak. If there is no special positive information, the weak growth trend will continue, and the possibility of negative growth in May cannot be ruled out.

Among the top 10 stablecoins by market capitalization, the fastest growing stablecoin this month is FDUSD, which increased by 73.00%, followed by USDe, which increased by 51.87%. After a slight decline last month, FDUSD regained the top spot in the growth list this month, and USDe continued to perform as well as last month, showing a strong momentum; it is rising rapidly in the competition of stablecoins. In addition, PYUSD, a stablecoin launched by traditional payment institution Paypal, is currently ranked 12th. Combined with the empowerment and support of Paypal in cross-border remittance services, the issuance of PYUSD has been growing steadily, and is expected to enter the top 10 stablecoin market capitalization ranking in May.

According to PayPal's official website: its cross-border remittance service Xoom Finance now allows US Xoom users to convert their PayPal stablecoin PYUSD into US dollars and use it as a source of funds to remit to recipients in approximately 160 countries/regions around the world.

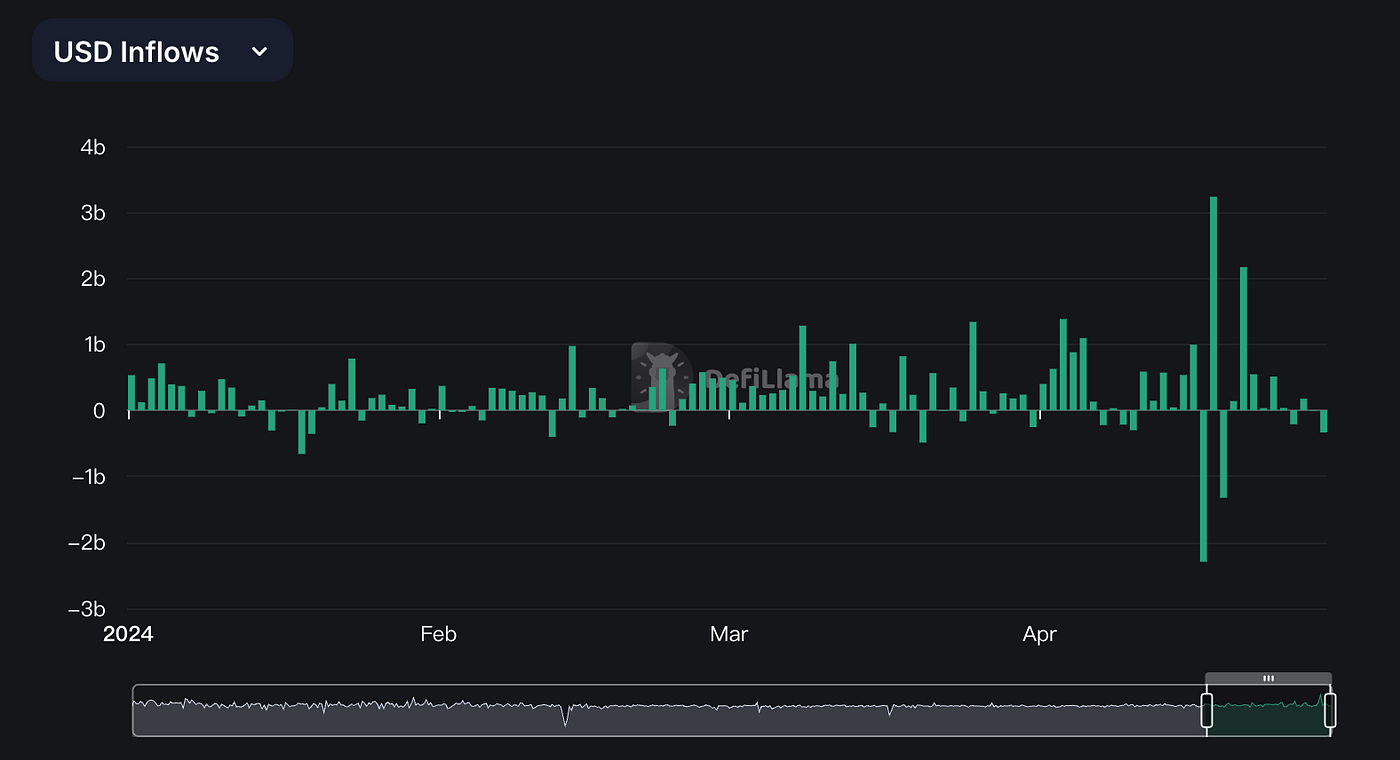

In terms of USD inflow, the growth trend is the same as that of the overall stablecoins, with the highest single-day net inflow of $3.24B on April 18. Among them, from April 17 to 21, the changes in inflow and outflow were extremely obvious. This period was just before and after the four halvings of BTC, which indirectly reflected the turnover and game of long and short forces in the market, but the amount and frequency of net outflows were still lower than net inflows. In addition, from the news perspective, the continuous outflow of US BTC spot ETFs is having a correlated impact on USD inflows, and the direction and strength of USD flows may reverse.

