Author: Fu Peng, Chief Economist of Northeast Securities

Introduction

Eventually, the logic of the gold mining town began to fail, and the problems of the core assets began to be exposed. All the trading chains that originally relied on this core with low volatility, high leverage, and even negligible carry costs began to liquidate. Nvidia's opening decline meant that the arbitrage asset side began to shrink, and the logic of intermediate cost hedging also began to reverse (choosing to hold Japanese yen assets and sell Japanese yen), and the entire liability side (borrowing Japanese yen) also began to shrink. At this time, the Bank of Japan could use a small amount of force to make the exchange rate return to the interest rate differential relationship.

To understand the global market, you must understand the carry trade

Carry trading is already a well-known capital operation method in the market. By selecting appropriate liability and asset objects, using low volatility characteristics to ensure transaction stability, and using interest rate spread trading to maximize profits, some traders can also add a certain amount of leverage on this basis. Of course, without considering leverage, asset volatility, asset potential returns and capital hedging costs are the key factors in measuring carry lending investment behavior.

By participating in such transactions, we can reveal the logic of global capital flows. Although capital should flow freely around the world in an ideal state, considering the political and geopolitical factors in reality, there are obstacles and various friction costs to the free flow of capital. After 2016, the role of many things has undergone a major reversal between assets and liabilities. The change in the global division of labor has led to a shift in the relationship of capital flows, especially the trend of deglobalization has had a significant impact on the international flow of capital.

The actual combination of carry trade in the past two years

After the epidemic, the interest rate level of the US dollar has increased significantly, and US dollar borrowing has also had a significant impact on global capital flows. First of all, although the US dollar is still the main borrowing currency, due to the significant increase in costs, it is necessary to match certainty, high leverage, low volatility, and ultimately high-return assets (low interest rates on the US dollar will promote uncertainty, high leverage, high volatility, and high investment return assets, such as Cathie Wood's investment strategy), so you will find that high-interest US dollars can still be used to allocate assets, but they will no longer be used for assets like Cathie Wood, while Nvidia and others have become assets that meet certainty, high leverage, low volatility, and ultimately generate high returns;

