Let's talk about Lido's buyback.

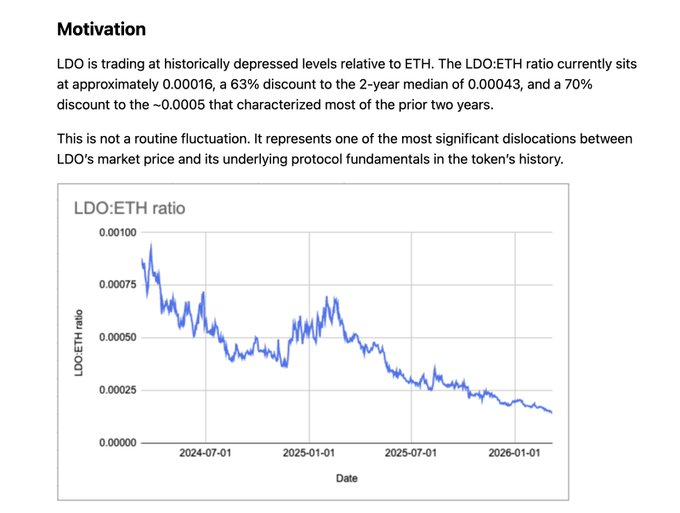

Recently, Lido proposed using 10,000 stETH to buy back $LDO. The motivation is simple and direct: they believe LDO is oversold against ETH, and they provided some data.

Currently, the LDO:ETH exchange rate is approximately 0.00016, about 63% lower than the median of 0.00043 over the past two years, while protocol revenue has only decreased by about 20%. From the LDO price perspective, it's basically close to its historical low.

The market capitalization is also similar; at its peak, it was $3 billion, and now it's around $300 million.

Interestingly, Lido's business remains stable and simple, earning approximately $50-60 million annually. However, it shares a portion with operators, so even halving that, it still generates $20-30 million.

From this perspective, it's quite inexpensive. The only question is whether the staking business is on the rise or on the fall. Frankly, pure staking is a declining business because the barrier to entry is getting lower and lower, and solo staking is gradually being encouraged.

So, does Lido have a chance to rise? Yes, it does. V3 has modularized its staking service, allowing direct integration with institutional needs. Most importantly, it allows Lido to inherit stETH's liquidity, which is currently Lido's biggest competitive advantage. If institutional staking requires on-chain circulation of LSD, Lido is a good choice.