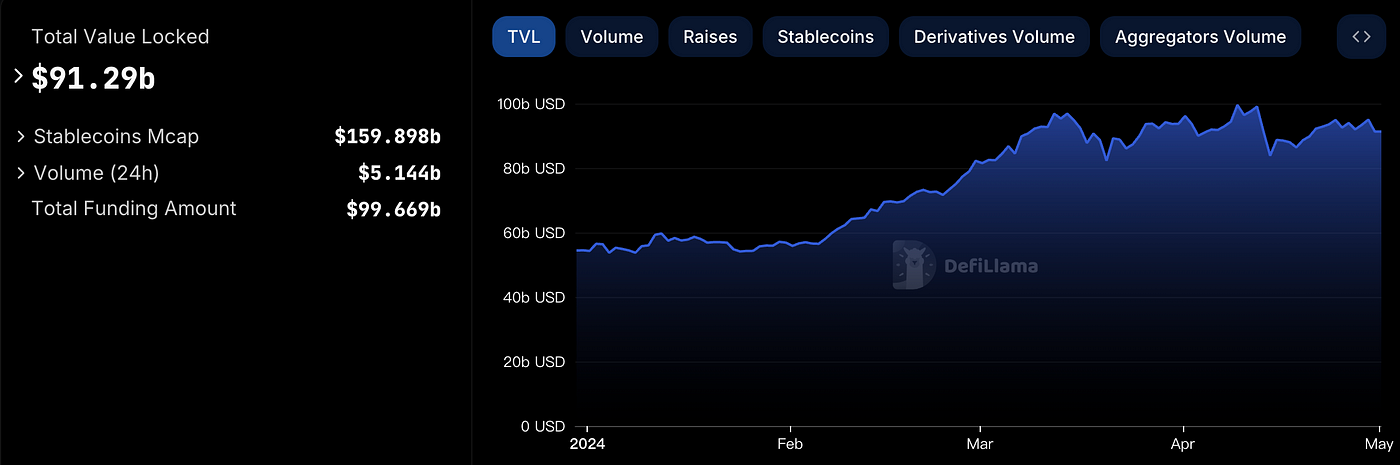

2.3 On-chain TVL ranking

The overall TVL on the chain fluctuated significantly in April, especially from April 12 to 14, when it dropped sharply, then began to rise slowly, and began to recover slowly in the third week, but the oscillation trend was obvious and the recovery was insufficient. Under the current volatile market, the on-chain activity has dropped significantly compared with last month, and the development of various ecosystems has also been affected. It is expected that the trend of on-chain TVL in May will be strongly correlated with the market trend, but the growth trend of the currency standard will slowly rise with the development of the ecosystem.

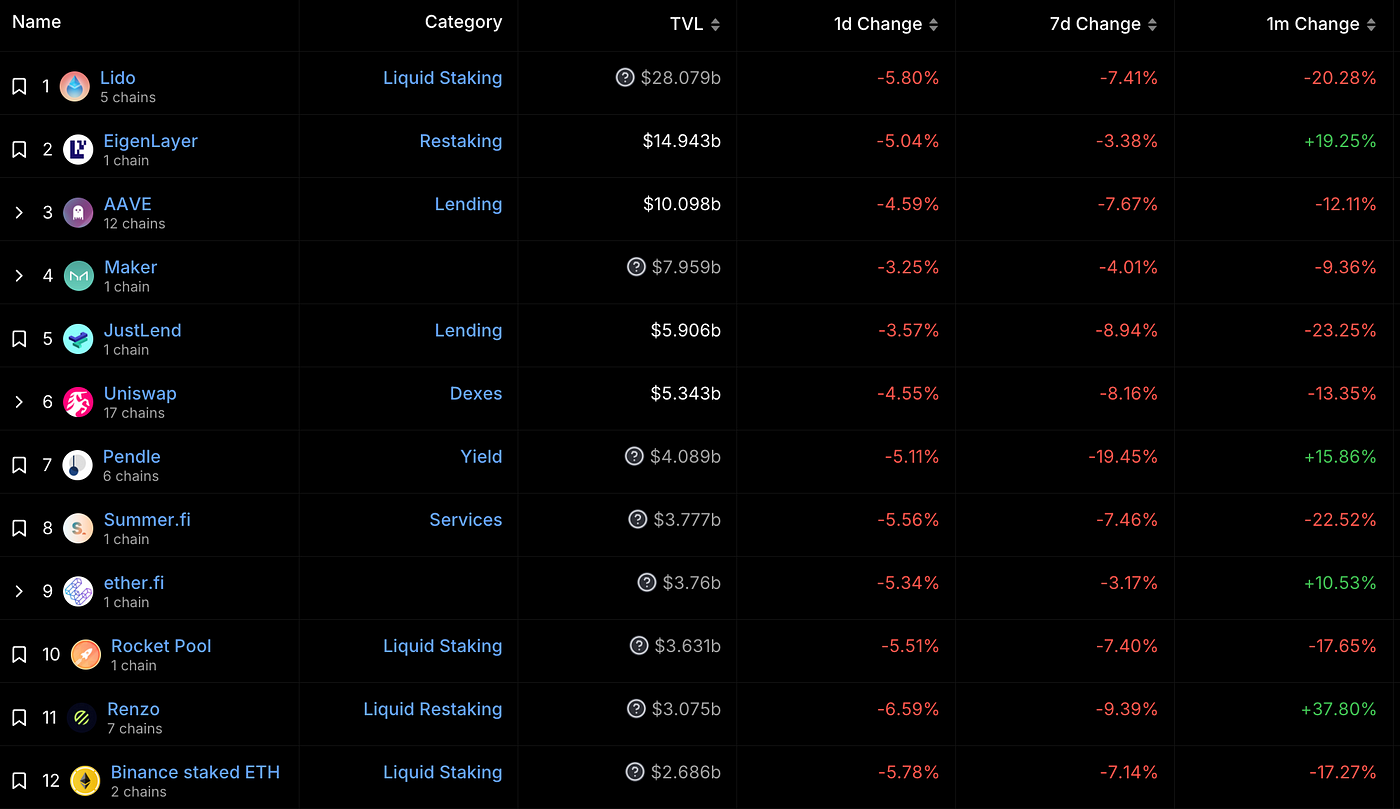

The most watched project this month is Renzo. Although the price of ezETH decoupled from the market due to community doubts about its token model, its TVL growth rate still ranks first (37.8%), leading other projects in the top 10 TVL rankings and far exceeding EigenLayer's 19.25% growth. In addition, EigenLayer's growth has begun to stabilize, and large-scale pledge withdrawals have begun to occur, and subsequent performance needs to be paid close attention to.

DeFiLlama data: As of April 30, the TVL of ETH liquidity re-staking protocols reached $26.91 billion, of which EigenLayer ranked first with a TVL of nearly $15 billion; followed by ether.fi, with a TVL of more than $3.7 billion; and Renzo, with a TVL of more than $3 billion.