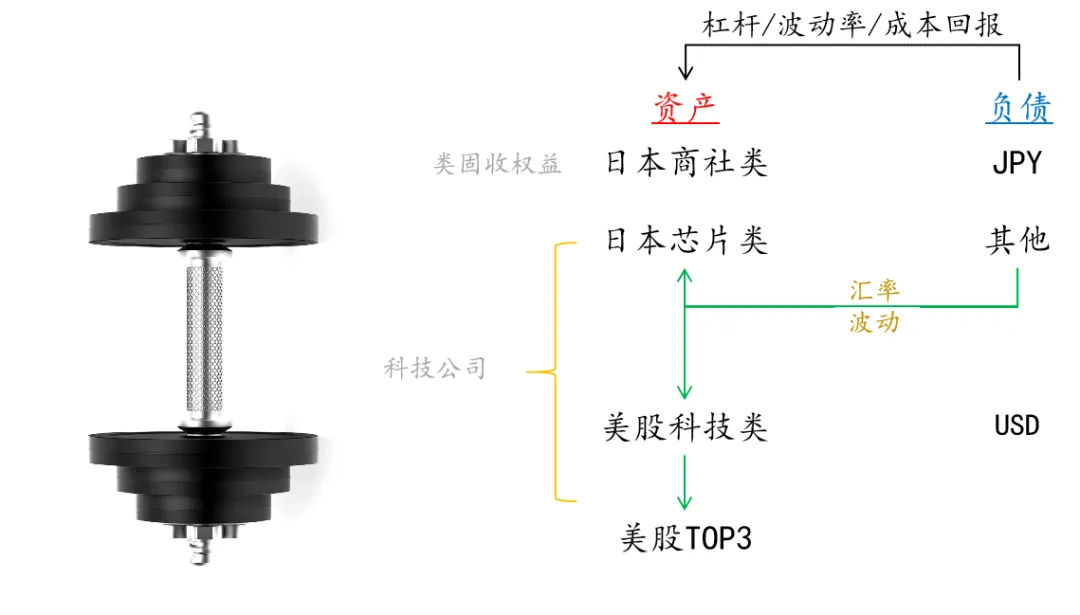

Figure: Dumbbell on the asset side of the global carry trade

Source: Fu Peng's Financial World

Secondly, as an ally of the US dollar, the Japanese yen also plays an important role on the liability side. Due to the long-term low interest rate policy, the Japanese yen has been used as a carry currency. In the past 30 years, borrowing Japanese yen has been invested in markets other than Japan. Due to the deep-seated problems behind Japan's domestic economy, investing in Japanese assets with borrowed Japanese yen is not feasible.

However, with the completion of Japan's natural cycle (internal allocation) and the redivision of labor in the international field, yen assets invested in yen have become increasingly popular in recent years. At a more micro level, the corporate governance reforms in the Japanese stock market have further brought about the demand for allocation of two types of assets within the Japanese stock market. One is that large trading companies have become stable and high-interest cash cows due to governance adjustments; the other is that Japanese technology stocks have become growth assets due to the redivision of labor in artificial intelligence and globalization in the United States.

The carry funds of Japanese yen loans mainly flow to these two types of assets in Japan, and Buffett's transaction of borrowing Japanese yen to buy Japanese trading companies is a typical case of the most certain arbitrage transaction, which completely hedges the risk/return of the Japanese yen exchange rate and focuses on the stable cash cows of large Japanese trading companies.

The other category of assets is the other end of the dumbbell - Japanese technology stocks, especially those represented by JEC. In fact, not only JEC, but also TSMC and others are actually a shadow of this round of American AI. However, these companies are all in the outer circle, while the core asset is the core of the core - Nvidia.

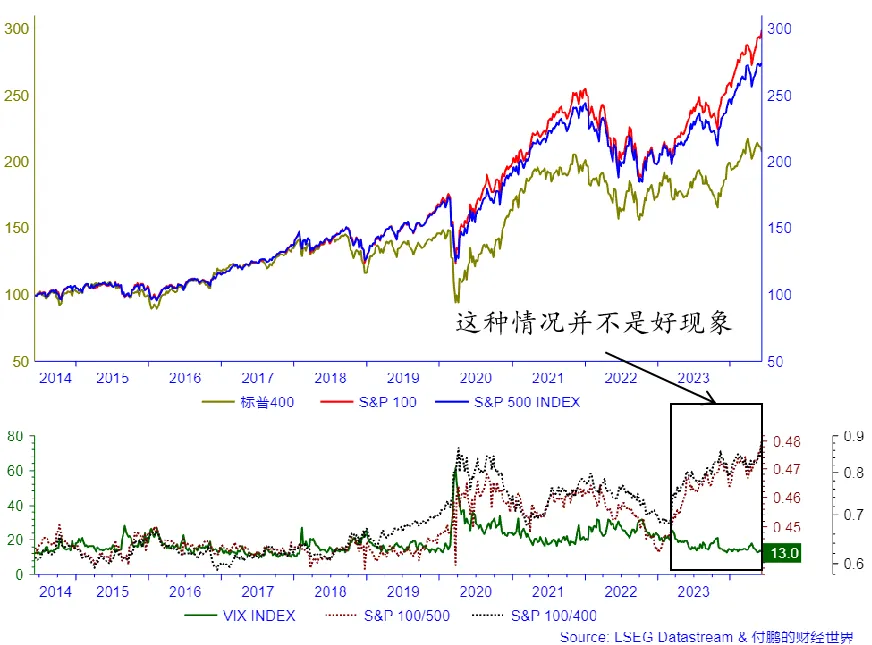

Just like everyone observes the shrinking circle of the US stock market, the price ratio of the top 100 and the bottom 400 in the S&P 500, then the top three companies and the bottom 97, and then the leader Nvidia among these three, market funds are increasingly concentrated in the top companies, and behind this phenomenon is the record low volatility of the S&P. In the previous diary, I emphasized the size of Nvidia's external options market. At this point, you will find that the three elements of low volatility, leverage, and return are all gathered together, and the climax will soon come;