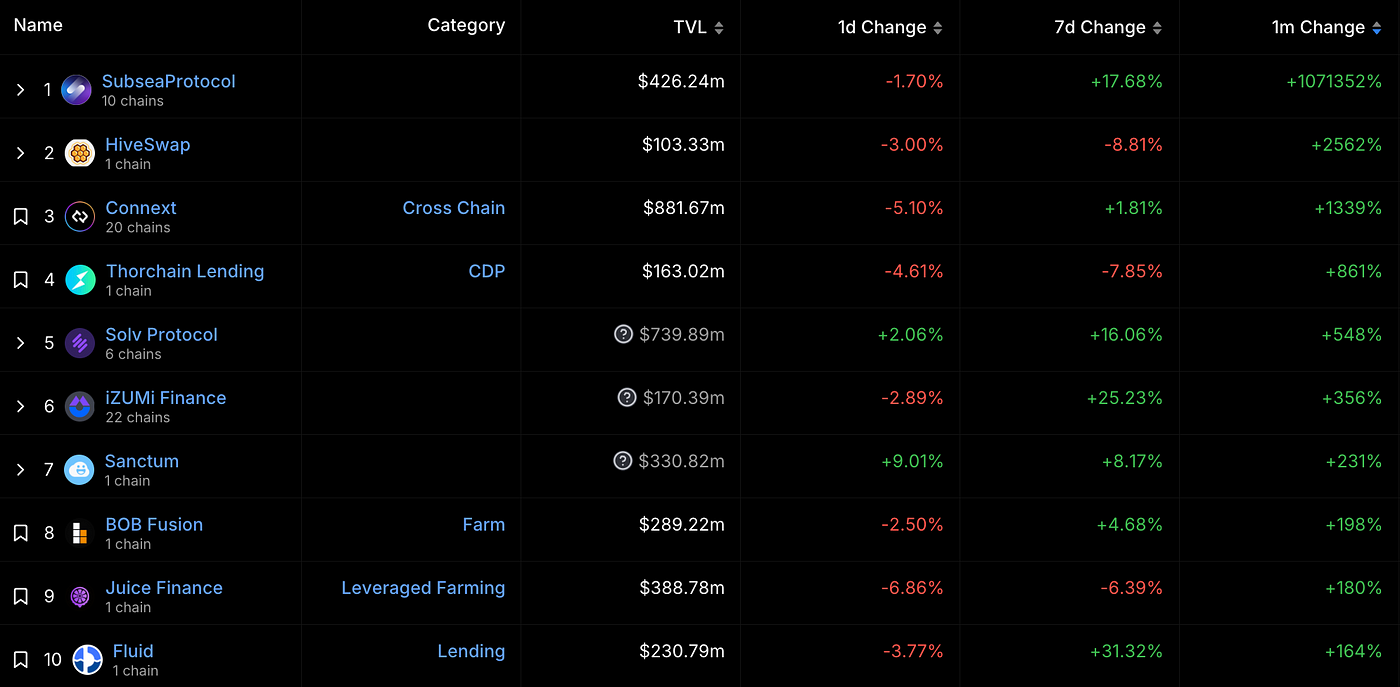

Among the 138 projects with TVL above $100 million (142 last month), the project with the largest TVL increase this month is Subsea Protocol (+1,071,352%), and HiveSwap (+2,562%) and Connext (+1,339%) ranked second and third. Subsea Protocol's TVL suddenly exploded on April 8. Currently, no action has been seen from the public information. It may be abnormal data, and we are paying attention and tracking it.

Subsea is a risk management marketplace for digital assets that pioneers a fully automated, transparent and impartial immutable detection mechanism to protect users from digital asset risks, hacks and attacks.

Hiveswap is a SWAP in the BTC ecosystem that uses the interoperable Bitcoin layer MAP protocol to provide liquidity services for assets in the Bitcoin ecosystem, including assets on BTC L1, MAP protocol interoperability layer, and various Bitcoin L2 assets.

Connext is a trust-minimized cross-chain communication protocol that makes blockchains composable. Developers can use Connext to build cross-chain applications. Connext is the leading protocol for fast, fully non-custodial transfers and contract calls between EVM-compatible chains. Anyone can use Connext to send value transactions or call data across chains and aggregate.

By DeFi category, among the TOP10 tracks with total TVL this month, LSD still ranks first with $45.329 billion, a significant decrease from last month ($51.44 billion). Considering the overall downward trend of the market, the scale of the gold standard has actually shrunk, but the total amount is still growing.

In addition, among other tracks, only Restaking and RWA have positive growth, especially the Restaking track, which has grown by about $3.5 billion. This shows that the market is entering a cooling-off period at this stage. People do not have a clearer investment direction except for Restaking, which also indirectly shows that people have further recognized Restaking. However, Restaking is an emerging product with relatively large unknown risks, and more users are cautious about it.

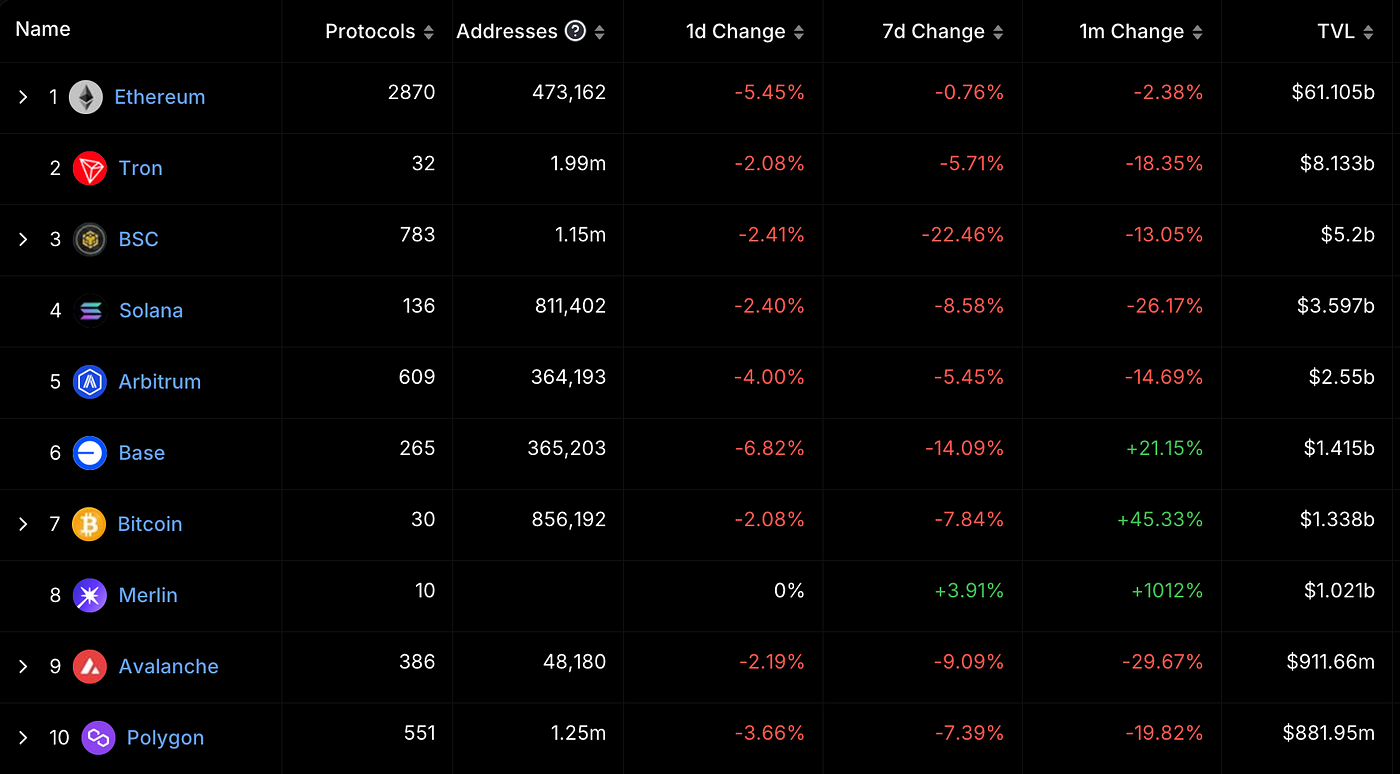

By chain category, the TVL growth of the BTC ecosystem was the most impressive in April, with Merlin's TVL growing by 1012% and Btcoin's TVL growing by 45.33%, followed by Base's 21.15% (up 116% last month). The remaining public chains all showed negative growth (Solana's growth also failed to maintain).

Under the current market conditions, Merlin's high growth and Bitcoin's continued growth are mainly due to the market's attention and investment in the BTC ecosystem, especially L2, after BTC's four halvings. With the implementation of more projects, the BTC ecosystem is beginning to become active. If the market conditions and market enthusiasm do not improve significantly in May, it is expected that the performance of the BTC ecosystem will still be higher than that of other public chains, and the growth of Base will be further weakened.

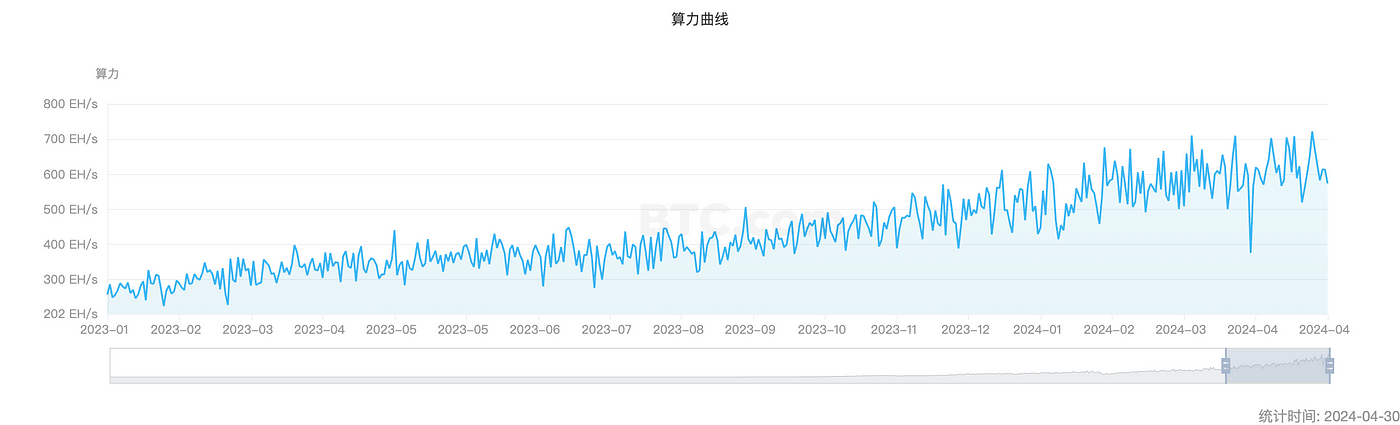

2.4 Mining Pool Data

BTC:

At present, the total POW computing power of the entire network has reached 617.86 EH/s, an increase of about 3.52% from the previous month (596.81 EH/s), and a slight decrease from the previous month (3.78%) but not obvious. With the four halvings of BTC, the income of miners per TH/s computing power has dropped by about 50% after 10 days, which is consistent with the output after the halving.

The obvious decline in miners' income has led to a corresponding reduction in the daily inflow of BTC into the market. The drop in BTC prices may drive more BTC in the hands of miners into the market. Once BTC reaches the shutdown price of some small and medium-sized miners (unable to bear the cost pressure), they may withdraw in batches, triggering a chain reaction in the market and even a new round of local reshuffle.

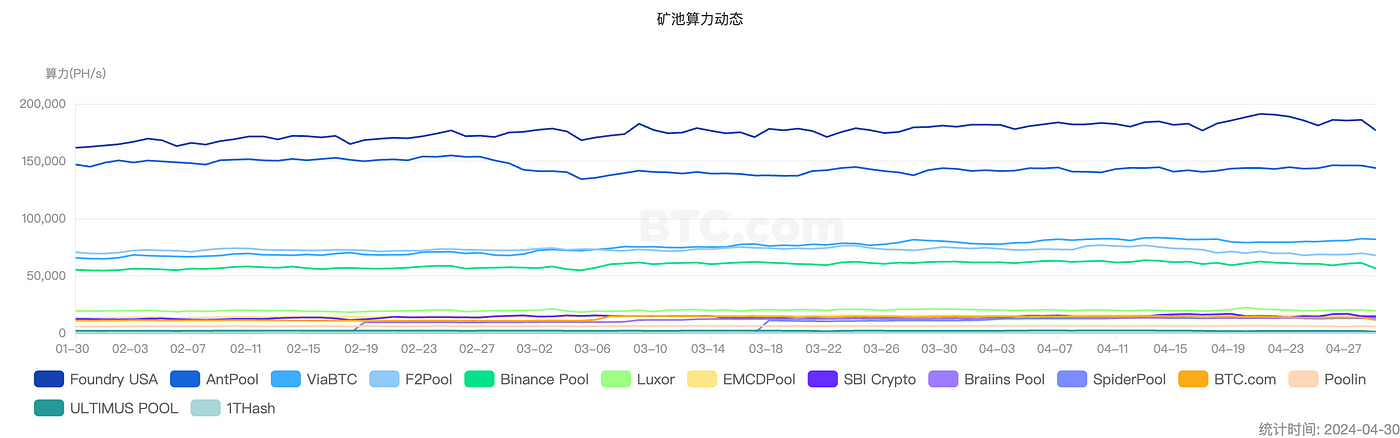

Among them, the top three mining pools are still Foundry USA, AntPool and ViaBTC, while F2Pool has dropped to fourth place, about 140 EH/s less than ViaBTC. In terms of growth rate, Foundry USA is still the most stable.