If we expand this shrinking process to integrate these two types of Japanese assets, you will see that Japan, as the most peripheral asset, has actually been swept down in the shrinking circle at the end of April this year. In fact, I have also said that you can regard Japan's chip companies as the shadow of a "little brother" of US technology companies, and at this time the yen exchange rate has become an important hedging tool;

At the end of April this year, the shrinking circle, Japanese chip stocks denominated in yen (such as JEOL) were unable to keep up with the pace led by Nvidia, just like other companies in the U.S. stock market. Funds were increasingly siphoned by Nvidia's leading companies. At this time, traders could choose to sell Japanese electronics (sell yen assets), but the risk of increasing concentration of leading companies, and considering the factors such as the second wave of industrial diffusion in the later stage, another option is to maintain such a carry portfolio, but use the sale of yen to replace the sale of yen assets, that is, continue to hold yen assets, but sell yen, so that this part of Japanese chip assets denominated in US dollars can still not cause a large loss in the investment portfolio. Of course, there will inevitably be a batch of funds borrowed in yen that will further flow into the leading U.S. technology companies;

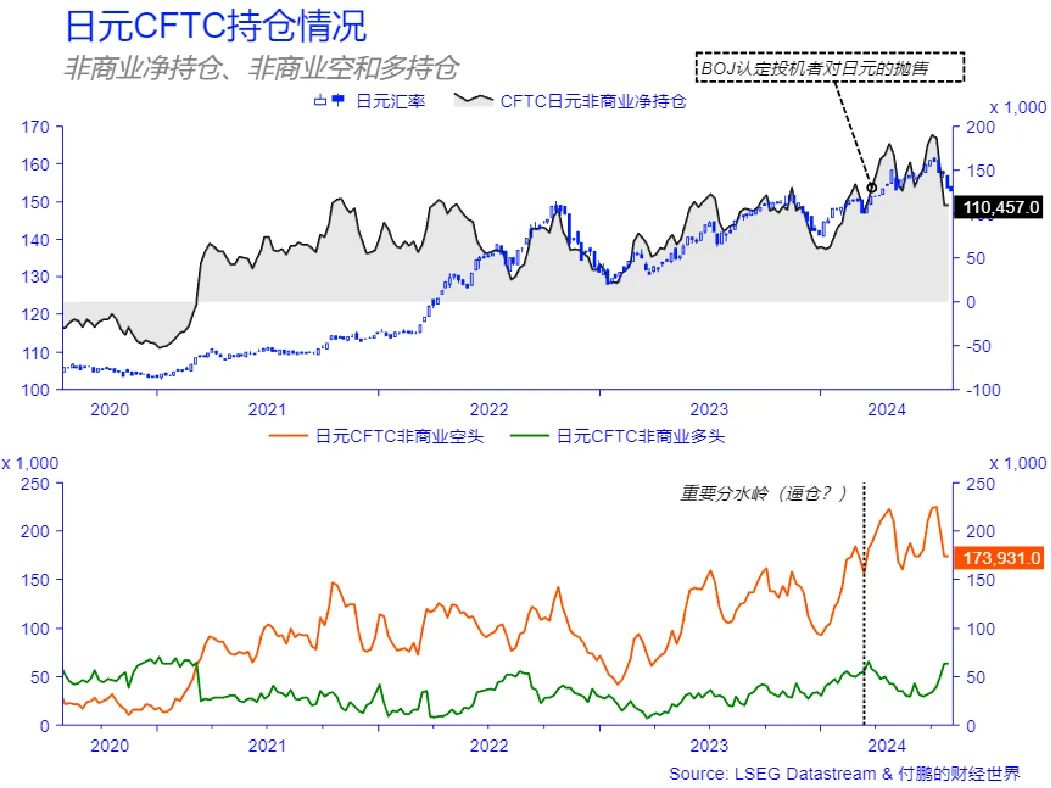

At this stage, we will see that exchange rate fluctuations (yen selling) are excessive speculative selling from the perspective of BOJ, and in the Carry portfolio, it becomes a hedge of holding yen assets. At this time, the exchange rate and the interest rate spread in the traditional liability logic begin to decouple. The loss of this part of the asset side is hedged with the income from exchange rate fluctuations, but it becomes the opponent of the Bank of Japan. If Nvidia continues to advance rapidly, the asset side will become more favorable. Even considering the risks and costs of exchange rate hedging, the expected return on investment will attract more arbitrageurs. Therefore, although the first intervention of the Bank of Japan did indeed eliminate some speculative yen shorts from the CFTC data, the Bank of Japan continued to lose bullets in the context of no changes in the entire asset side;

Eventually, the logic of the gold mining town began to fail, and the problems of the core assets began to be exposed. All the trading chains that originally relied on this core with low volatility, high leverage, and even negligible carry costs began to be liquidated. Nvidia's opening decline meant that the arbitrage asset side began to shrink, and the logic of intermediate cost hedging also began to reverse (choose to hold Japanese yen assets and sell Japanese yen), and the entire liability side (borrowing Japanese yen) also began to shrink. At this time, the Bank of Japan can make the exchange rate return to the interest rate differential relationship with little effort;

As the interest rate differential between the Bank of Japan and the United States is still as high as 4%, the exchange rate is bound to be constrained by the interest rate differential relationship (yen center 153). These chip assets in Japanese currency are actually just shadows of the U.S. stock market's artificial intelligence technology sector. Therefore, core Nvidia has become an important anchor point for the entire yen carry trade.