ETH:

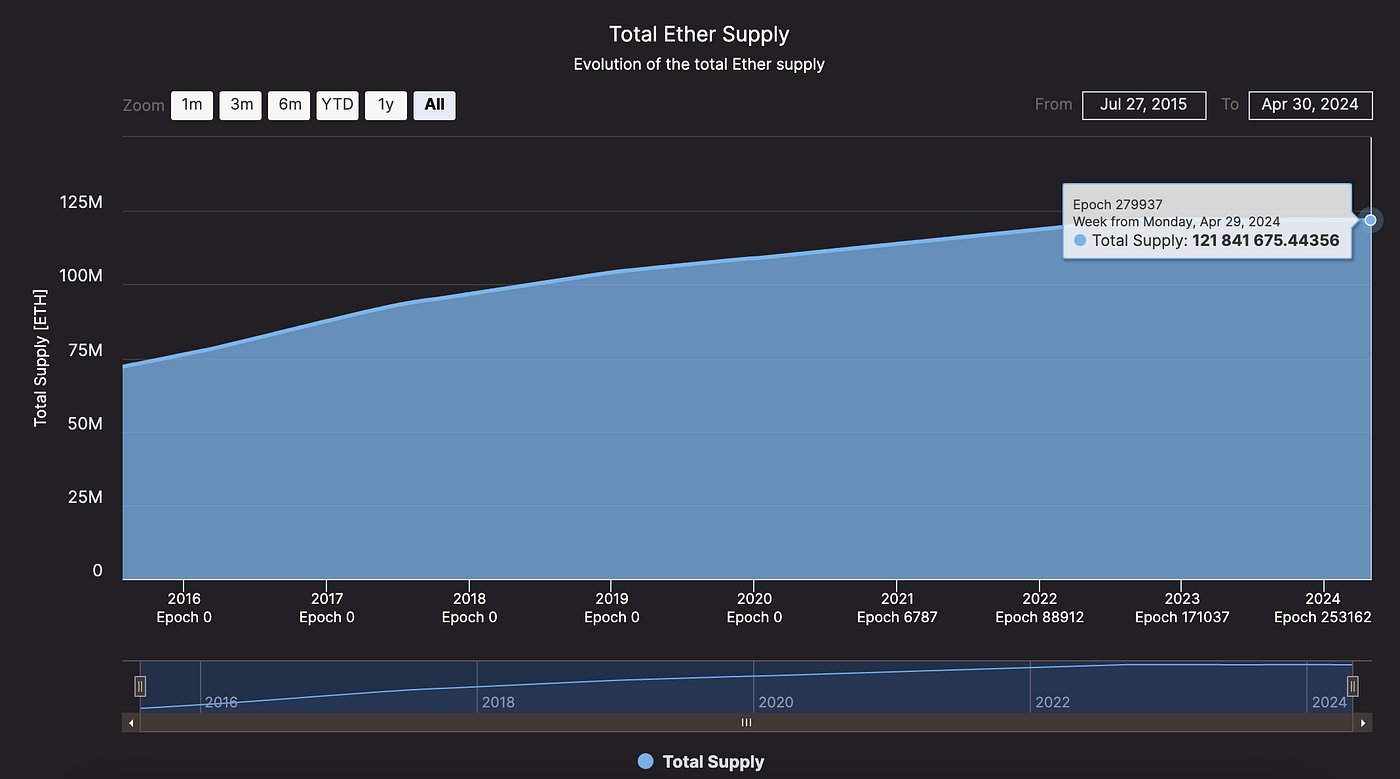

The supply trend of ETH remains flat, with no significant fluctuations since June 2022, and has basically remained around 122 million. This shows that the POS mechanism has indeed played a very positive role in stabilizing the ETH ecosystem, and ETH's market value is strongly correlated with its ecological value.

We see that ETH, as the largest ecosystem in the industry today, is focusing on the construction and expansion of its internal ecosystem and promoting the entire industry's continuous exploration of underlying facilities and services. This steady and progressive trend allows its potential to continue to accumulate, waiting for new opportunities to emerge.

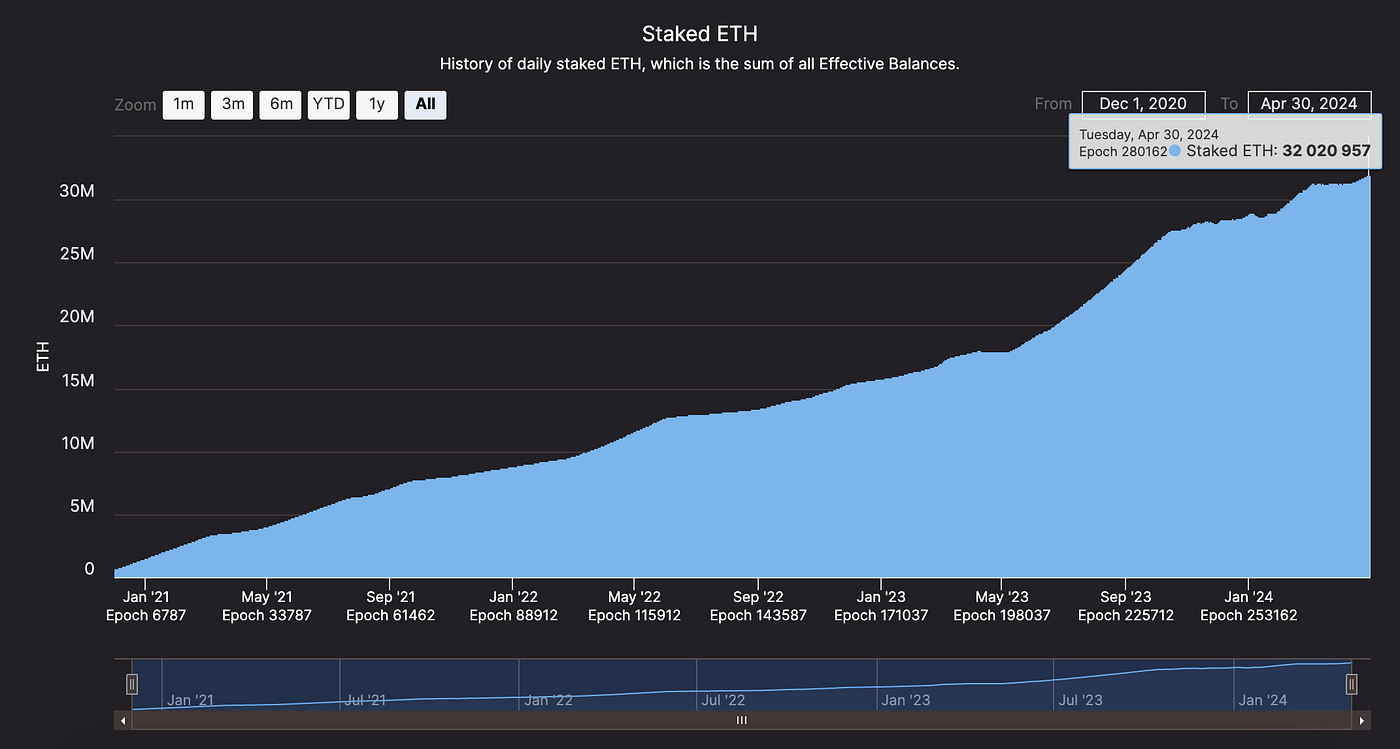

At the same time, the total number of ETH POS staked continued to rise. As of April 30, there were 1,000,766 active validators, and 32,024,157 ETH staked in the entire network, accounting for 26.28% of the total ETH supply. Among them, 692.898 new stakes were staked in April, and the stake share of the liquid staking protocol Lido accounted for 29.15% of the total, down from 30.11% last month.

On April 27, Lido tweeted that the SSV Simple DVT testnet has ended and the mainnet will be launched soon. In the next few weeks, selected participants will use SSV technology to join the mainnet Lido Simple DVT module. Although this will not make Lido's absolute share more decentralized, it will further ensure the security of stakers and allow more service providers to participate.

3. Market trends

3.1 BTC price fluctuates downward

https://www.binance.com/en/trade/BTC_USDT?_from=markets&type=spot

After experiencing a 16.6% increase in March, the BTC price began to pull back in April and showed a fluctuating downward trend. According to Binance data, as of 11:00 (UTC+8) on April 30, the highest price of BTC in April was $72,797.99 and the lowest price was $59,600.01, with a price drop of 10.51% in 30 days.

Regarding the BTC's volatile downward trend this month, the mainstream market view is that there are three possible reasons:

- Profit-taking and selling pressure after BTC price hit a new high. Binance trading data shows that BTC price hit a record high on March 14, 2024, reaching US$73,777 per coin. Considering that BTC has achieved its interim goal, many investors in the market have taken profits, resulting in a price drop.

- The conflict between Iran and Israel has caused panic in the crypto market. On April 13, local time, Iran used drones to attack Israel, which directly affected the trend of BTC prices. Binance trading data showed that on April 13, the price of Bitcoin fell, with the lowest price of $60,660.57. The uncertainty of regional conflicts has exacerbated the downward trend of crypto assets including Bitcoin.

- The net outflow of BTC spot ETF also affected the trend of BTC price. According to sosovalue data, from April 1 to April 26, BTC spot ETF had a net outflow of US$83.61 million, which also triggered a downward trend in BTC price.

As for BTC price: Since September 1, 2023, Bitcoin has been on a 7-day winning streak. Among them, the increase in February 2024 was about 43.57%, and the increase in March was about 16.6%;

In April, the biggest nodal event was the fourth Bitcoin halving. Based on the historical experience of BTC’s pullback before and after the halving, the overall decline of BTC by 10.51% this month was within expectations.

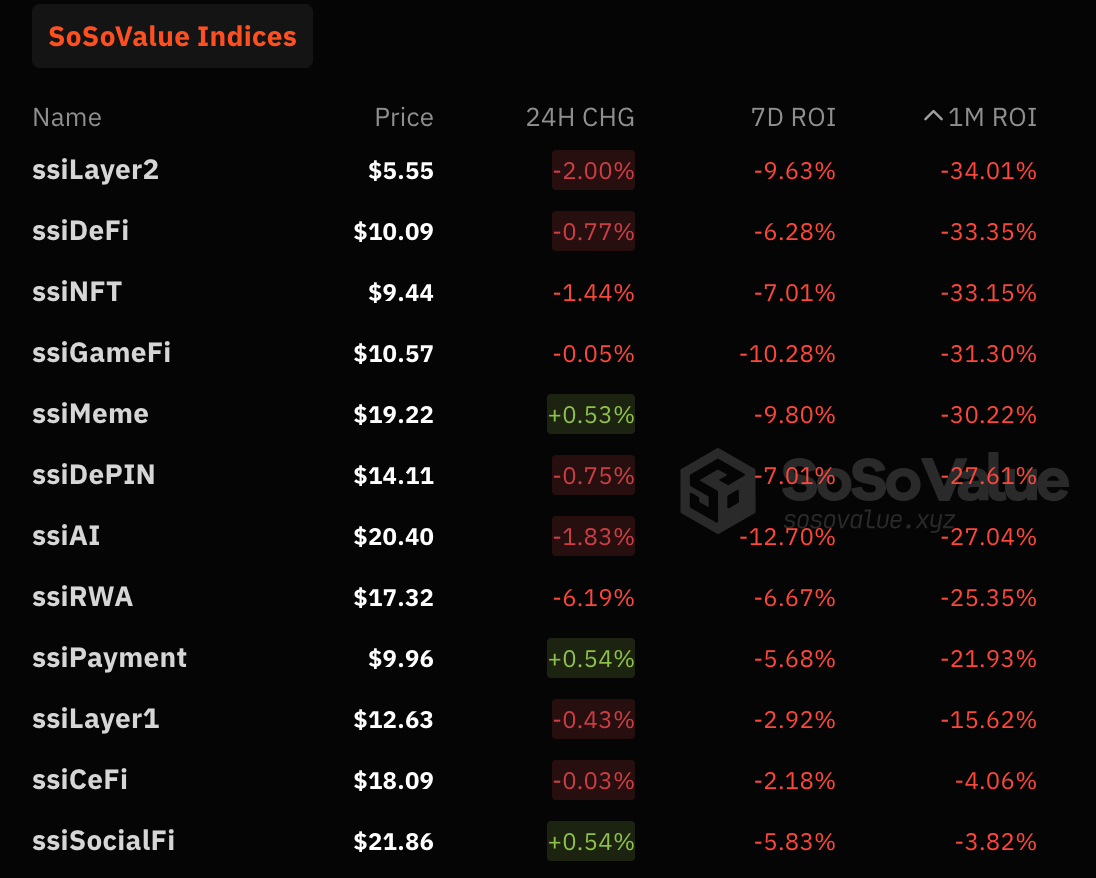

3.2 All sectors fell sharply

https://sosovalue.xyz/assets/cryptoIndex

As BTC prices fluctuated downward, other sectors in the crypto industry also showed signs of a general decline. According to sosovalue tracking data, Layer2, Defi, NFT, and Gamefi sectors saw the largest declines in ROI.

In addition to the above four sectors, the recently popular MemeCoin sector and AI sector have also seen a sharp correction:

- MemeCoin’s Doge fell 32.71% in 30 days, and Shib fell 21.25% in 30 days (CoinMarketCap data);

- In the AI sector, except for Near Protocol, representative projects such as RNDR, TAO, and GRT all experienced a drop of more than 20%;

Considering the general rise in the previous crypto assets and the BTC halving that caused many floating chips to take profits, the current downward volatility and the general decline in other sectors are most likely normal market adjustments.