In this context, the Japanese yen is relatively stable as a liability, and the interest rate differential between the US and Japan is relatively fixed. If Japanese technology assets can provide low volatility and high returns, they can be used as hedging tools with the exchange rate, allowing borrowers to obtain stable returns even in exchange rate fluctuations. However, when asset-side arbitrage becomes more favorable and the return on investment is higher, exchange rate fluctuations will become a hedging tool and break the interest rate differential relationship.

In general, the allocation of yen arbitrage funds is reflected in the (exchange rate) looking down at liabilities (interest rate spreads) and looking up at asset expectations. Below 153, it returns to interest rate spreads, and above 153, it depends on whether the asset side can provide higher investment return expectations and whether the yen hedging can be calculated as a cost and still be cost-effective.

RMB from carry asset to carry liability

The RMB has also unknowingly become part of the new global carry trade. For my country, there are certain problems of overcapacity and insufficient effective aggregate demand. The compression of the real estate market may further lead to an imbalance between supply and demand. This has prompted the supply side to turn to overseas markets through exports or enterprises going overseas, which has promoted the increase of China's exports and trade surplus. However, in the foreseeable future, this trade behavior may have an impact on overseas markets and trigger trade conflicts again.

As for the funds in China, their investment income is expected to drop significantly. Although a large number of surplus assets have been accumulated through exports, due to the low gross profit margin and the reliance on scale, the profits earned by these funds may not be returned to the RMB, resulting in a large amount of unsettled foreign exchange sales funds. These funds may be held in large quantities of US dollars through the banking system, or directly intercepted overseas through trade. This further highlights the problem of meager profits in the domestic production link, and the profits intercepted overseas may be invested overseas through RMB loans, forming an arbitrage investment portfolio of "RMB loans-US dollar assets". If enterprises hold QDII and then hold overseas assets through domestic RMB loans, although it is a legal arbitrage behavior, it may lead to the strengthening of the review of cross-border foreign direct investment and the tightening of quotas.

As for the funds that remain in the country, due to the existence of capital controls, they can only seek assets in the domestic capital market (low volatility, low-risk bond-like assets), such as dividends and government bonds, which leads to arbitrage behavior of funds in the country.

A small part of domestic RMB funds and the behavior of domestic enterprises reflect the trend of RMB lending turning to US dollar assets, some of which may be allocated to US dollar bonds, but a larger amount of funds may flow into high-tech fields such as semiconductors and artificial intelligence. This reflects the mismatch between the lack of RMB investment returns and investment demand, and further reflects the current situation of insufficient effective demand in the economy as a whole.