4. Investment and Financing Observation

4.1 Investment and Financing Overview

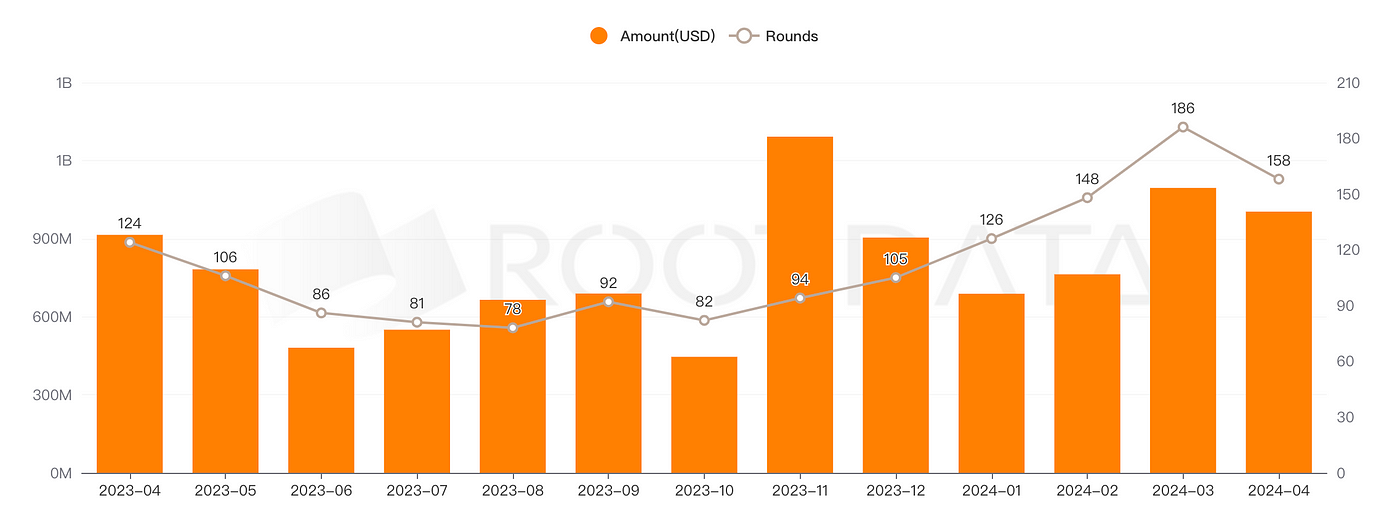

In April 2024, the total amount of the crypto market was US$1.004 billion, a decrease of 7.55% from the previous month. The public data is as follows:

- 158 financing events, a decrease of 12.15% month-on-month;

- 4 acquisitions, up 33.33% from the previous month;

- The average financing amount was US$8.8092 million, down 8.37% from the previous month.

- The median funding amount was $3.35 million, down 33% from the previous quarter.

Seed round financing events are still the most, followed by strategic financing and other types of financing. Pre-seed round financing events are growing rapidly:

- 44 sub-wheels started (-6.3% compared with the previous month);

- 15 strategic financings (-50% compared to the previous month);

- 0 in round A (-100% compared to last month);

- Pre-seed rounds started from 12 (+120% compared to the previous month);

- 13 cases of other types (up 23.5% from the previous month);

Although acquisition events have increased, financing events, average financing amount and median financing have all dropped significantly. The market is negative in the short term and the influx of hot money has slowed down. This shows that the market trend in April had a significant impact on investment and financing. Investment institutions began to be cautious and slowed down their progress, but acquisitions and mergers are becoming a trend in track competition. In the future, the competitive situation at the top of the track will become clearer.

Although acquisition events have increased, financing events, average financing amount and median financing have all dropped significantly. The market is negative in the short term and the influx of hot money has slowed down.

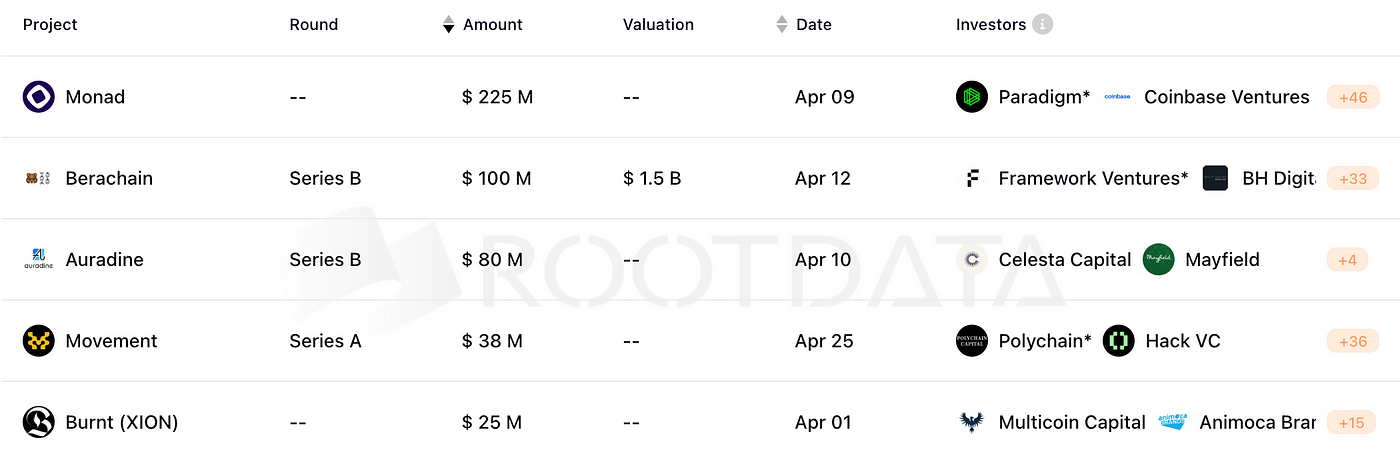

The five largest financing rounds in April:

Monad completes $225 million financing, valuation not disclosed;

Berachain completed a $100 million Series B financing round with a valuation of $1.5 billion;

Auradine completed $80 million in Series B financing, with an undisclosed valuation;

Movement completed a $38 million Series A financing, with an undisclosed valuation;

Burnt (XION) completed a $25 million financing round at an undisclosed valuation.

4.2 Brief Analysis of Investment and Financing Institutions

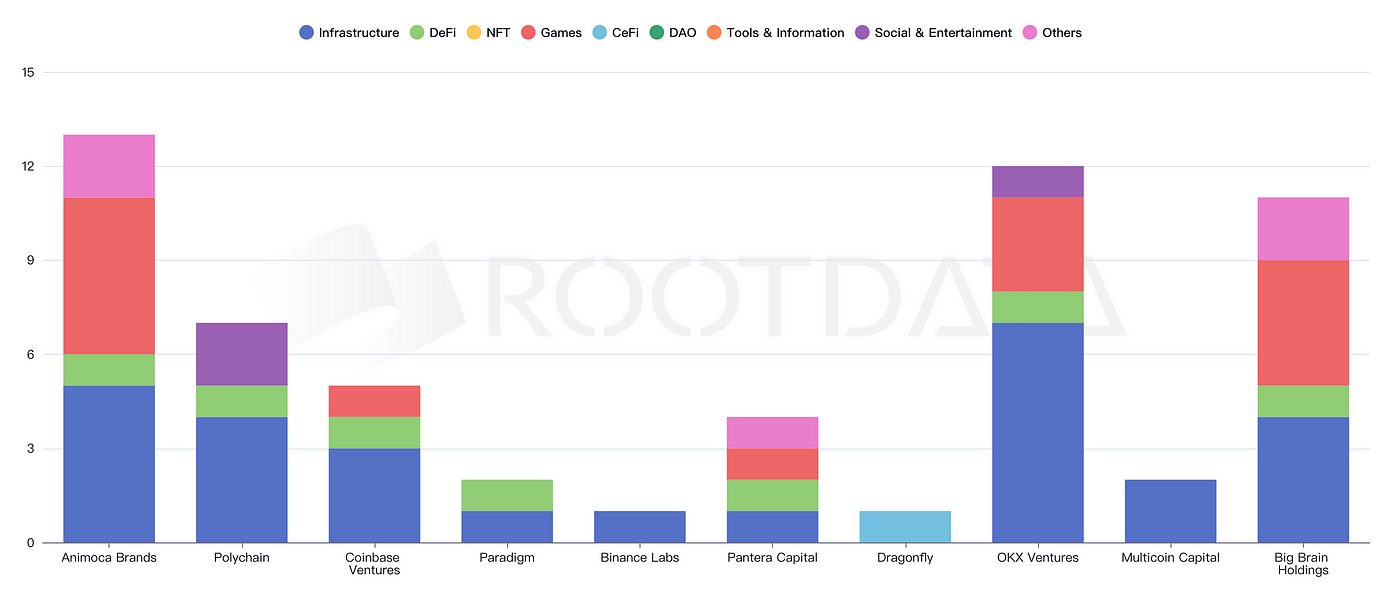

From the perspective of VC institutions: Animoca Brands has made the most investments in the GameFi field, followed by OKX, Big Brain and Polychain. These three have made large investments in infrastructure and GameFi, while other VC companies focus on infrastructure and DeFi.

This reflects the distribution and pattern of industry construction and application at this stage. Infrastructure is still the current focus of construction, and GameFi's share in the application side is becoming increasingly important. The market is focusing on GameFi as a new application after DeFi, and investors are advised to pay close attention.

4.3 Judgment of investment and financing trends

As the block reward decreases after the Bitcoin halving, miners' income and computing power face greater downward pressure. In addition, the expectation of the Federal Reserve's only interest rate cut this year has spread across the market, making VC institutions and TradFi funds more cautious. It is expected that investment institutions in May will be more cautious in their layout.

However, when the market is fearful, it is often necessary to be "greedy" and move forward, which is the best investment opportunity to find undervalued assets. With the continuous innovation and development of Bitcoin ecology, AI long-term narrative, GameFi chain games, and parallel EVM, it is expected that the investment and financing market will be stable and progressive in May, and will continue to focus on infrastructure and GameFi. Combined with the current on-chain data, the BTC ecology will perform better.

About Movement

At the end of April, modular blockchain Movement announced the completion of a $38 million Series A financing, becoming the fourth largest financing project in April. The financing was led by Polychain Capital, with participation from Hack VC, Foresight Ventures, Placeholder, Archetype, Maven 11, Robot Ventures, Figment Capital, Nomad Capital, Bankless Ventures, OKX Ventures, dao5 and Aptos Labs. The funds will support Movement to introduce Facebook's Move virtual machine into Ethereum to solve smart contract vulnerabilities and increase transaction throughput.

Movement is a modular framework that can be used to build and deploy Move-based infrastructure, applications, and blockchains in any distributed environment. The framework is compatible with Solidity, connects EVM and Move liquidity, and allows builders to customize modular and interoperable application chains with different user bases and liquidity out of the box.

5 Conclusion

The data and market dynamics in April 2024 show us several important trends:

- The expectation of US interest rate cut has been postponed, and the crypto market has fallen after reaching a new high, but the amplitude is still within the expected range, and a rebound in the future market is still expected;

- After the BTC halving, as the popularity of Runes faded, miners and mining companies began to take active actions to expand their business portfolios and revenue portfolios;

- The growth of stablecoins has begun to slow down, but this has not affected whale transactions. The increase in whale holdings has given people more expectations about the market trend.

- The on-chain TVL is declining with the market, but the Restaking and BTC ecosystems are still growing. This trend is expected to continue in June.

- Pre-seed round investment and financing events have grown rapidly, with GameFi accounting for a prominent share. This shows that although VC layout is affected by the market, it is still making steady progress.

Although the market is still fluctuating downward and the volatility is obvious, the main line of the market is still traditional capital and ETF. Under the trend of a sharp decline in all sectors, Restaking and BTC ecology have performed particularly well, showing strong ability to buck the market trend and potential for the future market. Once the market adjustment is completed and it starts to rebound upward, Restaking and BTC ecology may become the core narrative of this cycle.

In addition, the modularization and GameFi sectors have begun to show strong momentum in terms of investment, financing and implementation progress, especially GmeFi's dominant share in investment and financing projects, and Avail's upcoming mainnet launch, making them likely to become key variables affecting the industry and market conditions. Let us continue to pay close attention.

Note: All the above opinions are for reference only and are not investment advice. If you disagree, please contact us for correction.

Follow and join the MIIX Captial community to learn more cutting-edge information:

Twitter CN: https://twitter.com/MIIXCapital_CN ;

Telegram CN: https://t.me/MIIXCapitalcn ;Join the MIIX Capital team: [email protected] :

Recruiting positions: Investment Research Analyst/Operations Manager/Visual Designer.